Key Insights

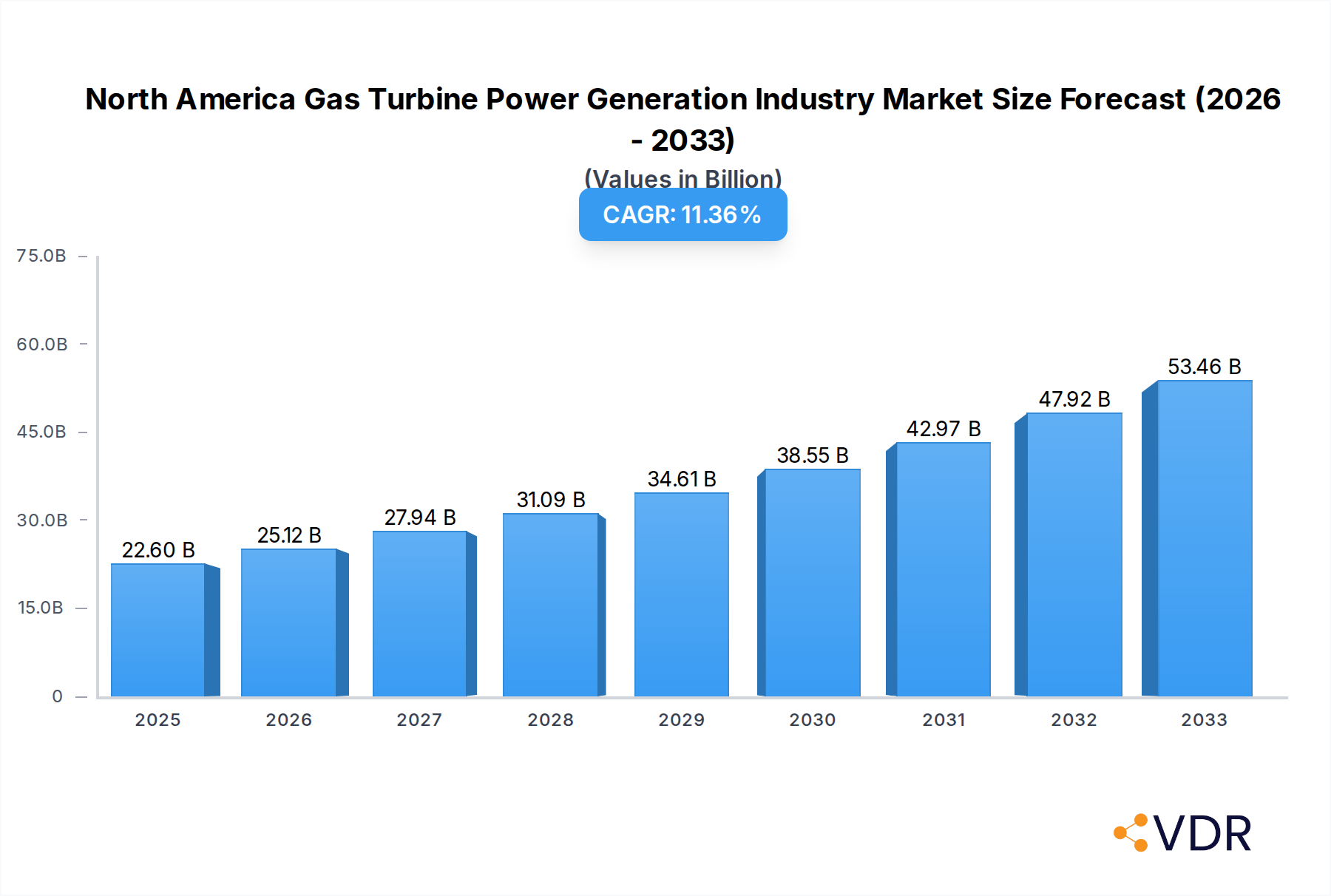

The North America Gas Turbine Power Generation Industry is poised for substantial growth, with a projected market size of USD 22.6 billion in 2025, expanding at a robust Compound Annual Growth Rate (CAGR) of 11.2% through 2033. This dynamic expansion is primarily fueled by the increasing demand for reliable and efficient power generation solutions, driven by the growing energy needs of industrial sectors and the ongoing modernization of existing power infrastructure. Key drivers include the necessity for flexible power plants capable of integrating renewable energy sources, the shift towards cleaner fossil fuel alternatives, and significant investments in upgrading aging power grids. The market is witnessing a strong trend towards the adoption of advanced gas turbine technologies that offer higher efficiency, reduced emissions, and enhanced operational flexibility, particularly for combined cycle power plants. Furthermore, the oil and gas sector's continuous demand for gas turbines in upstream and midstream operations, alongside other industrial applications, contributes significantly to market expansion.

North America Gas Turbine Power Generation Industry Market Size (In Billion)

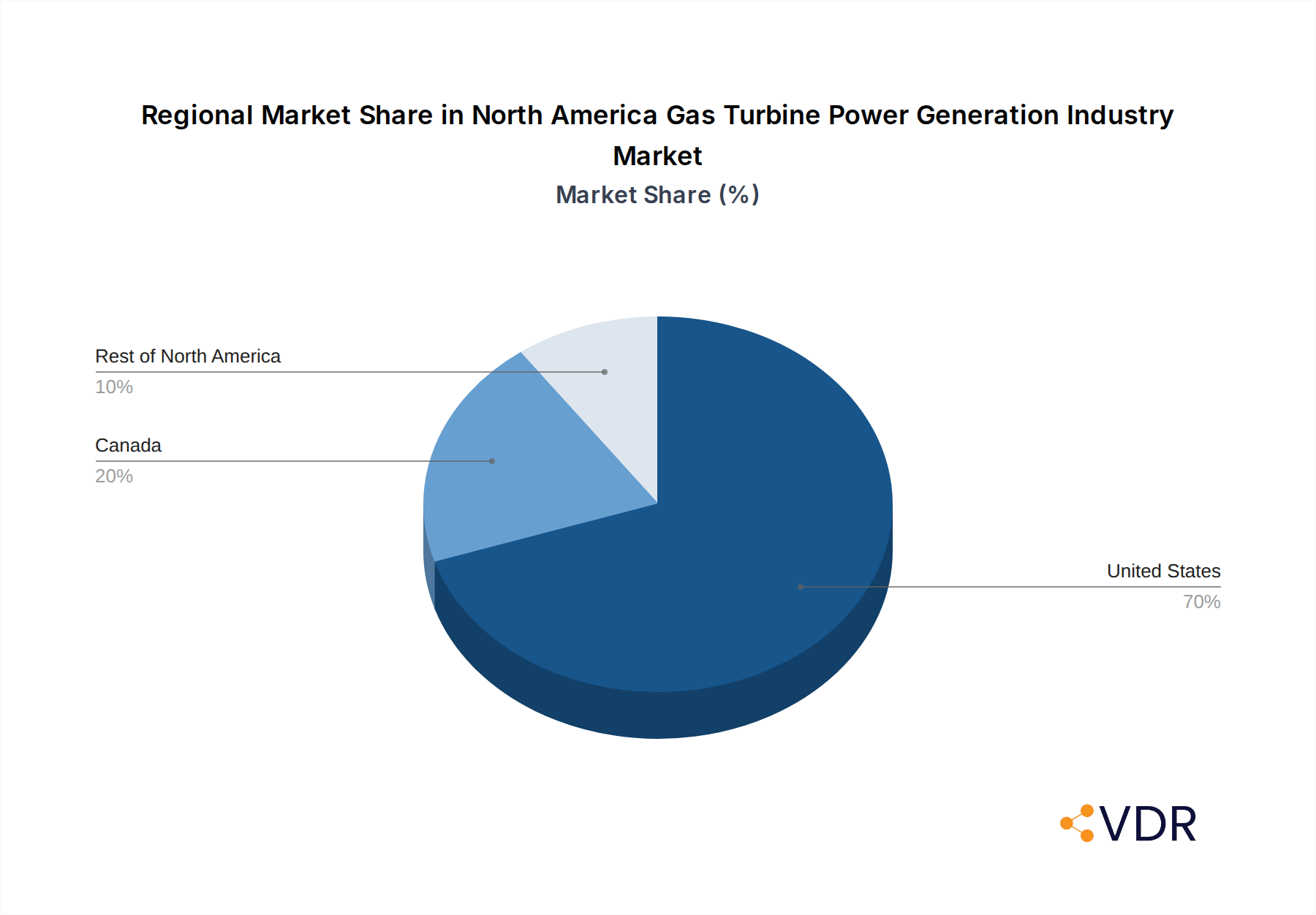

Despite the overwhelmingly positive growth trajectory, certain restraints could influence the market's pace. These may include stringent environmental regulations regarding emissions, the high initial capital investment required for new gas turbine installations, and the fluctuating costs of natural gas, a primary fuel source. However, the industry is actively innovating to address these challenges, with a focus on developing more fuel-efficient turbines and exploring hybrid solutions. The market segmentation reveals a diverse landscape, with capacities ranging from less than 30 MW to above 120 MW, catering to a broad spectrum of power generation needs. Combined cycle turbines are expected to dominate due to their superior efficiency. Geographically, the United States represents the largest market within North America, followed by Canada and the rest of the region, all exhibiting considerable potential for growth. Leading companies such as Siemens AG, General Electric Company, and Solar Turbines Inc. are at the forefront of technological advancements and market penetration.

North America Gas Turbine Power Generation Industry Company Market Share

North America Gas Turbine Power Generation Industry: Market Dynamics, Growth Trends, and Outlook (2019-2033)

This comprehensive report provides an in-depth analysis of the North America Gas Turbine Power Generation Industry, a critical sector for energy infrastructure. Covering the study period of 2019–2033, with a base year of 2025, this report offers unparalleled insights into market dynamics, growth trajectories, competitive landscapes, and future opportunities. Our analysis incorporates high-traffic keywords for maximum search visibility, focusing on parent and child markets to capture a broad audience of industry professionals, investors, and policymakers. All monetary values are presented in billion units for clarity.

North America Gas Turbine Power Generation Industry Market Dynamics & Structure

The North America Gas Turbine Power Generation Industry is characterized by a moderate to high level of market concentration, with key players such as General Electric Company, Siemens AG, and Mitsubishi Heavy Industries Ltd. holding significant market shares. Technological innovation is a primary driver, with continuous advancements in efficiency, emissions reduction, and fuel flexibility fueling market growth. The regulatory framework, particularly environmental regulations and energy transition policies in the United States and Canada, plays a pivotal role in shaping market dynamics. Competitive product substitutes, primarily renewable energy sources like solar and wind, present a constant challenge, driving the need for gas turbine technologies that offer grid stability and dispatchability. End-user demographics are shifting, with a growing demand for reliable and cleaner power generation solutions across the power and oil & gas sectors. Mergers and Acquisitions (M&A) trends indicate strategic consolidation and diversification within the industry.

- Market Concentration: Dominated by a few large players, with increasing fragmentation in niche segments.

- Technological Innovation Drivers: Focus on higher efficiency, lower emissions (e.g., hydrogen co-firing), and digitalization for predictive maintenance.

- Regulatory Frameworks: Stringent environmental standards and incentives for cleaner energy production.

- Competitive Product Substitutes: Growing integration of renewable energy, necessitating flexible and reliable backup power from gas turbines.

- End-User Demographics: Increasing demand from utilities for grid modernization and from the oil & gas sector for efficient on-site power.

- M&A Trends: Strategic acquisitions aimed at expanding product portfolios and geographic reach; divestitures of non-core assets.

North America Gas Turbine Power Generation Industry Growth Trends & Insights

The North America Gas Turbine Power Generation Industry is poised for robust growth, driven by the increasing demand for reliable and flexible power generation solutions. The market size is projected to evolve significantly, influenced by factors such as aging power infrastructure, the ongoing energy transition, and the need for a stable power source to complement intermittent renewables. Adoption rates of advanced gas turbine technologies, including those designed for combined cycle operations and for a wider range of fuel types, are expected to climb. Technological disruptions, such as the development of more efficient aeroderivative turbines and enhanced digital monitoring systems, are key to this evolution. Consumer behavior shifts, particularly the growing emphasis on sustainability and reduced carbon footprints, are compelling utilities and industrial users to invest in cleaner and more efficient gas turbine solutions. The market penetration of gas turbines for peak load and baseload power generation is expected to remain strong, adapting to the evolving energy mix. The Compound Annual Growth Rate (CAGR) is projected to be XX% during the forecast period. The estimated market size for 2025 is $XX billion, with an anticipated growth to $XX billion by 2033. This growth is underpinned by the ongoing replacement of older, less efficient units and the construction of new power plants designed to meet increasing energy demands and stringent environmental regulations. The industry is also witnessing a trend towards distributed power generation, with smaller-scale gas turbines playing a crucial role in supporting industrial operations and remote communities. Furthermore, the integration of advanced control systems and artificial intelligence in gas turbine operations is enhancing performance, reliability, and cost-effectiveness, further stimulating market expansion. The development of hydrogen-ready gas turbines is a significant emerging trend, positioning the technology as a key enabler of decarbonization efforts in the coming years.

Dominant Regions, Countries, or Segments in North America Gas Turbine Power Generation Industry

The United States stands as the dominant region within the North America Gas Turbine Power Generation Industry, driven by its vast energy consumption, established power infrastructure, and evolving regulatory landscape. The "Power" end-user industry, encompassing utilities and independent power producers, is the primary driver of this dominance. Within the capacity segments, "Above 120 MW" turbines are crucial for large-scale power generation, while "31 to 120 MW" turbines cater to intermediate load requirements and distributed generation. "Combined Cycle" power plants, leveraging the high efficiency of gas turbines, represent the favored technology for baseload and intermediate power generation due to their ability to maximize energy output and minimize emissions. The "Oil and Gas" sector also contributes significantly, utilizing gas turbines for power generation at extraction sites, refineries, and processing facilities. Canada, while smaller in market size, plays a vital role, particularly in the oil and gas sector and in supporting its own domestic power needs. The "Rest of North America," encompassing Mexico, also presents growing opportunities, especially with its increasing industrialization and demand for reliable energy. Key drivers for dominance in the U.S. include substantial investments in grid modernization, the retirement of aging coal-fired power plants, and the need for dispatchable power to balance the intermittency of renewable energy sources. Economic policies, such as tax incentives for clean energy investments and carbon pricing mechanisms, further bolster the adoption of gas turbine technologies. The market share of gas turbines in the overall North American power generation mix remains significant, estimated at XX%, highlighting their continued importance. The growth potential within the "Above 120 MW" segment is substantial, driven by the construction of new, highly efficient power plants. The adoption of advanced combustion technologies and emission control systems is essential for maintaining gas turbines' competitiveness.

- Dominant Country: United States, due to its large market size and extensive power infrastructure.

- Dominant End-User Industry: Power sector (utilities and independent power producers).

- Dominant Capacity Segment: Above 120 MW for large-scale power generation.

- Dominant Type: Combined Cycle for enhanced efficiency and reduced emissions.

- Key Drivers: Grid modernization, renewable energy integration, and environmental regulations.

- Growth Potential: Strong in new plant construction and replacement of older units.

North America Gas Turbine Power Generation Industry Product Landscape

The product landscape of the North America Gas Turbine Power Generation Industry is characterized by continuous innovation aimed at enhancing efficiency, reducing emissions, and improving reliability. Leading manufacturers like Siemens AG and General Electric Company are at the forefront, offering a diverse range of gas turbines from less than 30 MW for distributed power to above 120 MW for utility-scale operations. Key product innovations include advanced aerodynamic designs, novel materials for higher temperature operation, and sophisticated digital control systems. Applications span from large combined cycle power plants that form the backbone of electricity grids to open cycle turbines used for peaking power and industrial cogeneration. Performance metrics such as thermal efficiency, power output, and specific fuel consumption are constantly being improved, with the latest models achieving efficiencies exceeding XX%. Unique selling propositions include lower NOx emissions, extended maintenance intervals, and the capability to operate on a wider range of fuels, including natural gas with increasing percentages of hydrogen.

Key Drivers, Barriers & Challenges in North America Gas Turbine Power Generation Industry

The North America Gas Turbine Power Generation Industry is propelled by several key drivers. These include the ongoing need for reliable and dispatchable power to balance the grid, especially with the increasing integration of intermittent renewable energy sources. Technological advancements in efficiency and emissions reduction, such as hydrogen co-firing capabilities, are also significant drivers, aligning with decarbonization goals. Economic factors, like the retirement of aging fossil fuel power plants and the demand for cost-effective energy solutions, further contribute to market growth.

However, the industry faces substantial barriers and challenges. The primary challenge is the intensifying competition from renewable energy sources like solar and wind power, which are experiencing significant cost reductions. Stringent environmental regulations, while driving innovation, can also increase operational costs and necessitate complex compliance measures. Supply chain disruptions, particularly for specialized components and raw materials, pose a risk to production timelines and costs. Furthermore, the long lead times for large-scale gas turbine project development and the capital-intensive nature of these investments can be a barrier for some market participants. The perceived long-term uncertainty regarding fossil fuel reliance in some policy environments also presents a challenge.

Emerging Opportunities in North America Gas Turbine Power Generation Industry

Emerging opportunities in the North America Gas Turbine Power Generation Industry lie in the development and deployment of hydrogen-ready gas turbines, positioning them as a crucial component of future low-carbon energy systems. The growing demand for distributed generation and microgrids, particularly in industrial and remote areas, presents a significant market for smaller-capacity gas turbines. Furthermore, the modernization and repowering of existing gas turbine fleets with advanced technologies offer substantial opportunities for upgrades and performance enhancements. The digitalization of gas turbine operations, including predictive maintenance and remote monitoring powered by AI and IoT, is another area ripe for innovation and service-based revenue generation.

Growth Accelerators in the North America Gas Turbine Power Generation Industry Industry

The North America Gas Turbine Power Generation Industry is experiencing significant growth acceleration fueled by technological breakthroughs in fuel flexibility, particularly the integration of hydrogen. Strategic partnerships between turbine manufacturers, utilities, and research institutions are fostering rapid innovation and market adoption. Market expansion strategies, including the development of integrated energy solutions that combine gas turbines with renewable energy and energy storage, are also driving growth. The increasing focus on energy security and resilience, especially in light of geopolitical uncertainties, further accelerates the demand for reliable gas turbine power generation.

Key Players Shaping the North America Gas Turbine Power Generation Industry Market

- Solar Turbines Inc

- Kawasaki Heavy Industries Ltd

- Siemens AG

- General Electric Company

- Harbin Electric International Company Limited

- Capstone Turbine Corporation

- Mitsubishi Heavy Industries Ltd

- Rolls-Royce Holding PLC

Notable Milestones in North America Gas Turbine Power Generation Industry Sector

- 2023: Launch of next-generation hydrogen-capable gas turbines by major manufacturers, signaling a strong commitment to decarbonization.

- 2023: Increased investment in grid modernization projects across the US, incorporating advanced gas turbine solutions for grid stability.

- 2022: Several utility-scale combined cycle power plants announced or commenced construction, highlighting ongoing demand for baseload power.

- 2021: Significant advancements in digital twin technology for gas turbine predictive maintenance, improving uptime and reducing operational costs.

- 2020: Growing adoption of aeroderivative gas turbines for enhanced flexibility and faster ramp-up times in power generation.

In-Depth North America Gas Turbine Power Generation Industry Market Outlook

The future outlook for the North America Gas Turbine Power Generation Industry is one of continued evolution and adaptation. Growth accelerators such as advancements in hydrogen fuel combustion, sophisticated digital integration for operational optimization, and strategic collaborations will be instrumental in shaping the market. The industry is set to play a crucial role in enabling a smoother energy transition by providing reliable and flexible power to complement the growing renewable energy portfolio. Opportunities in repowering older assets, developing advanced distributed generation solutions, and enhancing the efficiency and environmental performance of existing fleets present substantial avenues for future growth and market leadership. The sector is well-positioned to meet evolving energy demands while addressing critical climate objectives.

North America Gas Turbine Power Generation Industry Segmentation

-

1. Capacity

- 1.1. Less than 30 MW

- 1.2. 31 to 120 MW

- 1.3. Above 120

-

2. Type

- 2.1. Combined Cycle

- 2.2. Open Cycle

-

3. End-User Industries

- 3.1. Power

- 3.2. Oil and Gas

- 3.3. Other End-User Industries

-

4. Geography

- 4.1. United States

- 4.2. Canada

- 4.3. Restof North America

North America Gas Turbine Power Generation Industry Segmentation By Geography

- 1. United States

- 2. Canada

- 3. Restof North America

North America Gas Turbine Power Generation Industry Regional Market Share

Geographic Coverage of North America Gas Turbine Power Generation Industry

North America Gas Turbine Power Generation Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Capacity

- 5.1.1. Less than 30 MW

- 5.1.2. 31 to 120 MW

- 5.1.3. Above 120

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Combined Cycle

- 5.2.2. Open Cycle

- 5.3. Market Analysis, Insights and Forecast - by End-User Industries

- 5.3.1. Power

- 5.3.2. Oil and Gas

- 5.3.3. Other End-User Industries

- 5.4. Market Analysis, Insights and Forecast - by Geography

- 5.4.1. United States

- 5.4.2. Canada

- 5.4.3. Restof North America

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. United States

- 5.5.2. Canada

- 5.5.3. Restof North America

- 5.1. Market Analysis, Insights and Forecast - by Capacity

- 6. North America Gas Turbine Power Generation Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Capacity

- 6.1.1. Less than 30 MW

- 6.1.2. 31 to 120 MW

- 6.1.3. Above 120

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Combined Cycle

- 6.2.2. Open Cycle

- 6.3. Market Analysis, Insights and Forecast - by End-User Industries

- 6.3.1. Power

- 6.3.2. Oil and Gas

- 6.3.3. Other End-User Industries

- 6.4. Market Analysis, Insights and Forecast - by Geography

- 6.4.1. United States

- 6.4.2. Canada

- 6.4.3. Restof North America

- 6.1. Market Analysis, Insights and Forecast - by Capacity

- 7. United States North America Gas Turbine Power Generation Industry Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Capacity

- 7.1.1. Less than 30 MW

- 7.1.2. 31 to 120 MW

- 7.1.3. Above 120

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Combined Cycle

- 7.2.2. Open Cycle

- 7.3. Market Analysis, Insights and Forecast - by End-User Industries

- 7.3.1. Power

- 7.3.2. Oil and Gas

- 7.3.3. Other End-User Industries

- 7.4. Market Analysis, Insights and Forecast - by Geography

- 7.4.1. United States

- 7.4.2. Canada

- 7.4.3. Restof North America

- 7.1. Market Analysis, Insights and Forecast - by Capacity

- 8. Canada North America Gas Turbine Power Generation Industry Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Capacity

- 8.1.1. Less than 30 MW

- 8.1.2. 31 to 120 MW

- 8.1.3. Above 120

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Combined Cycle

- 8.2.2. Open Cycle

- 8.3. Market Analysis, Insights and Forecast - by End-User Industries

- 8.3.1. Power

- 8.3.2. Oil and Gas

- 8.3.3. Other End-User Industries

- 8.4. Market Analysis, Insights and Forecast - by Geography

- 8.4.1. United States

- 8.4.2. Canada

- 8.4.3. Restof North America

- 8.1. Market Analysis, Insights and Forecast - by Capacity

- 9. Restof North America North America Gas Turbine Power Generation Industry Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Capacity

- 9.1.1. Less than 30 MW

- 9.1.2. 31 to 120 MW

- 9.1.3. Above 120

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Combined Cycle

- 9.2.2. Open Cycle

- 9.3. Market Analysis, Insights and Forecast - by End-User Industries

- 9.3.1. Power

- 9.3.2. Oil and Gas

- 9.3.3. Other End-User Industries

- 9.4. Market Analysis, Insights and Forecast - by Geography

- 9.4.1. United States

- 9.4.2. Canada

- 9.4.3. Restof North America

- 9.1. Market Analysis, Insights and Forecast - by Capacity

- 10. Competitive Analysis

- 10.1. Company Profiles

- 10.1.1 Solar Turbines Inc

- 10.1.1.1. Company Overview

- 10.1.1.2. Products

- 10.1.1.3. Company Financials

- 10.1.1.4. SWOT Analysis

- 10.1.2 Kawasaki Heavy Industries Ltd

- 10.1.2.1. Company Overview

- 10.1.2.2. Products

- 10.1.2.3. Company Financials

- 10.1.2.4. SWOT Analysis

- 10.1.3 Siemens AG

- 10.1.3.1. Company Overview

- 10.1.3.2. Products

- 10.1.3.3. Company Financials

- 10.1.3.4. SWOT Analysis

- 10.1.4 General Electric Company

- 10.1.4.1. Company Overview

- 10.1.4.2. Products

- 10.1.4.3. Company Financials

- 10.1.4.4. SWOT Analysis

- 10.1.5 Harbin Electric International Company Limited

- 10.1.5.1. Company Overview

- 10.1.5.2. Products

- 10.1.5.3. Company Financials

- 10.1.5.4. SWOT Analysis

- 10.1.6 Capstone Turbine Corporation

- 10.1.6.1. Company Overview

- 10.1.6.2. Products

- 10.1.6.3. Company Financials

- 10.1.6.4. SWOT Analysis

- 10.1.7 Mitsubishi Heavy Industries Ltd

- 10.1.7.1. Company Overview

- 10.1.7.2. Products

- 10.1.7.3. Company Financials

- 10.1.7.4. SWOT Analysis

- 10.1.8 Rolls-Royce Holding PLC

- 10.1.8.1. Company Overview

- 10.1.8.2. Products

- 10.1.8.3. Company Financials

- 10.1.8.4. SWOT Analysis

- 10.1.1 Solar Turbines Inc

- 10.2. Market Entropy

- 10.2.1 Company's Key Areas Served

- 10.2.2 Recent Developments

- 10.3. Company Market Share Analysis 2025

- 10.3.1 Top 5 Companies Market Share Analysis

- 10.3.2 Top 3 Companies Market Share Analysis

- 10.4. List of Potential Customers

- 11. Research Methodology

List of Figures

- Figure 1: North America Gas Turbine Power Generation Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: North America Gas Turbine Power Generation Industry Share (%) by Company 2025

List of Tables

- Table 1: North America Gas Turbine Power Generation Industry Revenue billion Forecast, by Capacity 2020 & 2033

- Table 2: North America Gas Turbine Power Generation Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 3: North America Gas Turbine Power Generation Industry Revenue billion Forecast, by End-User Industries 2020 & 2033

- Table 4: North America Gas Turbine Power Generation Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 5: North America Gas Turbine Power Generation Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 6: North America Gas Turbine Power Generation Industry Revenue billion Forecast, by Capacity 2020 & 2033

- Table 7: North America Gas Turbine Power Generation Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 8: North America Gas Turbine Power Generation Industry Revenue billion Forecast, by End-User Industries 2020 & 2033

- Table 9: North America Gas Turbine Power Generation Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 10: North America Gas Turbine Power Generation Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 11: North America Gas Turbine Power Generation Industry Revenue billion Forecast, by Capacity 2020 & 2033

- Table 12: North America Gas Turbine Power Generation Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 13: North America Gas Turbine Power Generation Industry Revenue billion Forecast, by End-User Industries 2020 & 2033

- Table 14: North America Gas Turbine Power Generation Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 15: North America Gas Turbine Power Generation Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 16: North America Gas Turbine Power Generation Industry Revenue billion Forecast, by Capacity 2020 & 2033

- Table 17: North America Gas Turbine Power Generation Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 18: North America Gas Turbine Power Generation Industry Revenue billion Forecast, by End-User Industries 2020 & 2033

- Table 19: North America Gas Turbine Power Generation Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 20: North America Gas Turbine Power Generation Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Gas Turbine Power Generation Industry?

The projected CAGR is approximately 11.2%.

2. Which companies are prominent players in the North America Gas Turbine Power Generation Industry?

Key companies in the market include Solar Turbines Inc, Kawasaki Heavy Industries Ltd, Siemens AG, General Electric Company, Harbin Electric International Company Limited, Capstone Turbine Corporation, Mitsubishi Heavy Industries Ltd, Rolls-Royce Holding PLC.

3. What are the main segments of the North America Gas Turbine Power Generation Industry?

The market segments include Capacity, Type, End-User Industries, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 22.6 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Supportive Government Policies and Incentives4.; Environmental Concerns.

6. What are the notable trends driving market growth?

Power Generation Application is Expected to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; Fossil Fuel Subsidies.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Gas Turbine Power Generation Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Gas Turbine Power Generation Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Gas Turbine Power Generation Industry?

To stay informed about further developments, trends, and reports in the North America Gas Turbine Power Generation Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence