Key Insights

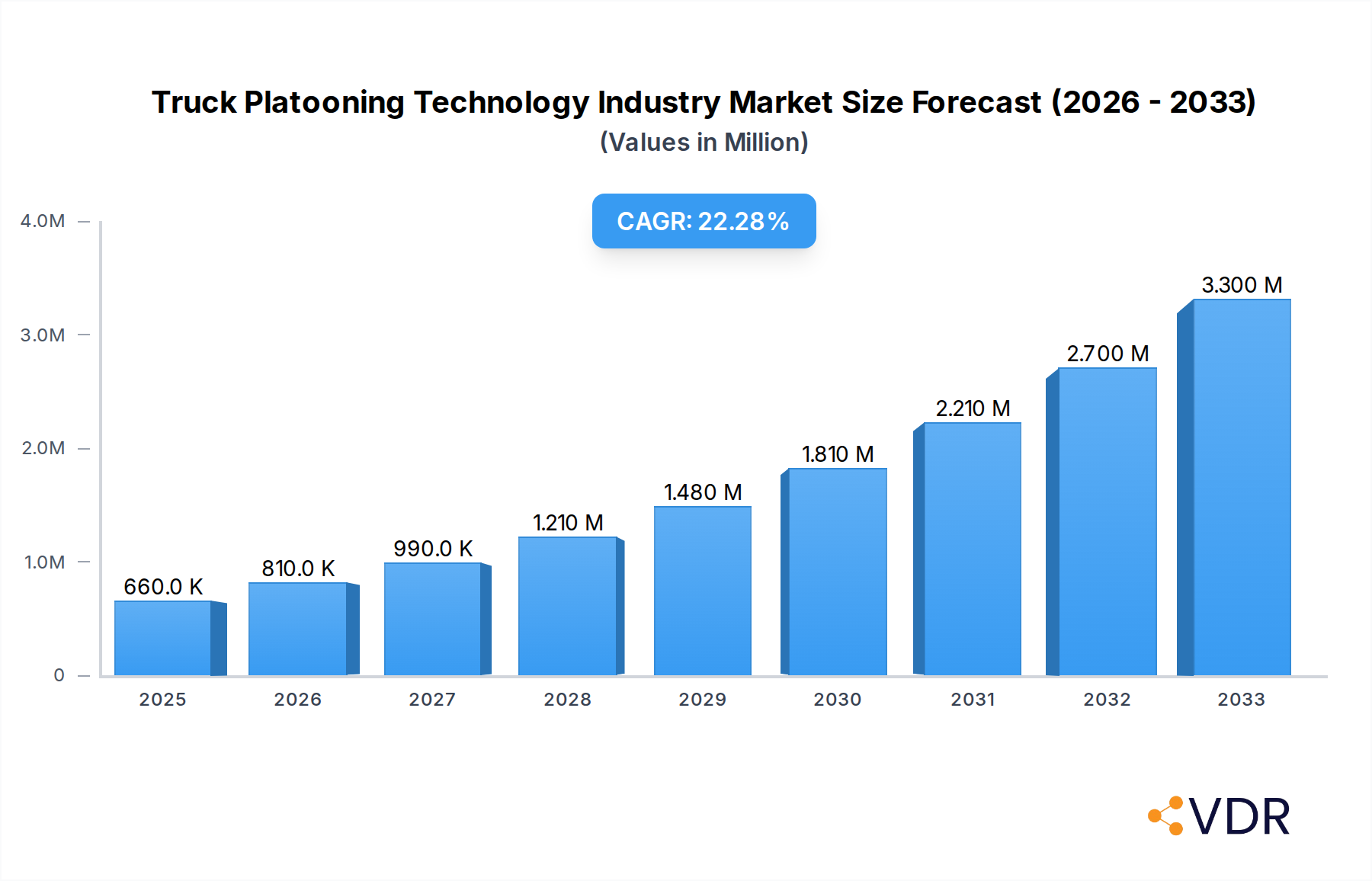

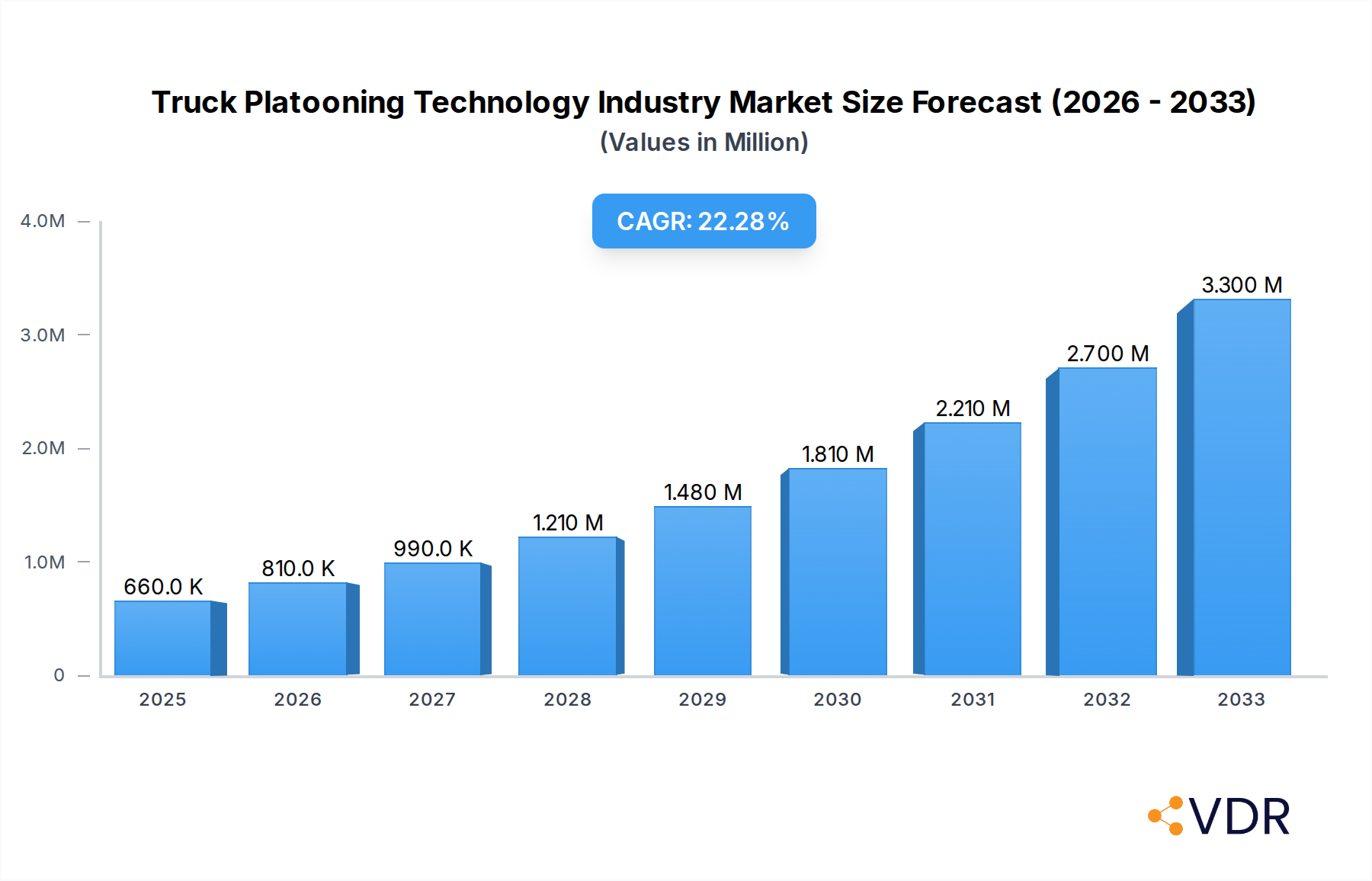

The global Truck Platooning Technology market is poised for remarkable expansion, projected to reach $0.66 million by 2025 and thereafter experience a substantial Compound Annual Growth Rate (CAGR) of 22.25% through 2033. This aggressive growth trajectory is primarily fueled by the increasing demand for enhanced fuel efficiency and reduced operational costs within the logistics and transportation sectors. Truck platooning, which enables vehicles to electronically link and travel in close formation, significantly cuts down on aerodynamic drag, leading to substantial fuel savings. Furthermore, government initiatives promoting autonomous vehicle technology and stricter regulations on emissions are acting as significant catalysts for market adoption. The integration of advanced driver-assistance systems (ADAS) and the ongoing development of vehicle-to-vehicle (V2V) and vehicle-to-infrastructure (V2I) communication technologies are critical enablers, driving innovation and adoption across the industry.

Truck Platooning Technology Industry Market Size (In Million)

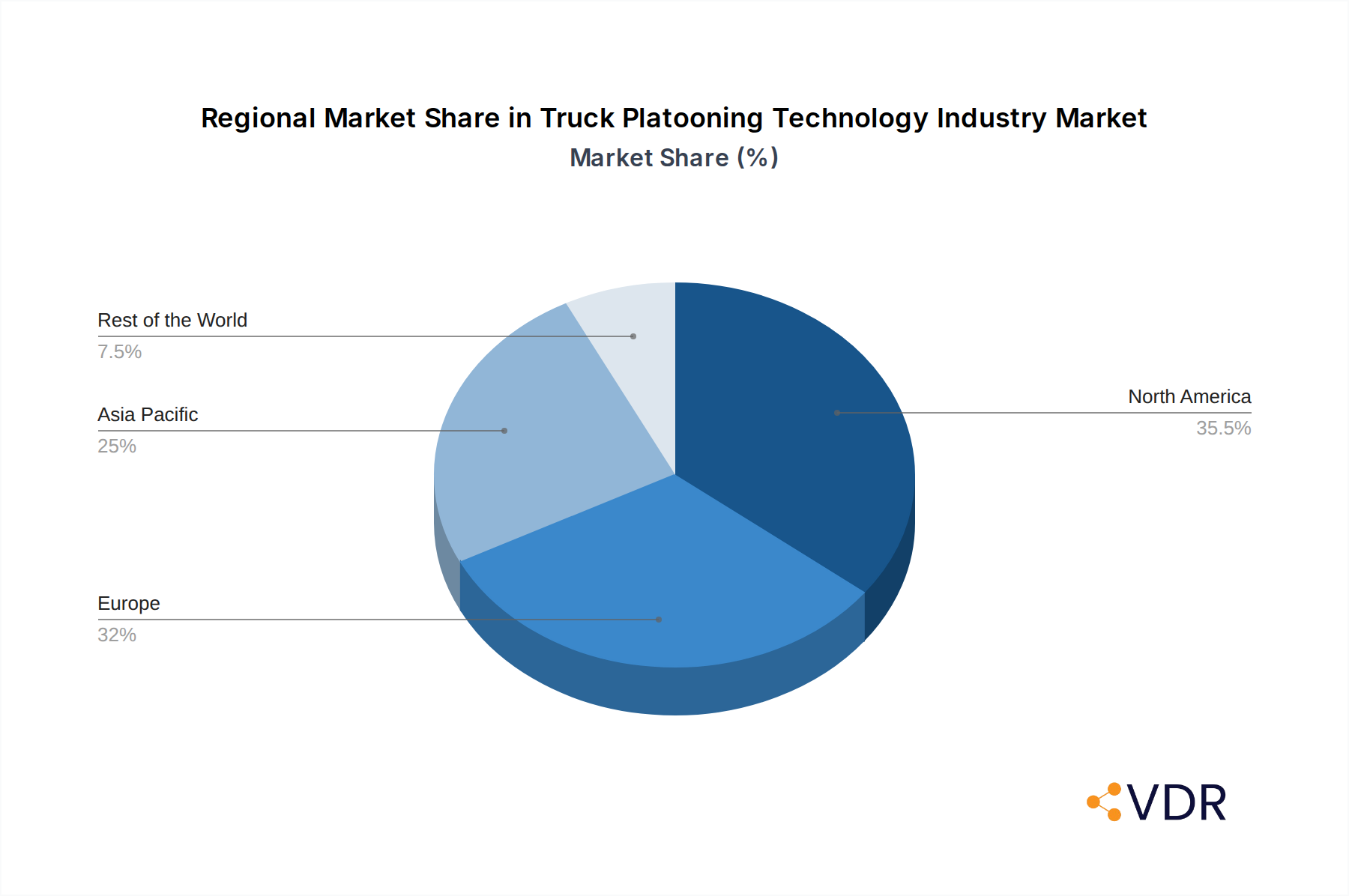

The market is segmented across various platooning types, technology types, and infrastructure types. Driver-Assistive Truck Platooning (DATP) and Autonomous Truck Platooning are the key platooning categories, with DATP expected to lead in the initial phases due to regulatory hurdles for full autonomy. Key technologies underpinning this market include Adaptive Cruise Control (ACC), Forward Collision Warning (FCW), Automated Emergency Braking (AEB), Active Brake Assist (ABA), and Lane Keep Assist (LKA). The advancement and widespread adoption of these technologies are integral to achieving safe and efficient platooning. Geographically, North America and Europe are anticipated to dominate the market, driven by established logistics networks, supportive regulatory frameworks, and early investments in autonomous driving technologies. However, the Asia Pacific region, particularly China and India, presents a significant growth opportunity due to its rapidly expanding e-commerce sector and increasing adoption of advanced transportation solutions. Key players like Daimler Truck AG, WABCO Holdings Inc., and Continental AG are at the forefront, investing heavily in research and development to secure a competitive edge in this burgeoning market.

Truck Platooning Technology Industry Company Market Share

Truck Platooning Technology Industry Report Description: Unlocking the Future of Logistics

This comprehensive report offers an in-depth analysis of the truck platooning technology market, exploring its intricate dynamics, growth trajectories, and the pivotal role it plays in revolutionizing the global logistics sector. With a forecast period extending from 2025–2033, this study provides unparalleled insights into market size, adoption rates, and technological advancements shaping the future of freight transportation. Dive into the parent market of Autonomous Trucking and its child market, Connected Trucking, to understand the broader ecosystem influencing truck platooning.

Truck Platooning Technology Industry Market Dynamics & Structure

The truck platooning technology industry exhibits a dynamic and evolving market structure, characterized by increasing collaboration and strategic alliances among key players. Market concentration is moderate, with a blend of established automotive giants and specialized technology providers vying for dominance. Technological innovation is a primary driver, fueled by the relentless pursuit of enhanced fuel efficiency, reduced emissions, and improved road safety. Regulatory frameworks, though still developing in many regions, are gradually becoming more supportive, paving the way for wider deployment. Competitive product substitutes, such as traditional long-haul trucking with advanced driver-assistance systems (ADAS), are present but are increasingly being challenged by the unique advantages of platooning. End-user demographics are shifting towards large fleet operators and logistics companies prioritizing operational cost reductions and supply chain optimization. Mergers and acquisitions (M&A) trends are on the rise as companies seek to consolidate expertise and accelerate market penetration. For instance, the historical period (2019-2024) saw several smaller technology firms being acquired by larger automotive manufacturers and technology conglomerates to integrate platooning capabilities into their product portfolios.

- Market Concentration: Moderate, with emerging consolidation trends.

- Technological Innovation Drivers: Fuel efficiency, safety, emissions reduction, driver shortage mitigation.

- Regulatory Frameworks: Evolving, with increasing government support for pilot programs and infrastructure development.

- Competitive Product Substitutes: Advanced Driver-Assistance Systems (ADAS) in conventional trucks.

- End-User Demographics: Large fleet operators, third-party logistics (3PL) providers, e-commerce fulfillment centers.

- M&A Trends: Increasing as companies seek to acquire critical technologies and market access.

Truck Platooning Technology Industry Growth Trends & Insights

The truck platooning technology industry is poised for significant growth, driven by a confluence of economic imperatives and technological advancements. The market size is projected to witness a substantial expansion from an estimated USD XXX million in 2025 to exceed USD XXX million by 2033, exhibiting a robust Compound Annual Growth Rate (CAGR) of XX.X% during the forecast period. Adoption rates are steadily increasing as early adopters demonstrate the tangible benefits of platooning, including substantial fuel savings of up to 15% and a reduction in CO2 emissions. Technological disruptions, such as the advancement of 5G connectivity and sophisticated AI algorithms, are enabling more seamless and reliable platooning operations. Consumer behavior shifts are also playing a role, with an increased demand for faster and more cost-effective freight delivery pushing logistics companies to explore innovative solutions like truck platooning. The integration of platooning capabilities is no longer a distant prospect but a rapidly materializing reality.

The market penetration of truck platooning technology, while still nascent, is expected to accelerate rapidly. Early deployments are focusing on specific routes and use cases, such as highway transit and dedicated freight corridors. The ability to form virtual couplings between trucks, enabling them to travel closely together, significantly reduces aerodynamic drag for trailing vehicles, leading to substantial fuel cost savings. This economic incentive is a primary catalyst for adoption among fleet managers. Furthermore, the ongoing global driver shortage is creating a pressing need for technologies that can optimize operational efficiency and reduce reliance on human drivers for every mile driven. Truck platooning, by enabling a single driver to oversee multiple platooning trucks or by facilitating driver breaks during long-haul journeys, offers a partial solution to this persistent challenge.

The evolution of autonomous truck platooning is a key trend, moving beyond driver-assistive modes. As the technology matures and regulatory frameworks adapt, fully autonomous platoons are expected to become more prevalent, further amplifying the benefits of reduced labor costs and increased operational uptime. The development of robust Vehicle-to-Vehicle (V2V) and Vehicle-to-Infrastructure (V2I) communication systems is crucial for the safe and efficient functioning of platoons. These communication protocols enable trucks to share real-time data about speed, braking, and steering, allowing for instantaneous adjustments and maintaining tight platooning formations. The impact of these advancements on consumer behavior is indirect but significant; as logistics become more efficient and cost-effective, consumers will benefit from lower shipping costs and potentially faster delivery times. The increasing investment in R&D by major automotive manufacturers and technology providers underscores the industry's confidence in the transformative potential of truck platooning.

Dominant Regions, Countries, or Segments in Truck Platooning Technology Industry

The North America region is emerging as a dominant force in the truck platooning technology industry, driven by a combination of strong economic incentives, a developed highway infrastructure, and proactive government initiatives. Within North America, the United States stands out as a leading country, with numerous pilot programs and testing grounds facilitating the advancement of platooning technologies. The Driver-Assistive Truck Platooning (DATP) segment is currently leading the market growth due to its lower regulatory hurdles and immediate applicability in enhancing existing fleet operations. However, the rapid development in Autonomous Truck Platooning signals a future shift in market leadership.

Key drivers for North America's dominance include significant investments in logistics and supply chain optimization by large corporations and a well-established trucking industry facing persistent driver shortages. The adoption of Adaptive Cruise Control (ACC) and Forward Collision Warning (FCW) technologies within platooning systems is widespread, serving as foundational elements. As the technology matures, Automated Emergency Braking (AEB) and Lane Keep Assist (LKA) will become increasingly critical for ensuring safety within platoons, further propelling their adoption.

The Infrastructure Type segment of Vehicle-to-Vehicle (V2V) communication is paramount, enabling the core functionality of platooning. This is complemented by Vehicle-to-Infrastructure (V2I) communication, which facilitates traffic management and real-time updates from road authorities. The integration of Global Positioning System (GPS) remains fundamental for navigation and coordination.

- Dominant Region: North America

- Leading Country: United States

- Key Drivers: Economic incentives, robust highway infrastructure, supportive regulatory environment, driver shortage, investment in logistics.

- Dominant Platooning Type: Driver-Assistive Truck Platooning (DATP)

- Growth Potential: Autonomous Truck Platooning poised for significant future growth.

- Dominant Technology Type: Adaptive Cruise Control (ACC), Forward Collision Warning (FCW)

- Emerging Importance: Automated Emergency Braking (AEB), Lane Keep Assist (LKA).

- Dominant Infrastructure Type: Vehicle-to-Vehicle (V2V) communication

- Complementary Infrastructure: Vehicle-to-Infrastructure (V2I), Global Positioning System (GPS).

Truck Platooning Technology Industry Product Landscape

The product landscape of the truck platooning technology industry is characterized by continuous innovation in sensor fusion, artificial intelligence, and communication systems. Leading companies are developing integrated solutions that combine advanced ADAS features with robust V2V communication protocols. Products range from software modules enhancing existing truck systems to complete platooning hardware kits. Unique selling propositions often revolve around the demonstrated improvements in fuel efficiency, safety enhancements through reduced reaction times, and the potential for increased operational uptime. Technological advancements focus on achieving higher levels of automation and reliability, with a strong emphasis on cybersecurity to protect sensitive communication data.

Key Drivers, Barriers & Challenges in Truck Platooning Technology Industry

The truck platooning technology industry is propelled by several key drivers, primarily the pursuit of enhanced fuel efficiency and significant cost reductions in freight transportation. The global driver shortage crisis also acts as a powerful catalyst, driving the demand for automated solutions. Technological advancements in AI, sensor technology, and wireless communication are enabling more sophisticated and reliable platooning systems. Furthermore, government initiatives and pilot programs aimed at promoting innovation and sustainability in the logistics sector are providing crucial support.

However, the industry faces substantial barriers and challenges. Regulatory hurdles remain a significant restraint, with a lack of standardized regulations across different jurisdictions hindering widespread deployment. Public perception and acceptance of autonomous vehicle technology, particularly in a commercial context, require continuous effort to build trust and confidence. The high initial investment cost for platooning technology can be a deterrent for smaller operators. Furthermore, ensuring the robust cybersecurity of V2V and V2I communication systems is paramount to prevent potential breaches and ensure operational safety. Supply chain disruptions and the availability of specialized components also pose ongoing challenges.

Emerging Opportunities in Truck Platooning Technology Industry

Emerging opportunities in the truck platooning technology industry lie in the expansion into new geographical markets and the development of specialized applications. Untapped markets in developing economies present a significant growth potential as they seek to modernize their logistics infrastructure. Innovative applications, such as platooning for last-mile delivery in urban environments and specialized platooning for industries like mining and agriculture, are poised to gain traction. Evolving consumer preferences for faster and more sustainable delivery options are also creating a favorable environment for the adoption of advanced platooning solutions. The integration of platooning with smart city initiatives and logistics hubs offers further avenues for innovation and market penetration.

Growth Accelerators in the Truck Platooning Technology Industry Industry

The long-term growth of the truck platooning technology industry is being accelerated by transformative technological breakthroughs and strategic market expansion. The ongoing advancements in artificial intelligence and machine learning are enabling more sophisticated decision-making capabilities for platooning vehicles, leading to enhanced safety and efficiency. Strategic partnerships between technology providers, truck manufacturers, and logistics companies are crucial for fostering collaboration, sharing expertise, and accelerating the development and deployment of platooning solutions. Market expansion strategies, including the establishment of platooning corridors and the development of robust charging and maintenance infrastructure for electric and autonomous fleets, will be vital in driving sustained growth.

Key Players Shaping the Truck Platooning Technology Industry Market

- Daimler Truck AG

- Wabco Holdings Inc

- NXP Semiconductors N V

- Toyota Motor Corporation (Toyota Tsusho)

- ZF Friedrichshafen

- Continental AG

- Peloton Technology

- Hyundai Motor Company

- Paccar Inc (DAF Trucks)

- Robert Bosch GmbH

- Iveco S p A

- Volkswagen Group (MAN Scania)

- Knorr-Bremse AG

- AB Volvo

Notable Milestones in Truck Platooning Technology Industry Sector

- December 2023: Softbank partnered with West Japan Railway Company to research 5G-enabled V2V technology for BRT systems and truck platooning on Japanese highways, aiming to enhance the logistics sector and address driver shortages.

- July 2023: FPInnovations collaborated with Robotic Research Autonomous Industries (RRAI) to adapt its self-driving technology for the off-highway forestry sector, completing initial tests for its off-highway truck platooning project to address lower-qualified drivers in Canada's forestry sector. Funding of nearly USD 1 million was provided by Société du Plan Nord and Natural Resources Canada.

- March 2023: Ohmio collaborated with the Port Authority of New York and New Jersey to host a three-vehicle platooning demonstration at John F. Kennedy International Airport, featuring eight driverless passenger shuttles in a platoon of three unconnected vehicles.

In-Depth Truck Platooning Technology Industry Market Outlook

The truck platooning technology industry is set for substantial future growth, with future market potential driven by increasing demand for efficiency and sustainability in freight transportation. Strategic opportunities include the further development and deployment of fully autonomous platooning systems, offering unparalleled cost savings and operational benefits. The integration of platooning with emerging technologies like electric powertrains and advanced data analytics will unlock new levels of performance. Collaboration between public and private sectors to establish dedicated platooning infrastructure and standardized regulatory frameworks will be crucial for market expansion. The industry's outlook is bright, promising a transformative impact on global logistics and supply chains.

Truck Platooning Technology Industry Segmentation

-

1. Platooning Type

- 1.1. Driver-Assistive Truck Platooning (DATP)

- 1.2. Autonomous Truck Platooning

-

2. Technology Type

- 2.1. Adaptive Cruise Control

- 2.2. Forward Collision Warning

- 2.3. Automated Emergency Braking

- 2.4. Active Brake Assist

- 2.5. Lane Keep Assist

- 2.6. Others (Blind Spot Warning, etc.)

-

3. Infrastructure Type

- 3.1. Vehicle-to-Vehicle (V2V)

- 3.2. Vehicle-to-Infrastructure (V2I)

- 3.3. Global Positioning System (GPS)

Truck Platooning Technology Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Rest of North America

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Spain

- 2.5. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. India

- 3.3. Japan

- 3.4. South Korea

- 3.5. Rest of Asia Pacific

-

4. Rest of the World

- 4.1. South America

- 4.2. Middle East and Africa

Truck Platooning Technology Industry Regional Market Share

Geographic Coverage of Truck Platooning Technology Industry

Truck Platooning Technology Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 22.25% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Platooning Type

- 5.1.1. Driver-Assistive Truck Platooning (DATP)

- 5.1.2. Autonomous Truck Platooning

- 5.2. Market Analysis, Insights and Forecast - by Technology Type

- 5.2.1. Adaptive Cruise Control

- 5.2.2. Forward Collision Warning

- 5.2.3. Automated Emergency Braking

- 5.2.4. Active Brake Assist

- 5.2.5. Lane Keep Assist

- 5.2.6. Others (Blind Spot Warning, etc.)

- 5.3. Market Analysis, Insights and Forecast - by Infrastructure Type

- 5.3.1. Vehicle-to-Vehicle (V2V)

- 5.3.2. Vehicle-to-Infrastructure (V2I)

- 5.3.3. Global Positioning System (GPS)

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by Platooning Type

- 6. Global Truck Platooning Technology Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Platooning Type

- 6.1.1. Driver-Assistive Truck Platooning (DATP)

- 6.1.2. Autonomous Truck Platooning

- 6.2. Market Analysis, Insights and Forecast - by Technology Type

- 6.2.1. Adaptive Cruise Control

- 6.2.2. Forward Collision Warning

- 6.2.3. Automated Emergency Braking

- 6.2.4. Active Brake Assist

- 6.2.5. Lane Keep Assist

- 6.2.6. Others (Blind Spot Warning, etc.)

- 6.3. Market Analysis, Insights and Forecast - by Infrastructure Type

- 6.3.1. Vehicle-to-Vehicle (V2V)

- 6.3.2. Vehicle-to-Infrastructure (V2I)

- 6.3.3. Global Positioning System (GPS)

- 6.1. Market Analysis, Insights and Forecast - by Platooning Type

- 7. North America Truck Platooning Technology Industry Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Platooning Type

- 7.1.1. Driver-Assistive Truck Platooning (DATP)

- 7.1.2. Autonomous Truck Platooning

- 7.2. Market Analysis, Insights and Forecast - by Technology Type

- 7.2.1. Adaptive Cruise Control

- 7.2.2. Forward Collision Warning

- 7.2.3. Automated Emergency Braking

- 7.2.4. Active Brake Assist

- 7.2.5. Lane Keep Assist

- 7.2.6. Others (Blind Spot Warning, etc.)

- 7.3. Market Analysis, Insights and Forecast - by Infrastructure Type

- 7.3.1. Vehicle-to-Vehicle (V2V)

- 7.3.2. Vehicle-to-Infrastructure (V2I)

- 7.3.3. Global Positioning System (GPS)

- 7.1. Market Analysis, Insights and Forecast - by Platooning Type

- 8. Europe Truck Platooning Technology Industry Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Platooning Type

- 8.1.1. Driver-Assistive Truck Platooning (DATP)

- 8.1.2. Autonomous Truck Platooning

- 8.2. Market Analysis, Insights and Forecast - by Technology Type

- 8.2.1. Adaptive Cruise Control

- 8.2.2. Forward Collision Warning

- 8.2.3. Automated Emergency Braking

- 8.2.4. Active Brake Assist

- 8.2.5. Lane Keep Assist

- 8.2.6. Others (Blind Spot Warning, etc.)

- 8.3. Market Analysis, Insights and Forecast - by Infrastructure Type

- 8.3.1. Vehicle-to-Vehicle (V2V)

- 8.3.2. Vehicle-to-Infrastructure (V2I)

- 8.3.3. Global Positioning System (GPS)

- 8.1. Market Analysis, Insights and Forecast - by Platooning Type

- 9. Asia Pacific Truck Platooning Technology Industry Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Platooning Type

- 9.1.1. Driver-Assistive Truck Platooning (DATP)

- 9.1.2. Autonomous Truck Platooning

- 9.2. Market Analysis, Insights and Forecast - by Technology Type

- 9.2.1. Adaptive Cruise Control

- 9.2.2. Forward Collision Warning

- 9.2.3. Automated Emergency Braking

- 9.2.4. Active Brake Assist

- 9.2.5. Lane Keep Assist

- 9.2.6. Others (Blind Spot Warning, etc.)

- 9.3. Market Analysis, Insights and Forecast - by Infrastructure Type

- 9.3.1. Vehicle-to-Vehicle (V2V)

- 9.3.2. Vehicle-to-Infrastructure (V2I)

- 9.3.3. Global Positioning System (GPS)

- 9.1. Market Analysis, Insights and Forecast - by Platooning Type

- 10. Rest of the World Truck Platooning Technology Industry Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Platooning Type

- 10.1.1. Driver-Assistive Truck Platooning (DATP)

- 10.1.2. Autonomous Truck Platooning

- 10.2. Market Analysis, Insights and Forecast - by Technology Type

- 10.2.1. Adaptive Cruise Control

- 10.2.2. Forward Collision Warning

- 10.2.3. Automated Emergency Braking

- 10.2.4. Active Brake Assist

- 10.2.5. Lane Keep Assist

- 10.2.6. Others (Blind Spot Warning, etc.)

- 10.3. Market Analysis, Insights and Forecast - by Infrastructure Type

- 10.3.1. Vehicle-to-Vehicle (V2V)

- 10.3.2. Vehicle-to-Infrastructure (V2I)

- 10.3.3. Global Positioning System (GPS)

- 10.1. Market Analysis, Insights and Forecast - by Platooning Type

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 Daimler Truck AG

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 Wabco Holdings Inc

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 NXP Semiconductors N V

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 Toyota Motor Corporation (Toyota Tsusho)

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 ZF Friedrichshafen

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 Continental AG

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 Peloton Technology

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 Hyundai Motor Company

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 Paccar Inc (DAF Trucks)

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.10 Robert Bosch GmbH

- 11.1.10.1. Company Overview

- 11.1.10.2. Products

- 11.1.10.3. Company Financials

- 11.1.10.4. SWOT Analysis

- 11.1.11 Iveco S p A

- 11.1.11.1. Company Overview

- 11.1.11.2. Products

- 11.1.11.3. Company Financials

- 11.1.11.4. SWOT Analysis

- 11.1.12 Volkswagen Group (MAN Scania)

- 11.1.12.1. Company Overview

- 11.1.12.2. Products

- 11.1.12.3. Company Financials

- 11.1.12.4. SWOT Analysis

- 11.1.13 Knorr-Bremse AG

- 11.1.13.1. Company Overview

- 11.1.13.2. Products

- 11.1.13.3. Company Financials

- 11.1.13.4. SWOT Analysis

- 11.1.14 AB Volvo

- 11.1.14.1. Company Overview

- 11.1.14.2. Products

- 11.1.14.3. Company Financials

- 11.1.14.4. SWOT Analysis

- 11.1.1 Daimler Truck AG

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Global Truck Platooning Technology Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Truck Platooning Technology Industry Revenue (Million), by Platooning Type 2025 & 2033

- Figure 3: North America Truck Platooning Technology Industry Revenue Share (%), by Platooning Type 2025 & 2033

- Figure 4: North America Truck Platooning Technology Industry Revenue (Million), by Technology Type 2025 & 2033

- Figure 5: North America Truck Platooning Technology Industry Revenue Share (%), by Technology Type 2025 & 2033

- Figure 6: North America Truck Platooning Technology Industry Revenue (Million), by Infrastructure Type 2025 & 2033

- Figure 7: North America Truck Platooning Technology Industry Revenue Share (%), by Infrastructure Type 2025 & 2033

- Figure 8: North America Truck Platooning Technology Industry Revenue (Million), by Country 2025 & 2033

- Figure 9: North America Truck Platooning Technology Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe Truck Platooning Technology Industry Revenue (Million), by Platooning Type 2025 & 2033

- Figure 11: Europe Truck Platooning Technology Industry Revenue Share (%), by Platooning Type 2025 & 2033

- Figure 12: Europe Truck Platooning Technology Industry Revenue (Million), by Technology Type 2025 & 2033

- Figure 13: Europe Truck Platooning Technology Industry Revenue Share (%), by Technology Type 2025 & 2033

- Figure 14: Europe Truck Platooning Technology Industry Revenue (Million), by Infrastructure Type 2025 & 2033

- Figure 15: Europe Truck Platooning Technology Industry Revenue Share (%), by Infrastructure Type 2025 & 2033

- Figure 16: Europe Truck Platooning Technology Industry Revenue (Million), by Country 2025 & 2033

- Figure 17: Europe Truck Platooning Technology Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Pacific Truck Platooning Technology Industry Revenue (Million), by Platooning Type 2025 & 2033

- Figure 19: Asia Pacific Truck Platooning Technology Industry Revenue Share (%), by Platooning Type 2025 & 2033

- Figure 20: Asia Pacific Truck Platooning Technology Industry Revenue (Million), by Technology Type 2025 & 2033

- Figure 21: Asia Pacific Truck Platooning Technology Industry Revenue Share (%), by Technology Type 2025 & 2033

- Figure 22: Asia Pacific Truck Platooning Technology Industry Revenue (Million), by Infrastructure Type 2025 & 2033

- Figure 23: Asia Pacific Truck Platooning Technology Industry Revenue Share (%), by Infrastructure Type 2025 & 2033

- Figure 24: Asia Pacific Truck Platooning Technology Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Asia Pacific Truck Platooning Technology Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Rest of the World Truck Platooning Technology Industry Revenue (Million), by Platooning Type 2025 & 2033

- Figure 27: Rest of the World Truck Platooning Technology Industry Revenue Share (%), by Platooning Type 2025 & 2033

- Figure 28: Rest of the World Truck Platooning Technology Industry Revenue (Million), by Technology Type 2025 & 2033

- Figure 29: Rest of the World Truck Platooning Technology Industry Revenue Share (%), by Technology Type 2025 & 2033

- Figure 30: Rest of the World Truck Platooning Technology Industry Revenue (Million), by Infrastructure Type 2025 & 2033

- Figure 31: Rest of the World Truck Platooning Technology Industry Revenue Share (%), by Infrastructure Type 2025 & 2033

- Figure 32: Rest of the World Truck Platooning Technology Industry Revenue (Million), by Country 2025 & 2033

- Figure 33: Rest of the World Truck Platooning Technology Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Truck Platooning Technology Industry Revenue Million Forecast, by Platooning Type 2020 & 2033

- Table 2: Global Truck Platooning Technology Industry Revenue Million Forecast, by Technology Type 2020 & 2033

- Table 3: Global Truck Platooning Technology Industry Revenue Million Forecast, by Infrastructure Type 2020 & 2033

- Table 4: Global Truck Platooning Technology Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 5: Global Truck Platooning Technology Industry Revenue Million Forecast, by Platooning Type 2020 & 2033

- Table 6: Global Truck Platooning Technology Industry Revenue Million Forecast, by Technology Type 2020 & 2033

- Table 7: Global Truck Platooning Technology Industry Revenue Million Forecast, by Infrastructure Type 2020 & 2033

- Table 8: Global Truck Platooning Technology Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 9: United States Truck Platooning Technology Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Canada Truck Platooning Technology Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: Rest of North America Truck Platooning Technology Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: Global Truck Platooning Technology Industry Revenue Million Forecast, by Platooning Type 2020 & 2033

- Table 13: Global Truck Platooning Technology Industry Revenue Million Forecast, by Technology Type 2020 & 2033

- Table 14: Global Truck Platooning Technology Industry Revenue Million Forecast, by Infrastructure Type 2020 & 2033

- Table 15: Global Truck Platooning Technology Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Germany Truck Platooning Technology Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: United Kingdom Truck Platooning Technology Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: France Truck Platooning Technology Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 19: Spain Truck Platooning Technology Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Rest of Europe Truck Platooning Technology Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 21: Global Truck Platooning Technology Industry Revenue Million Forecast, by Platooning Type 2020 & 2033

- Table 22: Global Truck Platooning Technology Industry Revenue Million Forecast, by Technology Type 2020 & 2033

- Table 23: Global Truck Platooning Technology Industry Revenue Million Forecast, by Infrastructure Type 2020 & 2033

- Table 24: Global Truck Platooning Technology Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 25: China Truck Platooning Technology Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: India Truck Platooning Technology Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 27: Japan Truck Platooning Technology Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: South Korea Truck Platooning Technology Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 29: Rest of Asia Pacific Truck Platooning Technology Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: Global Truck Platooning Technology Industry Revenue Million Forecast, by Platooning Type 2020 & 2033

- Table 31: Global Truck Platooning Technology Industry Revenue Million Forecast, by Technology Type 2020 & 2033

- Table 32: Global Truck Platooning Technology Industry Revenue Million Forecast, by Infrastructure Type 2020 & 2033

- Table 33: Global Truck Platooning Technology Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 34: South America Truck Platooning Technology Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 35: Middle East and Africa Truck Platooning Technology Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Truck Platooning Technology Industry?

The projected CAGR is approximately 22.25%.

2. Which companies are prominent players in the Truck Platooning Technology Industry?

Key companies in the market include Daimler Truck AG, Wabco Holdings Inc, NXP Semiconductors N V, Toyota Motor Corporation (Toyota Tsusho), ZF Friedrichshafen, Continental AG, Peloton Technology, Hyundai Motor Company, Paccar Inc (DAF Trucks), Robert Bosch GmbH, Iveco S p A, Volkswagen Group (MAN Scania), Knorr-Bremse AG, AB Volvo.

3. What are the main segments of the Truck Platooning Technology Industry?

The market segments include Platooning Type, Technology Type, Infrastructure Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 0.66 Million as of 2022.

5. What are some drivers contributing to market growth?

Governments' Aggressive Push Towards Lowering Fuel Consumption and Co2 Emission of Vehicles to Foster the Growth of the Market.

6. What are the notable trends driving market growth?

Adaptive Cruise Control Segment to Gain Traction during the Forecast Period.

7. Are there any restraints impacting market growth?

High Cost of Platooning Technology Deters Market Growth.

8. Can you provide examples of recent developments in the market?

In December 2023, Softbank announced its partnership with West Japan Railway Company to research 5G-enabled Vehicle-to-Vehicle (V2V) technology for a Bus Rapid Transit (BRT) system and truck platooning on Japanese highways. The research aims to enhance the country's logistics sector by facilitating advanced communication technology while assisting in addressing the issue of driver shortages.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Truck Platooning Technology Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Truck Platooning Technology Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Truck Platooning Technology Industry?

To stay informed about further developments, trends, and reports in the Truck Platooning Technology Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence