Key Insights

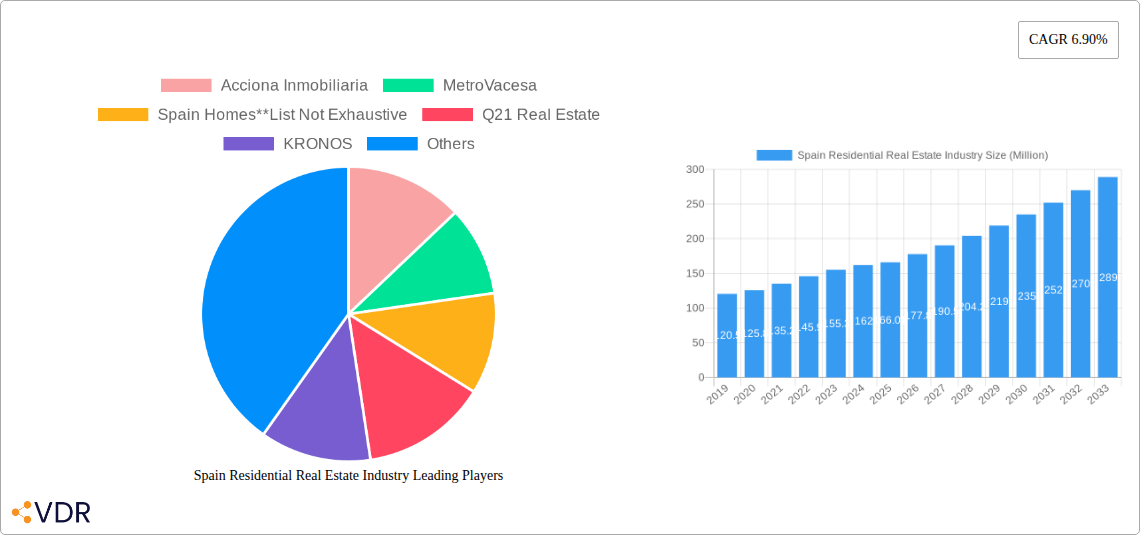

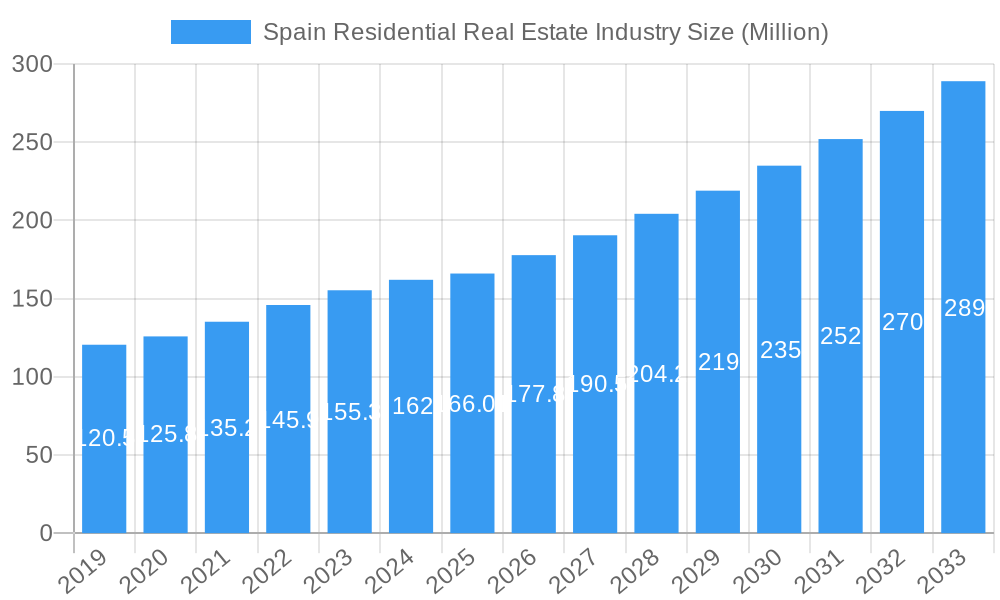

The Spanish residential real estate market is poised for robust expansion, projected to reach approximately USD 166.01 million by 2025, with a compelling Compound Annual Growth Rate (CAGR) of 6.90% expected to sustain this momentum through 2033. This growth is significantly driven by a confluence of economic recovery, favorable interest rates, and a persistent demand for housing, particularly in key urban centers. The market is experiencing a dynamic shift in property types, with apartments and condominiums witnessing substantial interest due to urbanization and lifestyle preferences, while villas and landed houses continue to attract buyers seeking space and exclusivity. Major cities like Madrid, Barcelona, and Valencia are at the forefront of this expansion, benefiting from strong economic activity, job creation, and a burgeoning tourism sector that fuels rental demand. The sustained interest from both domestic and international buyers underscores the inherent attractiveness of Spanish property as a stable investment and a desirable lifestyle choice.

Spain Residential Real Estate Industry Market Size (In Million)

While the market demonstrates strong growth prospects, certain factors warrant attention. The primary drivers are sustained economic stability, an increase in household disposable income, and supportive government policies aimed at promoting homeownership. Emerging trends include a growing preference for sustainable and energy-efficient homes, the continued rise of proptech solutions enhancing property discovery and transactions, and a revitalized interest in second-home ownership. However, potential restraints such as rising construction costs, a shortage of skilled labor in the construction sector, and evolving regulatory landscapes could temper the pace of growth. Nevertheless, the underlying demand, coupled with strategic investments from key players like Acciona Inmobiliaria, MetroVacesa, and Neinor Homes, suggests a resilient and dynamic market. The focus on diverse property segments and strategic expansion across key regions positions the Spanish residential real estate industry for sustained success in the coming years.

Spain Residential Real Estate Industry Company Market Share

Spain Residential Real Estate Industry Report: Market Dynamics, Growth Outlook, and Key Player Analysis (2019-2033)

This comprehensive report offers an in-depth analysis of the Spain Residential Real Estate Industry, providing critical insights for industry professionals, investors, and stakeholders. Delving into market dynamics, growth trends, regional dominance, and key players, this report covers the period from 2019 to 2033, with a base year of 2025. Utilizing high-traffic keywords and a structured format, it maximizes search engine visibility and delivers actionable intelligence. Our analysis includes parent and child market perspectives, with all values presented in Million units for clarity.

Spain Residential Real Estate Industry Market Dynamics & Structure

The Spanish residential real estate market is characterized by a moderate level of concentration, with larger developers like Acciona Inmobiliaria and MetroVacesa holding significant sway, yet ample space for agile players such as Spain Homes and Q21 Real Estate. Technological innovation is a growing driver, particularly in sustainable building practices and proptech solutions, though adoption barriers persist due to upfront investment costs and a traditionally conservative industry. Regulatory frameworks, including evolving urban planning laws and foreign investment incentives, significantly shape market accessibility and development. Competitive product substitutes are primarily other asset classes like commercial real estate or international property markets, influencing investor allocation. End-user demographics are increasingly shaped by a growing population of remote workers, a rising demand for energy-efficient homes, and an aging demographic requiring specialized housing solutions. Mergers and acquisitions (M&A) trends are on the rise as larger entities seek to consolidate market share and acquire innovative technologies or prime land assets.

- Market Concentration: Moderate, with key players and emerging developers.

- Technological Drivers: Proptech, sustainable construction, smart home integration.

- Regulatory Impact: Urban planning, foreign investment policies, rental regulations.

- Competitive Landscape: Diversification into other asset classes and international markets.

- End-User Demographics: Young professionals, retirees, families seeking quality housing.

- M&A Activity: Increasing consolidation and strategic acquisitions.

Spain Residential Real Estate Industry Growth Trends & Insights

The Spain Residential Real Estate Industry is poised for robust growth, driven by sustained economic recovery, favorable interest rate environments, and a persistent undersupply of quality housing in prime locations. The market size is projected to witness a healthy Compound Annual Growth Rate (CAGR) over the forecast period, reflecting increasing domestic demand and a resurgence in international investor interest. Adoption rates of sustainable building technologies and digital property management solutions are accelerating, indicating a shift towards more efficient and environmentally conscious development. Technological disruptions, such as the integration of AI in property valuation and virtual reality in property tours, are enhancing buyer experiences and streamlining the transaction process. Consumer behavior is evolving, with a greater emphasis on urban regeneration projects, proximity to amenities, and a preference for flexible living spaces that accommodate remote work. The market penetration of Build-to-Rent (BTR) developments is also expanding, catering to a growing rental market.

Dominant Regions, Countries, or Segments in Spain Residential Real Estate Industry

The Apartments and Condominiums segment is a dominant force within the Spain Residential Real Estate Industry, driven by urbanization trends and a strong demand in major cities like Madrid and Barcelona. Catalonia, particularly Barcelona, and the region of Madrid consistently lead market growth due to their economic vitality, international appeal, and robust infrastructure development. Valencia and Malaga are rapidly emerging as significant hubs, attracting both domestic and international buyers with their lifestyle offerings and improving connectivity.

- Key Drivers for Apartments and Condominiums:

- Urbanization: High population density and demand for city living.

- Affordability: Often more accessible price points compared to villas.

- Convenience: Proximity to amenities, transport, and employment centers.

- Dominance Factors in Madrid and Catalonia:

- Economic Hubs: Strong job markets and business opportunities.

- Infrastructure: Well-developed public transportation and international airports.

- Tourism & Investment: High appeal to foreign buyers and investors.

- Market Share: Consistently holding the largest share of residential transactions.

- Emerging Growth in Valencia and Malaga:

- Lifestyle Appeal: Coastal locations, favorable climate, and recreational activities.

- Infrastructure Investment: Expansion of transport networks and urban regeneration.

- Affordability Potential: Offering attractive entry points compared to more established markets.

- Growth Potential: Significant upside for property value appreciation.

Spain Residential Real Estate Industry Product Landscape

The product landscape in the Spain Residential Real Estate Industry is evolving to meet sophisticated consumer demands. Beyond traditional apartments and villas, there is a growing emphasis on energy-efficient designs, smart home integration, and the incorporation of communal amenities like co-working spaces and fitness centers. Developers are increasingly focusing on sustainable materials and construction methods, aligning with environmental regulations and consumer preferences for green living. Innovations in modular construction and prefabricated elements are also being explored to improve build times and cost-efficiency, while maintaining high aesthetic standards.

Key Drivers, Barriers & Challenges in Spain Residential Real Estate Industry

Key Drivers:

- Economic Recovery: A rebounding economy fuels consumer confidence and purchasing power.

- Favorable Interest Rates: Historically low interest rates continue to make mortgages more affordable.

- Foreign Investment: Spain remains an attractive destination for international buyers seeking second homes or investment opportunities.

- Urban Regeneration: Government and private sector initiatives to revitalize urban areas create new housing stock.

Barriers & Challenges:

- Supply Chain Disruptions: Ongoing global supply chain issues can lead to construction delays and increased material costs.

- Regulatory Hurdles: Complex planning permissions and bureaucratic processes can slow down development.

- Rising Construction Costs: Inflationary pressures on materials and labor impact project profitability.

- Affordability Crisis: In prime locations, rising property prices can outpace wage growth, creating affordability challenges for some segments of the population.

Emerging Opportunities in Spain Residential Real Estate Industry

Emerging opportunities lie in the growing demand for Build-to-Rent (BTR) developments, catering to a younger demographic and the increasing transient population. The niche market for senior living and co-housing solutions is also poised for significant growth, driven by an aging population and a desire for community living. Furthermore, the integration of PropTech solutions, from AI-driven property management to blockchain for secure transactions, presents a vast untapped potential for streamlining operations and enhancing customer experience. Sustainable and energy-efficient housing continues to gain traction, creating opportunities for developers specializing in green building certifications and innovative environmental technologies.

Growth Accelerators in the Spain Residential Real Estate Industry Industry

Technological breakthroughs in sustainable construction and smart home automation are key growth accelerators, enhancing the appeal and value of residential properties. Strategic partnerships between developers, construction firms, and PropTech companies are fostering innovation and streamlining development processes. The Spanish government's commitment to promoting foreign investment and providing incentives for sustainable development further bolsters market expansion. Furthermore, the ongoing digitalization of the real estate sector, from virtual tours to online transaction platforms, is increasing market accessibility and efficiency.

Key Players Shaping the Spain Residential Real Estate Industry Market

- Acciona Inmobiliaria

- MetroVacesa

- Spain Homes

- Q21 Real Estate

- KRONOS

- Via Celere

- AELCA

- Neinor Homes

- Pryconsa

- AEDAS Homes

Notable Milestones in Spain Residential Real Estate Industry Sector

- October 2022: Layetana Living and Aviva Investors established a build-to-rent (BTR) cooperation. This collaboration aims to construct a residential portfolio valued at over EUR 500 million (USD 531.20 Million). The partnership secured its first development project, a 71-unit residential building in Barcelona, with construction slated to begin at the end of 2023.

- September 2022: Berkshire Hathaway HomeServices expanded its services in the Valencian Community, opening its fourth facility in 2022 in Denia, under the direction of Maryana Kim.

In-Depth Spain Residential Real Estate Industry Market Outlook

The future outlook for the Spain Residential Real Estate Industry is highly promising, driven by a confluence of factors including ongoing economic resilience, attractive investment conditions, and a continued demand for quality housing. Growth accelerators such as advancements in sustainable building practices, the increasing adoption of PropTech, and strategic international partnerships will continue to propel the market forward. Emerging opportunities in niche segments like Build-to-Rent and senior living, coupled with the potential for urban regeneration projects, indicate a dynamic and evolving market landscape ripe for strategic investment and development.

Spain Residential Real Estate Industry Segmentation

-

1. Type

- 1.1. Apartments and Condominiums

- 1.2. Villas and Landed Houses

-

2. Key Cities

- 2.1. Madrid

- 2.2. Catalonia

- 2.3. Valencia

- 2.4. Barcelona

- 2.5. Malaga

- 2.6. Others

Spain Residential Real Estate Industry Segmentation By Geography

- 1. Spain

Spain Residential Real Estate Industry Regional Market Share

Geographic Coverage of Spain Residential Real Estate Industry

Spain Residential Real Estate Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.90% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Apartments and Condominiums

- 5.1.2. Villas and Landed Houses

- 5.2. Market Analysis, Insights and Forecast - by Key Cities

- 5.2.1. Madrid

- 5.2.2. Catalonia

- 5.2.3. Valencia

- 5.2.4. Barcelona

- 5.2.5. Malaga

- 5.2.6. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Spain

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Spain Residential Real Estate Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Apartments and Condominiums

- 6.1.2. Villas and Landed Houses

- 6.2. Market Analysis, Insights and Forecast - by Key Cities

- 6.2.1. Madrid

- 6.2.2. Catalonia

- 6.2.3. Valencia

- 6.2.4. Barcelona

- 6.2.5. Malaga

- 6.2.6. Others

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Acciona Inmobiliaria

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 MetroVacesa

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Spain Homes**List Not Exhaustive

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Q21 Real Estate

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 KRONOS

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Via Celere

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 AELCA

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Neinor Homes

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Pryconsa

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 AEDAS homes

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Acciona Inmobiliaria

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Spain Residential Real Estate Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Spain Residential Real Estate Industry Share (%) by Company 2025

List of Tables

- Table 1: Spain Residential Real Estate Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 2: Spain Residential Real Estate Industry Revenue Million Forecast, by Key Cities 2020 & 2033

- Table 3: Spain Residential Real Estate Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Spain Residential Real Estate Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 5: Spain Residential Real Estate Industry Revenue Million Forecast, by Key Cities 2020 & 2033

- Table 6: Spain Residential Real Estate Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Spain Residential Real Estate Industry?

The projected CAGR is approximately 6.90%.

2. Which companies are prominent players in the Spain Residential Real Estate Industry?

Key companies in the market include Acciona Inmobiliaria, MetroVacesa, Spain Homes**List Not Exhaustive, Q21 Real Estate, KRONOS, Via Celere, AELCA, Neinor Homes, Pryconsa, AEDAS homes.

3. What are the main segments of the Spain Residential Real Estate Industry?

The market segments include Type, Key Cities.

4. Can you provide details about the market size?

The market size is estimated to be USD 166.01 Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Increasing Number of High Net-Worth Individuals (HNWIs).

6. What are the notable trends driving market growth?

Rise in International Property Buyers in Spain.

7. Are there any restraints impacting market growth?

4.; Rising Interest Rates.

8. Can you provide examples of recent developments in the market?

October 2022: A build-to-rent (BTR) cooperation between Layetana Living and Aviva Investors was established in Spain. According to the statement, the collaboration between Aviva and the Spanish developer Layetana will construct a more than EUR 500 million (USD 531.20 Million) residential portfolio, already securing its first development project. Based on the recommendation of international real estate consultancy Knight Frank, the partnership purchased a 71-unit residential building in Barcelona's Sants neighborhood. Construction is scheduled to begin at the end of 2023.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Spain Residential Real Estate Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Spain Residential Real Estate Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Spain Residential Real Estate Industry?

To stay informed about further developments, trends, and reports in the Spain Residential Real Estate Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence