Key Insights

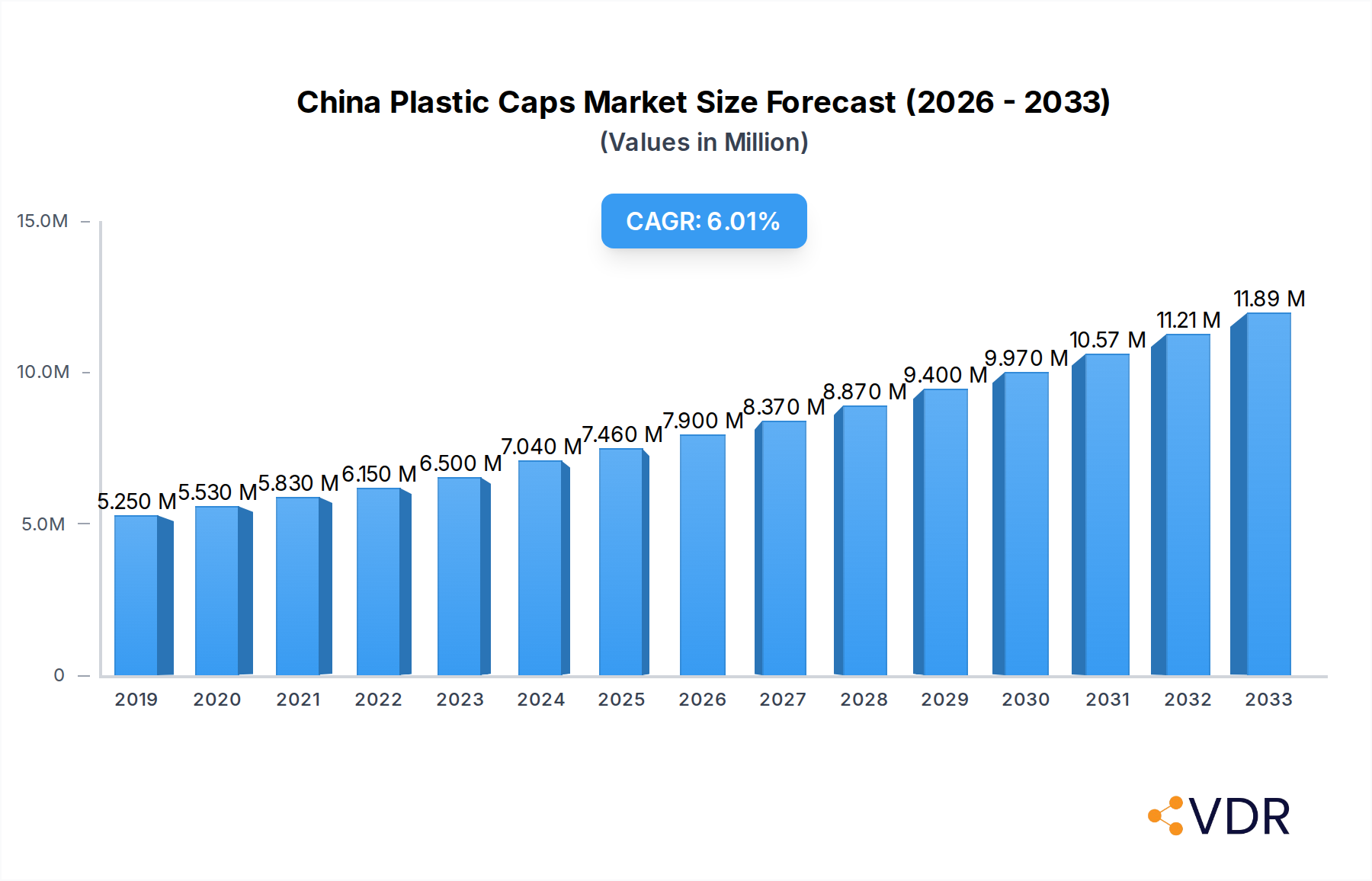

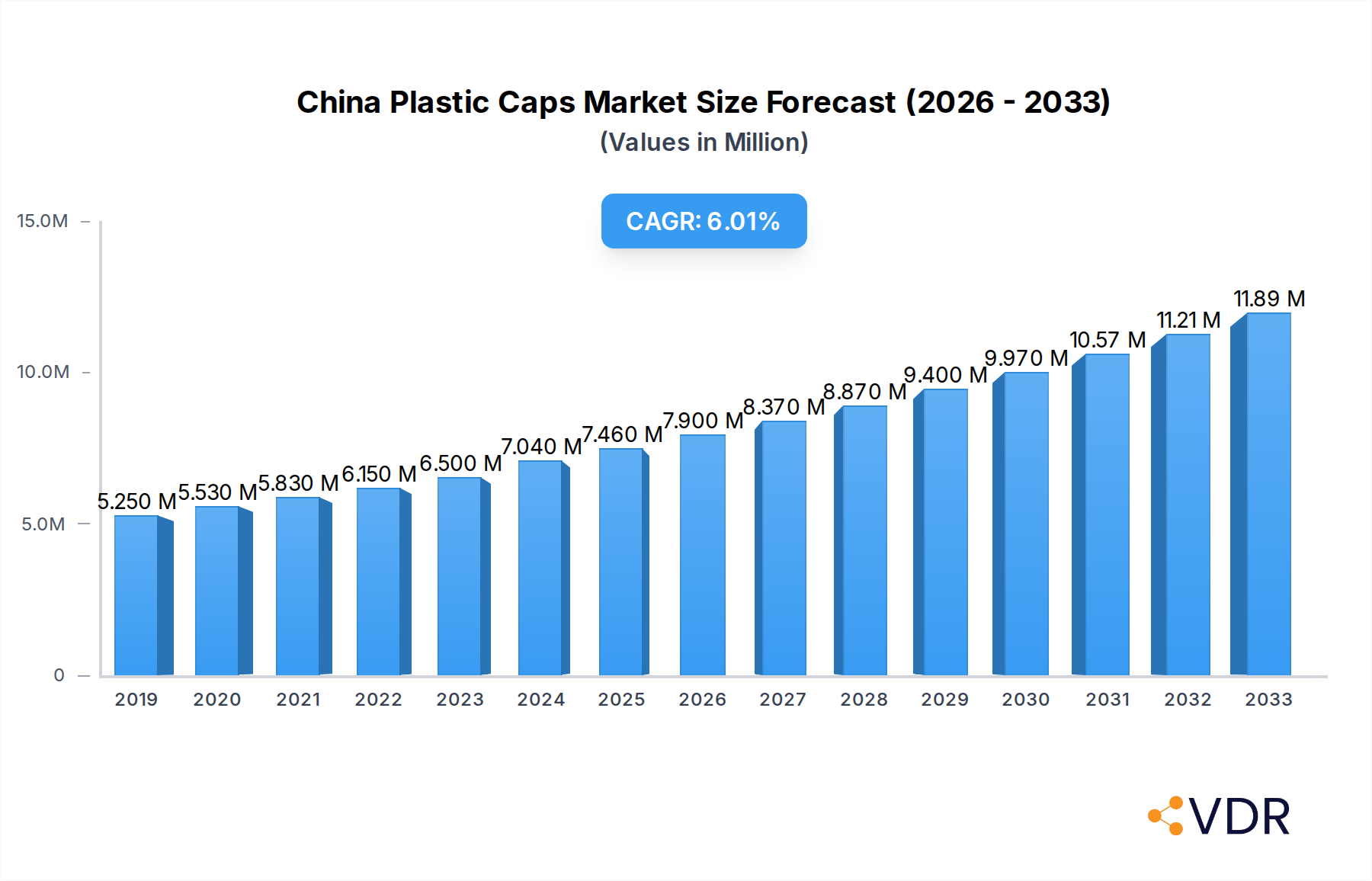

The China Plastic Caps & Closures Industry is experiencing robust growth, projected to reach an estimated USD 7.04 billion by 2024, with a compelling Compound Annual Growth Rate (CAGR) of 5.7% during the forecast period of 2025-2033. This expansion is significantly driven by the burgeoning demand from the food and beverage sector, which constitutes a substantial portion of the market. The increasing consumer preference for packaged goods, coupled with advancements in packaging technologies that enhance product shelf-life and safety, are key accelerators. Furthermore, the pharmaceutical and cosmetics industries are also contributing to market dynamism, seeking innovative and secure closure solutions that meet stringent regulatory standards and evolving consumer aesthetics. The rise in disposable incomes and the subsequent growth in organized retail further fuel the need for reliable and attractive plastic caps and closures across various product categories.

China Plastic Caps & Closures Industry Market Size (In Million)

Despite a generally positive outlook, the industry faces certain restraints. Fluctuations in raw material prices, particularly for key polymers like Polyethylene Terephthalate (PET) and Polypropylene (PP), can impact profit margins. Moreover, increasing environmental concerns and growing pressure for sustainable packaging solutions are prompting a shift towards recyclable and biodegradable alternatives, necessitating significant investment in research and development by manufacturers. The competitive landscape, characterized by a mix of large global players and numerous domestic manufacturers, also poses challenges in terms of market penetration and price pressures. However, the continuous innovation in product design, enhanced functionality, and the adoption of advanced manufacturing processes are expected to outweigh these challenges, ensuring sustained growth and market expansion. The industry's ability to adapt to these evolving demands and regulatory landscapes will be crucial for its continued success.

China Plastic Caps & Closures Industry Company Market Share

This in-depth report provides a definitive analysis of the China plastic caps and closures market, a critical component of the global packaging industry. Covering the historical period of 2019-2024, base year 2025, and a robust forecast period of 2025-2033, this study offers unparalleled insights into market size, growth drivers, challenges, and competitive landscapes. We delve into the intricate dynamics of the parent market and explore the growth potential within child markets, offering a holistic view for industry stakeholders. With a focus on polyethylene terephthalate (PET) caps, polypropylene (PP) closures, HDPE caps, and LDPE closures, alongside key industry verticals like food packaging, beverage caps, pharmaceutical closures, and cosmetic packaging, this report is essential for strategic planning and investment decisions.

China Plastic Caps & Closures Industry Market Dynamics & Structure

The China plastic caps and closures market is characterized by a moderately concentrated structure, with leading global and domestic players vying for market share. Technological innovation, particularly in areas like smart packaging, tamper-evident features, and sustainable materials, acts as a significant driver, pushing companies to invest heavily in R&D. Stringent regulatory frameworks, focusing on food safety, environmental impact, and material traceability, are shaping product development and manufacturing processes. Competitive product substitutes, such as metal closures and alternative packaging formats, exert pressure, necessitating continuous improvement in plastic cap and closure performance and cost-effectiveness. End-user demographics are evolving, with an increasing demand for convenience, shelf-appeal, and sustainability across various industries. Mergers and acquisitions (M&A) trends are active, driven by the pursuit of market consolidation, technological acquisition, and expanded geographic reach within this dynamic plastic caps and closures China landscape.

- Market Concentration: Moderate, with key global players and significant domestic manufacturers.

- Technological Innovation Drivers: Smart packaging, anti-counterfeiting features, lightweighting, sustainable material adoption.

- Regulatory Frameworks: Food safety standards (e.g., GB standards), environmental protection policies, and recycling initiatives.

- Competitive Product Substitutes: Metal closures, glass bottles, carton packaging, pouches.

- End-User Demographics: Growing middle class, rising disposable incomes, increasing demand for premium and convenient packaging solutions.

- M&A Trends: Strategic acquisitions for technology, market access, and capacity expansion. For instance, the proposed acquisition of HCP by Carlyle highlights consolidation efforts in the cosmetic packaging sector.

China Plastic Caps & Closures Industry Growth Trends & Insights

The China plastic caps and closures market is poised for substantial growth, driven by burgeoning domestic consumption and the expansion of key end-use industries. The market size is projected to witness a robust Compound Annual Growth Rate (CAGR) of xx% during the forecast period of 2025-2033. Adoption rates for innovative closure solutions, such as those offering enhanced tamper evidence and convenience, are steadily increasing, fueled by evolving consumer preferences and brand requirements. Technological disruptions, including advancements in injection molding techniques, automation, and the integration of IoT capabilities for supply chain tracking, are reshaping the manufacturing landscape. Consumer behavior shifts, emphasizing health and wellness, convenience, and a growing awareness of environmental sustainability, are significantly influencing product demand. For example, Nestle's successful launch of QR code closure solutions in China, later expanded to Vietnam, underscores the trend towards integrated digital functionalities. The market penetration of specialized closures for niche applications, such as leak-proof pharmaceutical bottles and child-resistant caps, is also on an upward trajectory.

Dominant Regions, Countries, or Segments in China Plastic Caps & Closures Industry

The China plastic caps and closures industry is experiencing dominant growth driven by the Food and Beverages sector, which consistently represents the largest segment in terms of volume and value. This dominance is attributable to the sheer scale of China's food and beverage production and consumption, necessitating vast quantities of reliable and safe packaging solutions. The Polypropylene (PP) raw material segment is also a significant contributor to market growth, given its versatility, cost-effectiveness, and suitability for a wide range of cap and closure applications, from beverage bottles to household product containers. Key drivers for the food and beverage sector's dominance include:

- Economic Policies: Government support for domestic food processing and agricultural industries.

- Infrastructure: Well-developed logistics and distribution networks facilitating efficient product movement.

- Consumer Demand: A rapidly expanding middle class with increasing disposable income, driving demand for packaged food and beverages.

- Product Innovation: Manufacturers continually introducing new food and beverage products requiring specialized and attractive packaging.

Within the Cosmetics and Household industry vertical, there is also substantial growth, particularly for premium and specialized closures. The Polyethylene Terephthalate (PET) segment remains crucial, especially for beverage packaging, due to its clarity, strength, and barrier properties. However, the growth potential of HDPE and LDPE is significant in applications requiring flexibility and impact resistance. The dynamic growth of these segments is further propelled by:

- Rising Disposable Incomes: Leading to increased consumer spending on cosmetics, personal care items, and household products.

- E-commerce Growth: Driving demand for robust and secure packaging for online retail.

- Brand Differentiation: Companies seeking unique and functional closures to enhance brand appeal and consumer experience.

China Plastic Caps & Closures Industry Product Landscape

The product landscape of the China plastic caps and closures industry is marked by continuous innovation and diversification. Manufacturers are actively developing advanced solutions, including tamper-evident seals for enhanced product security, flip-top caps for ease of use, and child-resistant closures to meet safety regulations. The application scope extends across a broad spectrum, from rigid beverage bottles and flexible sauce sachets to sophisticated cosmetic jars and pharmaceutical vials. Performance metrics such as seal integrity, dispensing efficiency, and material durability are paramount. Unique selling propositions often revolve around sustainable material integration, such as recycled PET (rPET) closures, and smart features like QR codes for traceability and consumer engagement, exemplified by Nestle's innovative QR code closure solution. Technological advancements in multi-component molding and precision engineering are enabling the creation of highly functional and aesthetically pleasing closures.

Key Drivers, Barriers & Challenges in China Plastic Caps & Closures Industry

Key Drivers:

- Robust Demand from Food & Beverage Sector: Continued expansion of China's food and beverage industry drives significant demand for closures.

- Growth in E-commerce: Increased online retail necessitates secure and reliable packaging solutions.

- Rising Disposable Incomes: Higher consumer spending on packaged goods, cosmetics, and pharmaceuticals.

- Technological Advancements: Innovations in materials, manufacturing processes, and smart packaging features.

- Government Support for Sustainability: Growing emphasis on recyclable and eco-friendly packaging solutions.

Barriers & Challenges:

- Raw Material Price Volatility: Fluctuations in the cost of petrochemicals impact profitability.

- Intense Competition: A highly competitive market with numerous domestic and international players leading to price pressures.

- Regulatory Compliance: Evolving environmental regulations and food safety standards require continuous adaptation.

- Supply Chain Disruptions: Global events can impact raw material availability and logistics.

- Counterfeit Products: Challenges in preventing the replication of branded caps and closures.

Emerging Opportunities in China Plastic Caps & Closures Industry

Emerging opportunities in the China plastic caps and closures industry lie in the expanding market for sustainable and bio-based materials, driven by increasing consumer and regulatory demand for eco-friendly packaging. The development of smart closures with integrated sensors, RFID tags, and NFC capabilities presents a significant avenue for growth, enabling enhanced product tracking, authentication, and consumer engagement. The pharmaceutical and nutraceutical sectors offer substantial opportunities for specialized, high-barrier, and tamper-evident closures. Furthermore, the growth of the personal care and premium cosmetics market in China presents a niche for aesthetically designed and functionally superior closures, catering to evolving consumer preferences for luxury and convenience. Untapped rural markets also represent a growing opportunity as urbanization and rising incomes increase demand for packaged goods.

Growth Accelerators in the China Plastic Caps & Closures Industry Industry

Long-term growth in the China plastic caps and closures industry is being significantly accelerated by several catalysts. Technological breakthroughs in material science are enabling the development of lighter, stronger, and more sustainable plastic materials for closures, meeting environmental mandates and consumer expectations. Strategic partnerships between raw material suppliers, closure manufacturers, and brand owners are fostering innovation and co-development of bespoke packaging solutions. Market expansion strategies, particularly focusing on emerging consumer segments and less saturated regional markets within China, are driving volume growth. The increasing adoption of automation and digitalization in manufacturing processes is enhancing efficiency, reducing costs, and improving product quality, further accelerating growth.

Key Players Shaping the China Plastic Caps & Closures Industry Market

- Aptar Group Inc

- Yuyao Friend Packing Co Ltd

- Amcor Ltd

- Fuzhou Kinglong Commodity & Cosmetic Co Ltd

- Bericap GmbH

- Albea Group

- Silgan White Cap (Shanghai) Co

- Shandong Haishengyu Plastics Industry Co Ltd

- Crown Asia Pacific Holdings Limited

- Berry Global Inc

Notable Milestones in China Plastic Caps & Closures Industry Sector

- May 2022: Carlyle plans to acquire China-based cosmetic packaging company HCP, a move aimed at strengthening R&D capabilities and strategic acquisitions within the cosmetic packaging sector, impacting brands like Estée Lauder, L'Oréal, and Shiseido.

- August 2021: Nestle successfully launched its QR code closure solution in China, which was subsequently introduced in Vietnam, featuring scannable QR codes for reward point redemption via Zalo, showcasing innovation in consumer engagement through packaging.

In-Depth China Plastic Caps & Closures Industry Market Outlook

The future market potential for the China plastic caps and closures industry is exceptionally promising, driven by sustained economic growth, evolving consumer lifestyles, and a strong emphasis on sustainable packaging solutions. The continuous demand from the food, beverage, pharmaceutical, and cosmetic sectors, coupled with the increasing adoption of advanced packaging technologies, will serve as significant growth accelerators. Strategic investments in R&D for innovative materials and smart closures, alongside proactive adaptation to environmental regulations, will be crucial for market leaders. The industry is poised for further consolidation and innovation, creating a dynamic landscape of opportunity for both established players and new entrants focused on delivering value-added, sustainable, and high-performance closure solutions.

China Plastic Caps & Closures Industry Segmentation

-

1. Raw Material

- 1.1. Polyethylene Terephthalate

- 1.2. Polypropylene

- 1.3. HDPE and LDPE

- 1.4. Other Ra

-

2. Industry Vertical

- 2.1. Food

- 2.2. Beverages

- 2.3. Pharmaceutical

- 2.4. Cosmetics and Household

- 2.5. Other In

China Plastic Caps & Closures Industry Segmentation By Geography

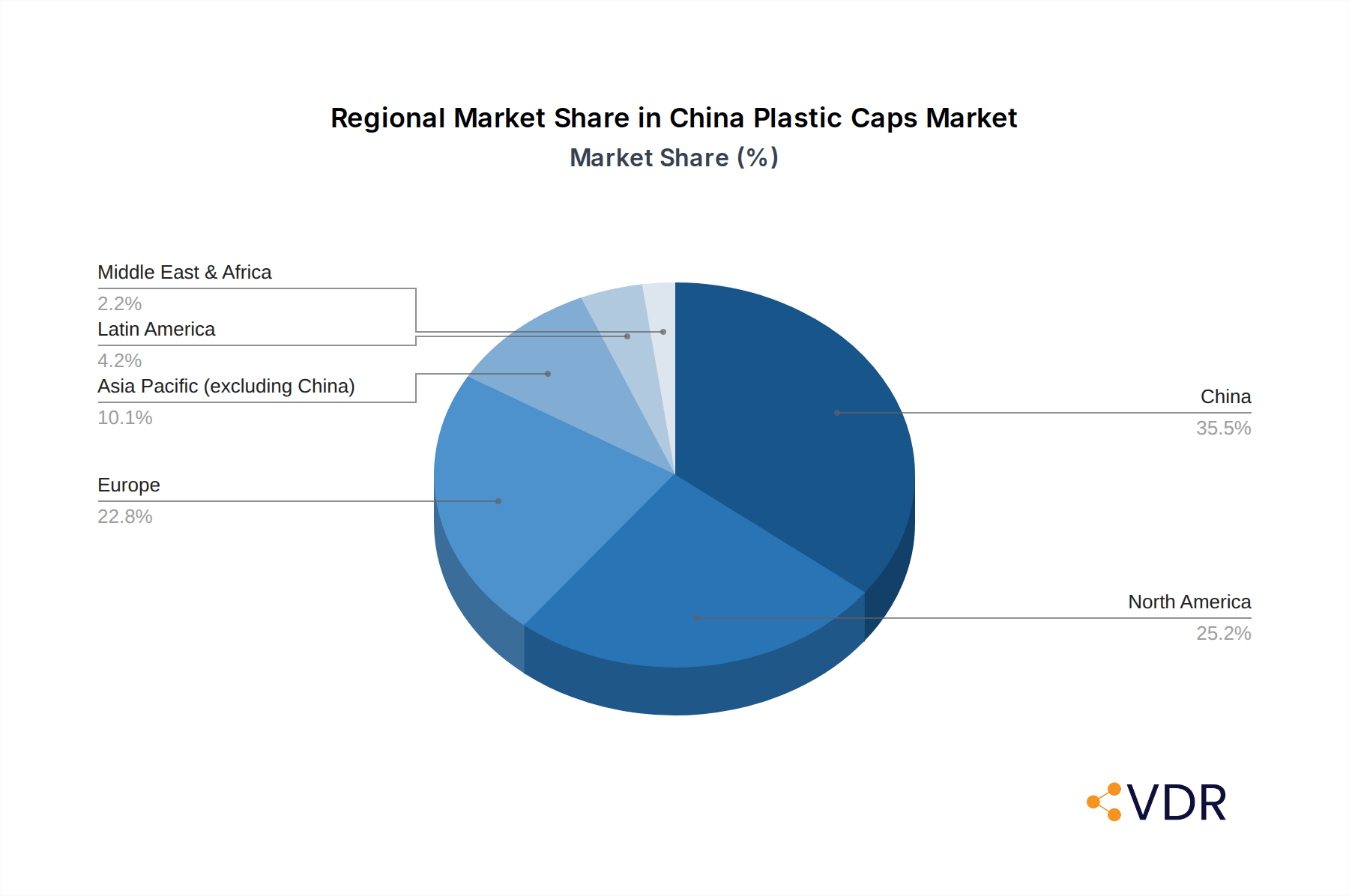

- 1. China

China Plastic Caps & Closures Industry Regional Market Share

Geographic Coverage of China Plastic Caps & Closures Industry

China Plastic Caps & Closures Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Raw Material

- 5.1.1. Polyethylene Terephthalate

- 5.1.2. Polypropylene

- 5.1.3. HDPE and LDPE

- 5.1.4. Other Ra

- 5.2. Market Analysis, Insights and Forecast - by Industry Vertical

- 5.2.1. Food

- 5.2.2. Beverages

- 5.2.3. Pharmaceutical

- 5.2.4. Cosmetics and Household

- 5.2.5. Other In

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. China

- 5.1. Market Analysis, Insights and Forecast - by Raw Material

- 6. China Plastic Caps & Closures Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Raw Material

- 6.1.1. Polyethylene Terephthalate

- 6.1.2. Polypropylene

- 6.1.3. HDPE and LDPE

- 6.1.4. Other Ra

- 6.2. Market Analysis, Insights and Forecast - by Industry Vertical

- 6.2.1. Food

- 6.2.2. Beverages

- 6.2.3. Pharmaceutical

- 6.2.4. Cosmetics and Household

- 6.2.5. Other In

- 6.1. Market Analysis, Insights and Forecast - by Raw Material

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Aptar Group Inc

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Yuyao Friend Packing Co Ltd

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Amcor Ltd*List Not Exhaustive

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Fuzhou Kinglong Commodity & Cosmetic Co Ltd

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Bericap GmbH

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Albea Group

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Silgan White Cap (Shanghai) Co

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Shandong Haishengyu Plastics Industry Co Ltd

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Crown Asia Pacific Holdings Limited

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Berry Global Inc

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Aptar Group Inc

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: China Plastic Caps & Closures Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: China Plastic Caps & Closures Industry Share (%) by Company 2025

List of Tables

- Table 1: China Plastic Caps & Closures Industry Revenue billion Forecast, by Raw Material 2020 & 2033

- Table 2: China Plastic Caps & Closures Industry Revenue billion Forecast, by Industry Vertical 2020 & 2033

- Table 3: China Plastic Caps & Closures Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: China Plastic Caps & Closures Industry Revenue billion Forecast, by Raw Material 2020 & 2033

- Table 5: China Plastic Caps & Closures Industry Revenue billion Forecast, by Industry Vertical 2020 & 2033

- Table 6: China Plastic Caps & Closures Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the China Plastic Caps & Closures Industry?

The projected CAGR is approximately 5.7%.

2. Which companies are prominent players in the China Plastic Caps & Closures Industry?

Key companies in the market include Aptar Group Inc, Yuyao Friend Packing Co Ltd, Amcor Ltd*List Not Exhaustive, Fuzhou Kinglong Commodity & Cosmetic Co Ltd, Bericap GmbH, Albea Group, Silgan White Cap (Shanghai) Co, Shandong Haishengyu Plastics Industry Co Ltd, Crown Asia Pacific Holdings Limited, Berry Global Inc.

3. What are the main segments of the China Plastic Caps & Closures Industry?

The market segments include Raw Material, Industry Vertical.

4. Can you provide details about the market size?

The market size is estimated to be USD 6.34 billion as of 2022.

5. What are some drivers contributing to market growth?

Growing Consumption of Single Serve Beverages; Growing Demand from Cosmetic Industry.

6. What are the notable trends driving market growth?

Food and Beverage Industry to Drive the Growth of the Market.

7. Are there any restraints impacting market growth?

Lightweight and Cost-effective Stand-up Pouch Packaging Alternatives.

8. Can you provide examples of recent developments in the market?

May 2022: Carlyle plans to acquire China-based cosmetic packaging company HCP. HCP works with more than 250 leading cosmetics, skincare, and fragrance brands, including Estée Lauder, L'Oréal, and Shiseido. Carlyle will work with HCP through strategic acquisitions to strengthen the company's research and development (R&D) capabilities.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "China Plastic Caps & Closures Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the China Plastic Caps & Closures Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the China Plastic Caps & Closures Industry?

To stay informed about further developments, trends, and reports in the China Plastic Caps & Closures Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence