Key Insights

The UK Insurtech market is projected for substantial growth, driven by increasing digital adoption and demand for personalized, efficient insurance solutions. With an estimated market size of 49.51 billion by 2025, and a Compound Annual Growth Rate (CAGR) of 31.6%, the sector is set for significant expansion. This growth is propelled by the ongoing need for enhanced customer experiences, the integration of AI and machine learning for improved risk assessment and claims processing, and the rising popularity of embedded insurance models. Furthermore, the pursuit of greater transparency and simplified policy management through advanced Insurtech platforms fosters innovation and market penetration. Key segments such as Health and Motor insurance are anticipated to lead this expansion, as consumers increasingly seek flexible, on-demand, and data-driven products tailored to their specific needs and lifestyles.

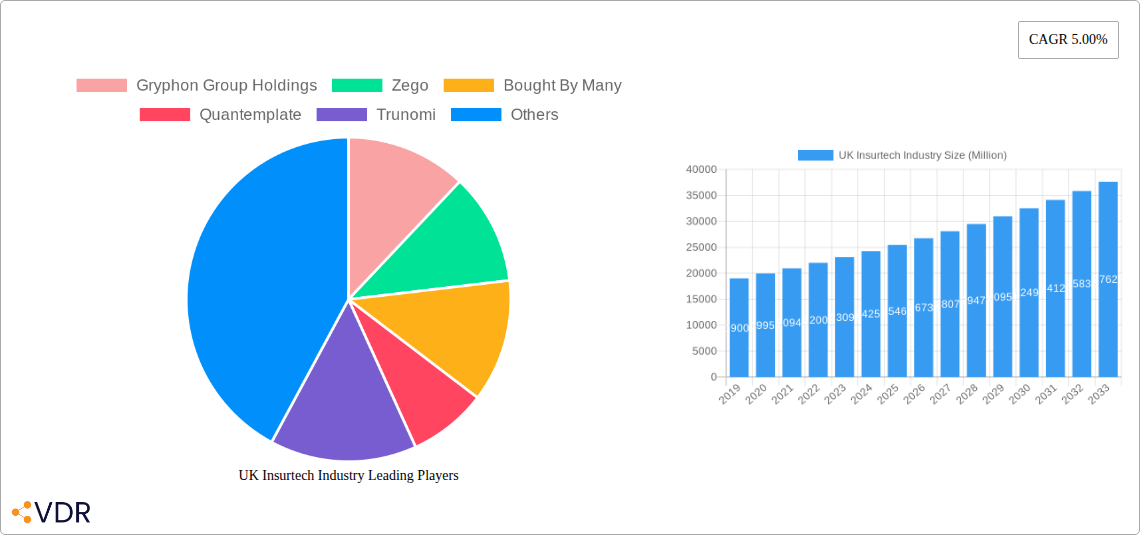

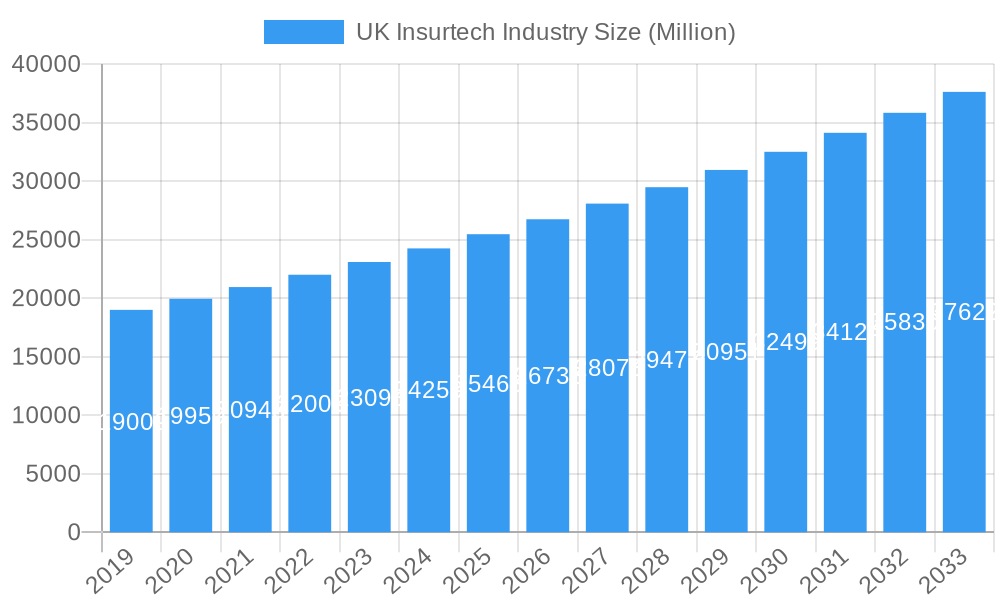

UK Insurtech Industry Market Size (In Billion)

The UK Insurtech landscape is characterized by a dynamic interplay between established insurers and agile startups, fostering intense competition and continuous innovation. While digital channel adoption and advanced analytics offer significant growth opportunities, challenges such as evolving regulatory frameworks, the critical need for robust data security and privacy, and overcoming traditional consumer inertia towards digital insurance products persist. Nevertheless, the overarching trend indicates Insurtech evolving from a supplementary service to an integral component of the insurance value chain, transforming policy design, distribution, and management. Emerging trends like parametric insurance and specialized insurtech solutions for niche markets will further diversify and accelerate market trajectory, solidifying the UK's position as a global hub for insurtech innovation.

UK Insurtech Industry Company Market Share

Report Title: UK Insurtech Market Analysis & Forecast (2025-2033)

Report Description:

This comprehensive report offers an in-depth analysis of the UK Insurtech Industry's market dynamics, growth trajectory, and future potential. Utilizing high-impact SEO keywords and a clear, structured format, this report serves as an essential resource for industry professionals, investors, and strategists. It meticulously examines key segments, product innovations, and the competitive landscape, providing actionable insights for navigating this rapidly evolving sector. Market values are presented in billions of USD for clarity.

UK Insurtech Industry Market Dynamics & Structure

The UK Insurtech market is characterized by a moderate level of concentration, with a growing number of innovative startups challenging established players. Technological innovation, driven by advancements in AI, machine learning, and blockchain, is a primary catalyst for market evolution. Regulatory frameworks, particularly those from the Financial Conduct Authority (FCA), are continuously adapting to foster innovation while ensuring consumer protection. Competitive product substitutes, ranging from traditional insurance offerings to embedded insurance solutions, are shaping consumer choices. End-user demographics are increasingly tech-savvy, demanding personalized, convenient, and transparent insurance products. Mergers and acquisitions (M&A) activity is on the rise as larger insurers seek to integrate insurtech capabilities and startups aim for scalability.

- Market Concentration: Moderate, with increasing fragmentation due to new entrants.

- Technological Innovation Drivers: AI, ML, Big Data Analytics, Blockchain, IoT.

- Regulatory Frameworks: FCA initiatives, Open Insurance, Data Protection regulations.

- Competitive Product Substitutes: Embedded insurance, Pay-as-you-go models, Insured by tech platforms.

- End-User Demographics: Digitally native millennials and Gen Z, seeking seamless digital experiences.

- M&A Trends: Strategic acquisitions for technology integration and market expansion, with an estimated XX deal volumes in the historical period.

UK Insurtech Industry Growth Trends & Insights

The UK Insurtech industry is poised for substantial growth, driven by increasing digital adoption and evolving consumer expectations. The market size is projected to expand significantly from XX Million in 2019 to an estimated XXXX Million by 2033. Key growth drivers include the demand for personalized insurance products, the efficiency gains offered by automation, and the potential for enhanced customer experiences through data-driven insights. Adoption rates for insurtech solutions are climbing across all insurance segments, with motor and health insurance leading the charge. Technological disruptions, such as the integration of IoT devices for risk assessment and the use of AI for claims processing, are revolutionizing operational efficiency and customer engagement. Consumer behavior shifts towards self-service platforms, on-demand policies, and value-added services are further accelerating the adoption of insurtech. The Compound Annual Growth Rate (CAGR) is anticipated to be in the range of XX% over the forecast period. Market penetration is expected to increase from XX% in 2019 to an estimated XX% by 2033.

Dominant Regions, Countries, or Segments in UK Insurtech Industry

Within the UK Insurtech Industry, the Non-Life insurance segment, particularly Motor and House insurance, currently dominates market growth. This dominance is attributed to the higher frequency of claims in these categories, creating a greater imperative for efficient and innovative claims handling and underwriting processes. The adoption of telematics in motor insurance, for instance, has significantly improved risk assessment and pricing, while smart home technology is beginning to influence house insurance. The Health insurance segment is also witnessing significant insurtech advancements, focusing on preventative care and personalized wellness programs, indicating strong future growth potential.

- Dominant Segments:

- Non-Life:

- Motor Insurance: Driven by telematics, usage-based insurance, and advanced claims management. Estimated market share of XX% within insurtech.

- House Insurance: Benefiting from IoT integration for property monitoring and smart home technologies. Estimated market share of XX%.

- Accident Insurance: Emerging with micro-insurance and on-demand policy options.

- Health Insurance: Rapidly evolving with personalized wellness programs, remote diagnostics, and preventative care solutions. Strong growth potential.

- Others: Including travel, pet, and cyber insurance, showing niche growth.

- Non-Life:

- Dominance Factors:

- Technological Adoption: Higher integration of AI, IoT, and data analytics in Motor and House insurance.

- Consumer Demand: Increasing preference for flexible, digital, and personalized policies in these segments.

- Regulatory Support: Initiatives encouraging innovation in frequently purchased insurance types.

- Data Availability: Rich datasets available for underwriting and risk modeling in Motor and House insurance.

UK Insurtech Industry Product Landscape

The UK Insurtech product landscape is characterized by a surge in innovative offerings designed to enhance customer experience and operational efficiency. Products are increasingly leveraging AI for personalized underwriting and claims automation, Big Data for sophisticated risk assessment, and blockchain for enhanced transparency and security. Notable innovations include usage-based insurance (UBI) for motor, on-demand policies for various life events, and parametric insurance solutions that trigger payouts automatically based on predefined conditions. These advancements lead to competitive pricing, faster claims settlement, and a more tailored approach to risk management, setting new benchmarks for the industry.

Key Drivers, Barriers & Challenges in UK Insurtech Industry

Key Drivers:

- Technological Advancements: AI, ML, Big Data, and IoT are enabling data-driven insights, automation, and personalized offerings.

- Consumer Demand for Digitalization: Growing preference for seamless online experiences, self-service options, and on-demand policies.

- Regulatory Support for Innovation: Initiatives like Open Insurance and sandboxes encourage new business models and technologies.

- Efficiency and Cost Reduction: Insurtech solutions streamline operations, reduce overheads, and improve claims processing efficiency.

Barriers & Challenges:

- Regulatory Hurdles: Evolving regulatory landscapes can create compliance complexities and slow down innovation.

- Data Security and Privacy Concerns: Protecting sensitive customer data is paramount and requires robust cybersecurity measures.

- Customer Trust and Adoption: Overcoming skepticism towards new technologies and ensuring a smooth transition for traditional insurance users.

- Legacy System Integration: Integrating new insurtech platforms with existing, often outdated, IT infrastructure of established insurers.

- Talent Shortage: A lack of skilled professionals in data science, AI, and cybersecurity within the insurtech domain.

- Market Competition: Intense competition from both established players and emerging insurtech startups, with XX new entrants in the historical period.

Emerging Opportunities in UK Insurtech Industry

Emerging opportunities in the UK Insurtech industry lie in the expansion of embedded insurance solutions within non-financial platforms, the development of hyper-personalized insurance products leveraging AI and IoT, and the growth of parametric insurance for climate-related risks. Untapped markets in micro-insurance for gig economy workers and the underserved elderly population also present significant potential. Furthermore, the increasing focus on ESG (Environmental, Social, and Governance) factors creates opportunities for developing sustainable and socially responsible insurance products. The demand for advanced cybersecurity insurance is also expected to surge with the growing threat landscape, creating a market segment estimated at XX Million.

Growth Accelerators in the UK Insurtech Industry Industry

Several factors are accelerating growth in the UK Insurtech Industry. Technological breakthroughs in AI for predictive analytics and personalized pricing, coupled with the widespread adoption of IoT devices for real-time risk monitoring, are fundamental accelerators. Strategic partnerships between insurtech startups and traditional insurers facilitate broader market reach and access to capital. The ongoing digital transformation across all sectors of the economy encourages the integration of insurance services at the point of need. Furthermore, regulatory sandboxes provide a controlled environment for testing and scaling innovative solutions, fostering a more dynamic and competitive market.

Key Players Shaping the UK Insurtech Industry Market

- Gryphon Group Holdings

- Zego

- Bought By Many

- Quantemplate

- Trunomi

- Anorak Technologies

- Wrisk

- Cazana

- Setoo

- By Miles

- Other

Notable Milestones in UK Insurtech Industry Sector

- 2019: Significant growth in seed funding for insurtech startups focusing on AI and data analytics.

- 2020: Increased adoption of digital claims processing and remote customer service due to global events.

- 2021: Expansion of embedded insurance models in e-commerce and travel sectors.

- 2022: Launch of several insurtech platforms targeting niche markets like pet and cyber insurance.

- 2023: Major insurers initiate strategic investments and acquisitions of innovative insurtech firms.

- 2024 (Estimated): Continued consolidation and focus on profitability within the insurtech ecosystem.

- 2025 (Projected): Greater integration of generative AI for customer service and product development.

In-Depth UK Insurtech Industry Market Outlook

The UK Insurtech industry is set for robust future growth, driven by a confluence of technological innovation, evolving consumer preferences, and supportive regulatory environments. Growth accelerators, including advanced AI for personalized risk management and the expanding ecosystem of embedded insurance, will continue to fuel expansion. Strategic partnerships and market expansion initiatives by key players will broaden the reach of insurtech solutions. The market is projected to witness a CAGR of XX% from 2025 to 2033, reaching an estimated XXXX Million. Opportunities abound in underserved segments and in leveraging data for proactive risk mitigation, positioning the UK as a global leader in insurtech innovation.

UK Insurtech Industry Segmentation

-

1. Insurance type

- 1.1. Life

-

1.2. Non-Life

- 1.2.1. Motor

- 1.2.2. House

- 1.2.3. Accident

- 1.2.4. Health

- 1.2.5. Others

UK Insurtech Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

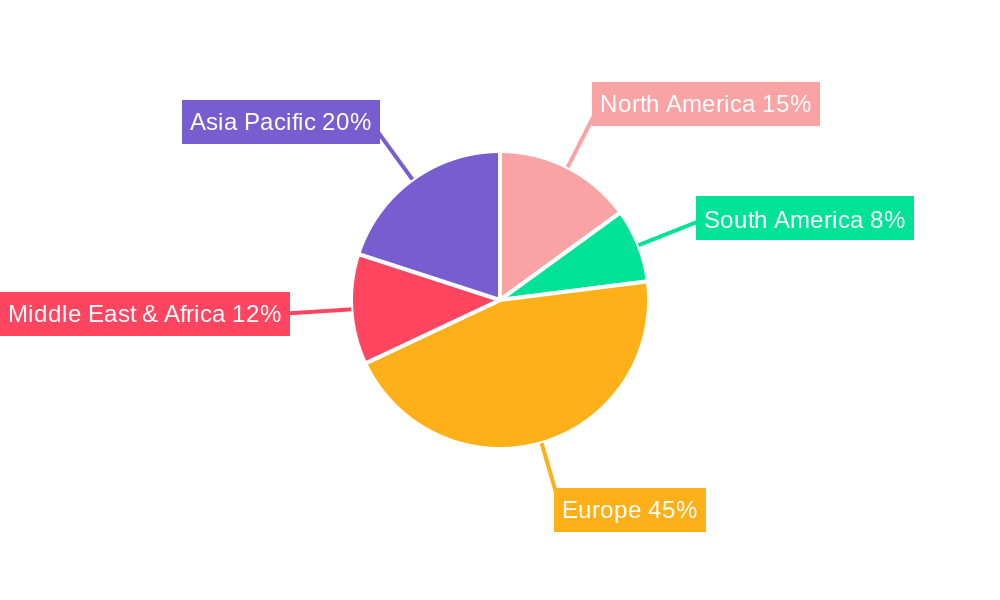

UK Insurtech Industry Regional Market Share

Geographic Coverage of UK Insurtech Industry

UK Insurtech Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 31.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Insurance type

- 5.1.1. Life

- 5.1.2. Non-Life

- 5.1.2.1. Motor

- 5.1.2.2. House

- 5.1.2.3. Accident

- 5.1.2.4. Health

- 5.1.2.5. Others

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. North America

- 5.2.2. South America

- 5.2.3. Europe

- 5.2.4. Middle East & Africa

- 5.2.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Insurance type

- 6. Global UK Insurtech Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Insurance type

- 6.1.1. Life

- 6.1.2. Non-Life

- 6.1.2.1. Motor

- 6.1.2.2. House

- 6.1.2.3. Accident

- 6.1.2.4. Health

- 6.1.2.5. Others

- 6.1. Market Analysis, Insights and Forecast - by Insurance type

- 7. North America UK Insurtech Industry Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Insurance type

- 7.1.1. Life

- 7.1.2. Non-Life

- 7.1.2.1. Motor

- 7.1.2.2. House

- 7.1.2.3. Accident

- 7.1.2.4. Health

- 7.1.2.5. Others

- 7.1. Market Analysis, Insights and Forecast - by Insurance type

- 8. South America UK Insurtech Industry Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Insurance type

- 8.1.1. Life

- 8.1.2. Non-Life

- 8.1.2.1. Motor

- 8.1.2.2. House

- 8.1.2.3. Accident

- 8.1.2.4. Health

- 8.1.2.5. Others

- 8.1. Market Analysis, Insights and Forecast - by Insurance type

- 9. Europe UK Insurtech Industry Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Insurance type

- 9.1.1. Life

- 9.1.2. Non-Life

- 9.1.2.1. Motor

- 9.1.2.2. House

- 9.1.2.3. Accident

- 9.1.2.4. Health

- 9.1.2.5. Others

- 9.1. Market Analysis, Insights and Forecast - by Insurance type

- 10. Middle East & Africa UK Insurtech Industry Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Insurance type

- 10.1.1. Life

- 10.1.2. Non-Life

- 10.1.2.1. Motor

- 10.1.2.2. House

- 10.1.2.3. Accident

- 10.1.2.4. Health

- 10.1.2.5. Others

- 10.1. Market Analysis, Insights and Forecast - by Insurance type

- 11. Asia Pacific UK Insurtech Industry Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Insurance type

- 11.1.1. Life

- 11.1.2. Non-Life

- 11.1.2.1. Motor

- 11.1.2.2. House

- 11.1.2.3. Accident

- 11.1.2.4. Health

- 11.1.2.5. Others

- 11.1. Market Analysis, Insights and Forecast - by Insurance type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Gryphon Group Holdings

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Zego

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Bought By Many

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Quantemplate

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Trunomi

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Anorak Technologies

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Wrisk

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Cazana

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Setoo

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 By Miles

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Other

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.1 Gryphon Group Holdings

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global UK Insurtech Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America UK Insurtech Industry Revenue (billion), by Insurance type 2025 & 2033

- Figure 3: North America UK Insurtech Industry Revenue Share (%), by Insurance type 2025 & 2033

- Figure 4: North America UK Insurtech Industry Revenue (billion), by Country 2025 & 2033

- Figure 5: North America UK Insurtech Industry Revenue Share (%), by Country 2025 & 2033

- Figure 6: South America UK Insurtech Industry Revenue (billion), by Insurance type 2025 & 2033

- Figure 7: South America UK Insurtech Industry Revenue Share (%), by Insurance type 2025 & 2033

- Figure 8: South America UK Insurtech Industry Revenue (billion), by Country 2025 & 2033

- Figure 9: South America UK Insurtech Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe UK Insurtech Industry Revenue (billion), by Insurance type 2025 & 2033

- Figure 11: Europe UK Insurtech Industry Revenue Share (%), by Insurance type 2025 & 2033

- Figure 12: Europe UK Insurtech Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: Europe UK Insurtech Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Middle East & Africa UK Insurtech Industry Revenue (billion), by Insurance type 2025 & 2033

- Figure 15: Middle East & Africa UK Insurtech Industry Revenue Share (%), by Insurance type 2025 & 2033

- Figure 16: Middle East & Africa UK Insurtech Industry Revenue (billion), by Country 2025 & 2033

- Figure 17: Middle East & Africa UK Insurtech Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Pacific UK Insurtech Industry Revenue (billion), by Insurance type 2025 & 2033

- Figure 19: Asia Pacific UK Insurtech Industry Revenue Share (%), by Insurance type 2025 & 2033

- Figure 20: Asia Pacific UK Insurtech Industry Revenue (billion), by Country 2025 & 2033

- Figure 21: Asia Pacific UK Insurtech Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global UK Insurtech Industry Revenue billion Forecast, by Insurance type 2020 & 2033

- Table 2: Global UK Insurtech Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 3: Global UK Insurtech Industry Revenue billion Forecast, by Insurance type 2020 & 2033

- Table 4: Global UK Insurtech Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 5: United States UK Insurtech Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 6: Canada UK Insurtech Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 7: Mexico UK Insurtech Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Global UK Insurtech Industry Revenue billion Forecast, by Insurance type 2020 & 2033

- Table 9: Global UK Insurtech Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 10: Brazil UK Insurtech Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Argentina UK Insurtech Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Rest of South America UK Insurtech Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Global UK Insurtech Industry Revenue billion Forecast, by Insurance type 2020 & 2033

- Table 14: Global UK Insurtech Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 15: United Kingdom UK Insurtech Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Germany UK Insurtech Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: France UK Insurtech Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Italy UK Insurtech Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 19: Spain UK Insurtech Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Russia UK Insurtech Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: Benelux UK Insurtech Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Nordics UK Insurtech Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Rest of Europe UK Insurtech Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Global UK Insurtech Industry Revenue billion Forecast, by Insurance type 2020 & 2033

- Table 25: Global UK Insurtech Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 26: Turkey UK Insurtech Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Israel UK Insurtech Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: GCC UK Insurtech Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 29: North Africa UK Insurtech Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: South Africa UK Insurtech Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 31: Rest of Middle East & Africa UK Insurtech Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Global UK Insurtech Industry Revenue billion Forecast, by Insurance type 2020 & 2033

- Table 33: Global UK Insurtech Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 34: China UK Insurtech Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: India UK Insurtech Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Japan UK Insurtech Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: South Korea UK Insurtech Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: ASEAN UK Insurtech Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 39: Oceania UK Insurtech Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 40: Rest of Asia Pacific UK Insurtech Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the UK Insurtech Industry?

The projected CAGR is approximately 31.6%.

2. Which companies are prominent players in the UK Insurtech Industry?

Key companies in the market include Gryphon Group Holdings, Zego, Bought By Many, Quantemplate, Trunomi, Anorak Technologies, Wrisk, Cazana, Setoo, By Miles, Other.

3. What are the main segments of the UK Insurtech Industry?

The market segments include Insurance type.

4. Can you provide details about the market size?

The market size is estimated to be USD 49.51 billion as of 2022.

5. What are some drivers contributing to market growth?

; Customer Acquisition; Customer Retention; Risk Assessment; Fraud Prevention and Detection; Others.

6. What are the notable trends driving market growth?

INSURTECHS FOCUS ON ANALYTICS / BIG DATA and AI.

7. Are there any restraints impacting market growth?

; Customer Acquisition; Customer Retention; Risk Assessment; Fraud Prevention and Detection; Others.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "UK Insurtech Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the UK Insurtech Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the UK Insurtech Industry?

To stay informed about further developments, trends, and reports in the UK Insurtech Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence