Key Insights

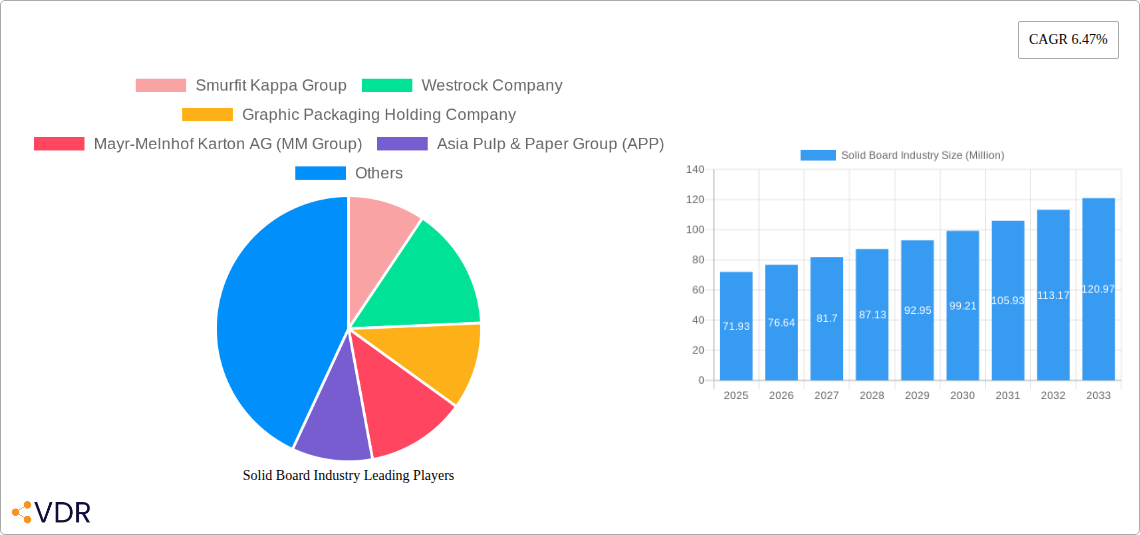

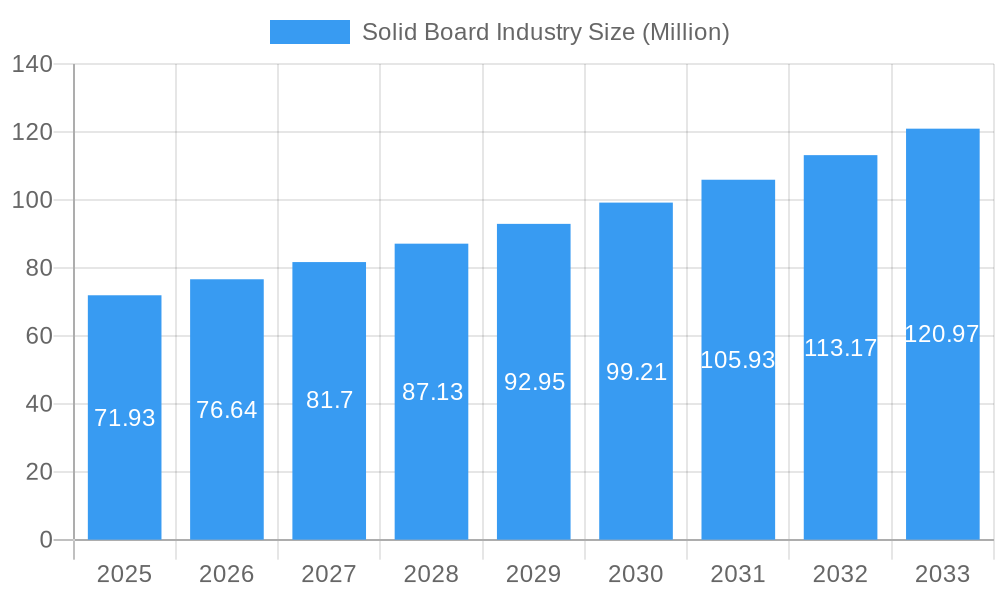

The global Solid Board market is poised for robust expansion, projected to reach USD 71.93 million by 2025 and exhibiting a compound annual growth rate (CAGR) of 6.47% through 2033. This growth is underpinned by increasing demand across diverse end-user industries, notably the beverage and food sectors, where solid board's excellent barrier properties, printability, and sustainability credentials make it an ideal packaging solution. The pharmaceutical and healthcare, cosmetics and toiletries, and tobacco industries are also significant contributors to market growth, driven by evolving consumer preferences for premium, protective, and eco-friendly packaging. Key product grades such as Folding Boxboard and Liquid Packaging Board are expected to witness substantial uptake due to their versatility and functional advantages in these applications. Leading manufacturers like Smurfit Kappa Group, WestRock Company, and Graphic Packaging Holding Company are at the forefront of innovation, developing advanced solid board solutions to meet stringent industry standards and consumer expectations.

Solid Board Industry Market Size (In Million)

The market's dynamism is further shaped by several driving forces and emerging trends. A primary driver is the escalating consumer consciousness regarding environmental sustainability, propelling the demand for recyclable and biodegradable packaging materials like solid board. Regulatory pressures and corporate sustainability initiatives further amplify this trend, pushing manufacturers to adopt greener production processes and develop eco-certified products. Technological advancements in paperboard manufacturing, including improved coating techniques and enhanced structural integrity, are also contributing to market growth by enabling the production of specialized solid board grades for demanding applications. While the market presents significant opportunities, it also faces certain restraints. Fluctuations in raw material prices, particularly for pulp and energy, can impact production costs and profit margins. Intense competition and the availability of alternative packaging materials, such as flexible plastics and metal cans, necessitate continuous innovation and cost-effectiveness from solid board manufacturers. Nevertheless, the inherent advantages of solid board in terms of recyclability, lightweight properties, and visual appeal are expected to sustain its market dominance.

Solid Board Industry Company Market Share

Unveiling the Solid Board Industry: A Comprehensive Market Analysis (2019-2033)

This in-depth report provides a definitive overview of the global Solid Board Industry, offering critical insights for stakeholders navigating this dynamic sector. Covering the historical period from 2019-2024 and projecting growth through 2033, with a base and estimated year of 2025, this analysis dissects market dynamics, growth trends, regional dominance, product landscapes, and key player strategies. Leveraging high-traffic keywords and a parent-child market approach, this report ensures maximum SEO visibility and engagement for industry professionals. We delve into market size in million units, CAGR, adoption rates, and market penetration, offering actionable intelligence for strategic decision-making.

Solid Board Industry Market Dynamics & Structure

The global Solid Board Industry exhibits a moderately concentrated market structure, with key players like Smurfit Kappa Group, Westrock Company, Graphic Packaging Holding Company, Mayr-Melnhof Karton AG (MM Group), Asia Pulp & Paper Group (APP), and Stora Enso OYJ holding significant market shares. Technological innovation is primarily driven by the demand for sustainable packaging solutions, enhanced barrier properties, and improved printability. Regulatory frameworks, particularly concerning environmental impact and recyclability, are increasingly shaping market strategies and product development. Competitive product substitutes include plastics, metal, and flexible packaging, necessitating continuous innovation in the solid board segment. End-user demographics are diverse, with significant influence from the food & beverage, pharmaceutical, and cosmetics sectors, all demanding robust, safe, and aesthetically pleasing packaging. Mergers and acquisitions (M&A) trends are evident, with companies consolidating to expand their geographical reach, product portfolios, and technological capabilities. For instance, strategic acquisitions aim to integrate downstream operations and enhance supply chain efficiency, contributing to market consolidation.

- Market Concentration: Dominated by a few key global players, with ongoing M&A activities.

- Innovation Drivers: Sustainability, recyclability, barrier properties, and advanced printing capabilities.

- Regulatory Impact: Increasing focus on environmental compliance and circular economy principles.

- Competitive Landscape: Intense competition from alternative packaging materials.

- End-User Influence: Strong demand from food & beverage, healthcare, and consumer goods.

- M&A Trends: Strategic acquisitions and consolidations to gain market share and expand capabilities.

Solid Board Industry Growth Trends & Insights

The Solid Board Industry is poised for robust growth, driven by an escalating global demand for sustainable and eco-friendly packaging solutions. Market size, estimated at XX million units in the base year of 2025, is projected to witness a Compound Annual Growth Rate (CAGR) of XX% during the forecast period of 2025-2033. Adoption rates for specialized solid board grades, such as Liquid Packaging Board and Food Service Board, are on the rise, propelled by evolving consumer preferences and stringent regulations on single-use plastics. Technological disruptions, including advancements in papermaking processes and coating technologies, are enhancing the performance and application range of solid board products. Consumer behavior shifts, particularly the growing preference for ethically sourced and recyclable products, are directly influencing purchasing decisions and driving demand for solid board packaging. The parent market, encompassing all paper and paperboard products, sees solid board as a significant and growing segment. The child markets, such as folding carton manufacturers and converters, are directly impacted by the availability and innovation within the solid board sector. This synergy fosters market penetration of advanced solid board solutions across various consumer goods categories.

- Market Size Evolution: Significant growth projected from XX million units (2025) to XX million units (2033).

- CAGR: Estimated at XX% during the forecast period, indicating sustained expansion.

- Adoption Rates: Increasing for specialized boards like Liquid Packaging Board and Food Service Board.

- Technological Disruptions: Innovations in papermaking, coatings, and barrier technologies.

- Consumer Behavior Shifts: Growing demand for sustainable, recyclable, and ethically produced packaging.

- Market Penetration: Expanding into new applications and consumer segments due to enhanced properties and sustainability credentials.

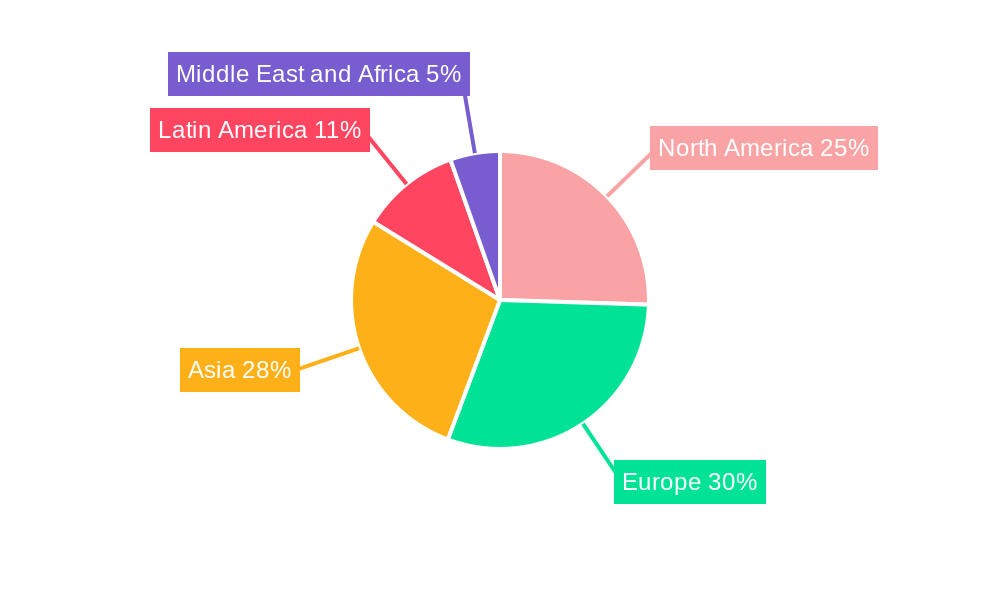

Dominant Regions, Countries, or Segments in Solid Board Industry

The Asia-Pacific region, particularly China and Southeast Asian nations, is emerging as a dominant force in the Solid Board Industry, driven by a rapidly expanding consumer base, burgeoning e-commerce sector, and significant investments in manufacturing infrastructure. Within the product grade segment, Folding Boxboard holds a substantial market share due to its widespread application in the packaging of consumer goods, pharmaceuticals, and food items. The Food & Beverage end-user segment represents the largest market for solid board, owing to the critical need for safe, hygienic, and visually appealing packaging for a vast array of products. Economic policies promoting domestic manufacturing and trade agreements facilitating cross-border commerce further bolster the growth in key Asian countries.

- Leading Region: Asia-Pacific, with significant contributions from China and emerging economies.

- Dominant Product Grade: Folding Boxboard, widely utilized across various consumer goods.

- Largest End-User Segment: Food & Beverage, demanding high standards of safety and presentation.

- Key Drivers:

- Economic Policies: Government support for manufacturing and industrial growth.

- E-commerce Boom: Increased demand for robust and protective packaging.

- Urbanization: Rising consumer spending and demand for packaged goods.

- Infrastructure Development: Improved logistics and supply chain networks.

- Growth Potential: Significant untapped potential in developing economies within the region.

- Market Share: Asia-Pacific is projected to capture an increasing share of the global solid board market.

Solid Board Industry Product Landscape

The Solid Board Industry is characterized by a diverse product landscape featuring continuous innovation in product grades and their applications. Solid Bleached Board and Folding Boxboard are prominent, offering excellent printability and structural integrity for premium packaging. Liquid Packaging Board is experiencing significant advancements in barrier properties to meet the demand for sustainable alternatives to plastic containers for beverages. White-lined Chipboard remains a cost-effective solution for secondary packaging and industrial goods. Performance metrics are consistently improving, with a focus on enhanced stiffness, moisture resistance, and food contact compliance. The unique selling propositions revolve around sustainability, recyclability, and the ability to deliver high-quality graphics, making solid board an attractive choice for brands seeking to communicate value and responsibility to consumers.

Key Drivers, Barriers & Challenges in Solid Board Industry

Key Drivers, Barriers & Challenges in Solid Board Industry

Key Drivers:

- Sustainability Imperative: Growing global demand for eco-friendly and recyclable packaging materials is a primary growth catalyst.

- E-commerce Expansion: The surge in online retail necessitates robust, protective, and lightweight packaging solutions like solid board.

- Consumer Preference Shifts: Increasing consumer awareness regarding environmental impact favors paper-based packaging over plastics.

- Technological Advancements: Innovations in pulp processing, coating, and printing technologies enhance the functionality and appeal of solid board.

- Regulatory Support: Government initiatives and policies promoting circular economy principles and reducing plastic waste indirectly boost the solid board market.

Key Barriers & Challenges:

- Raw Material Price Volatility: Fluctuations in the cost of pulp, a key raw material, can impact profit margins.

- Competition from Alternative Materials: Plastics, flexible packaging, and metal packaging continue to pose significant competitive threats.

- Energy Intensity of Production: Papermaking is an energy-intensive process, leading to concerns about operational costs and environmental footprint.

- Supply Chain Disruptions: Global supply chain issues, including logistics and raw material availability, can impact production and delivery timelines.

- Recycling Infrastructure Limitations: In some regions, inadequate or inefficient recycling infrastructure can hinder the full potential of a circular economy for paperboard.

Emerging Opportunities in Solid Board Industry

Emerging opportunities in the Solid Board Industry lie in the development of advanced functional coatings that enhance barrier properties, offering sustainable alternatives to plastic laminations. The burgeoning demand for personalized and premium packaging presents a niche for high-graphic print capabilities on various solid board grades. Untapped markets in developing economies, particularly for food and pharmaceutical packaging, offer significant growth potential. Furthermore, the exploration of novel fiber sources and innovative manufacturing processes to reduce the environmental footprint and enhance the performance of solid board products will be crucial. The integration of smart packaging features, such as track-and-trace capabilities, into solid board designs also presents a promising avenue for future development.

Growth Accelerators in the Solid Board Industry Industry

Several key catalysts are accelerating the growth of the Solid Board Industry. Technological breakthroughs in papermaking, such as closed-loop water systems and energy-efficient production methods, are enhancing sustainability and reducing operational costs. Strategic partnerships between solid board manufacturers and packaging converters are fostering innovation and expanding market reach. The development of specialized solid board grades tailored for specific applications, like those with enhanced grease or moisture resistance, is driving adoption across diverse industries. Furthermore, aggressive market expansion strategies by leading players, focusing on emerging economies and high-growth application segments, are fueling overall industry expansion and solidifying the position of solid board as a preferred packaging material.

Key Players Shaping the Solid Board Industry Market

Smurfit Kappa Group Westrock Company Graphic Packaging Holding Company Mayr-Melnhof Karton AG (MM Group) Asia Pulp & Paper Group (APP) Pankaboard OYJ International Paper Company Stora Enso OYJ Metsa Board Nine Dragons Paper Holdings Limited

Notable Milestones in Solid Board Industry Sector

- June 2023: Stora Enso opened a new corrugated board manufacturing facility in De Lier, the Netherlands, as part of the De Jong Packaging Group acquisition, enhancing their Western Europe business unit with a strong focus on sustainable operations.

- June 2023: Metsa Group, in collaboration with Mets Spring and Fiskars Group, introduced Mouto 3D, a groundbreaking fiber-based packaging solution for outer packaging, enhancing the consumer experience by showcasing Fiskars' ReNew scissors made from recycled materials.

In-Depth Solid Board Industry Market Outlook

The future outlook for the Solid Board Industry is exceptionally promising, driven by a confluence of sustained demand for sustainable packaging solutions and continuous innovation. Growth accelerators such as the ongoing expansion of e-commerce, increasing consumer consciousness, and supportive regulatory environments are creating a fertile ground for market expansion. Strategic opportunities lie in the development of higher-value, specialty solid board grades with enhanced barrier properties and unique functionalities, catering to the evolving needs of the food, beverage, pharmaceutical, and cosmetic sectors. Companies that invest in R&D, focus on circular economy principles, and strategically expand their global footprint are best positioned to capitalize on the significant future market potential and solidify their leadership in this dynamic industry.

Solid Board Industry Segmentation

-

1. Product Grade

- 1.1. Solid Bleached Board

- 1.2. Solid Unbleached Board

- 1.3. Folding Boxboard

- 1.4. White-lined Chipboard

- 1.5. Liquid Packaging Board

- 1.6. Food Service Board

-

2. End-User

- 2.1. Beverage

- 2.2. Food

- 2.3. Pharmaceutical and Healthcare

- 2.4. Cosmetics and Toiletries

- 2.5. Tobacco

Solid Board Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

-

2. Europe

- 2.1. United Kingdom

- 2.2. Germany

- 2.3. France

- 2.4. Italy

- 2.5. Spain

-

3. Asia

- 3.1. China

- 3.2. India

- 3.3. Japan

- 3.4. Australia and New Zealand

-

4. Latin America

- 4.1. Brazil

- 4.2. Argentina

- 4.3. Mexico

-

5. Middle East and Africa

- 5.1. United Arab Emirates

- 5.2. Saudi Arabia

- 5.3. South Africa

- 5.4. Egypt

Solid Board Industry Regional Market Share

Geographic Coverage of Solid Board Industry

Solid Board Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.47% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Grade

- 5.1.1. Solid Bleached Board

- 5.1.2. Solid Unbleached Board

- 5.1.3. Folding Boxboard

- 5.1.4. White-lined Chipboard

- 5.1.5. Liquid Packaging Board

- 5.1.6. Food Service Board

- 5.2. Market Analysis, Insights and Forecast - by End-User

- 5.2.1. Beverage

- 5.2.2. Food

- 5.2.3. Pharmaceutical and Healthcare

- 5.2.4. Cosmetics and Toiletries

- 5.2.5. Tobacco

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia

- 5.3.4. Latin America

- 5.3.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Product Grade

- 6. Global Solid Board Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Grade

- 6.1.1. Solid Bleached Board

- 6.1.2. Solid Unbleached Board

- 6.1.3. Folding Boxboard

- 6.1.4. White-lined Chipboard

- 6.1.5. Liquid Packaging Board

- 6.1.6. Food Service Board

- 6.2. Market Analysis, Insights and Forecast - by End-User

- 6.2.1. Beverage

- 6.2.2. Food

- 6.2.3. Pharmaceutical and Healthcare

- 6.2.4. Cosmetics and Toiletries

- 6.2.5. Tobacco

- 6.1. Market Analysis, Insights and Forecast - by Product Grade

- 7. North America Solid Board Industry Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Product Grade

- 7.1.1. Solid Bleached Board

- 7.1.2. Solid Unbleached Board

- 7.1.3. Folding Boxboard

- 7.1.4. White-lined Chipboard

- 7.1.5. Liquid Packaging Board

- 7.1.6. Food Service Board

- 7.2. Market Analysis, Insights and Forecast - by End-User

- 7.2.1. Beverage

- 7.2.2. Food

- 7.2.3. Pharmaceutical and Healthcare

- 7.2.4. Cosmetics and Toiletries

- 7.2.5. Tobacco

- 7.1. Market Analysis, Insights and Forecast - by Product Grade

- 8. Europe Solid Board Industry Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Product Grade

- 8.1.1. Solid Bleached Board

- 8.1.2. Solid Unbleached Board

- 8.1.3. Folding Boxboard

- 8.1.4. White-lined Chipboard

- 8.1.5. Liquid Packaging Board

- 8.1.6. Food Service Board

- 8.2. Market Analysis, Insights and Forecast - by End-User

- 8.2.1. Beverage

- 8.2.2. Food

- 8.2.3. Pharmaceutical and Healthcare

- 8.2.4. Cosmetics and Toiletries

- 8.2.5. Tobacco

- 8.1. Market Analysis, Insights and Forecast - by Product Grade

- 9. Asia Solid Board Industry Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Product Grade

- 9.1.1. Solid Bleached Board

- 9.1.2. Solid Unbleached Board

- 9.1.3. Folding Boxboard

- 9.1.4. White-lined Chipboard

- 9.1.5. Liquid Packaging Board

- 9.1.6. Food Service Board

- 9.2. Market Analysis, Insights and Forecast - by End-User

- 9.2.1. Beverage

- 9.2.2. Food

- 9.2.3. Pharmaceutical and Healthcare

- 9.2.4. Cosmetics and Toiletries

- 9.2.5. Tobacco

- 9.1. Market Analysis, Insights and Forecast - by Product Grade

- 10. Latin America Solid Board Industry Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Product Grade

- 10.1.1. Solid Bleached Board

- 10.1.2. Solid Unbleached Board

- 10.1.3. Folding Boxboard

- 10.1.4. White-lined Chipboard

- 10.1.5. Liquid Packaging Board

- 10.1.6. Food Service Board

- 10.2. Market Analysis, Insights and Forecast - by End-User

- 10.2.1. Beverage

- 10.2.2. Food

- 10.2.3. Pharmaceutical and Healthcare

- 10.2.4. Cosmetics and Toiletries

- 10.2.5. Tobacco

- 10.1. Market Analysis, Insights and Forecast - by Product Grade

- 11. Middle East and Africa Solid Board Industry Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Product Grade

- 11.1.1. Solid Bleached Board

- 11.1.2. Solid Unbleached Board

- 11.1.3. Folding Boxboard

- 11.1.4. White-lined Chipboard

- 11.1.5. Liquid Packaging Board

- 11.1.6. Food Service Board

- 11.2. Market Analysis, Insights and Forecast - by End-User

- 11.2.1. Beverage

- 11.2.2. Food

- 11.2.3. Pharmaceutical and Healthcare

- 11.2.4. Cosmetics and Toiletries

- 11.2.5. Tobacco

- 11.1. Market Analysis, Insights and Forecast - by Product Grade

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Smurfit Kappa Group

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Westrock Company

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Graphic Packaging Holding Company

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Mayr-Melnhof Karton AG (MM Group)

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Asia Pulp & Paper Group (APP)

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Pankaboard OYJ*List Not Exhaustive

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 International Paper Company

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Stora Enso OYJ

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Metsa Board

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Nine Dragons Paper Holdings Limited

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Smurfit Kappa Group

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Solid Board Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Solid Board Industry Revenue (Million), by Product Grade 2025 & 2033

- Figure 3: North America Solid Board Industry Revenue Share (%), by Product Grade 2025 & 2033

- Figure 4: North America Solid Board Industry Revenue (Million), by End-User 2025 & 2033

- Figure 5: North America Solid Board Industry Revenue Share (%), by End-User 2025 & 2033

- Figure 6: North America Solid Board Industry Revenue (Million), by Country 2025 & 2033

- Figure 7: North America Solid Board Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Solid Board Industry Revenue (Million), by Product Grade 2025 & 2033

- Figure 9: Europe Solid Board Industry Revenue Share (%), by Product Grade 2025 & 2033

- Figure 10: Europe Solid Board Industry Revenue (Million), by End-User 2025 & 2033

- Figure 11: Europe Solid Board Industry Revenue Share (%), by End-User 2025 & 2033

- Figure 12: Europe Solid Board Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: Europe Solid Board Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Solid Board Industry Revenue (Million), by Product Grade 2025 & 2033

- Figure 15: Asia Solid Board Industry Revenue Share (%), by Product Grade 2025 & 2033

- Figure 16: Asia Solid Board Industry Revenue (Million), by End-User 2025 & 2033

- Figure 17: Asia Solid Board Industry Revenue Share (%), by End-User 2025 & 2033

- Figure 18: Asia Solid Board Industry Revenue (Million), by Country 2025 & 2033

- Figure 19: Asia Solid Board Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Latin America Solid Board Industry Revenue (Million), by Product Grade 2025 & 2033

- Figure 21: Latin America Solid Board Industry Revenue Share (%), by Product Grade 2025 & 2033

- Figure 22: Latin America Solid Board Industry Revenue (Million), by End-User 2025 & 2033

- Figure 23: Latin America Solid Board Industry Revenue Share (%), by End-User 2025 & 2033

- Figure 24: Latin America Solid Board Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Latin America Solid Board Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East and Africa Solid Board Industry Revenue (Million), by Product Grade 2025 & 2033

- Figure 27: Middle East and Africa Solid Board Industry Revenue Share (%), by Product Grade 2025 & 2033

- Figure 28: Middle East and Africa Solid Board Industry Revenue (Million), by End-User 2025 & 2033

- Figure 29: Middle East and Africa Solid Board Industry Revenue Share (%), by End-User 2025 & 2033

- Figure 30: Middle East and Africa Solid Board Industry Revenue (Million), by Country 2025 & 2033

- Figure 31: Middle East and Africa Solid Board Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Solid Board Industry Revenue Million Forecast, by Product Grade 2020 & 2033

- Table 2: Global Solid Board Industry Revenue Million Forecast, by End-User 2020 & 2033

- Table 3: Global Solid Board Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Global Solid Board Industry Revenue Million Forecast, by Product Grade 2020 & 2033

- Table 5: Global Solid Board Industry Revenue Million Forecast, by End-User 2020 & 2033

- Table 6: Global Solid Board Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: United States Solid Board Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: Canada Solid Board Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 9: Global Solid Board Industry Revenue Million Forecast, by Product Grade 2020 & 2033

- Table 10: Global Solid Board Industry Revenue Million Forecast, by End-User 2020 & 2033

- Table 11: Global Solid Board Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 12: United Kingdom Solid Board Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 13: Germany Solid Board Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: France Solid Board Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: Italy Solid Board Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Spain Solid Board Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: Global Solid Board Industry Revenue Million Forecast, by Product Grade 2020 & 2033

- Table 18: Global Solid Board Industry Revenue Million Forecast, by End-User 2020 & 2033

- Table 19: Global Solid Board Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 20: China Solid Board Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 21: India Solid Board Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Japan Solid Board Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 23: Australia and New Zealand Solid Board Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: Global Solid Board Industry Revenue Million Forecast, by Product Grade 2020 & 2033

- Table 25: Global Solid Board Industry Revenue Million Forecast, by End-User 2020 & 2033

- Table 26: Global Solid Board Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 27: Brazil Solid Board Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: Argentina Solid Board Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 29: Mexico Solid Board Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: Global Solid Board Industry Revenue Million Forecast, by Product Grade 2020 & 2033

- Table 31: Global Solid Board Industry Revenue Million Forecast, by End-User 2020 & 2033

- Table 32: Global Solid Board Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 33: United Arab Emirates Solid Board Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: Saudi Arabia Solid Board Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Solid Board Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: Egypt Solid Board Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Solid Board Industry?

The projected CAGR is approximately 6.47%.

2. Which companies are prominent players in the Solid Board Industry?

Key companies in the market include Smurfit Kappa Group, Westrock Company, Graphic Packaging Holding Company, Mayr-Melnhof Karton AG (MM Group), Asia Pulp & Paper Group (APP), Pankaboard OYJ*List Not Exhaustive, International Paper Company, Stora Enso OYJ, Metsa Board, Nine Dragons Paper Holdings Limited.

3. What are the main segments of the Solid Board Industry?

The market segments include Product Grade, End-User.

4. Can you provide details about the market size?

The market size is estimated to be USD 71.93 Million as of 2022.

5. What are some drivers contributing to market growth?

Strong Demand from the E-commerce Sector; Growing Demand for Lightweight Materials and Scope for Printing Innovations Propelling Growth in the Personal Care Segment.

6. What are the notable trends driving market growth?

The Beverage Segment is Expected to Record the Fastest Growth.

7. Are there any restraints impacting market growth?

Increasing Operational Costs.

8. Can you provide examples of recent developments in the market?

June 2023: Stora Enso opened a new corrugated board manufacturing facility in De Lier, the Netherlands. The site was part of the De Jong Packaging Group acquisition, later known as the Western Europe business unit within the Packaging Solutions Division. This massive expansion was designed with a strong focus on sustainable operations.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Solid Board Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Solid Board Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Solid Board Industry?

To stay informed about further developments, trends, and reports in the Solid Board Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence