Key Insights

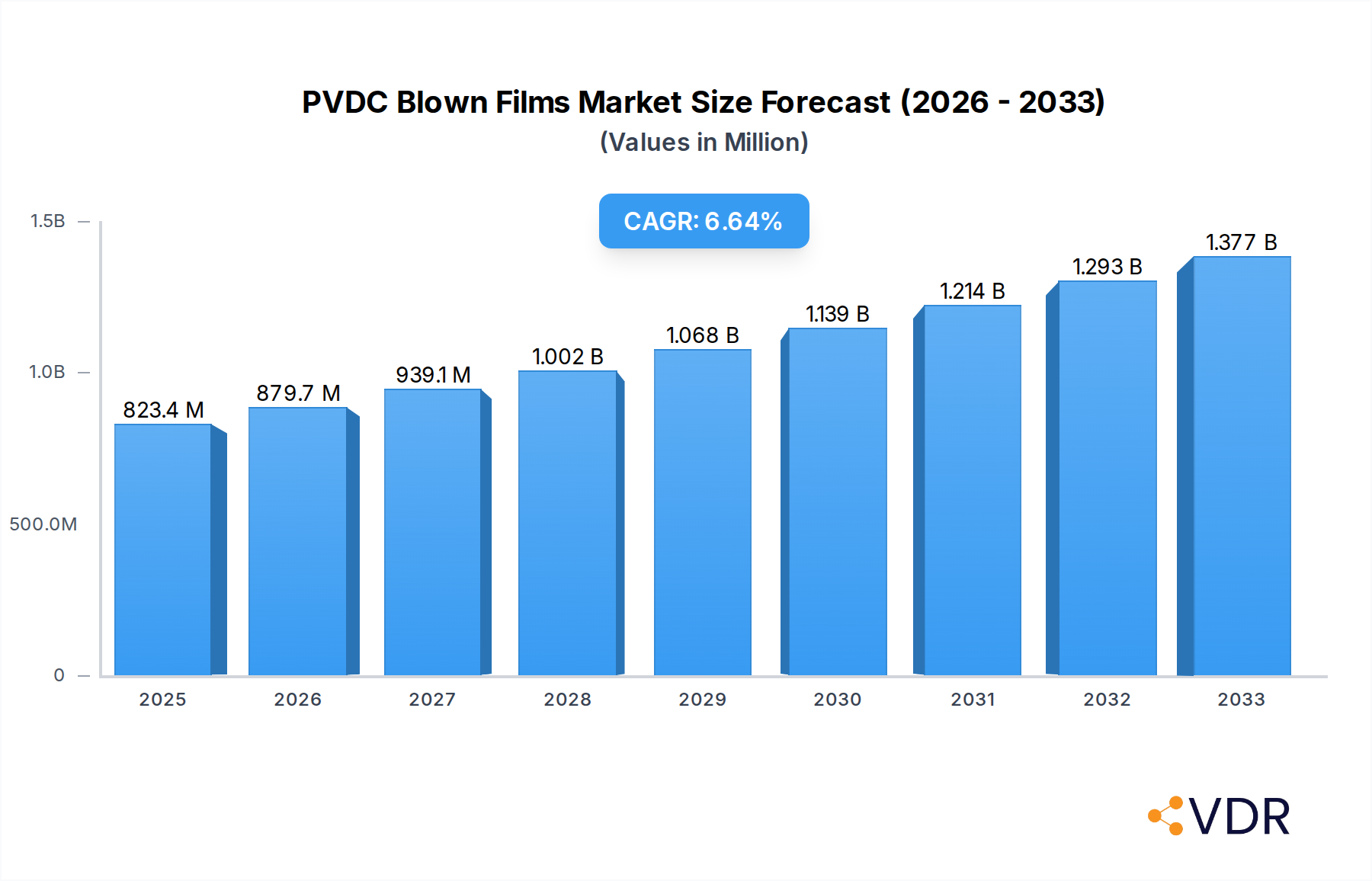

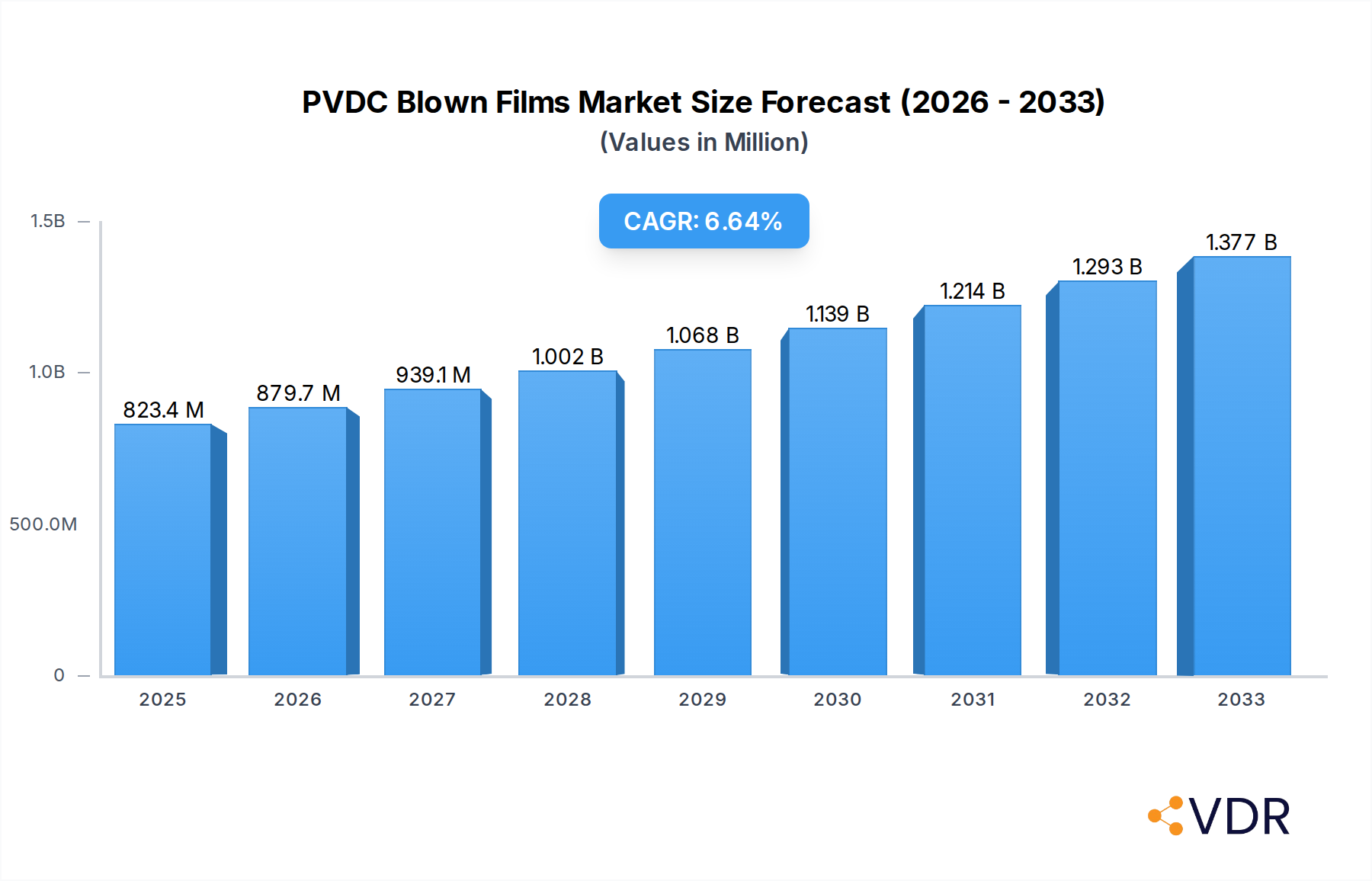

The global market for PVDC Blown Films is poised for robust growth, projected to reach $823.4 million by 2025, driven by a CAGR of 6.6% through 2033. This expansion is primarily fueled by the escalating demand for high-barrier packaging solutions across the food and pharmaceutical industries. PVDC's exceptional oxygen and moisture barrier properties make it indispensable for extending shelf life, preserving product integrity, and reducing food waste, thereby aligning with global sustainability efforts. The increasing consumer awareness regarding food safety and the growing prevalence of processed and convenience foods further bolster market demand. Moreover, the pharmaceutical sector's stringent requirements for drug stability and protection against environmental factors are a significant contributor to the adoption of PVDC blown films. Emerging economies, with their expanding middle class and increasing disposable incomes, represent a substantial growth opportunity, fostering greater consumption of packaged goods.

PVDC Blown Films Market Size (In Million)

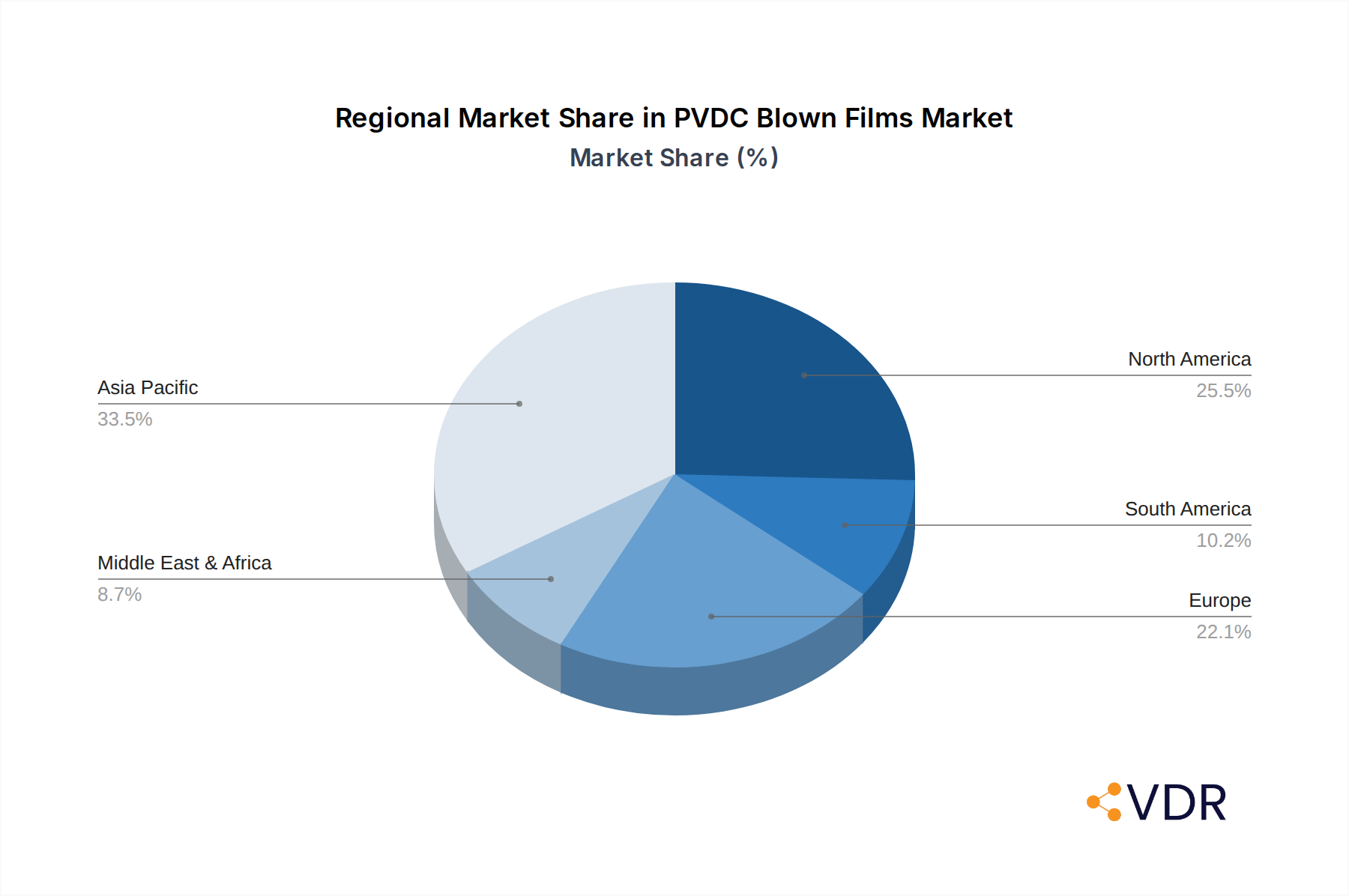

While the market demonstrates a positive trajectory, certain factors may influence its pace. Potential challenges include the fluctuating prices of raw materials, which can impact manufacturing costs and pricing strategies for PVDC blown films. Furthermore, the development and increasing adoption of alternative barrier materials, such as advanced polymers and bio-based plastics, could present competitive pressure. However, PVDC's established performance and cost-effectiveness in many critical applications are expected to sustain its market relevance. Key market players are actively investing in research and development to enhance film properties, explore sustainable manufacturing processes, and expand their geographical reach. The market segmentation reveals a strong emphasis on multilayer films due to their superior barrier performance, catering to specialized packaging needs. Regional dominance is anticipated in Asia Pacific, driven by its large population, rapid industrialization, and burgeoning consumer market, followed closely by North America and Europe, which have well-established packaging industries and high standards for product protection.

PVDC Blown Films Company Market Share

Here is the SEO-optimized report description for PVDC Blown Films, designed for maximum visibility and engagement with industry professionals, presented in millions of units where applicable, and without placeholders for further modification.

This in-depth market research report provides a definitive analysis of the global PVDC Blown Films market, offering critical insights into its dynamics, growth trajectories, and future potential. Covering the period from 2019 to 2033, with a base year of 2025 and a forecast period of 2025–2033, this report is an indispensable resource for manufacturers, suppliers, investors, and stakeholders seeking to understand and capitalize on evolving market trends. Our analysis delves into parent and child market segments, regional dominance, technological advancements, and competitive landscapes to deliver a holistic view of the PVDC Blown Films industry.

PVDC Blown Films Market Dynamics & Structure

The PVDC Blown Films market exhibits a moderate concentration, with key players like Dow Chemical, Asahi Kasei, Kureha, and Syensqo holding significant influence. Technological innovation is a primary driver, with advancements in multilayer film extrusion and barrier property enhancement continually reshaping product offerings. Regulatory frameworks, particularly concerning food contact materials and sustainability, are increasingly shaping market development. Competitive product substitutes, such as EVOH and PET films, present both challenges and opportunities, prompting continuous product development. End-user demographics in the food packaging and pharmaceutical packaging sectors are evolving, demanding enhanced shelf-life, safety, and convenience. Mergers and acquisitions (M&A) trends indicate strategic consolidation, with recent activities by companies like Frachem Technologies and Tianjin Kangtai Plastic Packing signaling a push for vertical integration and expanded market reach. The market is also influenced by evolving consumer preferences for sustainable and high-performance packaging solutions. Innovation barriers primarily stem from the capital-intensive nature of advanced film extrusion technologies and stringent regulatory compliance requirements.

- Market Concentration: Moderate, with a few dominant global players.

- Technological Drivers: Enhanced barrier properties, co-extrusion technology, and recyclability innovations.

- Regulatory Frameworks: Increasing scrutiny on food contact safety and environmental impact.

- Competitive Substitutes: EVOH, PET, and other high-barrier polymer films.

- End-User Demographics: Growing demand from sophisticated food preservation and pharmaceutical applications.

- M&A Trends: Strategic acquisitions to gain market share and technological capabilities.

PVDC Blown Films Growth Trends & Insights

The PVDC Blown Films market is poised for robust growth, projected to expand at a Compound Annual Growth Rate (CAGR) of approximately 5.8% from 2025 to 2033. This expansion is fueled by escalating demand for superior barrier properties in food and pharmaceutical packaging, where PVDC's excellent oxygen and moisture barrier capabilities are paramount for extending shelf life and ensuring product integrity. The adoption rate of advanced multilayer PVDC blown films is accelerating, driven by the need for sophisticated packaging solutions that meet stringent safety standards and consumer expectations for freshness. Technological disruptions, including improvements in co-extrusion processes and the development of more sustainable PVDC formulations, are enhancing the material's appeal. Consumer behavior shifts towards convenience and premium food products are indirectly boosting the demand for high-performance packaging that maintains product quality. The market penetration of PVDC blown films in specialized packaging applications is expected to deepen significantly. The global market size for PVDC blown films is estimated to reach approximately USD 3,500 million in 2025, with projections indicating a rise to over USD 5,000 million by the end of the forecast period. This growth is underpinned by a steady increase in global food consumption and the expanding pharmaceutical industry, both of which heavily rely on effective packaging to minimize spoilage and maintain efficacy. The inherent properties of PVDC, such as its low permeability to gases, vapors, and aromas, make it a preferred choice for applications requiring extended shelf stability, like processed meats, cheeses, and sensitive pharmaceuticals. Furthermore, ongoing research into enhancing the recyclability and biodegradability of PVDC-containing films, though challenging, is a critical area of development that could further accelerate market adoption and address environmental concerns. The increasing sophistication of packaging machinery also allows for the more efficient and cost-effective production of multilayer films incorporating PVDC, making them more accessible to a wider range of manufacturers.

Dominant Regions, Countries, or Segments in PVDC Blown Films

The Food Packaging segment is the primary growth engine for the PVDC Blown Films market, driven by escalating demand for extended shelf-life and preservation of perishable goods globally. Within this segment, multilayer films are particularly dominant, offering superior barrier protection that significantly reduces food spoilage and waste. North America and Europe currently lead in terms of market share due to their well-established food processing industries, stringent food safety regulations, and high consumer demand for premium, long-lasting food products. However, the Asia-Pacific region is exhibiting the fastest growth, propelled by rapid economic development, a burgeoning middle class, and increasing adoption of Western dietary habits, leading to a greater need for sophisticated food packaging.

- Leading Segment (Application): Food Packaging, accounting for an estimated 65% of the market share in 2025.

- Dominant Type: Multilayer Film, representing approximately 75% of the total PVDC blown film production due to its enhanced barrier properties.

- Key Drivers in Asia-Pacific:

- Rapidly expanding processed food industry.

- Increasing disposable incomes and changing consumer preferences.

- Government initiatives to improve food safety and reduce waste.

- Growth in export-oriented food manufacturing.

- Market Share in Leading Regions (Estimated 2025):

- North America: ~25%

- Europe: ~23%

- Asia-Pacific: ~28% (with highest projected growth rate)

- Growth Potential in Pharmaceutical Packaging: Significant, driven by the need for sterile and moisture-resistant packaging for drugs and medical devices.

- Emerging Applications: Industrial applications requiring high barrier properties, such as for electronics and chemicals.

PVDC Blown Films Product Landscape

Innovations in PVDC blown films are primarily focused on enhancing barrier performance, improving processability, and addressing sustainability concerns. Manufacturers are developing advanced multilayer structures that optimize the combination of PVDC with other polymers like PE, PP, and PET to achieve specific performance characteristics. Applications range from high-barrier flexible packaging for processed meats, cheeses, and snacks, to specialized pharmaceutical blister packs and medical device packaging where sterility and moisture protection are critical. Performance metrics such as oxygen transmission rate (OTR) and water vapor transmission rate (WVTR) are continuously being improved, often reaching values as low as 0.1 cc/m²/day and 0.1 g/m²/day respectively, providing unmatched product protection and extended shelf life. The unique selling proposition of PVDC films lies in their exceptional balance of barrier properties, thermal stability, and sealability.

Key Drivers, Barriers & Challenges in PVDC Blown Films

Key Drivers:

- Unparalleled Barrier Properties: Superior protection against oxygen, moisture, and aromas, crucial for food and pharmaceutical preservation.

- Extended Shelf Life: Direct impact on reducing food waste and ensuring product efficacy.

- Regulatory Compliance: Meeting stringent global standards for food contact and pharmaceutical packaging safety.

- Growing Demand in Emerging Markets: Increasing consumption of processed foods and pharmaceuticals in developing economies.

- Technological Advancements: Improvements in co-extrusion techniques and film formulation.

Barriers & Challenges:

- Environmental Concerns & Recyclability: PVDC's inherent properties can make it challenging to recycle, leading to a focus on alternative materials or advanced recycling solutions.

- Cost Competitiveness: Higher production costs compared to some commodity plastics can be a barrier in price-sensitive applications.

- Supply Chain Volatility: Dependence on specific raw material suppliers and potential geopolitical factors influencing availability.

- Competition from Alternatives: Growing availability and performance improvements in competing barrier materials like EVOH and specialized polyolefins.

- Processing Complexity: Certain grades of PVDC may require specific processing conditions, impacting operational efficiency for some manufacturers.

Emerging Opportunities in PVDC Blown Films

Emerging opportunities lie in the development of more sustainable PVDC formulations and enhanced recyclability solutions. Innovations in compatibilization agents and multilayer film design are enabling the incorporation of higher percentages of recycled content. Untapped markets in specialized medical packaging, such as for sensitive biologicals and advanced drug delivery systems, present significant growth potential. Evolving consumer preferences for transparent, high-barrier packaging that clearly showcases product quality also offer opportunities for PVDC films with improved clarity and aesthetics. The development of thinner, yet equally effective PVDC films can lead to material savings and reduced environmental footprint, aligning with sustainability goals.

Growth Accelerators in the PVDC Blown Films Industry

Long-term growth in the PVDC Blown Films industry will be significantly accelerated by breakthroughs in chemical recycling technologies that specifically target PVDC, making it more economically viable to recover and reuse the material. Strategic partnerships between PVDC manufacturers and food/pharmaceutical companies will foster the co-development of tailored packaging solutions that address specific product protection needs and sustainability targets. Market expansion strategies focusing on regions with rapidly growing middle classes and increasing demand for packaged goods will be crucial. Furthermore, advancements in additive technologies that enhance UV resistance or antimicrobial properties of PVDC films will open new application avenues and premium market segments.

Key Players Shaping the PVDC Blown Films Market

- Dow Chemical

- Asahi Kasei

- Kureha

- Syensqo

- Supratama

- Shuanghui

- Juhua Group

- Tipack

- Frachem Technologies

- Tianjin Kangtai Plastic Packing

Notable Milestones in PVDC Blown Films Sector

- 2019: Launch of advanced co-extrusion technologies enabling higher PVDC content in multilayer films.

- 2020: Increased investment in R&D for sustainable PVDC solutions and chemical recycling feasibility studies.

- 2021: Major food packaging companies adopt PVDC multilayer films for extended shelf-life meat products, boosting demand.

- 2022: Syensqo (formerly Solvay's specialty polymers business) announces strategic focus on high-performance barrier solutions, including PVDC.

- 2023: Frachem Technologies expands its production capacity for specialized PVDC barrier films.

- 2024: Tianjin Kangtai Plastic Packing partners with a major pharmaceutical firm to develop advanced blister packaging solutions.

- 2025 (Estimated): Introduction of novel PVDC formulations with improved UV resistance for specialized applications.

In-Depth PVDC Blown Films Market Outlook

The future outlook for the PVDC Blown Films market is exceptionally positive, driven by its indispensable role in protecting high-value food and pharmaceutical products. Key growth accelerators include the continuous pursuit of enhanced barrier performance for extended shelf life, which directly combats food waste and ensures drug efficacy. Strategic alliances between key players and end-users will accelerate the adoption of innovative, customized packaging solutions. The market's expansion into emerging economies, fueled by rising disposable incomes and urbanization, presents substantial untapped potential. Furthermore, ongoing advancements in processing technologies and the crucial development of more sustainable and recyclable PVDC-based materials are poised to address environmental concerns and reinforce its market position in the long term.

PVDC Blown Films Segmentation

-

1. Application

- 1.1. Food Packaging

- 1.2. Pharmaceutical Packaging

- 1.3. Others

-

2. Types

- 2.1. Multilayer Film

- 2.2. Monolayer Film

PVDC Blown Films Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

PVDC Blown Films Regional Market Share

Geographic Coverage of PVDC Blown Films

PVDC Blown Films REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Food Packaging

- 5.1.2. Pharmaceutical Packaging

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Multilayer Film

- 5.2.2. Monolayer Film

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global PVDC Blown Films Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Food Packaging

- 6.1.2. Pharmaceutical Packaging

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Multilayer Film

- 6.2.2. Monolayer Film

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America PVDC Blown Films Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Food Packaging

- 7.1.2. Pharmaceutical Packaging

- 7.1.3. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Multilayer Film

- 7.2.2. Monolayer Film

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America PVDC Blown Films Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Food Packaging

- 8.1.2. Pharmaceutical Packaging

- 8.1.3. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Multilayer Film

- 8.2.2. Monolayer Film

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe PVDC Blown Films Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Food Packaging

- 9.1.2. Pharmaceutical Packaging

- 9.1.3. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Multilayer Film

- 9.2.2. Monolayer Film

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa PVDC Blown Films Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Food Packaging

- 10.1.2. Pharmaceutical Packaging

- 10.1.3. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Multilayer Film

- 10.2.2. Monolayer Film

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific PVDC Blown Films Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Food Packaging

- 11.1.2. Pharmaceutical Packaging

- 11.1.3. Others

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Multilayer Film

- 11.2.2. Monolayer Film

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Dow Chemical

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Asahi Kasei

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Kureha

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Syensqo

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Supratama

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Shuanghui

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Juhua Group

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Tipack

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Frachem Technologies

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Tianjin Kangtai Plastic Packing

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Dow Chemical

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global PVDC Blown Films Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America PVDC Blown Films Revenue (billion), by Application 2025 & 2033

- Figure 3: North America PVDC Blown Films Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America PVDC Blown Films Revenue (billion), by Types 2025 & 2033

- Figure 5: North America PVDC Blown Films Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America PVDC Blown Films Revenue (billion), by Country 2025 & 2033

- Figure 7: North America PVDC Blown Films Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America PVDC Blown Films Revenue (billion), by Application 2025 & 2033

- Figure 9: South America PVDC Blown Films Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America PVDC Blown Films Revenue (billion), by Types 2025 & 2033

- Figure 11: South America PVDC Blown Films Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America PVDC Blown Films Revenue (billion), by Country 2025 & 2033

- Figure 13: South America PVDC Blown Films Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe PVDC Blown Films Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe PVDC Blown Films Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe PVDC Blown Films Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe PVDC Blown Films Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe PVDC Blown Films Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe PVDC Blown Films Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa PVDC Blown Films Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa PVDC Blown Films Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa PVDC Blown Films Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa PVDC Blown Films Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa PVDC Blown Films Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa PVDC Blown Films Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific PVDC Blown Films Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific PVDC Blown Films Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific PVDC Blown Films Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific PVDC Blown Films Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific PVDC Blown Films Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific PVDC Blown Films Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global PVDC Blown Films Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global PVDC Blown Films Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global PVDC Blown Films Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global PVDC Blown Films Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global PVDC Blown Films Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global PVDC Blown Films Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States PVDC Blown Films Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada PVDC Blown Films Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico PVDC Blown Films Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global PVDC Blown Films Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global PVDC Blown Films Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global PVDC Blown Films Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil PVDC Blown Films Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina PVDC Blown Films Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America PVDC Blown Films Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global PVDC Blown Films Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global PVDC Blown Films Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global PVDC Blown Films Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom PVDC Blown Films Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany PVDC Blown Films Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France PVDC Blown Films Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy PVDC Blown Films Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain PVDC Blown Films Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia PVDC Blown Films Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux PVDC Blown Films Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics PVDC Blown Films Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe PVDC Blown Films Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global PVDC Blown Films Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global PVDC Blown Films Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global PVDC Blown Films Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey PVDC Blown Films Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel PVDC Blown Films Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC PVDC Blown Films Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa PVDC Blown Films Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa PVDC Blown Films Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa PVDC Blown Films Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global PVDC Blown Films Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global PVDC Blown Films Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global PVDC Blown Films Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China PVDC Blown Films Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India PVDC Blown Films Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan PVDC Blown Films Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea PVDC Blown Films Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN PVDC Blown Films Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania PVDC Blown Films Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific PVDC Blown Films Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the PVDC Blown Films?

The projected CAGR is approximately 3.1%.

2. Which companies are prominent players in the PVDC Blown Films?

Key companies in the market include Dow Chemical, Asahi Kasei, Kureha, Syensqo, Supratama, Shuanghui, Juhua Group, Tipack, Frachem Technologies, Tianjin Kangtai Plastic Packing.

3. What are the main segments of the PVDC Blown Films?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 10 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "PVDC Blown Films," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the PVDC Blown Films report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the PVDC Blown Films?

To stay informed about further developments, trends, and reports in the PVDC Blown Films, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence