Key Insights

The Saudi Arabian solar energy industry is poised for exceptional growth, with a projected market size of $8.3 billion in 2025, driven by ambitious national renewable energy targets and substantial government investment. The sector is experiencing a remarkable 37.39% CAGR, indicating a rapid expansion that will reshape the energy landscape. This surge is underpinned by strong government support through initiatives like Vision 2030, which aims to diversify the economy away from oil and significantly increase the share of renewable energy in the power generation mix. Key drivers include the declining cost of solar technology, the nation's abundant solar irradiation, and the growing demand for clean energy to meet rising electricity consumption. The market is segmented primarily into Solar Photovoltaic (PV) and Concentrated Solar Power (CSP) technologies, with PV expected to dominate due to its widespread applicability and cost-effectiveness for utility-scale and distributed generation projects.

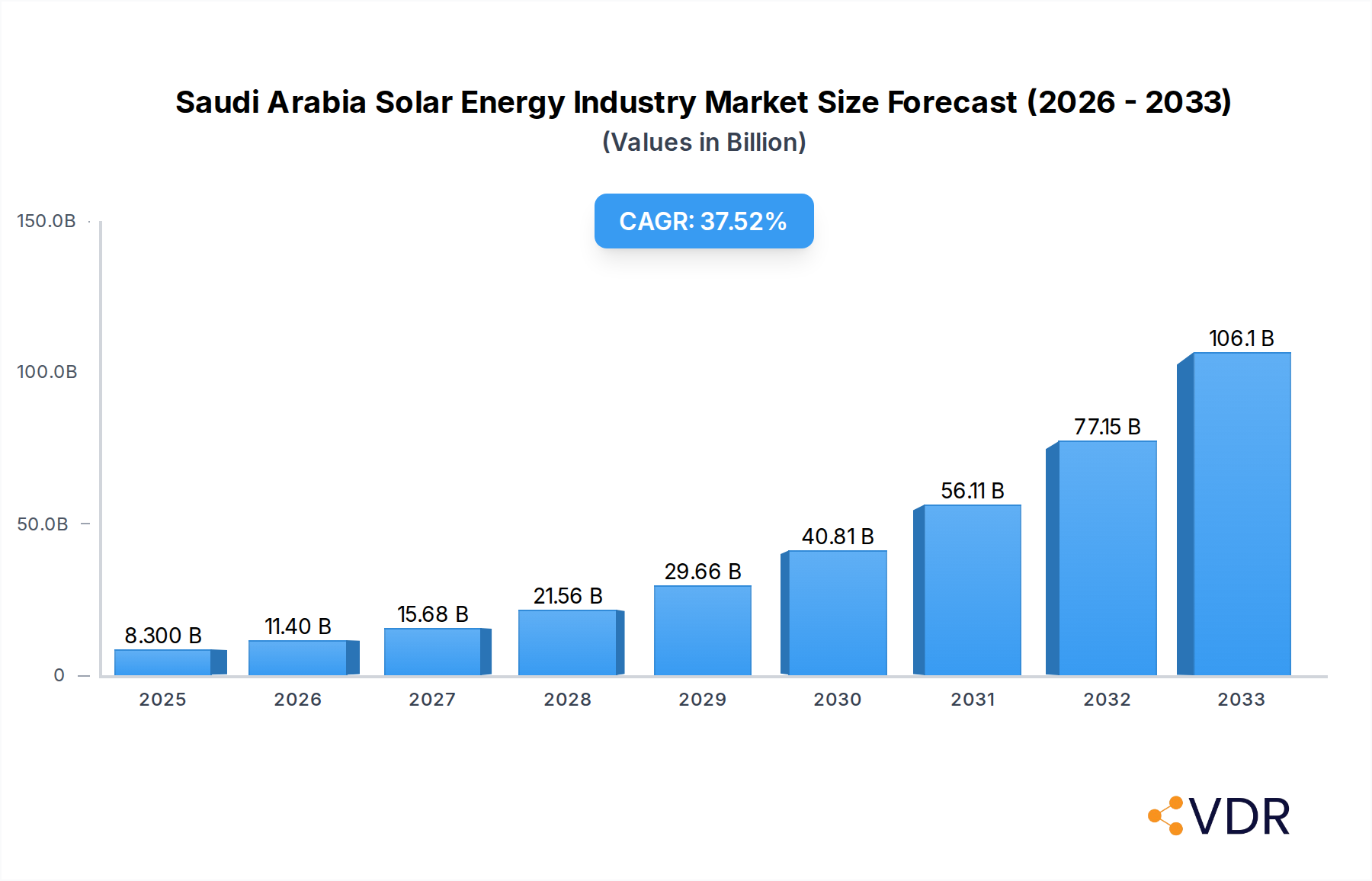

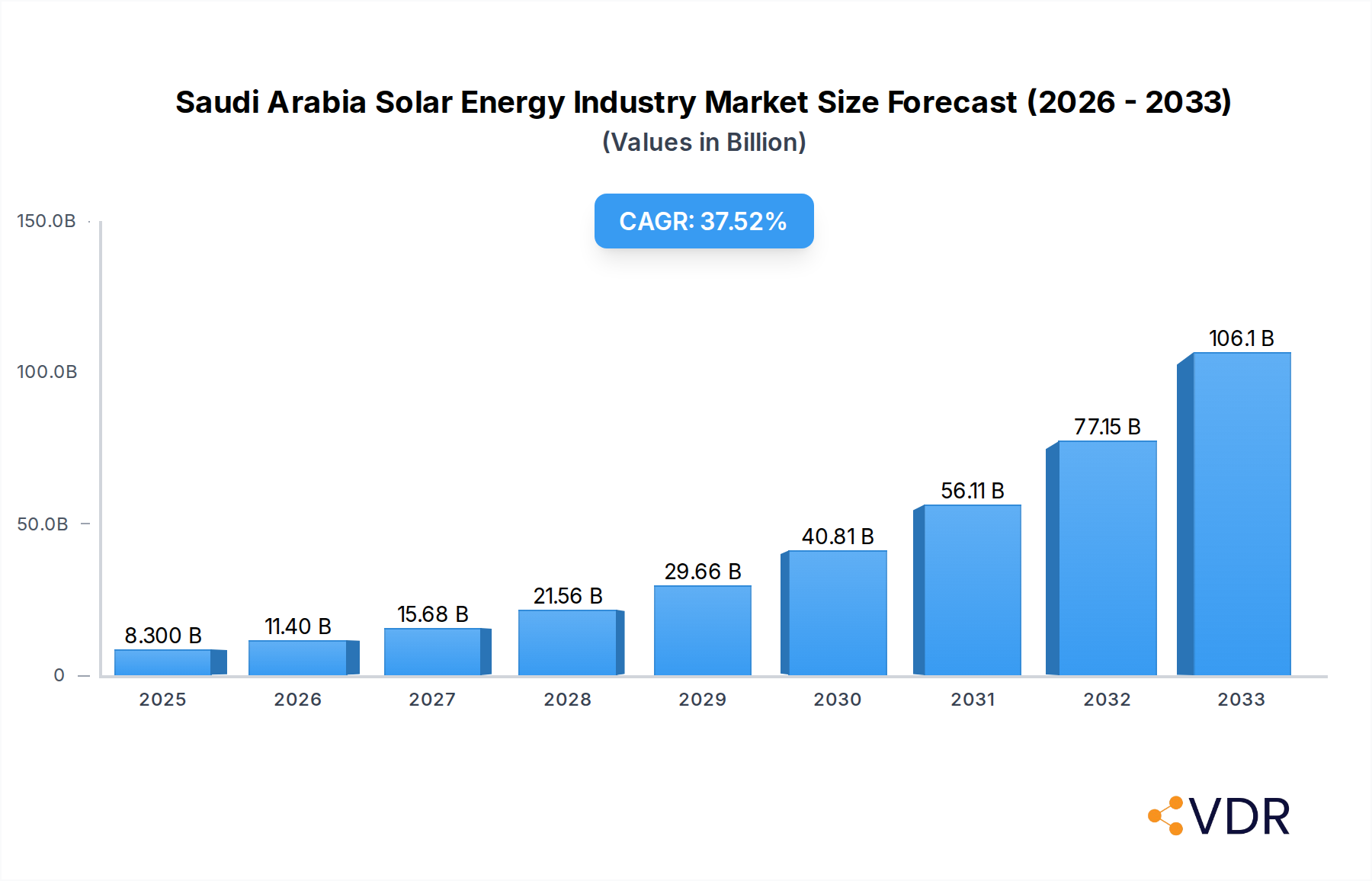

Saudi Arabia Solar Energy Industry Market Size (In Billion)

The competitive landscape features prominent global and local players, including JinkoSolar Holding Co Ltd, Enel SpA, Saudi Electricity Company, Engie SA, Alfanar Group, Abu Dhabi Future Energy Company (Masdar), EDF Renewables, and ACWA Power Company. These companies are actively involved in developing large-scale solar projects, contributing to the Kingdom's capacity expansion goals. While the industry enjoys robust growth, potential restraints could include the need for continuous grid modernization to accommodate intermittent renewable sources, evolving regulatory frameworks, and the development of a skilled local workforce. However, the overwhelming positive sentiment and strategic focus on solar energy development position Saudi Arabia as a leading market for solar power in the Middle East and globally.

Saudi Arabia Solar Energy Industry Company Market Share

This comprehensive report offers an in-depth analysis of the Saudi Arabia Solar Energy Industry, projecting significant growth and transformation from 2019 to 2033. Leveraging extensive market data and expert insights, this study provides a granular view of market dynamics, growth trajectories, dominant segments, product innovations, key drivers, barriers, emerging opportunities, and the strategic landscape shaped by leading industry players. With a focus on Saudi Arabia's ambitious renewable energy targets, this report is an essential resource for investors, policymakers, technology providers, and industry professionals seeking to capitalize on the burgeoning solar energy market in the Kingdom.

Saudi Arabia Solar Energy Industry Market Dynamics & Structure

The Saudi Arabia Solar Energy Industry is characterized by a rapidly evolving market structure, driven by visionary national energy strategies and substantial investments. Market concentration is gradually shifting as new players enter, though established entities like Saudi Electricity Company and ACWA Power Company maintain significant influence. Technological innovation serves as a primary driver, with advancements in solar photovoltaic (PV) efficiency and concentrated solar power (CSP) thermal storage solutions continuously pushing the boundaries of what's economically viable. Regulatory frameworks are being progressively refined to attract foreign investment and streamline project development, though localized challenges can still arise. Competitive product substitutes, primarily from conventional energy sources, are diminishing in relevance as solar energy's cost-competitiveness increases. End-user demographics are expanding beyond utility-scale projects to include commercial and residential installations, reflecting a growing awareness and demand for sustainable power solutions. Mergers and acquisitions (M&A) trends are on an upward trajectory, with major developers and international technology providers actively seeking strategic partnerships and acquisitions to secure market share and leverage local expertise. The M&A deal volume is expected to witness substantial growth in the forecast period, reflecting a maturing and consolidating market.

- Market Concentration: Increasing competition from both domestic and international players.

- Technological Innovation Drivers: Focus on increasing PV efficiency, advanced CSP technologies, and grid integration solutions.

- Regulatory Frameworks: Government incentives, PPA standardization, and streamlined permitting processes are crucial.

- Competitive Product Substitutes: Declining cost of solar power makes it increasingly competitive against fossil fuels.

- End-User Demographics: Growing demand from utility, commercial, and residential sectors.

- M&A Trends: Active pursuit of strategic partnerships and acquisitions for market consolidation and expansion.

Saudi Arabia Solar Energy Industry Growth Trends & Insights

The Saudi Arabia Solar Energy Industry is poised for extraordinary growth, projected to witness a robust Compound Annual Growth Rate (CAGR) of approximately 18.5% during the forecast period. This expansion is fundamentally driven by the Kingdom's commitment to diversifying its energy mix and achieving ambitious renewable energy targets outlined in Vision 2030. The market size is expected to surge from an estimated $5.0 billion in 2024 to an impressive $25.0 billion by 2033. Adoption rates for solar technologies are accelerating, fueled by declining levelized cost of energy (LCOE) for both solar PV and CSP. Technological disruptions, particularly in areas such as bifacial solar panels, perovskite solar cells, and advanced energy storage systems, are enhancing efficiency and reliability, making solar power a more attractive investment. Consumer behavior is shifting significantly, with a growing appetite for clean energy solutions among corporations seeking to reduce their carbon footprint and achieve sustainability goals, as well as a nascent but growing interest from the residential sector. The market penetration of solar energy is expected to climb steadily, displacing a larger share of fossil fuel-based electricity generation.

The historical period (2019-2024) laid the groundwork for this surge, with initial project developments and policy frameworks being established. The base year of 2025 marks a critical inflection point, with several large-scale projects scheduled for commissioning and further policy enhancements expected. The estimated market size for 2025 is approximately $6.2 billion, signaling a strong start to the accelerated growth phase. The forecast period (2025-2033) will witness the full realization of these growth drivers, with the market size evolving to accommodate an increasing number of utility-scale solar farms, distributed generation projects, and innovative hybrid energy solutions.

Key metrics underscoring this growth include:

- Market Size Evolution: From approximately $5.0 billion in 2024 to an estimated $25.0 billion by 2033.

- CAGR: Projected at 18.5% during the forecast period.

- Adoption Rates: Steadily increasing, driven by cost-competitiveness and policy support.

- Technological Disruptions: Advancements in PV efficiency, CSP storage, and grid integration are key enablers.

- Consumer Behavior Shifts: Growing demand from corporate entities and increasing interest from the residential sector.

- Market Penetration: Significant increase in solar's share of the overall energy mix.

- Base Year (2025) Estimated Market Size: Approximately $6.2 billion.

Dominant Regions, Countries, or Segments in Saudi Arabia Solar Energy Industry

The Saudi Arabia Solar Energy Industry is experiencing a dynamic shift in dominance, with Solar Photovoltaic (PV) emerging as the leading segment driving market growth. This dominance is underpinned by several critical factors, including the declining capital costs of PV technology, its modularity for scalable deployments, and rapid technological advancements that continuously improve efficiency and performance. Saudi Arabia's vast land availability further supports large-scale PV projects, which are crucial for meeting the nation's ambitious renewable energy targets. While Concentrated Solar Power (CSP) also plays a vital role, particularly in providing dispatchable power and thermal storage solutions, the sheer volume of utility-scale PV projects currently in development and planned execution positions PV as the primary growth engine.

The economic policies enacted by the Saudi government are a significant driver of this dominance. Initiatives such as the Renewable Energy Program (REP) and the Saudi Energy Efficiency Program (SEEP) have created a conducive environment for solar investments, attracting both domestic and international players. Projects like the Sakaka PV IPP (Independent Power Producer) and the Sudair Solar PV project are testaments to the scale and ambition of PV deployments. Infrastructure development, including grid enhancements and transmission line upgrades, is also crucial for integrating the massive influx of solar power into the national grid, further bolstering the dominance of PV.

The market share of Solar PV within the overall solar energy market is expected to consistently outpace CSP, primarily due to its more mature supply chain and lower upfront investment per megawatt compared to CSP. The growth potential for PV is immense, with numerous tenders and competitive bidding processes consistently awarding projects to PV-based solutions. The future outlook indicates continued PV supremacy, although CSP will remain an important component of the energy mix, especially for baseload renewable power and grid stability. The geographical distribution of these projects is spread across the Kingdom, with key industrial zones and arid regions being prime locations due to optimal solar irradiance and land availability.

- Dominant Segment: Solar Photovoltaic (PV) is the primary growth driver.

- Key Drivers for PV Dominance:

- Decreasing capital costs and LCOE.

- Modular and scalable deployment capabilities.

- Rapid technological advancements in efficiency and performance.

- Abundant land availability for utility-scale projects.

- Government economic policies and renewable energy targets.

- Infrastructure development for grid integration.

- Market Share: PV is projected to hold a larger market share compared to CSP.

- Growth Potential: Significant, with numerous large-scale projects in development and planned.

- CSP's Role: Important for dispatchable power and thermal storage, but not the primary growth driver.

Saudi Arabia Solar Energy Industry Product Landscape

The product landscape in the Saudi Arabia Solar Energy Industry is characterized by a rapid evolution of solar technologies, focusing on enhanced efficiency, durability, and cost-effectiveness. Solar Photovoltaic (PV) modules are dominated by high-efficiency monocrystalline silicon panels, with a growing adoption of bifacial modules to capture reflected sunlight from the ground, thereby increasing energy yield by up to 20%. Technological advancements in inverters, including smart and string inverters with advanced monitoring capabilities, are optimizing energy conversion and grid integration. For Concentrated Solar Power (CSP), advancements are focused on molten salt thermal storage systems, allowing for the dispatch of electricity even after sunset, and hybrid systems that combine solar thermal with other energy sources. The performance metrics being targeted include higher energy conversion efficiencies, longer operational lifespans exceeding 25 years, and enhanced resilience to harsh environmental conditions like high temperatures and sandstorms. Unique selling propositions revolve around increased power output per unit area, improved reliability, and integrated smart grid functionalities.

Key Drivers, Barriers & Challenges in Saudi Arabia Solar Energy Industry

The Saudi Arabia Solar Energy Industry is propelled by strong key drivers including the nation's ambitious Vision 2030, which aims for significant renewable energy penetration, thereby diversifying the economy away from oil. Government incentives, such as competitive tariffs and favorable power purchase agreements (PPAs), are attracting substantial investment. Furthermore, the declining global cost of solar technologies, particularly PV, makes solar energy increasingly cost-competitive with conventional power sources. Technological advancements are also contributing to higher efficiencies and improved reliability.

However, the industry faces barriers and challenges. One significant challenge is the upfront capital requirement for large-scale solar projects, which can be substantial. Supply chain disruptions and logistics for transporting large components to remote project sites can also pose hurdles. Regulatory complexities and the need for further standardization in permitting and grid connection processes can introduce delays. Competition from established fossil fuel interests and the need for robust grid infrastructure upgrades to handle intermittent renewable energy are also considerable challenges. The availability of skilled labor for project development, installation, and maintenance is another area that requires continuous development.

- Key Drivers:

- Vision 2030 renewable energy targets.

- Government incentives and favorable PPAs.

- Declining cost of solar technologies.

- Technological advancements in efficiency and reliability.

- Key Barriers & Challenges:

- High upfront capital investment.

- Supply chain and logistics complexities.

- Regulatory and permitting process streamlining.

- Grid infrastructure upgrades.

- Competition from conventional energy.

- Skilled labor availability.

Emerging Opportunities in Saudi Arabia Solar Energy Industry

Emerging opportunities within the Saudi Arabia Solar Energy Industry are multifaceted, extending beyond utility-scale projects. The burgeoning distributed generation market, encompassing rooftop solar for commercial and industrial facilities, presents a significant untapped potential, driven by corporate sustainability goals and the desire for energy independence. Furthermore, the integration of energy storage solutions, particularly advanced battery technologies and green hydrogen production powered by solar energy, is a rapidly expanding frontier, promising enhanced grid stability and new revenue streams. The development of solar-powered desalination plants is another key opportunity, addressing Saudi Arabia's critical water needs with sustainable energy. Innovations in agrivoltaics, combining solar power generation with agricultural activities, also hold promise for optimizing land use and supporting food security. The increasing focus on smart grid technologies and digital solutions for energy management creates opportunities for service providers and technology developers.

Growth Accelerators in the Saudi Arabia Solar Energy Industry Industry

Several key factors are acting as significant growth accelerators for the Saudi Arabia Solar Energy Industry. Foremost among these is the unwavering political will and strategic commitment from the Saudi government, translating into supportive policies, clear targets, and substantial financial backing for renewable energy projects. The continuous decrease in the global levelized cost of energy (LCOE) for solar PV technology makes it an increasingly attractive economic proposition, outcompeting fossil fuels in many scenarios. Strategic partnerships between international technology providers and local developers, such as collaborations between companies like JinkoSolar Holding Co Ltd and ACWA Power Company, accelerate the transfer of expertise and the deployment of cutting-edge solutions. Investment in R&D and innovation, particularly in areas like high-efficiency solar cells and advanced energy storage, further fuels growth by improving performance and reducing costs. The growing demand for sustainable energy from the industrial and corporate sectors, driven by ESG (Environmental, Social, and Governance) mandates, is also a powerful accelerator.

Key Players Shaping the Saudi Arabia Solar Energy Industry Market

- JinkoSolar Holding Co Ltd

- Enel SpA

- Saudi Electricity Company

- Engie SA

- Alfanar Group

- Abu Dhabi Future Energy Company (Masdar)

- EDF Renewables

- ACWA Power Company

Notable Milestones in Saudi Arabia Solar Energy Industry Sector

- 2019: Sakaka PV IPP, Saudi Arabia's first utility-scale renewable energy project, commences operations.

- 2020: Saudi Arabia announces its Net-Zero by 2060 target, reinforcing its commitment to renewables.

- 2021: The Sudair Solar PV IPP, one of the largest single-site solar projects globally, reaches financial close.

- 2022: Launch of significant tenders for new solar PV and CSP projects under the National Renewable Energy Program (NREP).

- 2023: Several large-scale solar projects achieve significant construction milestones and begin contributing to the grid.

- 2024 (Projected): Increased commissioning of previously awarded solar projects, further boosting installed capacity.

- 2025 (Projected): Significant increase in the overall solar energy contribution to Saudi Arabia's national grid.

In-Depth Saudi Arabia Solar Energy Industry Market Outlook

The future outlook for the Saudi Arabia Solar Energy Industry is exceptionally bright, driven by a confluence of strategic government initiatives, technological advancements, and favorable economics. The market is expected to experience sustained high growth throughout the forecast period, transforming the Kingdom's energy landscape. Key growth accelerators, including continued policy support and the decreasing LCOE of solar technologies, will ensure a steady pipeline of projects. Strategic partnerships between global leaders like Enel SpA and local powerhouses such as Alfanar Group will foster innovation and efficient project execution. The increasing focus on energy storage and green hydrogen integration presents substantial future market potential, positioning Saudi Arabia as a leader in sustainable energy solutions. Capitalizing on these opportunities requires a proactive approach to investment, technology adoption, and talent development within the sector.

Saudi Arabia Solar Energy Industry Segmentation

- 1. Solar Photovoltaic (PV)

- 2. Concentrated Solar Power (CSP)

Saudi Arabia Solar Energy Industry Segmentation By Geography

- 1. Saudi Arabia

Saudi Arabia Solar Energy Industry Regional Market Share

Geographic Coverage of Saudi Arabia Solar Energy Industry

Saudi Arabia Solar Energy Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 37.39% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Solar Photovoltaic (PV)

- 5.2. Market Analysis, Insights and Forecast - by Concentrated Solar Power (CSP)

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Saudi Arabia

- 6. Saudi Arabia Solar Energy Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Solar Photovoltaic (PV)

- 6.2. Market Analysis, Insights and Forecast - by Concentrated Solar Power (CSP)

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 JinkoSolar Holding Co Ltd

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Enel SpA*List Not Exhaustive

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Saudi Electricity Company

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Engie SA

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Alfanar Group

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Abu Dhabi Future Energy Company (Masdar)

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 EDF Renewables

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 ACWA Power Company

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.1 JinkoSolar Holding Co Ltd

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Saudi Arabia Solar Energy Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Saudi Arabia Solar Energy Industry Share (%) by Company 2025

List of Tables

- Table 1: Saudi Arabia Solar Energy Industry Revenue billion Forecast, by Solar Photovoltaic (PV) 2020 & 2033

- Table 2: Saudi Arabia Solar Energy Industry Revenue billion Forecast, by Concentrated Solar Power (CSP) 2020 & 2033

- Table 3: Saudi Arabia Solar Energy Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Saudi Arabia Solar Energy Industry Revenue billion Forecast, by Solar Photovoltaic (PV) 2020 & 2033

- Table 5: Saudi Arabia Solar Energy Industry Revenue billion Forecast, by Concentrated Solar Power (CSP) 2020 & 2033

- Table 6: Saudi Arabia Solar Energy Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Saudi Arabia Solar Energy Industry?

The projected CAGR is approximately 37.39%.

2. Which companies are prominent players in the Saudi Arabia Solar Energy Industry?

Key companies in the market include JinkoSolar Holding Co Ltd, Enel SpA*List Not Exhaustive, Saudi Electricity Company, Engie SA, Alfanar Group, Abu Dhabi Future Energy Company (Masdar), EDF Renewables, ACWA Power Company.

3. What are the main segments of the Saudi Arabia Solar Energy Industry?

The market segments include Solar Photovoltaic (PV), Concentrated Solar Power (CSP).

4. Can you provide details about the market size?

The market size is estimated to be USD 8.3 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Increasing Diversification of Energy Sources from Oil and Gas to Cleaner Energy Sources4.; Supportive Government Policies for Increasing Renewable Power Capacity.

6. What are the notable trends driving market growth?

Solar Photovoltaic (PV) Type Expected to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; The Unstable Geopolitics of the Country.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Saudi Arabia Solar Energy Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Saudi Arabia Solar Energy Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Saudi Arabia Solar Energy Industry?

To stay informed about further developments, trends, and reports in the Saudi Arabia Solar Energy Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence