Key Insights

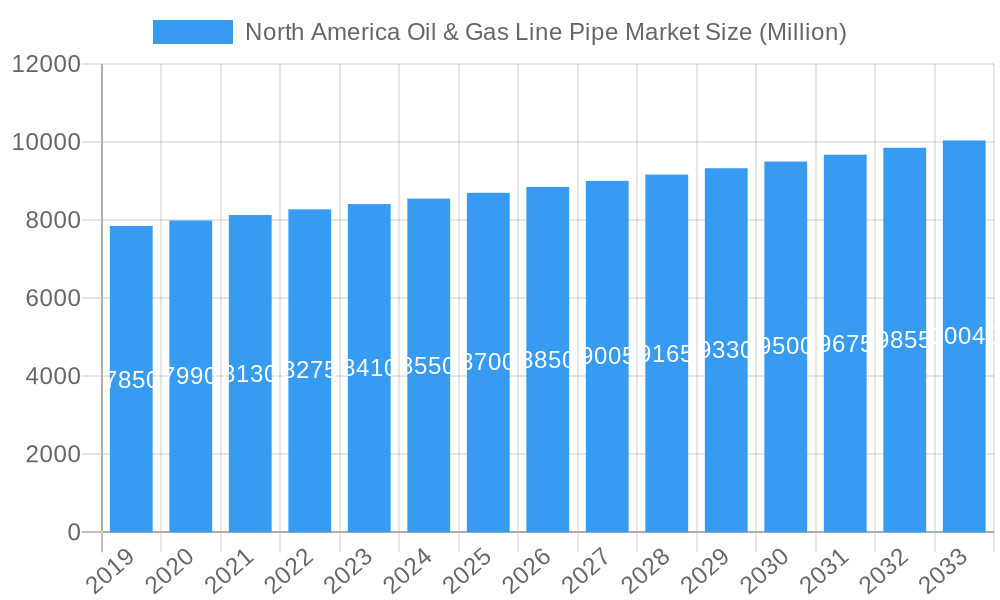

The North America Oil & Gas Line Pipe Market is poised for significant growth, projected to expand at a CAGR of 7.2%. The market, currently valued at $68.2 billion as of the base year 2025, is driven by robust demand for energy infrastructure development and the modernization of existing pipeline networks across the United States and Canada. Investments in new transportation routes for both conventional and unconventional resources, coupled with advancements in materials and manufacturing technologies, are key growth catalysts.

North America Oil & Gas Line Pipe Market Market Size (In Billion)

The market comprises key segments including Seamless and Welded pipes. Within the Welded category, LSAW, HSAW, and ERW pipes serve diverse applications from large-diameter transmission to smaller distribution networks. Challenges include stringent regulations, environmental concerns, and oil price volatility impacting capital expenditure. However, technological innovations in coatings, corrosion resistance, and leak detection are mitigating these factors. The competitive landscape features leading global players like Vallourec S.A., Tenaris S.A., and Nippon Steel & Sumitomo Metal Corporation, engaged in strategic initiatives to enhance market presence.

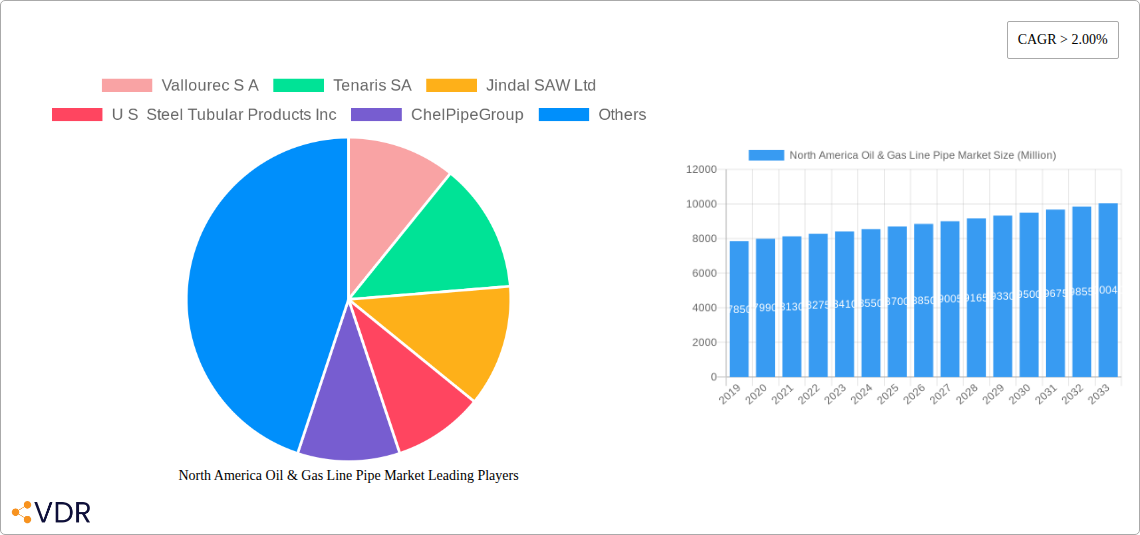

North America Oil & Gas Line Pipe Market Company Market Share

This report provides a comprehensive analysis of the North America Oil & Gas Line Pipe Market, covering market size, share, growth, trends, and forecasts from 2019 to 2033. With a base year of 2025, it offers critical insights into market dynamics, technological advancements, regulatory influences, and competitive strategies. All market size values are presented in billion units.

North America Oil & Gas Line Pipe Market Market Dynamics & Structure

The North America Oil & Gas Line Pipe Market is characterized by a moderate market concentration, with key players vying for dominance through continuous technological innovation and strategic expansion. Significant drivers include the persistent demand for energy infrastructure upgrades and new project developments across the United States, Canada, and the Rest of North America. Regulatory frameworks, particularly those pertaining to environmental safety and pipeline integrity, play a crucial role in shaping market access and product specifications. While competitive product substitutes exist, the specialized nature of line pipes for oil and gas applications limits their widespread adoption. End-user demographics are primarily dominated by major oil and gas exploration and production companies, as well as midstream operators. Mergers and Acquisitions (M&A) activity, though not intensely concentrated, continues to consolidate market share and enhance operational efficiencies.

- Market Concentration: Moderate, with a few key players holding significant market share.

- Technological Innovation Drivers: Advancements in material science for enhanced corrosion resistance, increased pressure handling, and extended lifespan of pipes.

- Regulatory Frameworks: Stringent safety and environmental regulations influence manufacturing processes and material selection.

- Competitive Product Substitutes: Limited, due to specialized requirements of oil and gas transportation.

- End-User Demographics: Dominated by E&P companies and midstream operators.

- M&A Trends: Strategic acquisitions aimed at expanding product portfolios and geographical reach.

North America Oil & Gas Line Pipe Market Growth Trends & Insights

The North America Oil & Gas Line Pipe Market is poised for robust growth, driven by an increasing need for secure and efficient energy transportation. The market size evolution is directly correlated with upstream and midstream project investments, particularly in shale gas production areas. Adoption rates of advanced pipe materials and manufacturing techniques are steadily rising, responding to demands for greater durability and reduced environmental impact. Technological disruptions, such as the development of smart pipelines with integrated monitoring systems, are set to redefine operational standards and safety protocols. Consumer behavior shifts, influenced by energy security concerns and the drive towards cleaner energy sources, are indirectly impacting the demand for line pipes as the industry adapts. The market is projected to witness a Compound Annual Growth Rate (CAGR) of approximately X.XX% during the forecast period. Market penetration is expected to deepen as infrastructure projects in remote and challenging terrains gain momentum.

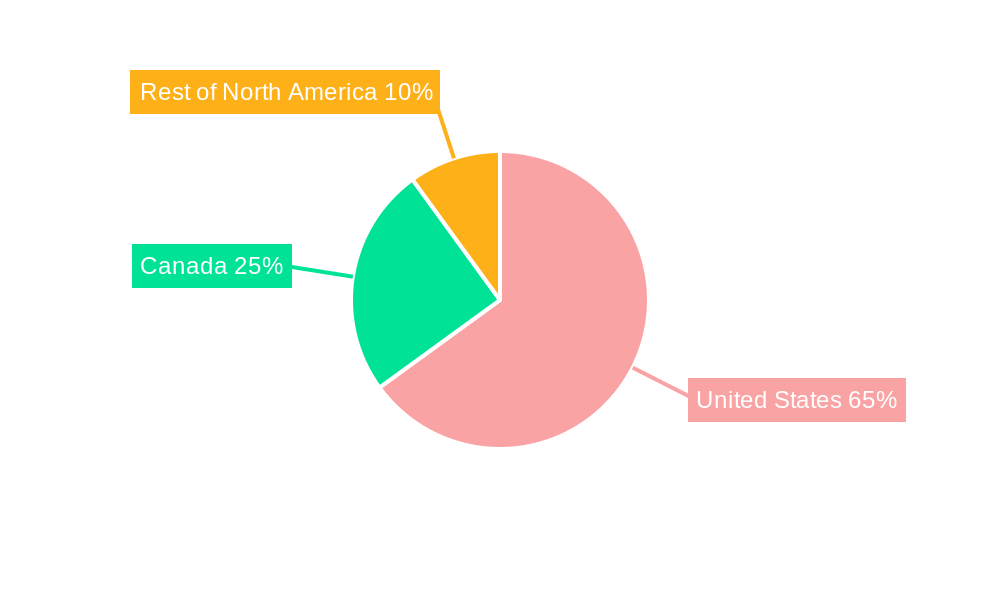

Dominant Regions, Countries, or Segments in North America Oil & Gas Line Pipe Market

The United States stands as the dominant region in the North America Oil & Gas Line Pipe Market, fueled by its extensive oil and gas reserves, significant refining capacity, and continuous investments in pipeline infrastructure for both domestic consumption and exports. Economic policies encouraging energy independence and the development of shale plays have consistently propelled demand for various types of line pipes. The sheer scale of its existing and planned pipeline network, coupled with ongoing maintenance and upgrades, solidifies its leading position.

- Dominant Country: United States

- Key Drivers for US Dominance:

- Extensive shale gas and oil production.

- Significant investments in new pipeline construction and maintenance.

- Supportive government policies for energy infrastructure development.

- Large existing network requiring continuous upgrades and replacements.

- Market Share: The United States accounts for approximately XX% of the total North American market share.

- Growth Potential: High, driven by ongoing energy transition projects and the need for modernized infrastructure.

Within the Type segment, Welded pipes, particularly Large Diameter Spiral Welded (LSAW) and Helical Submerged Arc Welded (HSAW) pipes, are expected to lead market growth. These types are favored for their cost-effectiveness and suitability for large-scale pipeline projects.

- Dominant Segment (Type): Welded Pipes

- Sub-segments: LSAW, HSAW, ERW

- Drivers for Welded Pipe Dominance:

- Cost-effectiveness for large-diameter applications.

- High production volumes and availability.

- Suitability for long-distance oil and gas transportation.

- Growth Potential within Welded Pipes: LSAW and HSAW segments are projected to exhibit higher growth rates due to large-scale infrastructure needs.

North America Oil & Gas Line Pipe Market Product Landscape

The product landscape for North America Oil & Gas Line Pipe is characterized by continuous innovation aimed at enhancing performance, durability, and safety. Key product innovations include advanced steel alloys offering superior corrosion and abrasion resistance, facilitating operations in harsher environments and extending pipe lifespan. Unique selling propositions revolve around specialized coatings for increased protection against internal and external degradation, and advancements in manufacturing processes to meet stringent API specifications. Technological advancements are focused on developing lighter yet stronger pipes, reducing transportation costs and installation complexities. Applications span the entire oil and gas value chain, from upstream exploration and production to midstream transportation and downstream distribution.

Key Drivers, Barriers & Challenges in North America Oil & Gas Line Pipe Market

Key Drivers:

- Growing Energy Demand: Continued global and regional demand for oil and natural gas necessitates robust transportation infrastructure.

- Infrastructure Development & Modernization: Extensive investments in new pipeline construction, expansion, and upgrades of aging systems are paramount.

- Technological Advancements: Innovations in materials and manufacturing processes enhance pipe performance and lifespan.

- Supportive Government Policies: Initiatives promoting energy independence and infrastructure development.

Key Barriers & Challenges:

- Regulatory Hurdles & Environmental Concerns: Stringent environmental regulations and public opposition to new pipeline projects can cause delays and increase costs.

- Supply Chain Volatility: Fluctuations in raw material prices (e.g., steel) and availability can impact production costs and timelines.

- Geopolitical Instability: Global geopolitical events can affect energy markets and investment decisions.

- Intense Competition: A competitive market landscape can lead to price pressures and challenges in maintaining profitability.

Emerging Opportunities in North America Oil & Gas Line Pipe Market

Emerging opportunities lie in the development and deployment of "smart" pipelines equipped with advanced sensor technologies for real-time monitoring, leak detection, and predictive maintenance. The growing focus on carbon capture, utilization, and storage (CCUS) projects presents a new avenue for specialized line pipe applications. Furthermore, the demand for line pipes in liquefied natural gas (LNG) terminals and associated infrastructure is expected to rise. Untapped markets within regions undergoing significant energy infrastructure expansion, coupled with evolving consumer preferences for more sustainable and secure energy supply chains, offer substantial growth potential.

Growth Accelerators in the North America Oil & Gas Line Pipe Market Industry

Long-term growth in the North America Oil & Gas Line Pipe Market will be significantly accelerated by breakthroughs in material science, leading to lighter, stronger, and more corrosion-resistant pipes. Strategic partnerships between pipe manufacturers, energy companies, and technology providers will foster collaborative innovation and streamline project execution. Market expansion strategies targeting underdeveloped regions with high energy potential and the increasing adoption of modular pipeline construction techniques will also act as crucial growth accelerators, driving efficiency and reducing project lead times.

Key Players Shaping the North America Oil & Gas Line Pipe Market Market

- Vallourec S A

- Tenaris SA

- Jindal SAW Ltd

- U S Steel Tubular Products Inc

- ChelPipe Group

- ArcelorMittal S A

- Nippon Steel & Sumitomo Metal Corporation

- ILJIN Steel Co

- Welspun Group

- JFE Steel Corporation

- EVRAZ plc

- PSL Limited

Notable Milestones in North America Oil & Gas Line Pipe Market Sector

- 2023 (Ongoing): Increased investment in carbon capture pipeline projects across the US, driving demand for specialized high-pressure line pipes.

- 2023 (Q4): Launch of advanced high-strength low-alloy (HSLA) steel pipes by key manufacturers, offering enhanced durability and weight reduction.

- 2022 (H2): Significant M&A activity, with major players consolidating to enhance production capacity and market reach.

- 2021: Implementation of new stringent API standards for pipeline integrity and safety, influencing manufacturing processes.

- 2020: Increased focus on digitalization and IoT integration in pipeline monitoring, impacting demand for associated infrastructure.

- 2019: Continued expansion of shale gas production in North America, leading to sustained demand for LSAW and HSAW pipes.

In-Depth North America Oil & Gas Line Pipe Market Market Outlook

The outlook for the North America Oil & Gas Line Pipe Market remains highly positive, driven by a confluence of sustained energy demand, critical infrastructure development, and continuous technological innovation. Growth accelerators such as the increasing adoption of smart pipeline technologies and the expansion into nascent areas like CCUS infrastructure will define the future market landscape. Strategic partnerships and advancements in material science are expected to further enhance efficiency and sustainability, solidifying the market's resilience and long-term growth potential. The industry is well-positioned to capitalize on evolving energy needs and environmental considerations, ensuring continued demand for high-quality line pipe solutions.

North America Oil & Gas Line Pipe Market Segmentation

-

1. Type

- 1.1. Seamless

-

1.2. Welded

- 1.2.1. LSAW

- 1.2.2. HSAW

- 1.2.3. ERW

-

2. Geography

- 2.1. United States

- 2.2. Canada

- 2.3. Rest of North America

North America Oil & Gas Line Pipe Market Segmentation By Geography

- 1. United States

- 2. Canada

- 3. Rest of North America

North America Oil & Gas Line Pipe Market Regional Market Share

Geographic Coverage of North America Oil & Gas Line Pipe Market

North America Oil & Gas Line Pipe Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Seamless

- 5.1.2. Welded

- 5.1.2.1. LSAW

- 5.1.2.2. HSAW

- 5.1.2.3. ERW

- 5.2. Market Analysis, Insights and Forecast - by Geography

- 5.2.1. United States

- 5.2.2. Canada

- 5.2.3. Rest of North America

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. United States

- 5.3.2. Canada

- 5.3.3. Rest of North America

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. North America Oil & Gas Line Pipe Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Seamless

- 6.1.2. Welded

- 6.1.2.1. LSAW

- 6.1.2.2. HSAW

- 6.1.2.3. ERW

- 6.2. Market Analysis, Insights and Forecast - by Geography

- 6.2.1. United States

- 6.2.2. Canada

- 6.2.3. Rest of North America

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. United States North America Oil & Gas Line Pipe Market Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Seamless

- 7.1.2. Welded

- 7.1.2.1. LSAW

- 7.1.2.2. HSAW

- 7.1.2.3. ERW

- 7.2. Market Analysis, Insights and Forecast - by Geography

- 7.2.1. United States

- 7.2.2. Canada

- 7.2.3. Rest of North America

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Canada North America Oil & Gas Line Pipe Market Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Seamless

- 8.1.2. Welded

- 8.1.2.1. LSAW

- 8.1.2.2. HSAW

- 8.1.2.3. ERW

- 8.2. Market Analysis, Insights and Forecast - by Geography

- 8.2.1. United States

- 8.2.2. Canada

- 8.2.3. Rest of North America

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Rest of North America North America Oil & Gas Line Pipe Market Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Seamless

- 9.1.2. Welded

- 9.1.2.1. LSAW

- 9.1.2.2. HSAW

- 9.1.2.3. ERW

- 9.2. Market Analysis, Insights and Forecast - by Geography

- 9.2.1. United States

- 9.2.2. Canada

- 9.2.3. Rest of North America

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Competitive Analysis

- 10.1. Company Profiles

- 10.1.1 Vallourec S A

- 10.1.1.1. Company Overview

- 10.1.1.2. Products

- 10.1.1.3. Company Financials

- 10.1.1.4. SWOT Analysis

- 10.1.2 Tenaris SA

- 10.1.2.1. Company Overview

- 10.1.2.2. Products

- 10.1.2.3. Company Financials

- 10.1.2.4. SWOT Analysis

- 10.1.3 Jindal SAW Ltd

- 10.1.3.1. Company Overview

- 10.1.3.2. Products

- 10.1.3.3. Company Financials

- 10.1.3.4. SWOT Analysis

- 10.1.4 U S Steel Tubular Products Inc

- 10.1.4.1. Company Overview

- 10.1.4.2. Products

- 10.1.4.3. Company Financials

- 10.1.4.4. SWOT Analysis

- 10.1.5 ChelPipeGroup

- 10.1.5.1. Company Overview

- 10.1.5.2. Products

- 10.1.5.3. Company Financials

- 10.1.5.4. SWOT Analysis

- 10.1.6 ArcelorMittal S A

- 10.1.6.1. Company Overview

- 10.1.6.2. Products

- 10.1.6.3. Company Financials

- 10.1.6.4. SWOT Analysis

- 10.1.7 Nippon Steel & Sumitomo Metal Corporation

- 10.1.7.1. Company Overview

- 10.1.7.2. Products

- 10.1.7.3. Company Financials

- 10.1.7.4. SWOT Analysis

- 10.1.8 ILJIN Steel Co

- 10.1.8.1. Company Overview

- 10.1.8.2. Products

- 10.1.8.3. Company Financials

- 10.1.8.4. SWOT Analysis

- 10.1.9 Welspun Group

- 10.1.9.1. Company Overview

- 10.1.9.2. Products

- 10.1.9.3. Company Financials

- 10.1.9.4. SWOT Analysis

- 10.1.10 JFE Steel Corporation

- 10.1.10.1. Company Overview

- 10.1.10.2. Products

- 10.1.10.3. Company Financials

- 10.1.10.4. SWOT Analysis

- 10.1.11 EVRAZ plc

- 10.1.11.1. Company Overview

- 10.1.11.2. Products

- 10.1.11.3. Company Financials

- 10.1.11.4. SWOT Analysis

- 10.1.12 PSL Limited

- 10.1.12.1. Company Overview

- 10.1.12.2. Products

- 10.1.12.3. Company Financials

- 10.1.12.4. SWOT Analysis

- 10.1.1 Vallourec S A

- 10.2. Market Entropy

- 10.2.1 Company's Key Areas Served

- 10.2.2 Recent Developments

- 10.3. Company Market Share Analysis 2025

- 10.3.1 Top 5 Companies Market Share Analysis

- 10.3.2 Top 3 Companies Market Share Analysis

- 10.4. List of Potential Customers

- 11. Research Methodology

List of Figures

- Figure 1: North America Oil & Gas Line Pipe Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: North America Oil & Gas Line Pipe Market Share (%) by Company 2025

List of Tables

- Table 1: North America Oil & Gas Line Pipe Market Revenue billion Forecast, by Type 2020 & 2033

- Table 2: North America Oil & Gas Line Pipe Market Volume K Units Forecast, by Type 2020 & 2033

- Table 3: North America Oil & Gas Line Pipe Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 4: North America Oil & Gas Line Pipe Market Volume K Units Forecast, by Geography 2020 & 2033

- Table 5: North America Oil & Gas Line Pipe Market Revenue billion Forecast, by Region 2020 & 2033

- Table 6: North America Oil & Gas Line Pipe Market Volume K Units Forecast, by Region 2020 & 2033

- Table 7: North America Oil & Gas Line Pipe Market Revenue billion Forecast, by Type 2020 & 2033

- Table 8: North America Oil & Gas Line Pipe Market Volume K Units Forecast, by Type 2020 & 2033

- Table 9: North America Oil & Gas Line Pipe Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 10: North America Oil & Gas Line Pipe Market Volume K Units Forecast, by Geography 2020 & 2033

- Table 11: North America Oil & Gas Line Pipe Market Revenue billion Forecast, by Country 2020 & 2033

- Table 12: North America Oil & Gas Line Pipe Market Volume K Units Forecast, by Country 2020 & 2033

- Table 13: North America Oil & Gas Line Pipe Market Revenue billion Forecast, by Type 2020 & 2033

- Table 14: North America Oil & Gas Line Pipe Market Volume K Units Forecast, by Type 2020 & 2033

- Table 15: North America Oil & Gas Line Pipe Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 16: North America Oil & Gas Line Pipe Market Volume K Units Forecast, by Geography 2020 & 2033

- Table 17: North America Oil & Gas Line Pipe Market Revenue billion Forecast, by Country 2020 & 2033

- Table 18: North America Oil & Gas Line Pipe Market Volume K Units Forecast, by Country 2020 & 2033

- Table 19: North America Oil & Gas Line Pipe Market Revenue billion Forecast, by Type 2020 & 2033

- Table 20: North America Oil & Gas Line Pipe Market Volume K Units Forecast, by Type 2020 & 2033

- Table 21: North America Oil & Gas Line Pipe Market Revenue billion Forecast, by Geography 2020 & 2033

- Table 22: North America Oil & Gas Line Pipe Market Volume K Units Forecast, by Geography 2020 & 2033

- Table 23: North America Oil & Gas Line Pipe Market Revenue billion Forecast, by Country 2020 & 2033

- Table 24: North America Oil & Gas Line Pipe Market Volume K Units Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Oil & Gas Line Pipe Market?

The projected CAGR is approximately 7.2%.

2. Which companies are prominent players in the North America Oil & Gas Line Pipe Market?

Key companies in the market include Vallourec S A, Tenaris SA, Jindal SAW Ltd, U S Steel Tubular Products Inc, ChelPipeGroup, ArcelorMittal S A, Nippon Steel & Sumitomo Metal Corporation, ILJIN Steel Co, Welspun Group, JFE Steel Corporation, EVRAZ plc, PSL Limited.

3. What are the main segments of the North America Oil & Gas Line Pipe Market?

The market segments include Type, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 68.2 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Growing Vehicle Ownership4.; Government Initiatives.

6. What are the notable trends driving market growth?

Seamless Type to Witness Significant Demand.

7. Are there any restraints impacting market growth?

4.; Volatile Crude Oil Prices.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K Units.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Oil & Gas Line Pipe Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Oil & Gas Line Pipe Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Oil & Gas Line Pipe Market?

To stay informed about further developments, trends, and reports in the North America Oil & Gas Line Pipe Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence