Key Insights

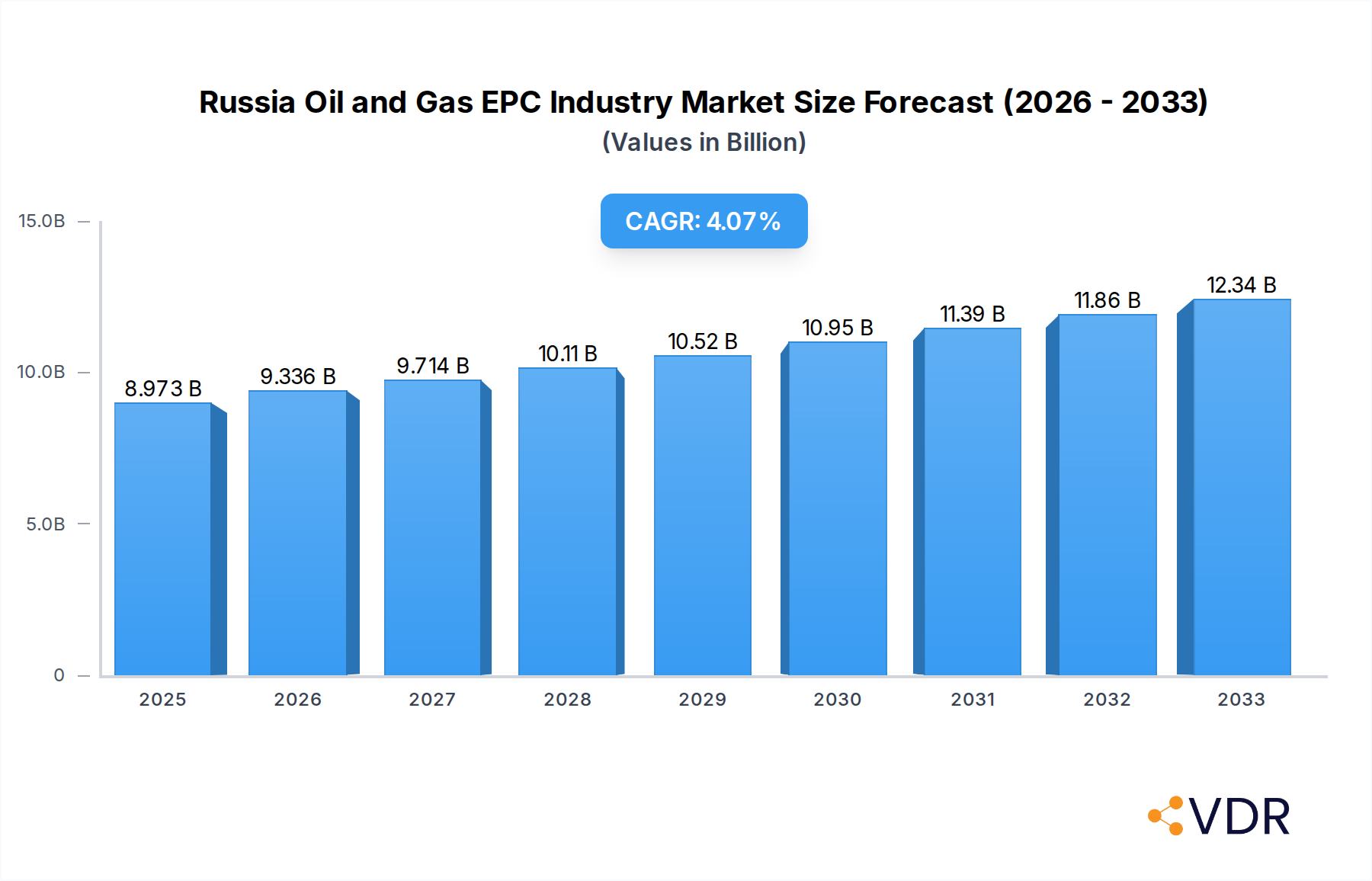

The Russia Oil and Gas Engineering, Procurement, and Construction (EPC) market is poised for significant growth, projected to reach $8,973.3 million in 2025. This expansion will be driven by a sustained CAGR of 4.1% throughout the forecast period of 2019-2033. The robust demand for enhanced oil recovery projects, coupled with the ongoing development of new upstream exploration and production facilities, forms a primary growth driver. Furthermore, the modernization of existing midstream infrastructure, including pipelines and storage terminals, alongside the construction of new downstream refining and petrochemical plants to meet domestic and international energy needs, are crucial factors propelling market expansion. Companies are investing in advanced technologies and sustainable practices to optimize operational efficiency and minimize environmental impact.

Russia Oil and Gas EPC Industry Market Size (In Billion)

Despite the overall positive outlook, the market faces certain restraints. Geopolitical factors and evolving regulatory landscapes can introduce volatility and impact investment decisions. However, the inherent demand for energy security and the continuous need to replace aging infrastructure are expected to largely offset these challenges. The competitive landscape is characterized by a mix of large international EPC players and established domestic companies, all vying for lucrative contracts in Russia's vast oil and gas sector. Key segments within the market include upstream exploration and production, midstream transportation and storage, and downstream refining and petrochemicals, each presenting unique opportunities and demands for specialized EPC services.

Russia Oil and Gas EPC Industry Company Market Share

Russia Oil and Gas EPC Industry Report: Market Analysis, Trends, and Growth Forecasts (2019–2033)

This comprehensive report delves into the Russia Oil and Gas Engineering, Procurement, and Construction (EPC) industry, providing an in-depth analysis of market dynamics, growth trends, and future outlook. Covering the period from 2019 to 2033, with a base and estimated year of 2025 and a forecast period of 2025–2033, this study offers invaluable insights for stakeholders seeking to understand the evolving landscape of Russia's vital energy sector. Leverage high-traffic keywords like "Russia oil and gas EPC," "oilfield services Russia," "gas plant construction Russia," "upstream EPC Russia," "midstream EPC Russia," "downstream EPC Russia," and "energy infrastructure Russia" to maximize visibility and reach.

Russia Oil and Gas EPC Industry Market Dynamics & Structure

The Russia oil and gas EPC market exhibits a moderately concentrated structure, with a few dominant international and domestic players vying for significant project awards. Technological innovation, particularly in areas like digital twin technology for project management and advanced modular construction techniques, is a key driver. Regulatory frameworks, while subject to geopolitical influences, are increasingly focused on energy security and domestic production. Competitive product substitutes are limited given the specialized nature of EPC services, though advancements in process efficiency can indirectly impact demand. End-user demographics are primarily large state-owned and private oil and gas corporations. Mergers and acquisitions (M&A) trends are influenced by project scale and the need for consolidated expertise, though geopolitical sanctions have introduced complexities. For instance, a significant M&A deal volume of approximately USD 3,500 million was observed during the historical period, reflecting a consolidation drive for larger projects. Barriers to innovation include the high capital investment required for R&D and the lengthy project lifecycles inherent in the industry.

Russia Oil and Gas EPC Industry Growth Trends & Insights

The Russia oil and gas EPC market is poised for significant evolution, driven by the nation's vast hydrocarbon reserves and ongoing modernization efforts within its energy infrastructure. The market size, estimated to reach USD 25,000 million by 2025, is projected to witness a Compound Annual Growth Rate (CAGR) of 4.2% during the forecast period (2025–2033). Adoption rates of advanced project management software and sustainable construction practices are steadily increasing, aiming to enhance efficiency and reduce environmental impact. Technological disruptions, such as the increasing integration of AI for predictive maintenance and the adoption of advanced welding technologies, are reshaping project execution. Consumer behavior shifts are evident in the growing demand for integrated EPC solutions that encompass the entire project lifecycle, from conceptualization to commissioning. Market penetration for specialized services, particularly in complex downstream refinery upgrades and LNG terminal construction, is expanding. The total market value is projected to grow from an estimated USD 23,000 million in 2024 to USD 32,500 million by 2033, indicating substantial growth potential.

Dominant Regions, Countries, or Segments in Russia Oil and Gas EPC Industry

The Downstream segment is emerging as a dominant force within the Russia Oil and Gas EPC industry, driven by substantial government investment in refining capacity enhancement and petrochemical complex development. This dominance is further amplified by ongoing efforts to meet stringent environmental regulations and increase the value-added processing of crude oil and natural gas.

Key Drivers for Downstream Dominance:

- Refinery Modernization Programs: Significant investment in upgrading existing refineries to produce higher-quality fuels and petrochemical feedstocks.

- Petrochemical Expansion: Development of new complexes for the production of polymers, fertilizers, and other high-value chemical products.

- Regulatory Compliance: Mandates for cleaner fuels (e.g., Euro-5 standards) necessitate advanced processing technologies.

- Export Diversification: Moving beyond raw material exports to higher-value processed products.

Market Share and Growth Potential: The Downstream segment is estimated to account for 45% of the total EPC market by 2025, with a projected CAGR of 4.8% during the forecast period. This segment's growth potential is further bolstered by projects like the Russian Baltic Complex, which signifies a massive expansion in polymer production capabilities. The demand for sophisticated EPC solutions in constructing and revamping these facilities is substantial, attracting major players.

While the Upstream sector remains fundamental, and the Midstream sector critical for transportation, the current focus on value addition and technological advancement in processing positions the Downstream segment for accelerated growth and market leadership in the coming years.

Russia Oil and Gas EPC Industry Product Landscape

The Russia Oil and Gas EPC industry is characterized by the delivery of highly specialized and integrated solutions. Key "products" are comprehensive project execution services, encompassing feasibility studies, front-end engineering design (FEED), detailed engineering, procurement of materials and equipment, construction, commissioning, and start-up. Innovations focus on modular construction for faster deployment, advanced welding techniques for enhanced structural integrity, and digital tools for real-time project monitoring and control. Unique selling propositions often lie in a company's proven track record in challenging environments, adherence to stringent safety standards, and expertise in specific technological processes, such as cryogenic processing for LNG or complex hydrocracking for fuel production.

Key Drivers, Barriers & Challenges in Russia Oil and Gas EPC Industry

Key Drivers:

- Vast Hydrocarbon Reserves: Russia's significant oil and gas reserves necessitate continuous exploration, production, and processing infrastructure development.

- Government Support & National Projects: Strategic government initiatives aimed at energy security, export diversification, and industrial modernization provide a strong impetus for EPC projects.

- Technological Advancements: Adoption of cutting-edge technologies in exploration, extraction, and processing drives demand for specialized EPC expertise.

- Global Energy Demand: Continued global demand for oil and gas ensures sustained investment in production and infrastructure.

Barriers & Challenges:

- Geopolitical Sanctions & Regulatory Uncertainty: International sanctions create complexities in project financing, technology transfer, and international collaboration, impacting project execution and cost.

- Supply Chain Disruptions: Global and domestic supply chain volatility can lead to delays and increased costs for critical equipment and materials.

- Skilled Workforce Shortages: A potential scarcity of highly skilled engineers, technicians, and project managers poses a challenge for executing complex projects.

- Environmental Regulations & Sustainability Pressures: Increasing global and domestic emphasis on environmental protection requires significant investment in greener technologies and practices.

- Project Financing: Securing adequate and timely project financing, especially for large-scale ventures, can be a significant hurdle.

Emerging Opportunities in Russia Oil and Gas EPC Industry

Emerging opportunities in the Russia Oil and Gas EPC industry lie in the burgeoning liquefied natural gas (LNG) sector, particularly for small and medium-scale LNG facilities. Furthermore, the increasing focus on decarbonization presents opportunities in carbon capture, utilization, and storage (CCUS) projects within existing and new infrastructure. The development of renewable energy integration within oil and gas operations, such as utilizing solar or wind power for remote field operations, also represents an untapped market.

Growth Accelerators in the Russia Oil and Gas EPC Industry Industry

The long-term growth of the Russia Oil and Gas EPC industry is being accelerated by several key catalysts. Technological breakthroughs in areas like digital twins for enhanced project management and automation in construction are streamlining operations and reducing project timelines. Strategic partnerships between international and domestic EPC firms, despite geopolitical challenges, are crucial for knowledge transfer and risk mitigation. Furthermore, market expansion strategies focusing on emerging regions within Russia and diversification into related infrastructure projects, such as gas pipelines for domestic consumption and export, are significant growth drivers.

Key Players Shaping the Russia Oil and Gas EPC Industry Market

- Petrofac Limited

- Daelim Industrial Co Ltd

- Hyundai Heavy Industries Co Ltd

- Saipem SpA

- Renaissance Heavy Industries

- McDermott International Inc

- VELESSTROY

- Assystem SA

- Linde plc

- TechnipFMC PLC

Notable Milestones in Russia Oil and Gas EPC Industry Sector

- January 2022: DL E&C signed an agreement to participate in the Russian Baltic Complex Project, valued at USD 1,330 million. DL E&C will lead the design and procurement for the construction of the world's largest single-line polymer plant in Ust-Luga, capable of producing 3 million tons of polyethylene, 120,000 tons of butane, and 50,000 tons of hexane annually.

- January 2022: Mairie Tecnimont S.p.A., through its subsidiaries Tecnimont S.p.A. and MT Russia LLC, secured an EPC contract with Rosneft for the VGO Hydrocracking Complex at Ryazan Refining Company (RORC). This USD 1,240 million contract includes design, equipment supply, construction, commissioning, and project finance services, aiming to achieve a daily capacity of 40,000 barrels upon completion of Class 5 regulation compliance.

In-Depth Russia Oil and Gas EPC Industry Market Outlook

The outlook for the Russia Oil and Gas EPC industry remains robust, propelled by substantial ongoing and planned investments in energy infrastructure. Future market potential is significantly influenced by the nation's strategic imperative to enhance its refining capabilities, expand petrochemical production, and maintain its position as a global energy supplier. Strategic opportunities abound in the development of large-scale LNG projects and the integration of greener technologies into existing and new energy facilities. The industry's capacity to adapt to evolving regulatory landscapes and embrace digital transformation will be critical for sustained growth and competitive advantage.

Russia Oil and Gas EPC Industry Segmentation

-

1. Sector

- 1.1. Upstream

- 1.2. Midstream

- 1.3. Downstream

Russia Oil and Gas EPC Industry Segmentation By Geography

- 1. Russia

Russia Oil and Gas EPC Industry Regional Market Share

Geographic Coverage of Russia Oil and Gas EPC Industry

Russia Oil and Gas EPC Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Sector

- 5.1.1. Upstream

- 5.1.2. Midstream

- 5.1.3. Downstream

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Russia

- 5.1. Market Analysis, Insights and Forecast - by Sector

- 6. Russia Oil and Gas EPC Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Sector

- 6.1.1. Upstream

- 6.1.2. Midstream

- 6.1.3. Downstream

- 6.1. Market Analysis, Insights and Forecast - by Sector

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Petrofac Limited

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Daelim Industrial Co Ltd

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Hyundai Heavy Industries Co Ltd

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Saipem SpA

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Renaissance Heavy Industries

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 McDermott International Inc

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 VELESSTROY

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Assystem SA

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Linde plc

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 TechnipFMC PLC

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Petrofac Limited

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Russia Oil and Gas EPC Industry Revenue Breakdown (million, %) by Product 2025 & 2033

- Figure 2: Russia Oil and Gas EPC Industry Share (%) by Company 2025

List of Tables

- Table 1: Russia Oil and Gas EPC Industry Revenue million Forecast, by Sector 2020 & 2033

- Table 2: Russia Oil and Gas EPC Industry Revenue million Forecast, by Region 2020 & 2033

- Table 3: Russia Oil and Gas EPC Industry Revenue million Forecast, by Sector 2020 & 2033

- Table 4: Russia Oil and Gas EPC Industry Revenue million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Russia Oil and Gas EPC Industry?

The projected CAGR is approximately 4.1%.

2. Which companies are prominent players in the Russia Oil and Gas EPC Industry?

Key companies in the market include Petrofac Limited, Daelim Industrial Co Ltd, Hyundai Heavy Industries Co Ltd, Saipem SpA, Renaissance Heavy Industries, McDermott International Inc, VELESSTROY, Assystem SA, Linde plc, TechnipFMC PLC.

3. What are the main segments of the Russia Oil and Gas EPC Industry?

The market segments include Sector.

4. Can you provide details about the market size?

The market size is estimated to be USD 8973.3 million as of 2022.

5. What are some drivers contributing to market growth?

4.; Increasing Demand for Crude Oil and Natural Gas4.; Growing Emphasis on Safe. Economic. and Reliable Connectivity for Oil and Gas Exploration.

6. What are the notable trends driving market growth?

Midstream Segment to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; Technical Challenges Like Construction. Deep-Water Challenges. and High Construction Costs.

8. Can you provide examples of recent developments in the market?

January 2022: an agreement was signed by DL E&C to participate in the Russian Baltic Complex Project. The contract is worth USD 1.33 billion, and DL E&C will be responsible for the project's design and procurement of all equipment. Among the objectives of the project is to construct the largest polymer plant in the world on a single-line basis in Ust-Luga, 110 kilometers southwest of St. Petersburg. Upon completion, the plant will be able to produce 3 million tons of polyethylene, 120,000 tons of butane, and 50,000 tons of hexane each year.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Russia Oil and Gas EPC Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Russia Oil and Gas EPC Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Russia Oil and Gas EPC Industry?

To stay informed about further developments, trends, and reports in the Russia Oil and Gas EPC Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence