Key Insights

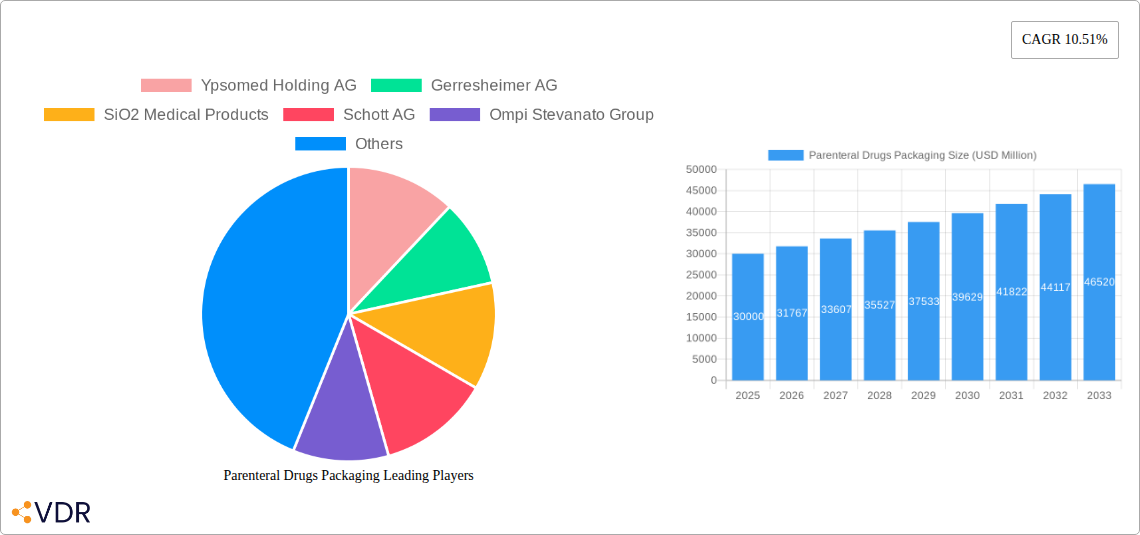

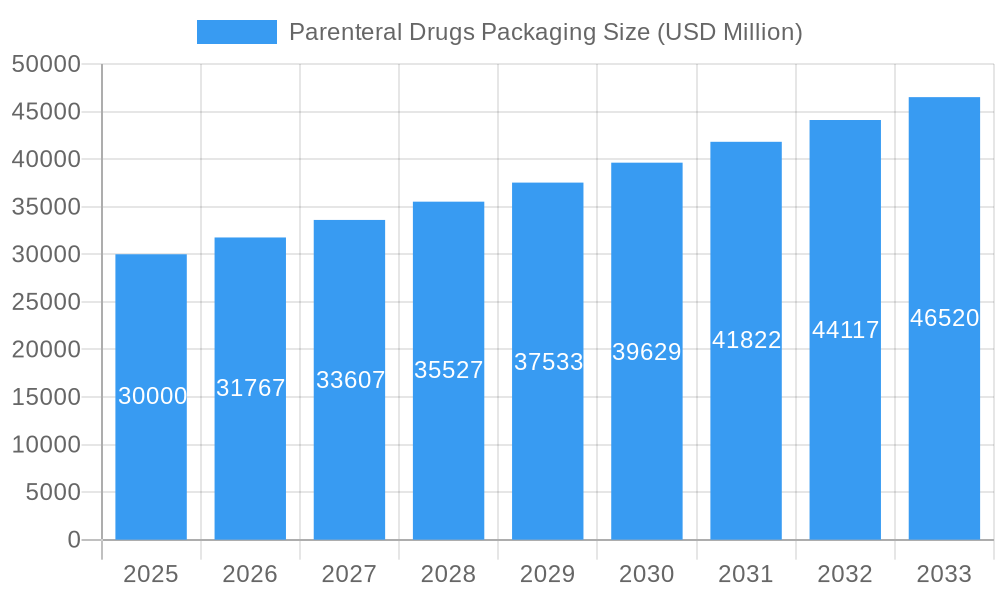

The global Parenteral Drugs Packaging market is poised for significant growth, projected to reach an estimated $30 billion in 2025, with a robust Compound Annual Growth Rate (CAGR) of 5.89% during the forecast period of 2025-2033. This expansion is primarily driven by the increasing prevalence of chronic diseases worldwide, necessitating a greater volume of injectable drug formulations for treatment. The growing demand for biopharmaceuticals, which often require specialized parenteral delivery systems, is also a key catalyst. Furthermore, advancements in drug delivery technologies, leading to the development of novel parenteral formulations and sophisticated packaging solutions, are fueling market expansion. The convenience and efficacy offered by parenteral drug administration for a wide range of therapeutic areas, from oncology to infectious diseases and pain management, continue to underpin its importance in modern healthcare.

Parenteral Drugs Packaging Market Size (In Billion)

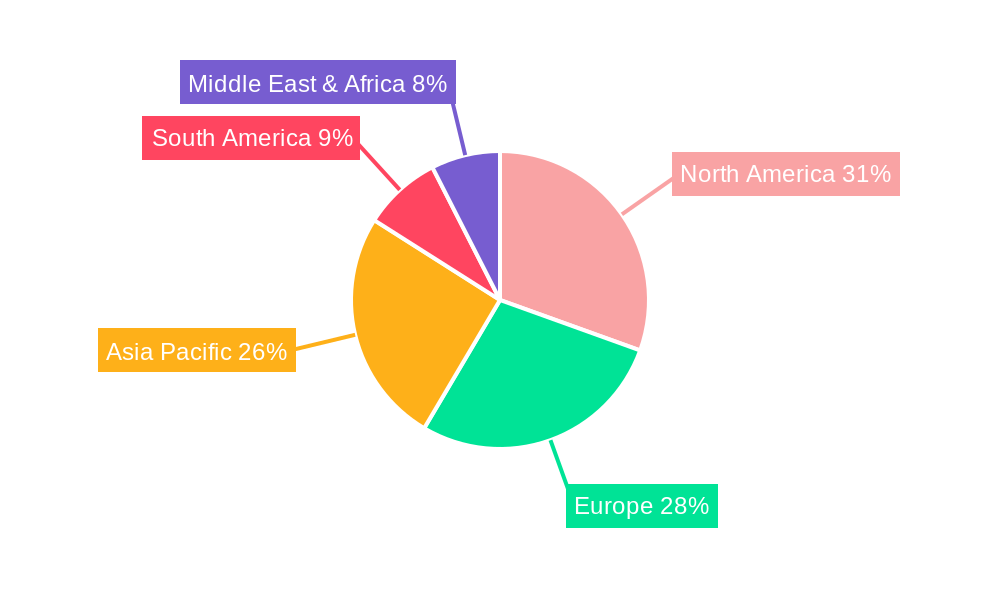

The market is segmented by application into Large Volume Parenteral (LVP) and Small Volume Parenteral (SVP), with both segments exhibiting steady growth. The increasing preference for pre-filled syringes and advanced drug delivery devices is a notable trend, offering enhanced patient compliance and reduced administration errors. In terms of material type, Polyvinyl Chloride (PVC) and Polyolefin containers continue to be dominant, though innovations in advanced materials offering improved barrier properties and enhanced safety are gaining traction. Key market restraints include stringent regulatory requirements for pharmaceutical packaging, which necessitate extensive testing and validation, potentially increasing development timelines and costs. Geographically, North America and Europe are expected to remain dominant markets due to established healthcare infrastructures and high healthcare expenditure. However, the Asia Pacific region is anticipated to witness the fastest growth, driven by a burgeoning population, increasing access to healthcare, and a rising number of pharmaceutical manufacturers. Key players like Ypsomed Holding AG, Gerresheimer AG, and Becton Dickinson and Company are actively investing in research and development to introduce innovative packaging solutions and expand their market reach.

Parenteral Drugs Packaging Company Market Share

Parenteral Drugs Packaging Market Research Report: Future Outlook, Growth Drivers, and Key Players (2019-2033)

This comprehensive report provides an in-depth analysis of the global parenteral drugs packaging market, offering critical insights into its dynamics, growth trajectories, and competitive landscape. Covering the historical period from 2019 to 2024, a base year of 2025, and an extensive forecast period from 2025 to 2033, this report is an indispensable resource for stakeholders seeking to understand and capitalize on the evolving parenteral drug delivery systems market. With a focus on market size evolution, technological innovations, regulatory influences, and emerging opportunities, this report equips industry professionals with actionable intelligence to navigate the complex parenteral drugs packaging industry.

Parenteral Drugs Packaging Market Dynamics & Structure

The parenteral drugs packaging market is characterized by a moderate to high level of concentration, with established players like Schott AG, Ompi Stevanato Group, and West Pharmaceutical Services holding significant market shares. Technological innovation is a primary driver, fueled by the increasing demand for advanced drug delivery systems such as pre-filled syringes and auto-injectors, which require specialized packaging solutions. The stringent regulatory frameworks governing pharmaceutical packaging, including Good Manufacturing Practices (GMP) and specific regional directives, play a crucial role in shaping market entry and product development. Competitive product substitutes, though limited for high-potency or sensitive biologics, primarily revolve around variations in primary packaging materials and container closure systems. End-user demographics, particularly the aging global population and the rising prevalence of chronic diseases, are driving the demand for injectable drug formulations and, consequently, their packaging. Mergers and acquisitions (M&A) trends are evident as key companies seek to expand their product portfolios, geographical reach, and technological capabilities, consolidating the market further. For instance, strategic acquisitions of smaller specialized packaging firms by larger entities are common, aimed at integrating niche technologies and expanding market access.

- Market Concentration: Moderate to High, driven by a few key global manufacturers.

- Technological Innovation: Focus on enhanced drug stability, user-friendliness, and safety in pre-filled syringes and vials.

- Regulatory Frameworks: Strict adherence to global pharmaceutical packaging standards and guidelines is paramount.

- Competitive Product Substitutes: Primarily related to material science advancements and secondary packaging innovations.

- End-User Demographics: Growing demand for self-administration of medications due to aging populations and chronic disease prevalence.

- M&A Trends: Companies are actively acquiring smaller players to gain technological advantages and market share, with an estimated XX billion units in deal values over the historical period.

Parenteral Drugs Packaging Growth Trends & Insights

The global parenteral drugs packaging market is poised for robust growth, driven by a confluence of factors including increasing healthcare expenditure, the expanding pipeline of biologic drugs, and the growing preference for minimally invasive drug administration methods. The market size evolution is projected to witness a significant upward trajectory throughout the forecast period. Adoption rates of advanced parenteral packaging solutions, such as pre-filled syringes and vials with specialized coatings, are accelerating as pharmaceutical manufacturers prioritize drug stability, patient safety, and convenience. Technological disruptions, including advancements in material science for enhanced barrier properties, tamper-evident features, and integrated drug-delivery functionalities, are transforming the packaging landscape. Consumer behavior shifts, influenced by a greater emphasis on self-care and home-based healthcare, are further bolstering the demand for user-friendly and pre-filled parenteral drug packaging.

The market is experiencing a significant CAGR, projected to be around XX%, from the historical period (2019-2024) to the forecast period (2025-2033). The increasing prevalence of chronic diseases like diabetes, cancer, and autoimmune disorders necessitates frequent parenteral administration of medications, directly impacting the demand for vials, syringes, and other parenteral drug packaging. Furthermore, the rise of biologics and biosimilars, which are often administered via injection, further fuels market expansion. The development of novel drug formulations requiring specific storage conditions, such as temperature-sensitive biologics, is spurring innovation in specialized parenteral packaging, including those with advanced insulation and monitoring capabilities. The shift towards personalized medicine also plays a role, with smaller, individualized doses requiring sophisticated and reliable packaging. The penetration of advanced parenteral packaging solutions, such as advanced vials with stoppers offering enhanced sterility and reduced extractables, is expected to grow substantially.

The global parenteral drugs packaging market size is estimated to reach approximately $XX billion in 2025, growing to an estimated $XX billion by 2033, exhibiting a compound annual growth rate (CAGR) of XX% during the forecast period. This growth is underpinned by the increasing global demand for pharmaceuticals and a heightened focus on drug safety and efficacy. The expansion of the biopharmaceutical sector, with its emphasis on injectable biologics and complex therapeutic proteins, is a primary growth accelerator. Moreover, the aging global population and the associated increase in chronic conditions requiring parenteral drug treatment are significant demand drivers. The market is also witnessing a surge in demand for specialized packaging solutions that ensure drug sterility, prevent contamination, and enhance patient compliance, particularly in the context of self-administered therapies. The development and adoption of advanced materials and manufacturing technologies are further shaping the market, offering improved functionality and sustainability.

- Market Size Evolution: Significant projected growth driven by healthcare advancements and disease prevalence.

- Adoption Rates: Increasing adoption of pre-filled syringes, auto-injectors, and advanced vial closures.

- Technological Disruptions: Innovations in material science, barrier properties, and smart packaging.

- Consumer Behavior Shifts: Growing preference for self-administration and convenience in drug delivery.

- CAGR: Estimated at XX% from 2019-2033.

- Market Penetration: Rising penetration of advanced and specialized parenteral packaging solutions.

Dominant Regions, Countries, or Segments in Parenteral Drugs Packaging

The global parenteral drugs packaging market is segmented by application into Large Volume Parenteral (LVP) and Small Volume Parenteral (SVP), and by type into Polyvinyl Chloride (PVC), Polyolefin, and other materials. Within these segments, North America and Europe currently dominate the market, driven by their well-established pharmaceutical industries, high healthcare expenditure, and robust research and development activities. The United States, in particular, stands out as a leading country due to its significant pharmaceutical production and consumption, coupled with a strong regulatory environment that encourages the adoption of advanced packaging solutions. The dominance of Small Volume Parenteral (SVP) packaging is notable, as this segment encompasses a vast array of injectable drugs for chronic diseases, vaccines, and biopharmaceuticals, all requiring precise and sterile packaging.

The growth in the SVP segment is further propelled by the increasing demand for pre-filled syringes and auto-injectors, which offer enhanced patient convenience and reduced risk of medication errors. Polyolefin-based packaging materials are gaining traction due to their superior chemical resistance, flexibility, and recyclability compared to traditional PVC, especially for sensitive biologic drugs. Key drivers for regional dominance include supportive government policies promoting pharmaceutical manufacturing and innovation, advanced healthcare infrastructure, and a high prevalence of target diseases. The economic policies in these regions often incentivize pharmaceutical companies to invest in cutting-edge packaging technologies to ensure drug safety and compliance. The market share for SVP applications is estimated to be approximately XX% of the total parenteral drugs packaging market.

Asia Pacific is emerging as a rapidly growing region, fueled by increasing investments in healthcare infrastructure, a growing generic drug market, and rising disposable incomes, which translate to greater access to healthcare services. Countries like China and India are becoming significant manufacturing hubs for both pharmaceuticals and their packaging. The Type segment, particularly Polyolefin, is witnessing substantial growth owing to its favorable properties for sensitive drug formulations and increasing environmental consciousness, leading to a phase-out of certain PVC applications in some regions. The market share for Polyolefin in parenteral drugs packaging is estimated to be XX% of the total market. The increasing clinical trials and approvals of new biologic drugs are directly contributing to the expansion of the SVP segment.

- Dominant Region: North America and Europe, with the United States as a leading country.

- Dominant Segment (Application): Small Volume Parenteral (SVP) due to its widespread use in chronic disease management and biopharmaceuticals.

- Dominant Segment (Type): While Polyvinyl Chloride (PVC) has historically been significant, Polyolefin is gaining substantial market share due to its advantages.

- Key Drivers: High healthcare expenditure, robust pharmaceutical R&D, supportive regulatory frameworks, and growing prevalence of chronic diseases.

- Emerging Region: Asia Pacific, driven by increasing healthcare investments and a growing pharmaceutical market.

- SVP Market Share: Approximately XX% of the total parenteral drugs packaging market.

- Polyolefin Market Share: Approximately XX% of the total parenteral drugs packaging market.

Parenteral Drugs Packaging Product Landscape

The parenteral drugs packaging product landscape is characterized by a diverse array of solutions designed to ensure the sterility, stability, and efficacy of injectable medications. This includes a wide range of primary packaging components such as glass vials and stoppers, plastic syringes and containers, and specialized delivery devices like pre-filled syringes and auto-injectors. Innovations focus on enhanced barrier properties to protect sensitive drug formulations from moisture, oxygen, and light, thereby extending shelf life. Advanced surface treatments for glass vials and stoppers are crucial for minimizing extractables and leachables, particularly for biologics. The development of tamper-evident features and child-resistant mechanisms enhances product security and patient safety. Unique selling propositions often lie in customized solutions catering to specific drug characteristics and dosage requirements, as well as sustainable packaging materials and designs. Technological advancements are driving the integration of smart features, such as temperature indicators and RFID tags, for improved supply chain traceability and patient monitoring.

Key Drivers, Barriers & Challenges in Parenteral Drugs Packaging

Key Drivers: The primary forces propelling the parenteral drugs packaging market include the escalating demand for biopharmaceuticals and complex injectable drugs, the growing prevalence of chronic diseases necessitating regular parenteral treatment, and the increasing adoption of patient-centric drug delivery devices like pre-filled syringes and auto-injectors. Technological advancements in material science and manufacturing processes, coupled with supportive regulatory policies that prioritize drug safety and efficacy, also act as significant growth catalysts. The expanding global healthcare infrastructure and rising disposable incomes in emerging economies further contribute to market expansion.

Barriers & Challenges: Significant challenges facing the market include the stringent and evolving regulatory landscape, which can lead to extended approval timelines and increased development costs. Supply chain complexities, particularly for temperature-sensitive products, and the risk of counterfeiting require robust packaging solutions and logistical management. High development and manufacturing costs for specialized packaging, especially for novel biologics, can be a barrier for smaller companies. Furthermore, concerns regarding the environmental impact of certain packaging materials and the need for sustainable alternatives are growing. Competitive pressures from established players and the threat of alternative drug delivery methods also pose challenges. The cost of raw materials, such as high-quality glass and specialized polymers, can also impact profit margins.

Emerging Opportunities in Parenteral Drugs Packaging

Emerging opportunities in the parenteral drugs packaging market are primarily centered around the burgeoning field of biologics and biosimilars, which require highly specialized and inert packaging. The growth of personalized medicine and cell and gene therapies presents a demand for novel, low-volume, and high-value packaging solutions. Advancements in nanotechnology for enhanced barrier properties and drug delivery systems offer significant potential. The increasing focus on sustainability is driving the demand for eco-friendly and recyclable packaging materials, creating opportunities for innovation in this area. Furthermore, the expansion of telehealth and home healthcare services is accelerating the need for user-friendly, pre-filled parenteral drug packaging with enhanced safety features. Digitalization and the integration of smart packaging technologies for supply chain traceability and patient adherence also represent a substantial growth avenue.

Growth Accelerators in the Parenteral Drugs Packaging Industry

Several key factors are acting as growth accelerators for the parenteral drugs packaging industry. The rapid innovation in pharmaceutical R&D, leading to a continuous pipeline of novel biologic drugs and vaccines, directly fuels the demand for advanced parenteral packaging. Strategic partnerships and collaborations between pharmaceutical companies and packaging manufacturers are crucial for developing tailored solutions and accelerating time-to-market. Market expansion strategies targeting emerging economies, where healthcare access and demand are rapidly increasing, are also significant growth drivers. Technological breakthroughs in areas such as advanced materials, sterile filling technologies, and tamper-evident sealing are enabling the development of safer and more effective packaging. The increasing outsourcing of packaging operations by pharmaceutical companies to specialized contract manufacturing organizations (CMOs) also contributes to industry growth by leveraging expertise and economies of scale.

Key Players Shaping the Parenteral Drugs Packaging Market

- Ypsomed Holding AG

- Gerresheimer AG

- SiO2 Medical Products

- Schott AG

- Ompi Stevanato Group

- Becton Dickinson and Company

- MeadWestvaco Corporation (now part of WestRock)

- Unilife Corporation Inc (acquired by Spectrum Pharmaceuticals)

- West Pharmaceutical Services

- Terumo Corporation

- Berry Plastics Corporation (now part of Berry Global)

- Owens-Illinois

- RPC Group (now part of Berry Global)

- Graphic Packaging Group

Notable Milestones in Parenteral Drugs Packaging Sector

- 2019: Increased regulatory scrutiny on extractables and leachables from primary packaging, driving demand for advanced glass and polymer solutions.

- 2020: Accelerated demand for vial and syringe packaging due to the global COVID-19 pandemic and the rapid development of vaccines.

- 2021: Significant investment in advanced manufacturing capabilities for pre-filled syringes and auto-injectors to meet growing demand for biologics.

- 2022: Growing emphasis on sustainable packaging solutions, with increased adoption of recycled content and innovative material designs.

- 2023: Expansion of pre-filled syringe capacity by key manufacturers to address supply chain challenges for critical medications.

- 2024: Further development of smart packaging technologies for enhanced drug traceability and patient adherence.

In-Depth Parenteral Drugs Packaging Market Outlook

The future outlook for the parenteral drugs packaging market is exceptionally promising, driven by sustained innovation and escalating demand from the biopharmaceutical sector. Growth accelerators such as the increasing prevalence of chronic diseases, the development of novel biologic therapies, and the expanding global healthcare market will continue to fuel expansion. Strategic collaborations between pharmaceutical and packaging leaders will be instrumental in bringing advanced, patient-centric solutions to market. Emerging opportunities in personalized medicine and cell and gene therapy packaging, alongside the growing imperative for sustainable packaging, represent significant avenues for future growth. The market is poised for substantial value creation as companies invest in cutting-edge technologies to ensure drug integrity, patient safety, and supply chain reliability.

Parenteral Drugs Packaging Segmentation

-

1. Application

- 1.1. Large Volume Parenteral (LVP)

- 1.2. Small Volume Parenteral (SVP)

-

2. Type

- 2.1. Polyvinyl Chloride (PVC)

- 2.2. Polyolefin

Parenteral Drugs Packaging Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Parenteral Drugs Packaging Regional Market Share

Geographic Coverage of Parenteral Drugs Packaging

Parenteral Drugs Packaging REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.63% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Large Volume Parenteral (LVP)

- 5.1.2. Small Volume Parenteral (SVP)

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Polyvinyl Chloride (PVC)

- 5.2.2. Polyolefin

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Parenteral Drugs Packaging Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Large Volume Parenteral (LVP)

- 6.1.2. Small Volume Parenteral (SVP)

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Polyvinyl Chloride (PVC)

- 6.2.2. Polyolefin

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Parenteral Drugs Packaging Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Large Volume Parenteral (LVP)

- 7.1.2. Small Volume Parenteral (SVP)

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Polyvinyl Chloride (PVC)

- 7.2.2. Polyolefin

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Parenteral Drugs Packaging Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Large Volume Parenteral (LVP)

- 8.1.2. Small Volume Parenteral (SVP)

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Polyvinyl Chloride (PVC)

- 8.2.2. Polyolefin

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Parenteral Drugs Packaging Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Large Volume Parenteral (LVP)

- 9.1.2. Small Volume Parenteral (SVP)

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Polyvinyl Chloride (PVC)

- 9.2.2. Polyolefin

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Parenteral Drugs Packaging Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Large Volume Parenteral (LVP)

- 10.1.2. Small Volume Parenteral (SVP)

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Polyvinyl Chloride (PVC)

- 10.2.2. Polyolefin

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Parenteral Drugs Packaging Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Large Volume Parenteral (LVP)

- 11.1.2. Small Volume Parenteral (SVP)

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. Polyvinyl Chloride (PVC)

- 11.2.2. Polyolefin

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Ypsomed Holding AG

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Gerresheimer AG

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 SiO2 Medical Products

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Schott AG

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Ompi Stevanato Group

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Becton Dickinson and Company

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 MeadWestvaco Corporation

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Unilife Corporation Inc

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 West Pharmaceutical Services

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Terumo Corporation

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Berry Plastics Corporation

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Owens-Illinois

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 RPC Group

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Graphic Packaging Group

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.1 Ypsomed Holding AG

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Parenteral Drugs Packaging Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Parenteral Drugs Packaging Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Parenteral Drugs Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Parenteral Drugs Packaging Revenue (billion), by Type 2025 & 2033

- Figure 5: North America Parenteral Drugs Packaging Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Parenteral Drugs Packaging Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Parenteral Drugs Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Parenteral Drugs Packaging Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Parenteral Drugs Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Parenteral Drugs Packaging Revenue (billion), by Type 2025 & 2033

- Figure 11: South America Parenteral Drugs Packaging Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Parenteral Drugs Packaging Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Parenteral Drugs Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Parenteral Drugs Packaging Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Parenteral Drugs Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Parenteral Drugs Packaging Revenue (billion), by Type 2025 & 2033

- Figure 17: Europe Parenteral Drugs Packaging Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Parenteral Drugs Packaging Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Parenteral Drugs Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Parenteral Drugs Packaging Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Parenteral Drugs Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Parenteral Drugs Packaging Revenue (billion), by Type 2025 & 2033

- Figure 23: Middle East & Africa Parenteral Drugs Packaging Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Parenteral Drugs Packaging Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Parenteral Drugs Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Parenteral Drugs Packaging Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Parenteral Drugs Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Parenteral Drugs Packaging Revenue (billion), by Type 2025 & 2033

- Figure 29: Asia Pacific Parenteral Drugs Packaging Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Parenteral Drugs Packaging Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Parenteral Drugs Packaging Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Parenteral Drugs Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Parenteral Drugs Packaging Revenue billion Forecast, by Type 2020 & 2033

- Table 3: Global Parenteral Drugs Packaging Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Parenteral Drugs Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Parenteral Drugs Packaging Revenue billion Forecast, by Type 2020 & 2033

- Table 6: Global Parenteral Drugs Packaging Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Parenteral Drugs Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Parenteral Drugs Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Parenteral Drugs Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Parenteral Drugs Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Parenteral Drugs Packaging Revenue billion Forecast, by Type 2020 & 2033

- Table 12: Global Parenteral Drugs Packaging Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Parenteral Drugs Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Parenteral Drugs Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Parenteral Drugs Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Parenteral Drugs Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Parenteral Drugs Packaging Revenue billion Forecast, by Type 2020 & 2033

- Table 18: Global Parenteral Drugs Packaging Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Parenteral Drugs Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Parenteral Drugs Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Parenteral Drugs Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Parenteral Drugs Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Parenteral Drugs Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Parenteral Drugs Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Parenteral Drugs Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Parenteral Drugs Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Parenteral Drugs Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Parenteral Drugs Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Parenteral Drugs Packaging Revenue billion Forecast, by Type 2020 & 2033

- Table 30: Global Parenteral Drugs Packaging Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Parenteral Drugs Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Parenteral Drugs Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Parenteral Drugs Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Parenteral Drugs Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Parenteral Drugs Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Parenteral Drugs Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Parenteral Drugs Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Parenteral Drugs Packaging Revenue billion Forecast, by Type 2020 & 2033

- Table 39: Global Parenteral Drugs Packaging Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Parenteral Drugs Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Parenteral Drugs Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Parenteral Drugs Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Parenteral Drugs Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Parenteral Drugs Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Parenteral Drugs Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Parenteral Drugs Packaging Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Parenteral Drugs Packaging?

The projected CAGR is approximately 4.63%.

2. Which companies are prominent players in the Parenteral Drugs Packaging?

Key companies in the market include Ypsomed Holding AG, Gerresheimer AG, SiO2 Medical Products, Schott AG, Ompi Stevanato Group, Becton Dickinson and Company, MeadWestvaco Corporation, Unilife Corporation Inc, West Pharmaceutical Services, Terumo Corporation, Berry Plastics Corporation, Owens-Illinois, RPC Group, Graphic Packaging Group.

3. What are the main segments of the Parenteral Drugs Packaging?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 13.39 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Parenteral Drugs Packaging," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Parenteral Drugs Packaging report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Parenteral Drugs Packaging?

To stay informed about further developments, trends, and reports in the Parenteral Drugs Packaging, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence