Key Insights

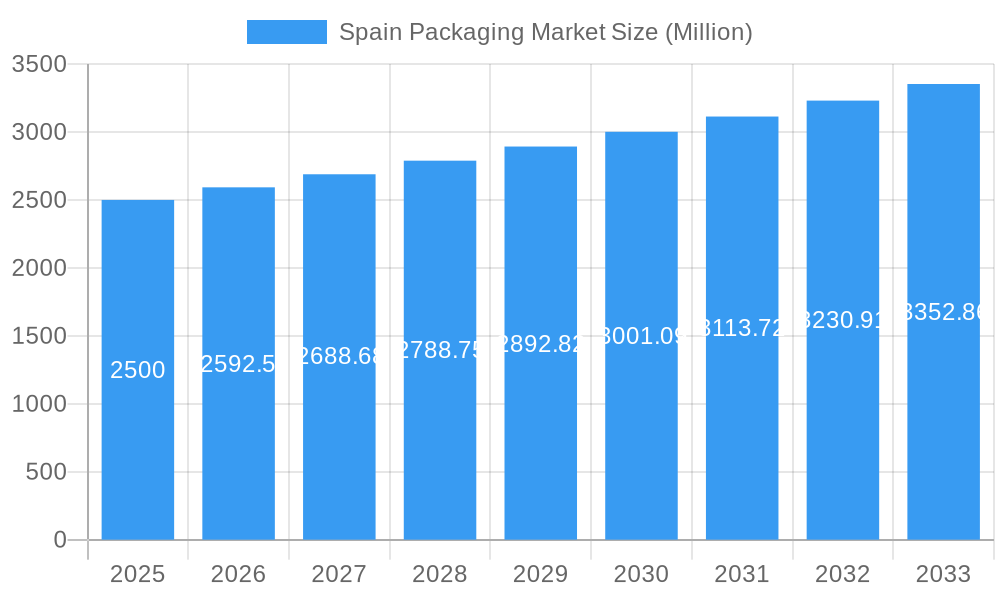

The Spain packaging market, valued at 620 million in 2025, is poised for robust expansion. Driven by escalating demand for packaged goods across the food & beverage, healthcare, and cosmetics industries, the market is projected to achieve a Compound Annual Growth Rate (CAGR) of 7.01% from 2025 to 2033. Key growth drivers include the increasing adoption of sustainable and eco-friendly packaging solutions, the preference for convenient and tamper-evident designs, and the growing demand for bespoke packaging to elevate brand presence. The market is segmented by packaging layers (primary, secondary, tertiary), materials (plastic, flexible packaging, paper, glass, metal), and end-users. The food and beverage sector is anticipated to maintain its position as the largest revenue contributor, followed by healthcare and pharmaceuticals, influenced by rigorous product safety and hygiene regulations. Potential market restraints include fluctuating raw material costs and environmental concerns regarding plastic waste. Prominent market players include Amcor PLC, Berry Global Inc., and Becton Dickinson, who compete through innovation and product portfolio diversification.

Spain Packaging Market Market Size (In Million)

The forecast period (2025-2033) indicates sustained market growth, significantly influenced by the expansion of e-commerce and the resultant need for efficient, durable packaging for online shipments. Growing consumer environmental consciousness is spurring investment in sustainable packaging alternatives, creating opportunities for eco-friendly solution providers. Technological advancements in packaging design and manufacturing are expected to boost efficiency and reduce operational costs, further supporting market expansion. Regional market dynamics within Spain may vary, with urban centers potentially exhibiting higher demand than rural areas, impacting the market's future trajectory. Strategic collaborations and mergers & acquisitions among industry participants are also anticipated to reshape the competitive landscape.

Spain Packaging Market Company Market Share

Spain Packaging Market: A Comprehensive Report (2019-2033)

This comprehensive report provides an in-depth analysis of the Spain packaging market, offering invaluable insights for industry professionals, investors, and strategic decision-makers. The report covers the period 2019-2033, with a focus on the forecast period 2025-2033, and utilizes 2025 as the base year. The market is segmented by layers of packing (primary, secondary, tertiary), packaging material (plastic, flexible packaging, paper, glass, metal), and end-users (food & beverage, healthcare & pharmaceutical, beauty & personal care, industrial, other). Key players like Becton Dickinson and Company (BD), Ball Corporation, Crown Holdings Inc, and Amcor PLC are analyzed in detail. The market size is expressed in million units.

Spain Packaging Market Dynamics & Structure

The Spain packaging market is characterized by moderate concentration, with several major players holding significant market share. Technological innovation, driven by sustainability concerns and evolving consumer preferences, is a key driver. Stringent regulatory frameworks regarding material composition and recyclability influence packaging choices. Competition from substitute materials like biodegradable options is increasing. The end-user demographics exhibit a shift towards eco-conscious consumers. M&A activity has been moderate in recent years, with notable deals impacting market consolidation.

- Market Concentration: xx% held by top 5 players in 2024.

- Technological Innovation: Focus on sustainable and recyclable materials, automation in production processes.

- Regulatory Framework: Emphasis on reducing plastic waste and promoting circular economy principles.

- Competitive Substitutes: Biodegradable and compostable packaging materials are gaining traction.

- End-User Demographics: Growing demand for convenience packaging and eco-friendly solutions.

- M&A Trends: xx M&A deals concluded in the period 2019-2024, primarily focused on expansion and technological acquisition.

Spain Packaging Market Growth Trends & Insights

The Spain packaging market is experiencing steady growth, driven by robust economic activity, increasing consumer spending, and the growth of various end-use sectors. The market size expanded from xx million units in 2019 to xx million units in 2024, exhibiting a CAGR of xx%. This growth is anticipated to continue, with a projected CAGR of xx% from 2025 to 2033, reaching xx million units by 2033. Technological disruptions, including the adoption of smart packaging and automation, are reshaping the industry landscape. Consumer behavior shifts towards sustainability and convenience are also influencing packaging choices. Market penetration of sustainable packaging materials is gradually increasing, with expectations of xx% penetration by 2033.

Dominant Regions, Countries, or Segments in Spain Packaging Market

The Spanish packaging market is characterized by its regional distribution, mirroring economic powerhouses and population centers. Key segments are driven by robust consumer demand and evolving industry needs. The Food & Beverage sector unequivocally holds the largest market share, a testament to Spain's strong gastronomic culture and continuous consumption. This dominance is further amplified by the demand for a wide array of packaging solutions that ensure product integrity, extend shelf life, and enhance consumer appeal. While plastic continues to be a prevalent material due to its inherent cost-effectiveness, remarkable versatility, and functional properties, there is a noticeable and growing trend towards exploring and adopting more sustainable alternatives. Within the packaging layers, primary packaging, which directly interacts with the product, remains the most significant segment, essential for product protection and branding.

- By Layers of Packing: Primary packaging continues to be the largest segment, accounting for an estimated XX% of the market share. This is closely followed by secondary packaging (estimated XX%), which bundles primary packages, and tertiary packaging (estimated XX%), used for shipping and logistics.

- By Packaging Material: Plastic remains the dominant material, capturing an estimated XX% of the market share, driven by its widespread application in food, beverage, and personal care products. Flexible packaging, offering adaptability and branding opportunities, follows with an estimated XX%. Paper and paperboard (estimated XX%) are significant, particularly in secondary and tertiary packaging. Metal packaging (estimated XX%) is crucial for beverages and certain food items, while glass packaging (estimated XX%) retains its appeal for premium products and specific applications.

- By End Users: The Food & Beverage sector is the leading end-user, commanding an impressive XX% of the market share due to consistent high-volume consumption and diverse packaging requirements. The Healthcare & Pharmaceutical sector (estimated XX%) is a critical and growing segment, demanding sterile and secure packaging. The Beauty & Personal Care sector (estimated XX%) relies heavily on innovative and visually appealing packaging. Industrial packaging (estimated XX%) and a range of other end users (estimated XX%) contribute to the overall market diversity.

- Key Drivers: Several factors are propelling the Spain packaging market forward. These include the escalating demand across all major end-user industries, a consistent rise in consumer spending power, and supportive government initiatives aimed at fostering innovation and sustainability within the packaging sector. Evolving consumer preferences towards convenience and premiumization also play a crucial role.

Spain Packaging Market Product Landscape

The Spanish packaging market is characterized by a dynamic and evolving product landscape, driven by continuous innovation in materials, design, and functionality. A significant trend is the growing prominence of sustainable packaging solutions. This encompasses the increased use of recycled content in various materials and the exploration of biodegradable and compostable alternatives, directly responding to both consumer demand for eco-friendly options and stringent regulatory frameworks aimed at reducing environmental impact. Furthermore, the adoption of smart packaging technologies is on the rise. These advanced solutions incorporate features such as tamper-evidence, providing enhanced product security and consumer trust, as well as track-and-trace capabilities, which are invaluable for supply chain management and product authentication, particularly in sensitive sectors like pharmaceuticals. These innovations are fundamentally driven by the pursuit of improved performance metrics, including superior barrier properties for extended product shelf life, enhanced recyclability to close material loops, and optimized product protection throughout the distribution chain.

Key Drivers, Barriers & Challenges in Spain Packaging Market

Key Drivers:

- Growth in e-commerce driving demand for protective and convenient packaging.

- Increased focus on brand building through innovative packaging designs.

- Government regulations promoting sustainable and recyclable packaging options.

Key Challenges:

- Fluctuating raw material prices impacting packaging costs.

- Supply chain disruptions impacting availability and delivery timelines.

- Stringent environmental regulations increasing compliance costs.

Emerging Opportunities in Spain Packaging Market

The market presents exciting opportunities related to sustainable packaging, particularly bioplastics and compostable alternatives. The growing demand for convenient and personalized packaging creates opportunities for innovative formats and designs. E-commerce continues to drive demand for secure and protective packaging solutions, presenting a significant market opportunity.

Growth Accelerators in the Spain Packaging Market Industry

The Spain packaging market is experiencing accelerated growth fueled by a confluence of technological advancements, strategic collaborations, and supportive policy environments. Cutting-edge technological advancements, particularly in automation within manufacturing processes and the development of advanced, high-performance materials, are significantly boosting efficiency and enabling the creation of novel packaging solutions. Strategic partnerships and collaborations between packaging manufacturers, material suppliers, and consumer brands are instrumental in driving innovation, streamlining product development cycles, and expanding market reach. Furthermore, government incentives and proactive initiatives specifically promoting the adoption of sustainable packaging practices are creating a fertile ground for growth and encouraging investment in eco-friendly technologies. The exponential expansion of the e-commerce sector represents another substantial growth catalyst. The unique demands of online retail, requiring robust, protective, and often space-efficient packaging, are stimulating the development of specialized packaging solutions, thereby significantly contributing to the overall market expansion.

Key Players Shaping the Spain Packaging Market Market

Notable Milestones in Spain Packaging Market Sector

- November 2022: Plastipak opened a new PET recycling plant in Toledo, Spain, with an annual capacity of 20,000 tonnes of food-grade rPET pellets. This significantly boosts the availability of recycled PET material for packaging.

- November 2022: Smurfit Kappa acquired Pusa Pack, expanding its bag-in-box packaging capacity and enhancing its ability to meet growing market demands.

In-Depth Spain Packaging Market Market Outlook

The Spain packaging market is poised for continued growth, driven by sustainability trends, technological advancements, and the expansion of key end-use sectors. Strategic investments in sustainable packaging solutions and partnerships will play a vital role in shaping the market's future. Companies focused on innovation and sustainability are well-positioned to capitalize on the market's potential, especially within the rapidly expanding e-commerce sector.

Spain Packaging Market Segmentation

-

1. Layers of Packing

- 1.1. Primary

- 1.2. Secondary & Tertiary

-

2. Packaging Material

-

2.1. Plastic

- 2.1.1. Rigid Packaging

- 2.1.2. Flexible Packaging

- 2.2. Paper

- 2.3. Glass

- 2.4. Metal

-

2.1. Plastic

-

3. End Users

- 3.1. Food & Beverage

- 3.2. Healthcare & Pharmaceutical

- 3.3. Beauty & Personal Care

- 3.4. Industrial

- 3.5. Other End Users

Spain Packaging Market Segmentation By Geography

- 1. Spain

Spain Packaging Market Regional Market Share

Geographic Coverage of Spain Packaging Market

Spain Packaging Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.01% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Layers of Packing

- 5.1.1. Primary

- 5.1.2. Secondary & Tertiary

- 5.2. Market Analysis, Insights and Forecast - by Packaging Material

- 5.2.1. Plastic

- 5.2.1.1. Rigid Packaging

- 5.2.1.2. Flexible Packaging

- 5.2.2. Paper

- 5.2.3. Glass

- 5.2.4. Metal

- 5.2.1. Plastic

- 5.3. Market Analysis, Insights and Forecast - by End Users

- 5.3.1. Food & Beverage

- 5.3.2. Healthcare & Pharmaceutical

- 5.3.3. Beauty & Personal Care

- 5.3.4. Industrial

- 5.3.5. Other End Users

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Spain

- 5.1. Market Analysis, Insights and Forecast - by Layers of Packing

- 6. Spain Packaging Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Layers of Packing

- 6.1.1. Primary

- 6.1.2. Secondary & Tertiary

- 6.2. Market Analysis, Insights and Forecast - by Packaging Material

- 6.2.1. Plastic

- 6.2.1.1. Rigid Packaging

- 6.2.1.2. Flexible Packaging

- 6.2.2. Paper

- 6.2.3. Glass

- 6.2.4. Metal

- 6.2.1. Plastic

- 6.3. Market Analysis, Insights and Forecast - by End Users

- 6.3.1. Food & Beverage

- 6.3.2. Healthcare & Pharmaceutical

- 6.3.3. Beauty & Personal Care

- 6.3.4. Industrial

- 6.3.5. Other End Users

- 6.1. Market Analysis, Insights and Forecast - by Layers of Packing

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Becton Dickinson and Company (BD)

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Ball Corporation

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Crown Holdings Inc

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Quadpack Industries SA

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Amcor PLC

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Agrado SA

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 International Paper Company

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Coveris Holdings

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Berry Global Inc

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Sealed Air Corporation

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Becton Dickinson and Company (BD)

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Spain Packaging Market Revenue Breakdown (million, %) by Product 2025 & 2033

- Figure 2: Spain Packaging Market Share (%) by Company 2025

List of Tables

- Table 1: Spain Packaging Market Revenue million Forecast, by Layers of Packing 2020 & 2033

- Table 2: Spain Packaging Market Revenue million Forecast, by Packaging Material 2020 & 2033

- Table 3: Spain Packaging Market Revenue million Forecast, by End Users 2020 & 2033

- Table 4: Spain Packaging Market Revenue million Forecast, by Region 2020 & 2033

- Table 5: Spain Packaging Market Revenue million Forecast, by Layers of Packing 2020 & 2033

- Table 6: Spain Packaging Market Revenue million Forecast, by Packaging Material 2020 & 2033

- Table 7: Spain Packaging Market Revenue million Forecast, by End Users 2020 & 2033

- Table 8: Spain Packaging Market Revenue million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Spain Packaging Market?

The projected CAGR is approximately 7.01%.

2. Which companies are prominent players in the Spain Packaging Market?

Key companies in the market include Becton Dickinson and Company (BD), Ball Corporation, Crown Holdings Inc, Quadpack Industries SA, Amcor PLC, Agrado SA, International Paper Company, Coveris Holdings, Berry Global Inc, Sealed Air Corporation.

3. What are the main segments of the Spain Packaging Market?

The market segments include Layers of Packing, Packaging Material, End Users.

4. Can you provide details about the market size?

The market size is estimated to be USD 620 million as of 2022.

5. What are some drivers contributing to market growth?

Growing Demand from the Food & Pharmaceutical Sectors; Rising Demand for Small and Convenient Packaging.

6. What are the notable trends driving market growth?

Surging Demand For Packaging in Food and Beverage Industry.

7. Are there any restraints impacting market growth?

Stringent Rules and Regulations on Packaging Materials.

8. Can you provide examples of recent developments in the market?

November 2022: Plastipak opened a new PET recycling plant at its Toledo, Spain, manufacturing location. The recycling plant would ensure that PET flake is converted into food-grade recycled PET (rPET) pellets for use in bottles, new preforms, and containers at the new recycling facility. The recycling factory, which was scheduled to begin operations in the summer of 2022, is planned to produce 20,000 Tonnes of food-grade pellets per year.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Spain Packaging Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Spain Packaging Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Spain Packaging Market?

To stay informed about further developments, trends, and reports in the Spain Packaging Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence