Key Insights

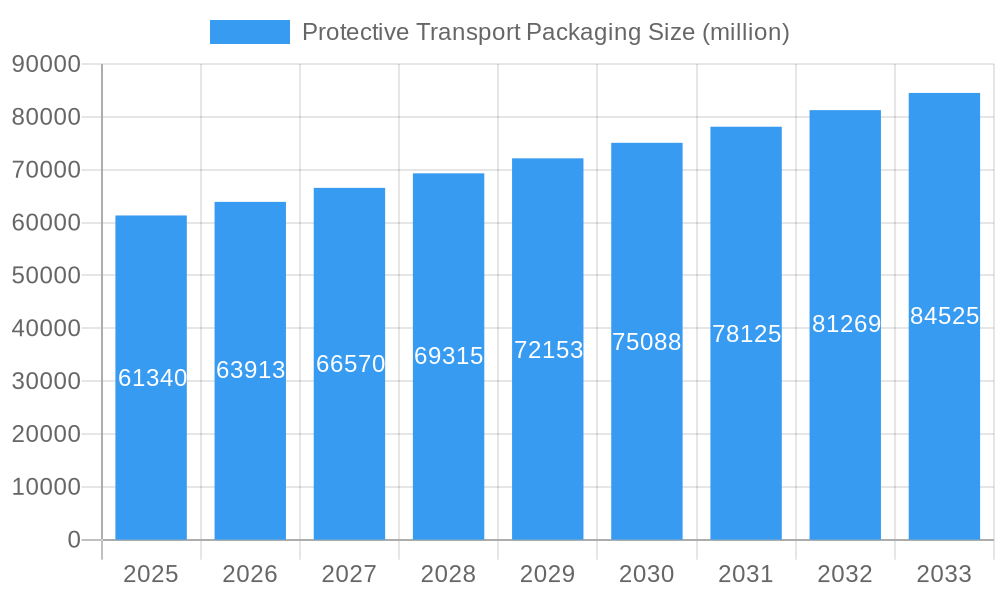

The global Protective Transport Packaging market is poised for robust expansion, projected to reach a substantial market size by 2025, with a healthy Compound Annual Growth Rate (CAGR) of 4.2% expected to persist through 2033. This sustained growth is fueled by a confluence of factors, primarily driven by the escalating demand for secure and efficient logistics across a myriad of industries. The burgeoning e-commerce sector stands as a significant propellant, necessitating advanced packaging solutions to safeguard products during transit and minimize damage. Furthermore, the increasing globalization of supply chains and the resultant increase in cross-border shipments contribute to the upward trajectory of the market. A growing emphasis on product integrity and brand reputation, especially within sensitive sectors like pharmaceuticals and electronics, also drives the adoption of premium protective packaging. Innovations in material science, leading to lighter, more sustainable, and cost-effective packaging options, are further bolstering market penetration and adoption rates.

Protective Transport Packaging Market Size (In Billion)

The market's segmentation reveals distinct growth opportunities across various applications and material types. The "White Goods and Electronics" and "Pharmaceutical and Medical Devices" segments are expected to exhibit particularly strong growth due to the high value and fragility of the products they protect. Similarly, the "Daily Consumer Goods" and "Food and Beverage" sectors are witnessing an increasing reliance on protective packaging to ensure product quality and consumer satisfaction. From a material perspective, Foam and Film packaging is anticipated to maintain its dominance due to its versatile protective qualities and adaptability to diverse product shapes. However, Paper and Paperboard packaging is experiencing a significant surge, driven by a global push towards sustainable and recyclable solutions. Leading market players like Amcor, Sealed Air Corporation, and Smurfit Kappa are actively investing in research and development to introduce innovative, eco-friendly, and high-performance packaging alternatives, catering to evolving consumer preferences and stringent regulatory frameworks.

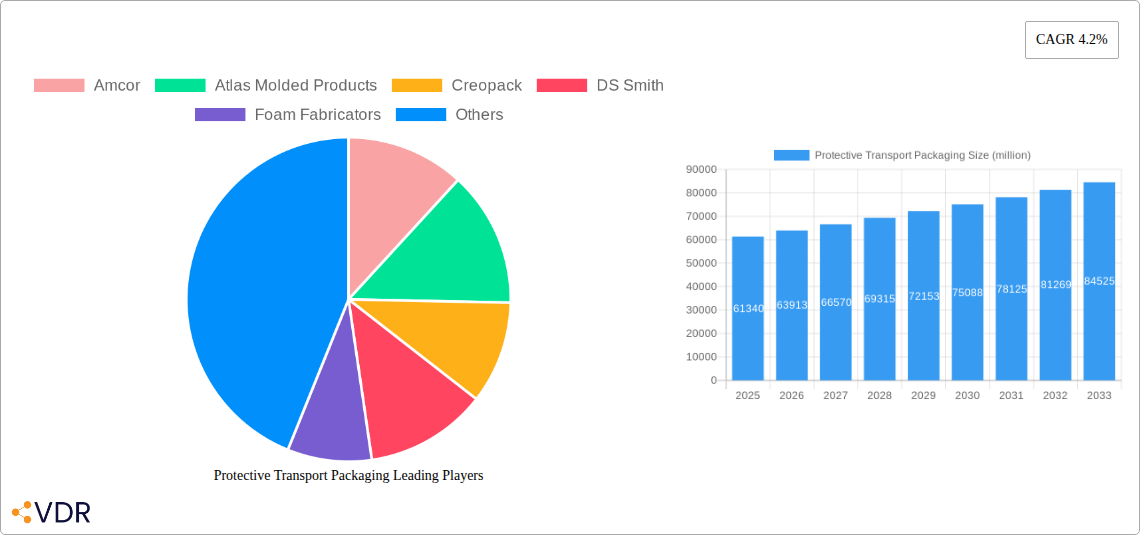

Protective Transport Packaging Company Market Share

Here's the SEO-optimized report description for Protective Transport Packaging, structured as requested and incorporating high-traffic keywords for maximum visibility.

This comprehensive report, "Protective Transport Packaging Market Dynamics & Structure 2024," offers an in-depth analysis of the global protective transport packaging industry. Covering the historical period of 2019–2024 and forecasting to 2033, with a base year of 2025, this research provides critical insights for manufacturers, suppliers, distributors, and investors in the e-commerce packaging, sustainable packaging solutions, and specialty packaging markets.

The report examines market concentration, technological innovation drivers, evolving regulatory frameworks, competitive product substitutes, shifting end-user demographics, and key merger and acquisition (M&A) trends. Quantitative data, including market share percentages and M&A deal volumes in million units, is presented alongside qualitative factors such as innovation barriers and the impact of environmental regulations on custom packaging and transit packaging.

Key Market Segments Covered:

- Application: White Goods and Electronics, Pharmaceutical and Medical Devices, Daily Consumer Goods, Food and Beverage, Others

- Type: Foam and Film, Paper and Paperboard, Others

- Parent Markets: E-commerce Logistics, Industrial Manufacturing, Consumer Goods Distribution

- Child Markets: Fragile Goods Packaging, Temperature-Controlled Packaging, Heavy-Duty Transit Boxes

Protective Transport Packaging Market Dynamics & Structure

The global protective transport packaging market exhibits a moderately consolidated structure, with a mix of large multinational corporations and specialized regional players. Key innovation drivers include the escalating demand for sustainable packaging materials, driven by consumer preferences and stringent environmental regulations. Technological advancements in material science, such as the development of advanced cushioning foams and biodegradable paper-based solutions, are reshaping the competitive landscape. Regulatory frameworks, particularly concerning waste reduction and recyclability, are increasingly influencing product development and market access for eco-friendly packaging. Competitive product substitutes, ranging from traditional corrugated boxes to advanced molded pulp and expanded polystyrene (EPS) alternatives, offer diverse protective capabilities. End-user demographics are evolving, with a significant surge in demand from the B2C e-commerce sector, requiring smaller, more adaptable packaging solutions. M&A trends indicate a strategic focus on acquiring companies with expertise in sustainable materials and advanced automation for packaging solutions. The market share of leading players is significant, with approximately 60% of the market dominated by the top 10-15 companies. Innovation barriers include high R&D costs for novel materials and the need for significant capital investment in new manufacturing processes for specialty protective packaging.

Protective Transport Packaging Growth Trends & Insights

The protective transport packaging market is poised for significant expansion, driven by robust growth in global e-commerce and a heightened awareness of product protection throughout the supply chain. The market size is projected to grow at a Compound Annual Growth Rate (CAGR) of approximately 5.8% during the forecast period, reaching an estimated USD 120,000 million units by 2033. Adoption rates for innovative and sustainable packaging materials are accelerating, with consumers and businesses increasingly prioritizing eco-friendly packaging solutions. Technological disruptions, such as the integration of smart packaging for real-time condition monitoring and advanced void fill technologies, are enhancing product performance and reducing shipping damage, a critical factor for fragile item packaging. Consumer behavior shifts, particularly the rise of online shopping for a wider array of products including pharmaceutical packaging and food and beverage packaging, are directly fueling demand for specialized protective solutions. The penetration of advanced cushioning foams and recyclable paper-based alternatives is steadily increasing, displacing traditional materials in many applications. The shift towards omnichannel retail strategies further necessitates adaptable and efficient packaging designs. The market penetration of customized packaging solutions is expected to reach 75% by 2030, reflecting the growing need for tailored protection.

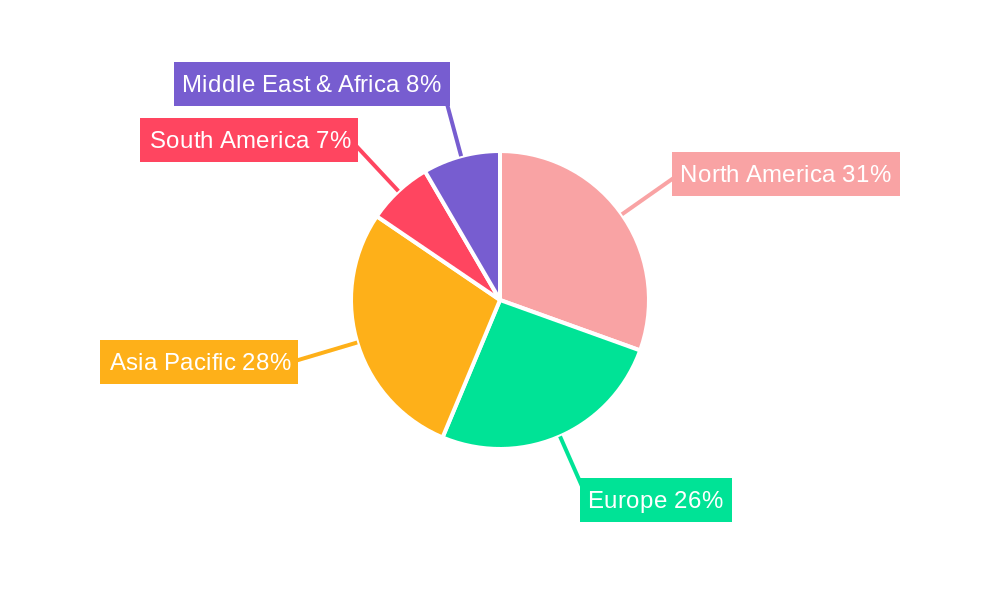

Dominant Regions, Countries, or Segments in Protective Transport Packaging

The White Goods and Electronics segment is a dominant driver of growth within the protective transport packaging market, largely due to the inherent fragility and high value of these products. This segment is expected to contribute over 35% of the total market revenue by 2033. The increasing global demand for consumer electronics, home appliances, and sophisticated electronic devices necessitates robust and specialized protective packaging solutions to prevent damage during transit and handling. Key drivers for this dominance include the extensive global supply chains involved in manufacturing and distribution of these goods, stringent quality control standards, and the high cost of product replacement due to damage. Economic policies that encourage manufacturing and trade in these sectors, coupled with advancements in logistics infrastructure, further bolster demand. Countries like China, the United States, and Germany are at the forefront of both production and consumption of white goods and electronics, thereby leading the demand for their specialized packaging.

The Foam and Film type segment, particularly encompassing materials like expanded polystyrene (EPS), polyethylene (PE) foam, and polyurethane (PU) foam, holds a substantial market share, estimated at 45% of the total market by value. These materials offer superior cushioning, shock absorption, and insulation properties, making them ideal for protecting sensitive items like electronics and medical devices. The continuous innovation in foam formulations to improve sustainability, such as the development of bio-based foams and recyclable alternatives, is sustaining their market dominance.

Protective Transport Packaging Product Landscape

The protective transport packaging product landscape is characterized by continuous innovation focused on enhancing protection, sustainability, and cost-effectiveness. Advanced cushioning foams, such as engineered EPP (Expanded Polypropylene) and EPE (Expanded Polyethylene) foams, offer superior shock absorption and impact resistance for high-value electronics and automotive components. Molded pulp packaging, derived from recycled paper, is gaining traction as a sustainable alternative, providing excellent structural integrity and customizable designs for various applications, including food packaging and consumer goods packaging. Innovative void-fill solutions, including air pillows made from recycled films and expandable bio-based materials, are minimizing product movement within transit packaging. Performance metrics are increasingly scrutinized, with a focus on drop test performance, compression strength, and thermal insulation capabilities. Unique selling propositions revolve around circular economy principles, enabling closed-loop recycling systems and minimizing environmental impact.

Key Drivers, Barriers & Challenges in Protective Transport Packaging

Key Drivers:

- E-commerce Growth: The continuous surge in online retail fuels demand for robust and efficient protective packaging to ensure product integrity during last-mile delivery.

- Sustainability Mandates: Increasing environmental consciousness and regulatory pressures are driving the adoption of recycled, recyclable, and biodegradable packaging materials.

- Product Fragility: The rise in sophisticated and delicate products across industries like electronics and pharmaceuticals necessitates advanced cushioning and protective solutions.

- Supply Chain Optimization: Companies are investing in packaging that reduces shipping damage, minimizes returns, and improves overall logistics efficiency.

Barriers & Challenges:

- Material Cost Volatility: Fluctuations in the cost of raw materials, such as petroleum-based plastics and paper pulp, can impact profitability.

- Recycling Infrastructure Limitations: Inadequate recycling infrastructure in certain regions can hinder the widespread adoption and effective end-of-life management of some packaging materials.

- Performance vs. Cost Trade-offs: Balancing the need for superior protection with cost-effectiveness remains a significant challenge for packaging manufacturers.

- Regulatory Complexity: Navigating diverse and evolving international regulations on packaging materials and waste management can be complex and costly.

- Supply Chain Disruptions: Global supply chain vulnerabilities can impact the availability and cost of raw materials, affecting production schedules.

Emerging Opportunities in Protective Transport Packaging

Emerging opportunities in the protective transport packaging sector lie in the development of smart packaging solutions that offer real-time condition monitoring for sensitive shipments, such as pharmaceuticals and perishables. The increasing demand for temperature-controlled packaging for the burgeoning pharmaceutical and food delivery sectors presents significant growth potential. Untapped markets in emerging economies, coupled with a growing middle class, offer substantial opportunities for expanded market reach. Furthermore, the integration of bio-based and compostable packaging materials derived from renewable resources aligns with evolving consumer preferences and corporate sustainability goals. Innovative applications in industrial protective packaging for large machinery and specialized equipment are also on the rise.

Growth Accelerators in the Protective Transport Packaging Industry

Growth accelerators in the protective transport packaging industry are significantly influenced by ongoing technological breakthroughs in material science, leading to lighter, stronger, and more sustainable packaging options. Strategic partnerships between packaging manufacturers and logistics providers are crucial for developing integrated solutions that optimize the entire supply chain. Market expansion strategies, particularly targeting the growing e-commerce hubs in Asia-Pacific and Latin America, are critical for long-term growth. Investment in automation and advanced manufacturing techniques by major players is enhancing production efficiency and scalability, enabling them to meet the escalating global demand for protective transport packaging. The development of closed-loop recycling programs and the adoption of circular economy principles further accelerate the industry's sustainable growth trajectory.

Key Players Shaping the Protective Transport Packaging Market

- Amcor

- Atlas Molded Products

- Creopack

- DS Smith

- Foam Fabricators

- Haijing

- Jiuding Group

- Plastifoam Company

- Plymouth Foam

- Polyfoam Corporation

- Pregis

- Ranpak

- Recticel

- Rogers Foam Corporation

- Sealed Air Corporation

- Smurfit Kappa

- Sonoco

- Speed Foam

- Teamway

- Tucson Container Corporation

- Wisconsin Foam Products

- Woodbridge

- Crawford Packaging

Notable Milestones in Protective Transport Packaging Sector

- 2019: Launch of innovative biodegradable cushioning materials by several key players, responding to growing environmental concerns.

- 2020: Significant increase in demand for e-commerce-specific protective packaging due to the global pandemic, accelerating investment in automated solutions.

- 2021: Expansion of mergers and acquisitions activity, with major companies acquiring smaller specialists in sustainable and advanced materials.

- 2022: Introduction of advanced void-fill solutions with higher recycled content, enhancing sustainability credentials.

- 2023: Increased focus on circular economy initiatives and development of closed-loop recycling programs for protective packaging.

- 2024: Heightened regulatory scrutiny on single-use plastics, driving further innovation in alternative materials for protective packaging.

In-Depth Protective Transport Packaging Market Outlook

The future outlook for the protective transport packaging market is exceptionally robust, driven by the sustained expansion of e-commerce and an unwavering commitment to product integrity. Growth accelerators, including the relentless pursuit of sustainable material innovations, the strategic implementation of smart packaging technologies, and the expansion into emerging geographical markets, will continue to propel the industry forward. The increasing emphasis on the circular economy and advancements in recycling infrastructure will further solidify the market's commitment to environmental responsibility. Strategic partnerships and investment in advanced manufacturing are poised to enhance efficiency and scalability, ensuring that the industry can effectively meet the evolving demands for comprehensive and responsible protective packaging solutions globally.

Study Period: 2019–2033 Base Year: 2025 Estimated Year: 2025 Forecast Period: 2025–2033 Historical Period: 2019–2024

Protective Transport Packaging Segmentation

-

1. Application

- 1.1. White Goods and Electronics

- 1.2. Pharmaceutical and Medical Devices

- 1.3. Daily Consumer Goods

- 1.4. Food and Beverage

- 1.5. Others

-

2. Type

- 2.1. Foam and Film

- 2.2. Paper and Paperboard

- 2.3. Others

Protective Transport Packaging Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Protective Transport Packaging Regional Market Share

Geographic Coverage of Protective Transport Packaging

Protective Transport Packaging REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. White Goods and Electronics

- 5.1.2. Pharmaceutical and Medical Devices

- 5.1.3. Daily Consumer Goods

- 5.1.4. Food and Beverage

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Foam and Film

- 5.2.2. Paper and Paperboard

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Protective Transport Packaging Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. White Goods and Electronics

- 6.1.2. Pharmaceutical and Medical Devices

- 6.1.3. Daily Consumer Goods

- 6.1.4. Food and Beverage

- 6.1.5. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Foam and Film

- 6.2.2. Paper and Paperboard

- 6.2.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Protective Transport Packaging Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. White Goods and Electronics

- 7.1.2. Pharmaceutical and Medical Devices

- 7.1.3. Daily Consumer Goods

- 7.1.4. Food and Beverage

- 7.1.5. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Foam and Film

- 7.2.2. Paper and Paperboard

- 7.2.3. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Protective Transport Packaging Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. White Goods and Electronics

- 8.1.2. Pharmaceutical and Medical Devices

- 8.1.3. Daily Consumer Goods

- 8.1.4. Food and Beverage

- 8.1.5. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Foam and Film

- 8.2.2. Paper and Paperboard

- 8.2.3. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Protective Transport Packaging Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. White Goods and Electronics

- 9.1.2. Pharmaceutical and Medical Devices

- 9.1.3. Daily Consumer Goods

- 9.1.4. Food and Beverage

- 9.1.5. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Foam and Film

- 9.2.2. Paper and Paperboard

- 9.2.3. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Protective Transport Packaging Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. White Goods and Electronics

- 10.1.2. Pharmaceutical and Medical Devices

- 10.1.3. Daily Consumer Goods

- 10.1.4. Food and Beverage

- 10.1.5. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Foam and Film

- 10.2.2. Paper and Paperboard

- 10.2.3. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Protective Transport Packaging Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. White Goods and Electronics

- 11.1.2. Pharmaceutical and Medical Devices

- 11.1.3. Daily Consumer Goods

- 11.1.4. Food and Beverage

- 11.1.5. Others

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. Foam and Film

- 11.2.2. Paper and Paperboard

- 11.2.3. Others

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Amcor

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Atlas Molded Products

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Creopack

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 DS Smith

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Foam Fabricators

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Haijing

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Jiuding Group

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Plastifoam Company

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Plymouth Foam

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Polyfoam Corporation

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Pregis

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Ranpak

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Recticel

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Rogers Foam Corporation

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Sealed Air Corporation

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 Smurfit Kappa

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.17 Sonoco

- 12.1.17.1. Company Overview

- 12.1.17.2. Products

- 12.1.17.3. Company Financials

- 12.1.17.4. SWOT Analysis

- 12.1.18 Speed Foam

- 12.1.18.1. Company Overview

- 12.1.18.2. Products

- 12.1.18.3. Company Financials

- 12.1.18.4. SWOT Analysis

- 12.1.19 Teamway

- 12.1.19.1. Company Overview

- 12.1.19.2. Products

- 12.1.19.3. Company Financials

- 12.1.19.4. SWOT Analysis

- 12.1.20 Tucson Container Corporation

- 12.1.20.1. Company Overview

- 12.1.20.2. Products

- 12.1.20.3. Company Financials

- 12.1.20.4. SWOT Analysis

- 12.1.21 Wisconsin Foam Products

- 12.1.21.1. Company Overview

- 12.1.21.2. Products

- 12.1.21.3. Company Financials

- 12.1.21.4. SWOT Analysis

- 12.1.22 Woodbridge

- 12.1.22.1. Company Overview

- 12.1.22.2. Products

- 12.1.22.3. Company Financials

- 12.1.22.4. SWOT Analysis

- 12.1.23 Crawford Packaging

- 12.1.23.1. Company Overview

- 12.1.23.2. Products

- 12.1.23.3. Company Financials

- 12.1.23.4. SWOT Analysis

- 12.1.1 Amcor

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Protective Transport Packaging Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Protective Transport Packaging Revenue (million), by Application 2025 & 2033

- Figure 3: North America Protective Transport Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Protective Transport Packaging Revenue (million), by Type 2025 & 2033

- Figure 5: North America Protective Transport Packaging Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Protective Transport Packaging Revenue (million), by Country 2025 & 2033

- Figure 7: North America Protective Transport Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Protective Transport Packaging Revenue (million), by Application 2025 & 2033

- Figure 9: South America Protective Transport Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Protective Transport Packaging Revenue (million), by Type 2025 & 2033

- Figure 11: South America Protective Transport Packaging Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Protective Transport Packaging Revenue (million), by Country 2025 & 2033

- Figure 13: South America Protective Transport Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Protective Transport Packaging Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Protective Transport Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Protective Transport Packaging Revenue (million), by Type 2025 & 2033

- Figure 17: Europe Protective Transport Packaging Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Protective Transport Packaging Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Protective Transport Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Protective Transport Packaging Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Protective Transport Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Protective Transport Packaging Revenue (million), by Type 2025 & 2033

- Figure 23: Middle East & Africa Protective Transport Packaging Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Protective Transport Packaging Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Protective Transport Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Protective Transport Packaging Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Protective Transport Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Protective Transport Packaging Revenue (million), by Type 2025 & 2033

- Figure 29: Asia Pacific Protective Transport Packaging Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Protective Transport Packaging Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Protective Transport Packaging Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Protective Transport Packaging Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Protective Transport Packaging Revenue million Forecast, by Type 2020 & 2033

- Table 3: Global Protective Transport Packaging Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Protective Transport Packaging Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Protective Transport Packaging Revenue million Forecast, by Type 2020 & 2033

- Table 6: Global Protective Transport Packaging Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Protective Transport Packaging Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Protective Transport Packaging Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Protective Transport Packaging Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Protective Transport Packaging Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Protective Transport Packaging Revenue million Forecast, by Type 2020 & 2033

- Table 12: Global Protective Transport Packaging Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Protective Transport Packaging Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Protective Transport Packaging Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Protective Transport Packaging Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Protective Transport Packaging Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Protective Transport Packaging Revenue million Forecast, by Type 2020 & 2033

- Table 18: Global Protective Transport Packaging Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Protective Transport Packaging Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Protective Transport Packaging Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Protective Transport Packaging Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Protective Transport Packaging Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Protective Transport Packaging Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Protective Transport Packaging Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Protective Transport Packaging Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Protective Transport Packaging Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Protective Transport Packaging Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Protective Transport Packaging Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Protective Transport Packaging Revenue million Forecast, by Type 2020 & 2033

- Table 30: Global Protective Transport Packaging Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Protective Transport Packaging Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Protective Transport Packaging Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Protective Transport Packaging Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Protective Transport Packaging Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Protective Transport Packaging Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Protective Transport Packaging Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Protective Transport Packaging Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Protective Transport Packaging Revenue million Forecast, by Type 2020 & 2033

- Table 39: Global Protective Transport Packaging Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Protective Transport Packaging Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Protective Transport Packaging Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Protective Transport Packaging Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Protective Transport Packaging Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Protective Transport Packaging Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Protective Transport Packaging Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Protective Transport Packaging Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Protective Transport Packaging?

The projected CAGR is approximately 4.2%.

2. Which companies are prominent players in the Protective Transport Packaging?

Key companies in the market include Amcor, Atlas Molded Products, Creopack, DS Smith, Foam Fabricators, Haijing, Jiuding Group, Plastifoam Company, Plymouth Foam, Polyfoam Corporation, Pregis, Ranpak, Recticel, Rogers Foam Corporation, Sealed Air Corporation, Smurfit Kappa, Sonoco, Speed Foam, Teamway, Tucson Container Corporation, Wisconsin Foam Products, Woodbridge, Crawford Packaging.

3. What are the main segments of the Protective Transport Packaging?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 61340 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4250.00, USD 6375.00, and USD 8500.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Protective Transport Packaging," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Protective Transport Packaging report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Protective Transport Packaging?

To stay informed about further developments, trends, and reports in the Protective Transport Packaging, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence