Key Insights

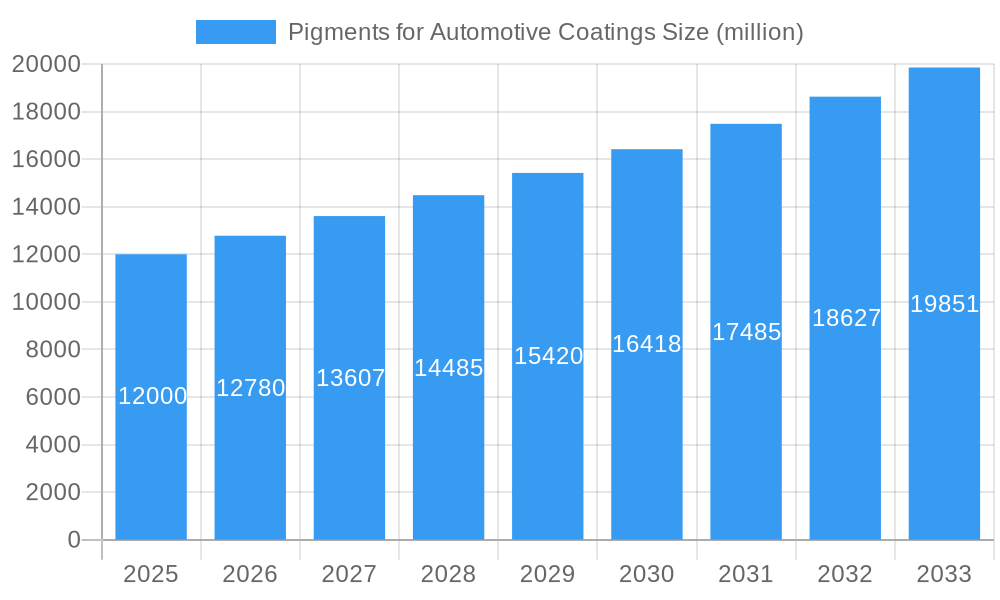

The global pigments for automotive coatings market is poised for robust growth, projected to reach approximately USD 12,000 million by 2025, with a Compound Annual Growth Rate (CAGR) of around 6.5% anticipated from 2025 to 2033. This expansion is primarily fueled by the burgeoning automotive industry, driven by increasing vehicle production and a growing demand for aesthetically pleasing and durable finishes. The rising disposable incomes in emerging economies, coupled with evolving consumer preferences for personalized and premium automotive aesthetics, are significant contributors to this upward trajectory. Furthermore, advancements in pigment technology, leading to enhanced color brilliance, weather resistance, and environmental friendliness, are creating new opportunities for market players. The segment of water-based coatings, in particular, is expected to witness substantial growth, aligning with stricter environmental regulations and a global shift towards sustainable coating solutions.

Pigments for Automotive Coatings Market Size (In Billion)

The market dynamics are characterized by a strong focus on innovation and product development, with companies investing heavily in research and development to introduce high-performance pigments. Key drivers include the demand for pigments that offer superior UV protection, scratch resistance, and unique visual effects like metallic and pearlescent finishes, enhancing vehicle appeal and longevity. However, the market also faces certain restraints, such as fluctuating raw material prices, particularly for titanium dioxide and specialty organic pigments, and the increasing complexity of regulatory landscapes concerning volatile organic compounds (VOCs) and heavy metal content. Despite these challenges, the increasing adoption of advanced pigment formulations, alongside the growing trend of custom color matching and special effects in automotive design, is expected to sustain the market's growth momentum throughout the forecast period.

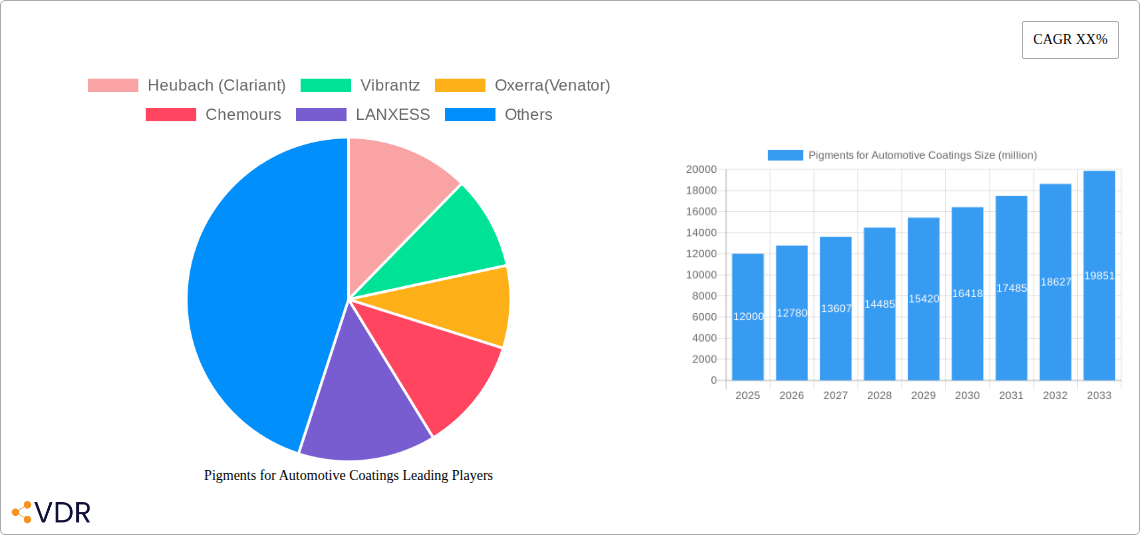

Pigments for Automotive Coatings Company Market Share

Here is a compelling, SEO-optimized report description for "Pigments for Automotive Coatings," integrating high-traffic keywords and market structure as requested.

Unlock critical insights into the global pigments for automotive coatings market with this in-depth report. Spanning the historical period from 2019 to 2024 and projecting growth through 2033, this analysis is your definitive guide to understanding market dynamics, growth drivers, technological advancements, and competitive landscapes. Essential for pigment manufacturers, automotive OEMs, coatings suppliers, and R&D professionals, this report provides actionable intelligence to navigate the evolving automotive refinish and OEM paint industries.

Pigments for Automotive Coatings Market Dynamics & Structure

The global pigments for automotive coatings market exhibits a moderately consolidated structure, with a few key players holding significant market share, including Heubach (Clariant), Vibrantz, Oxerra (Venator), Chemours, LANXESS, DIC Corporation, Tronox, and Kronos Worldwide. These dominant entities leverage extensive R&D capabilities and global supply chains to maintain their positions. Technological innovation remains a primary driver, with ongoing advancements in areas like high-performance effect pigments, eco-friendly formulations (low VOC, water-based), and durable color solutions. Regulatory frameworks, particularly concerning environmental impact and health safety of pigments, significantly influence product development and market access. Competitive product substitutes, such as digital printing inks and advanced ceramic coatings, are emerging, although traditional pigments continue to dominate. End-user demographics are shifting towards demand for more sustainable, durable, and aesthetically appealing coatings, driven by consumer preferences for personalization and vehicle longevity. Mergers and Acquisitions (M&A) activity is a notable trend, with strategic consolidations aimed at expanding product portfolios, geographical reach, and technological expertise. For instance, the acquisition of Venator's pigments business by Huntsman (now Vibrantz) highlights this consolidation trend.

- Market Concentration: Moderate to High.

- Key Innovation Drivers: Sustainability (water-based, low VOC), performance enhancement (durability, weather resistance), aesthetic appeal (effect pigments, color trends).

- Regulatory Influence: REACH, EPA regulations, emission standards impacting pigment composition and application.

- Competitive Substitutes: Digital printing, advanced ceramic coatings, nanocoatings.

- End-User Demand: Customization, eco-consciousness, extended vehicle lifespan.

- M&A Activity: Driven by portfolio expansion, market consolidation, and technology acquisition.

Pigments for Automotive Coatings Growth Trends & Insights

The global pigments for automotive coatings market is poised for robust growth, driven by an increasing global vehicle production and a persistent demand for sophisticated and sustainable automotive finishes. The market size is projected to grow from an estimated XX million units in 2025 to XX million units by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of approximately XX% during the forecast period (2025–2033). Adoption rates of water-based coatings are steadily increasing, propelled by stringent environmental regulations and OEM commitments to reduce volatile organic compounds (VOCs). This shift directly impacts the demand for corresponding water-dispersible pigments. Technological disruptions, such as the development of self-healing pigments and smart coatings with integrated functionalities, are beginning to influence the premium segments of the market. Consumer behavior is increasingly prioritizing vehicle aesthetics and personalization, leading to a higher demand for effect pigments like metallic, pearlescent, and chameleon pigments. Furthermore, the automotive refinish sector continues to be a significant contributor to market growth, fueled by accident repairs and vehicle customization trends. The parent market, encompassing all pigments, is vast, while the child market for automotive coatings represents a specialized and high-value segment. The projected market size for pigments for automotive coatings in the base year 2025 is estimated at XX million units, with the parent market size for all pigment applications estimated at XXX million units.

- Market Size Evolution: Expected to grow from XX million units (2025) to XX million units (2033).

- CAGR: Estimated at XX% (2025–2033).

- Adoption Rates: High growth in water-based coatings due to environmental mandates.

- Technological Disruptions: Emerging smart coatings, self-healing pigments, advanced effect pigments.

- Consumer Behavior Shifts: Emphasis on personalization, aesthetics, and vehicle longevity.

- Market Penetration: Significant penetration in both OEM and refinish segments.

- Parent Market Size (2025): XXX million units.

- Child Market Size (2025): XX million units.

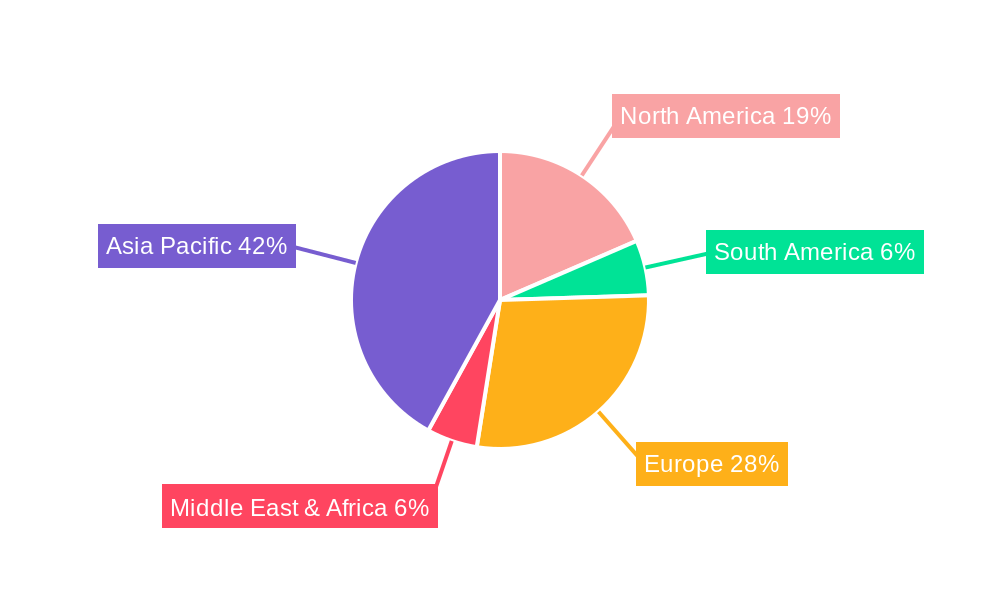

Dominant Regions, Countries, or Segments in Pigments for Automotive Coatings

Asia Pacific is emerging as the dominant region in the global pigments for automotive coatings market, driven by rapid industrialization, burgeoning automotive manufacturing hubs, and increasing disposable incomes leading to higher vehicle sales. Countries like China, India, and South Korea are spearheading this growth due to substantial investments in automotive production capacity and a growing domestic demand for passenger vehicles and commercial transport. Economic policies favorable to manufacturing and significant infrastructure development further bolster the region's dominance.

Within the application segments, Water-Based Coating is experiencing the most significant growth trajectory, projected to capture a substantial market share. This dominance is directly attributable to global environmental regulations pushing for reduced VOC emissions. Leading automotive manufacturers are increasingly adopting water-borne basecoats and clearcoats to meet sustainability targets and enhance worker safety. The shift towards water-based systems necessitates specialized pigments that offer excellent dispersion, color consistency, and durability in aqueous formulations.

In terms of pigment types, White Pigment, primarily Titanium Dioxide (TiO2), remains the largest segment due to its indispensable role in providing opacity, brightness, and whiteness to virtually all automotive paint systems. However, Metallic Luster Pigment and advanced effect pigments are witnessing accelerated growth, catering to the rising consumer demand for premium, customized, and visually striking automotive finishes.

- Dominant Region: Asia Pacific.

- Key Drivers: Robust automotive manufacturing growth, increasing vehicle sales, supportive economic policies, expanding middle class.

- Market Share: Estimated at XX% of the global market in 2025.

- Growth Potential: High, driven by ongoing industrial expansion.

- Dominant Application Segment: Water-Based Coating.

- Key Drivers: Stringent environmental regulations (low VOC), OEM sustainability initiatives, improved pigment technology for waterborne systems.

- Market Share (2025): Estimated at XX% of the automotive coatings pigment market.

- Growth Potential: Significant, driven by regulatory compliance and technological advancements.

- Dominant Pigment Type: White Pigment (Titanium Dioxide).

- Key Drivers: Universal use for opacity and brightness, cost-effectiveness, established technology.

- Market Share (2025): Estimated at XX% of the automotive pigments market.

- Growth Potential: Steady, with advancements in performance and sustainability.

- High-Growth Pigment Type: Metallic Luster Pigment.

- Key Drivers: Consumer demand for aesthetics, customization, and premium finishes.

- Growth Potential: High, driven by trends in vehicle personalization.

Pigments for Automotive Coatings Product Landscape

The product landscape for pigments in automotive coatings is characterized by innovation focused on enhancing performance, sustainability, and aesthetic appeal. Manufacturers are actively developing high-performance pigments that offer superior durability, weatherability, and chemical resistance, crucial for the demanding automotive environment. Innovations include advanced effect pigments like color-shifting and interference pigments, enabling unique visual effects. The development of eco-friendly pigment solutions, such as low-VOC and heavy metal-free organic pigments and improved inorganic pigment dispersions for water-based systems, is a key trend. Specialty pigments are also gaining traction for applications like anti-corrosion and heat-reflective coatings, contributing to vehicle efficiency and longevity.

Key Drivers, Barriers & Challenges in Pigments for Automotive Coatings

Key Drivers:

- Increasing Global Vehicle Production: Growing demand for new vehicles directly translates to higher demand for automotive coatings and pigments.

- Stringent Environmental Regulations: The push for low-VOC and sustainable coatings drives innovation and adoption of compliant pigment technologies.

- Consumer Demand for Aesthetics and Customization: The desire for unique vehicle appearances fuels the demand for effect pigments and a wider color palette.

- Technological Advancements: Development of higher-performance, more durable, and specialized pigments.

Key Barriers & Challenges:

- Raw Material Price Volatility: Fluctuations in the cost of key raw materials, such as titanium dioxide and various organic chemical precursors, can impact profitability.

- Regulatory Compliance Costs: Meeting evolving environmental and safety regulations can be costly and time-consuming for manufacturers.

- Supply Chain Disruptions: Geopolitical events, natural disasters, and logistical challenges can disrupt the supply of raw materials and finished products.

- Competition from Substitutes: While not yet dominant, emerging technologies and alternative coating solutions pose a long-term threat.

- High Capital Investment: Establishing and maintaining pigment manufacturing facilities requires significant capital expenditure.

Emerging Opportunities in Pigments for Automotive Coatings

Emerging opportunities lie in the development and adoption of novel pigment technologies that offer enhanced functionalities. This includes smart pigments capable of self-repairing minor scratches, thermochromic pigments that change color with temperature, and pigments with integrated UV-blocking or IR-reflective properties for improved energy efficiency. The growing demand for electric vehicles (EVs) also presents opportunities for specialized pigments that can manage heat dissipation or enhance battery performance through their application in battery casings or thermal management systems. Furthermore, the increasing focus on vehicle personalization and limited edition models will continue to drive demand for unique and complex effect pigments. The expansion of automotive manufacturing in emerging economies also offers untapped market potential.

Growth Accelerators in the Pigments for Automotive Coatings Industry

Long-term growth in the pigments for automotive coatings industry will be significantly accelerated by ongoing breakthroughs in nanotechnology, enabling the development of pigments with superior color strength, durability, and unique optical properties. Strategic partnerships between pigment manufacturers and automotive OEMs will be crucial for co-developing next-generation coatings that meet evolving performance and aesthetic requirements. The increasing global adoption of electric vehicles and the trend towards autonomous driving will also act as growth accelerators, necessitating new pigment solutions for functional coatings and sensor-integrated surfaces. Furthermore, the continuous drive towards a circular economy will foster innovation in sustainable pigment production and recycling processes.

Key Players Shaping the Pigments for Automotive Coatings Market

- Heubach (Clariant)

- Vibrantz

- Oxerra (Venator)

- Chemours

- LANXESS

- DIC Corporation

- Tronox

- Kronos Worldwide

- Alabama Pigments

- DCL Corporation

- TOMATEC

- The Shepherd Color Company

- Toyo Ink

- Sudarshan

- Ultramarine and Pigments Limited

- Asahi Kasei Kogyo

- Noelson Chemicals

- R.S. Pigments

- ECKART

- Gpro Titanium Industry

- CNNC HUA YUAN Titanium Dioxide

- YUXING PIGMENT

- Sunlour Pigment

- Fulln Chemical

- Hunan Jufa Pigment

- Cadello

- ZhongLong Materials Limited

- Shanghai Fulcolor Advanced Materials

Notable Milestones in Pigments for Automotive Coatings Sector

- 2019: Increased regulatory scrutiny on heavy metals in pigments leads to greater R&D investment in organic and alternative inorganic pigments.

- 2020: The COVID-19 pandemic temporarily disrupts automotive production but highlights the importance of supply chain resilience for pigment manufacturers.

- 2021: Several key players announce investments in expanding their water-based pigment production capacity.

- 2022: Advancements in pearlescent and metallic effect pigments gain traction, offering novel color and sheen options.

- 2023: Growing emphasis on sustainable pigment sourcing and production processes becomes a significant market differentiator.

- 2024: Increased consolidation within the pigment industry through M&A activities, aiming for vertical integration and portfolio diversification.

In-Depth Pigments for Automotive Coatings Market Outlook

The future of the pigments for automotive coatings market is exceptionally promising, driven by a confluence of factors including technological innovation, expanding automotive production, and evolving consumer preferences. Growth accelerators such as advanced nanotechnology, strategic collaborations, and the burgeoning electric vehicle market will propel the industry forward. The increasing adoption of sustainable practices and the demand for high-performance, aesthetically superior coatings will create significant opportunities for market players. The outlook suggests a dynamic and evolving market, where innovation in pigment functionality and sustainability will be paramount for sustained success and market leadership.

Pigments for Automotive Coatings Segmentation

-

1. Application

- 1.1. Water-Based Coating

- 1.2. Solvent Based Coating

- 1.3. Powder Coating

- 1.4. Others

-

2. Types

- 2.1. White Pigment

- 2.2. Red Pigment

- 2.3. Blue Pigment

- 2.4. Green Pigment

- 2.5. Metallic Luster Pigment

Pigments for Automotive Coatings Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Pigments for Automotive Coatings Regional Market Share

Geographic Coverage of Pigments for Automotive Coatings

Pigments for Automotive Coatings REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of XX% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Pigments for Automotive Coatings Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Water-Based Coating

- 5.1.2. Solvent Based Coating

- 5.1.3. Powder Coating

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. White Pigment

- 5.2.2. Red Pigment

- 5.2.3. Blue Pigment

- 5.2.4. Green Pigment

- 5.2.5. Metallic Luster Pigment

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Pigments for Automotive Coatings Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Water-Based Coating

- 6.1.2. Solvent Based Coating

- 6.1.3. Powder Coating

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. White Pigment

- 6.2.2. Red Pigment

- 6.2.3. Blue Pigment

- 6.2.4. Green Pigment

- 6.2.5. Metallic Luster Pigment

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Pigments for Automotive Coatings Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Water-Based Coating

- 7.1.2. Solvent Based Coating

- 7.1.3. Powder Coating

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. White Pigment

- 7.2.2. Red Pigment

- 7.2.3. Blue Pigment

- 7.2.4. Green Pigment

- 7.2.5. Metallic Luster Pigment

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Pigments for Automotive Coatings Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Water-Based Coating

- 8.1.2. Solvent Based Coating

- 8.1.3. Powder Coating

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. White Pigment

- 8.2.2. Red Pigment

- 8.2.3. Blue Pigment

- 8.2.4. Green Pigment

- 8.2.5. Metallic Luster Pigment

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Pigments for Automotive Coatings Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Water-Based Coating

- 9.1.2. Solvent Based Coating

- 9.1.3. Powder Coating

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. White Pigment

- 9.2.2. Red Pigment

- 9.2.3. Blue Pigment

- 9.2.4. Green Pigment

- 9.2.5. Metallic Luster Pigment

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Pigments for Automotive Coatings Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Water-Based Coating

- 10.1.2. Solvent Based Coating

- 10.1.3. Powder Coating

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. White Pigment

- 10.2.2. Red Pigment

- 10.2.3. Blue Pigment

- 10.2.4. Green Pigment

- 10.2.5. Metallic Luster Pigment

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Heubach (Clariant)

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Vibrantz

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Oxerra(Venator)

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Chemours

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 LANXESS

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 DIC Corporation

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Tronox

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Kronos Worldwide

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Alabama Pigments

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 DCL Corporation

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 TOMATEC

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 The Shepherd Color Company

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Toyo Ink

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Sudarshan

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Ultramarine and Pigments Limited

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Asahi Kasei Kogyo

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Noelson Chemicals

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 R.S. Pigments

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 ECKART

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 Gpro Titanium Industry

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.21 CNNC HUA YUAN Titanium Dioxide

- 11.2.21.1. Overview

- 11.2.21.2. Products

- 11.2.21.3. SWOT Analysis

- 11.2.21.4. Recent Developments

- 11.2.21.5. Financials (Based on Availability)

- 11.2.22 YUXING PIGMENT

- 11.2.22.1. Overview

- 11.2.22.2. Products

- 11.2.22.3. SWOT Analysis

- 11.2.22.4. Recent Developments

- 11.2.22.5. Financials (Based on Availability)

- 11.2.23 Sunlour Pigment

- 11.2.23.1. Overview

- 11.2.23.2. Products

- 11.2.23.3. SWOT Analysis

- 11.2.23.4. Recent Developments

- 11.2.23.5. Financials (Based on Availability)

- 11.2.24 Fulln Chemical

- 11.2.24.1. Overview

- 11.2.24.2. Products

- 11.2.24.3. SWOT Analysis

- 11.2.24.4. Recent Developments

- 11.2.24.5. Financials (Based on Availability)

- 11.2.25 Hunan Jufa Pigment

- 11.2.25.1. Overview

- 11.2.25.2. Products

- 11.2.25.3. SWOT Analysis

- 11.2.25.4. Recent Developments

- 11.2.25.5. Financials (Based on Availability)

- 11.2.26 Cadello

- 11.2.26.1. Overview

- 11.2.26.2. Products

- 11.2.26.3. SWOT Analysis

- 11.2.26.4. Recent Developments

- 11.2.26.5. Financials (Based on Availability)

- 11.2.27 ZhongLong Materials Limited

- 11.2.27.1. Overview

- 11.2.27.2. Products

- 11.2.27.3. SWOT Analysis

- 11.2.27.4. Recent Developments

- 11.2.27.5. Financials (Based on Availability)

- 11.2.28 Shanghai Fulcolor Advanced Materials

- 11.2.28.1. Overview

- 11.2.28.2. Products

- 11.2.28.3. SWOT Analysis

- 11.2.28.4. Recent Developments

- 11.2.28.5. Financials (Based on Availability)

- 11.2.1 Heubach (Clariant)

List of Figures

- Figure 1: Global Pigments for Automotive Coatings Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: Global Pigments for Automotive Coatings Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: North America Pigments for Automotive Coatings Revenue (million), by Application 2025 & 2033

- Figure 4: North America Pigments for Automotive Coatings Volume (K), by Application 2025 & 2033

- Figure 5: North America Pigments for Automotive Coatings Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Pigments for Automotive Coatings Volume Share (%), by Application 2025 & 2033

- Figure 7: North America Pigments for Automotive Coatings Revenue (million), by Types 2025 & 2033

- Figure 8: North America Pigments for Automotive Coatings Volume (K), by Types 2025 & 2033

- Figure 9: North America Pigments for Automotive Coatings Revenue Share (%), by Types 2025 & 2033

- Figure 10: North America Pigments for Automotive Coatings Volume Share (%), by Types 2025 & 2033

- Figure 11: North America Pigments for Automotive Coatings Revenue (million), by Country 2025 & 2033

- Figure 12: North America Pigments for Automotive Coatings Volume (K), by Country 2025 & 2033

- Figure 13: North America Pigments for Automotive Coatings Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Pigments for Automotive Coatings Volume Share (%), by Country 2025 & 2033

- Figure 15: South America Pigments for Automotive Coatings Revenue (million), by Application 2025 & 2033

- Figure 16: South America Pigments for Automotive Coatings Volume (K), by Application 2025 & 2033

- Figure 17: South America Pigments for Automotive Coatings Revenue Share (%), by Application 2025 & 2033

- Figure 18: South America Pigments for Automotive Coatings Volume Share (%), by Application 2025 & 2033

- Figure 19: South America Pigments for Automotive Coatings Revenue (million), by Types 2025 & 2033

- Figure 20: South America Pigments for Automotive Coatings Volume (K), by Types 2025 & 2033

- Figure 21: South America Pigments for Automotive Coatings Revenue Share (%), by Types 2025 & 2033

- Figure 22: South America Pigments for Automotive Coatings Volume Share (%), by Types 2025 & 2033

- Figure 23: South America Pigments for Automotive Coatings Revenue (million), by Country 2025 & 2033

- Figure 24: South America Pigments for Automotive Coatings Volume (K), by Country 2025 & 2033

- Figure 25: South America Pigments for Automotive Coatings Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Pigments for Automotive Coatings Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Pigments for Automotive Coatings Revenue (million), by Application 2025 & 2033

- Figure 28: Europe Pigments for Automotive Coatings Volume (K), by Application 2025 & 2033

- Figure 29: Europe Pigments for Automotive Coatings Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe Pigments for Automotive Coatings Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe Pigments for Automotive Coatings Revenue (million), by Types 2025 & 2033

- Figure 32: Europe Pigments for Automotive Coatings Volume (K), by Types 2025 & 2033

- Figure 33: Europe Pigments for Automotive Coatings Revenue Share (%), by Types 2025 & 2033

- Figure 34: Europe Pigments for Automotive Coatings Volume Share (%), by Types 2025 & 2033

- Figure 35: Europe Pigments for Automotive Coatings Revenue (million), by Country 2025 & 2033

- Figure 36: Europe Pigments for Automotive Coatings Volume (K), by Country 2025 & 2033

- Figure 37: Europe Pigments for Automotive Coatings Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Pigments for Automotive Coatings Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa Pigments for Automotive Coatings Revenue (million), by Application 2025 & 2033

- Figure 40: Middle East & Africa Pigments for Automotive Coatings Volume (K), by Application 2025 & 2033

- Figure 41: Middle East & Africa Pigments for Automotive Coatings Revenue Share (%), by Application 2025 & 2033

- Figure 42: Middle East & Africa Pigments for Automotive Coatings Volume Share (%), by Application 2025 & 2033

- Figure 43: Middle East & Africa Pigments for Automotive Coatings Revenue (million), by Types 2025 & 2033

- Figure 44: Middle East & Africa Pigments for Automotive Coatings Volume (K), by Types 2025 & 2033

- Figure 45: Middle East & Africa Pigments for Automotive Coatings Revenue Share (%), by Types 2025 & 2033

- Figure 46: Middle East & Africa Pigments for Automotive Coatings Volume Share (%), by Types 2025 & 2033

- Figure 47: Middle East & Africa Pigments for Automotive Coatings Revenue (million), by Country 2025 & 2033

- Figure 48: Middle East & Africa Pigments for Automotive Coatings Volume (K), by Country 2025 & 2033

- Figure 49: Middle East & Africa Pigments for Automotive Coatings Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa Pigments for Automotive Coatings Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific Pigments for Automotive Coatings Revenue (million), by Application 2025 & 2033

- Figure 52: Asia Pacific Pigments for Automotive Coatings Volume (K), by Application 2025 & 2033

- Figure 53: Asia Pacific Pigments for Automotive Coatings Revenue Share (%), by Application 2025 & 2033

- Figure 54: Asia Pacific Pigments for Automotive Coatings Volume Share (%), by Application 2025 & 2033

- Figure 55: Asia Pacific Pigments for Automotive Coatings Revenue (million), by Types 2025 & 2033

- Figure 56: Asia Pacific Pigments for Automotive Coatings Volume (K), by Types 2025 & 2033

- Figure 57: Asia Pacific Pigments for Automotive Coatings Revenue Share (%), by Types 2025 & 2033

- Figure 58: Asia Pacific Pigments for Automotive Coatings Volume Share (%), by Types 2025 & 2033

- Figure 59: Asia Pacific Pigments for Automotive Coatings Revenue (million), by Country 2025 & 2033

- Figure 60: Asia Pacific Pigments for Automotive Coatings Volume (K), by Country 2025 & 2033

- Figure 61: Asia Pacific Pigments for Automotive Coatings Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific Pigments for Automotive Coatings Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Pigments for Automotive Coatings Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Pigments for Automotive Coatings Volume K Forecast, by Application 2020 & 2033

- Table 3: Global Pigments for Automotive Coatings Revenue million Forecast, by Types 2020 & 2033

- Table 4: Global Pigments for Automotive Coatings Volume K Forecast, by Types 2020 & 2033

- Table 5: Global Pigments for Automotive Coatings Revenue million Forecast, by Region 2020 & 2033

- Table 6: Global Pigments for Automotive Coatings Volume K Forecast, by Region 2020 & 2033

- Table 7: Global Pigments for Automotive Coatings Revenue million Forecast, by Application 2020 & 2033

- Table 8: Global Pigments for Automotive Coatings Volume K Forecast, by Application 2020 & 2033

- Table 9: Global Pigments for Automotive Coatings Revenue million Forecast, by Types 2020 & 2033

- Table 10: Global Pigments for Automotive Coatings Volume K Forecast, by Types 2020 & 2033

- Table 11: Global Pigments for Automotive Coatings Revenue million Forecast, by Country 2020 & 2033

- Table 12: Global Pigments for Automotive Coatings Volume K Forecast, by Country 2020 & 2033

- Table 13: United States Pigments for Automotive Coatings Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: United States Pigments for Automotive Coatings Volume (K) Forecast, by Application 2020 & 2033

- Table 15: Canada Pigments for Automotive Coatings Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Canada Pigments for Automotive Coatings Volume (K) Forecast, by Application 2020 & 2033

- Table 17: Mexico Pigments for Automotive Coatings Revenue (million) Forecast, by Application 2020 & 2033

- Table 18: Mexico Pigments for Automotive Coatings Volume (K) Forecast, by Application 2020 & 2033

- Table 19: Global Pigments for Automotive Coatings Revenue million Forecast, by Application 2020 & 2033

- Table 20: Global Pigments for Automotive Coatings Volume K Forecast, by Application 2020 & 2033

- Table 21: Global Pigments for Automotive Coatings Revenue million Forecast, by Types 2020 & 2033

- Table 22: Global Pigments for Automotive Coatings Volume K Forecast, by Types 2020 & 2033

- Table 23: Global Pigments for Automotive Coatings Revenue million Forecast, by Country 2020 & 2033

- Table 24: Global Pigments for Automotive Coatings Volume K Forecast, by Country 2020 & 2033

- Table 25: Brazil Pigments for Automotive Coatings Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Brazil Pigments for Automotive Coatings Volume (K) Forecast, by Application 2020 & 2033

- Table 27: Argentina Pigments for Automotive Coatings Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Argentina Pigments for Automotive Coatings Volume (K) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America Pigments for Automotive Coatings Revenue (million) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America Pigments for Automotive Coatings Volume (K) Forecast, by Application 2020 & 2033

- Table 31: Global Pigments for Automotive Coatings Revenue million Forecast, by Application 2020 & 2033

- Table 32: Global Pigments for Automotive Coatings Volume K Forecast, by Application 2020 & 2033

- Table 33: Global Pigments for Automotive Coatings Revenue million Forecast, by Types 2020 & 2033

- Table 34: Global Pigments for Automotive Coatings Volume K Forecast, by Types 2020 & 2033

- Table 35: Global Pigments for Automotive Coatings Revenue million Forecast, by Country 2020 & 2033

- Table 36: Global Pigments for Automotive Coatings Volume K Forecast, by Country 2020 & 2033

- Table 37: United Kingdom Pigments for Automotive Coatings Revenue (million) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom Pigments for Automotive Coatings Volume (K) Forecast, by Application 2020 & 2033

- Table 39: Germany Pigments for Automotive Coatings Revenue (million) Forecast, by Application 2020 & 2033

- Table 40: Germany Pigments for Automotive Coatings Volume (K) Forecast, by Application 2020 & 2033

- Table 41: France Pigments for Automotive Coatings Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: France Pigments for Automotive Coatings Volume (K) Forecast, by Application 2020 & 2033

- Table 43: Italy Pigments for Automotive Coatings Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: Italy Pigments for Automotive Coatings Volume (K) Forecast, by Application 2020 & 2033

- Table 45: Spain Pigments for Automotive Coatings Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Spain Pigments for Automotive Coatings Volume (K) Forecast, by Application 2020 & 2033

- Table 47: Russia Pigments for Automotive Coatings Revenue (million) Forecast, by Application 2020 & 2033

- Table 48: Russia Pigments for Automotive Coatings Volume (K) Forecast, by Application 2020 & 2033

- Table 49: Benelux Pigments for Automotive Coatings Revenue (million) Forecast, by Application 2020 & 2033

- Table 50: Benelux Pigments for Automotive Coatings Volume (K) Forecast, by Application 2020 & 2033

- Table 51: Nordics Pigments for Automotive Coatings Revenue (million) Forecast, by Application 2020 & 2033

- Table 52: Nordics Pigments for Automotive Coatings Volume (K) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe Pigments for Automotive Coatings Revenue (million) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe Pigments for Automotive Coatings Volume (K) Forecast, by Application 2020 & 2033

- Table 55: Global Pigments for Automotive Coatings Revenue million Forecast, by Application 2020 & 2033

- Table 56: Global Pigments for Automotive Coatings Volume K Forecast, by Application 2020 & 2033

- Table 57: Global Pigments for Automotive Coatings Revenue million Forecast, by Types 2020 & 2033

- Table 58: Global Pigments for Automotive Coatings Volume K Forecast, by Types 2020 & 2033

- Table 59: Global Pigments for Automotive Coatings Revenue million Forecast, by Country 2020 & 2033

- Table 60: Global Pigments for Automotive Coatings Volume K Forecast, by Country 2020 & 2033

- Table 61: Turkey Pigments for Automotive Coatings Revenue (million) Forecast, by Application 2020 & 2033

- Table 62: Turkey Pigments for Automotive Coatings Volume (K) Forecast, by Application 2020 & 2033

- Table 63: Israel Pigments for Automotive Coatings Revenue (million) Forecast, by Application 2020 & 2033

- Table 64: Israel Pigments for Automotive Coatings Volume (K) Forecast, by Application 2020 & 2033

- Table 65: GCC Pigments for Automotive Coatings Revenue (million) Forecast, by Application 2020 & 2033

- Table 66: GCC Pigments for Automotive Coatings Volume (K) Forecast, by Application 2020 & 2033

- Table 67: North Africa Pigments for Automotive Coatings Revenue (million) Forecast, by Application 2020 & 2033

- Table 68: North Africa Pigments for Automotive Coatings Volume (K) Forecast, by Application 2020 & 2033

- Table 69: South Africa Pigments for Automotive Coatings Revenue (million) Forecast, by Application 2020 & 2033

- Table 70: South Africa Pigments for Automotive Coatings Volume (K) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa Pigments for Automotive Coatings Revenue (million) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa Pigments for Automotive Coatings Volume (K) Forecast, by Application 2020 & 2033

- Table 73: Global Pigments for Automotive Coatings Revenue million Forecast, by Application 2020 & 2033

- Table 74: Global Pigments for Automotive Coatings Volume K Forecast, by Application 2020 & 2033

- Table 75: Global Pigments for Automotive Coatings Revenue million Forecast, by Types 2020 & 2033

- Table 76: Global Pigments for Automotive Coatings Volume K Forecast, by Types 2020 & 2033

- Table 77: Global Pigments for Automotive Coatings Revenue million Forecast, by Country 2020 & 2033

- Table 78: Global Pigments for Automotive Coatings Volume K Forecast, by Country 2020 & 2033

- Table 79: China Pigments for Automotive Coatings Revenue (million) Forecast, by Application 2020 & 2033

- Table 80: China Pigments for Automotive Coatings Volume (K) Forecast, by Application 2020 & 2033

- Table 81: India Pigments for Automotive Coatings Revenue (million) Forecast, by Application 2020 & 2033

- Table 82: India Pigments for Automotive Coatings Volume (K) Forecast, by Application 2020 & 2033

- Table 83: Japan Pigments for Automotive Coatings Revenue (million) Forecast, by Application 2020 & 2033

- Table 84: Japan Pigments for Automotive Coatings Volume (K) Forecast, by Application 2020 & 2033

- Table 85: South Korea Pigments for Automotive Coatings Revenue (million) Forecast, by Application 2020 & 2033

- Table 86: South Korea Pigments for Automotive Coatings Volume (K) Forecast, by Application 2020 & 2033

- Table 87: ASEAN Pigments for Automotive Coatings Revenue (million) Forecast, by Application 2020 & 2033

- Table 88: ASEAN Pigments for Automotive Coatings Volume (K) Forecast, by Application 2020 & 2033

- Table 89: Oceania Pigments for Automotive Coatings Revenue (million) Forecast, by Application 2020 & 2033

- Table 90: Oceania Pigments for Automotive Coatings Volume (K) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific Pigments for Automotive Coatings Revenue (million) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific Pigments for Automotive Coatings Volume (K) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Pigments for Automotive Coatings?

The projected CAGR is approximately XX%.

2. Which companies are prominent players in the Pigments for Automotive Coatings?

Key companies in the market include Heubach (Clariant), Vibrantz, Oxerra(Venator), Chemours, LANXESS, DIC Corporation, Tronox, Kronos Worldwide, Alabama Pigments, DCL Corporation, TOMATEC, The Shepherd Color Company, Toyo Ink, Sudarshan, Ultramarine and Pigments Limited, Asahi Kasei Kogyo, Noelson Chemicals, R.S. Pigments, ECKART, Gpro Titanium Industry, CNNC HUA YUAN Titanium Dioxide, YUXING PIGMENT, Sunlour Pigment, Fulln Chemical, Hunan Jufa Pigment, Cadello, ZhongLong Materials Limited, Shanghai Fulcolor Advanced Materials.

3. What are the main segments of the Pigments for Automotive Coatings?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Pigments for Automotive Coatings," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Pigments for Automotive Coatings report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Pigments for Automotive Coatings?

To stay informed about further developments, trends, and reports in the Pigments for Automotive Coatings, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence