Key Insights

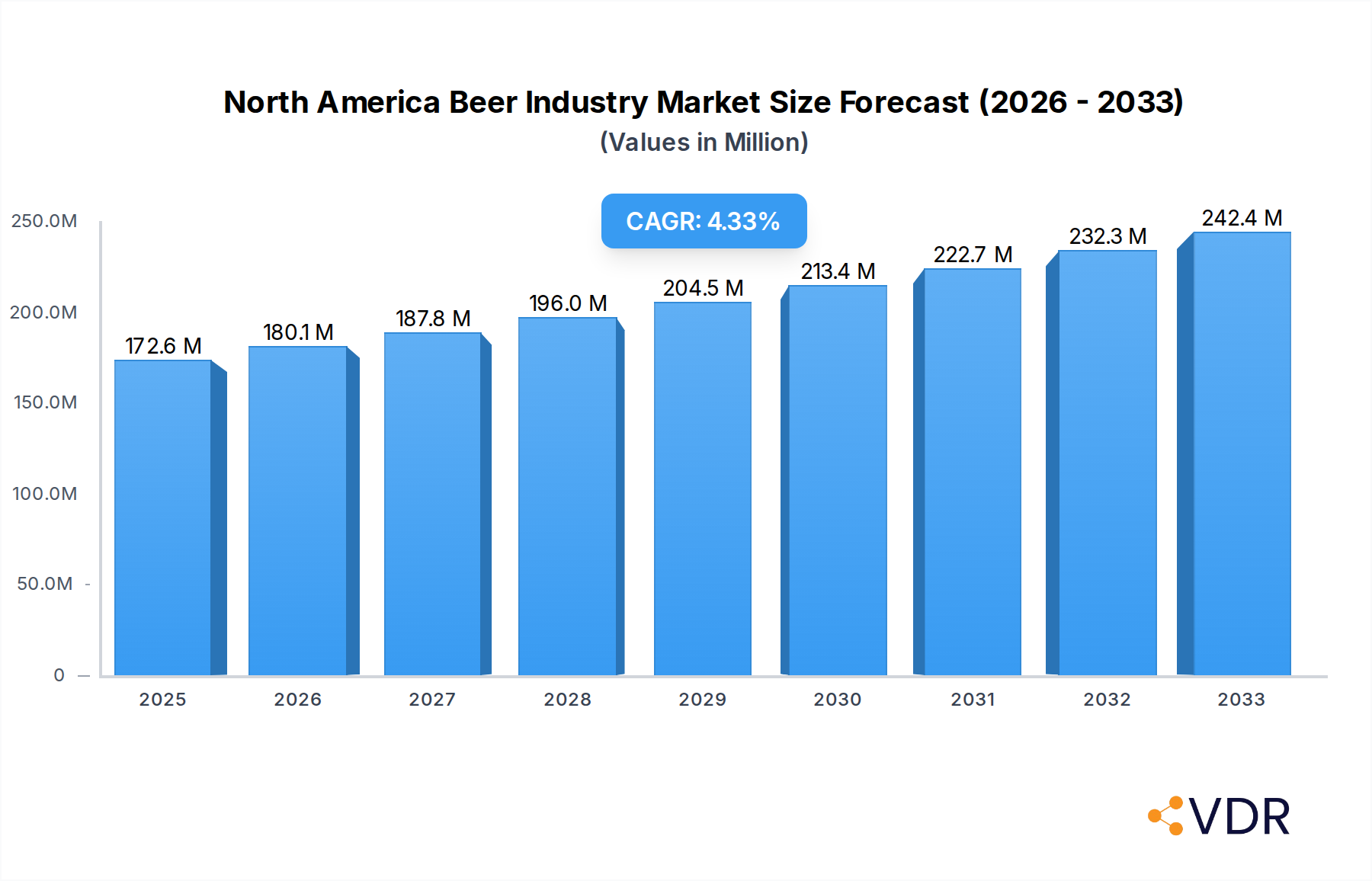

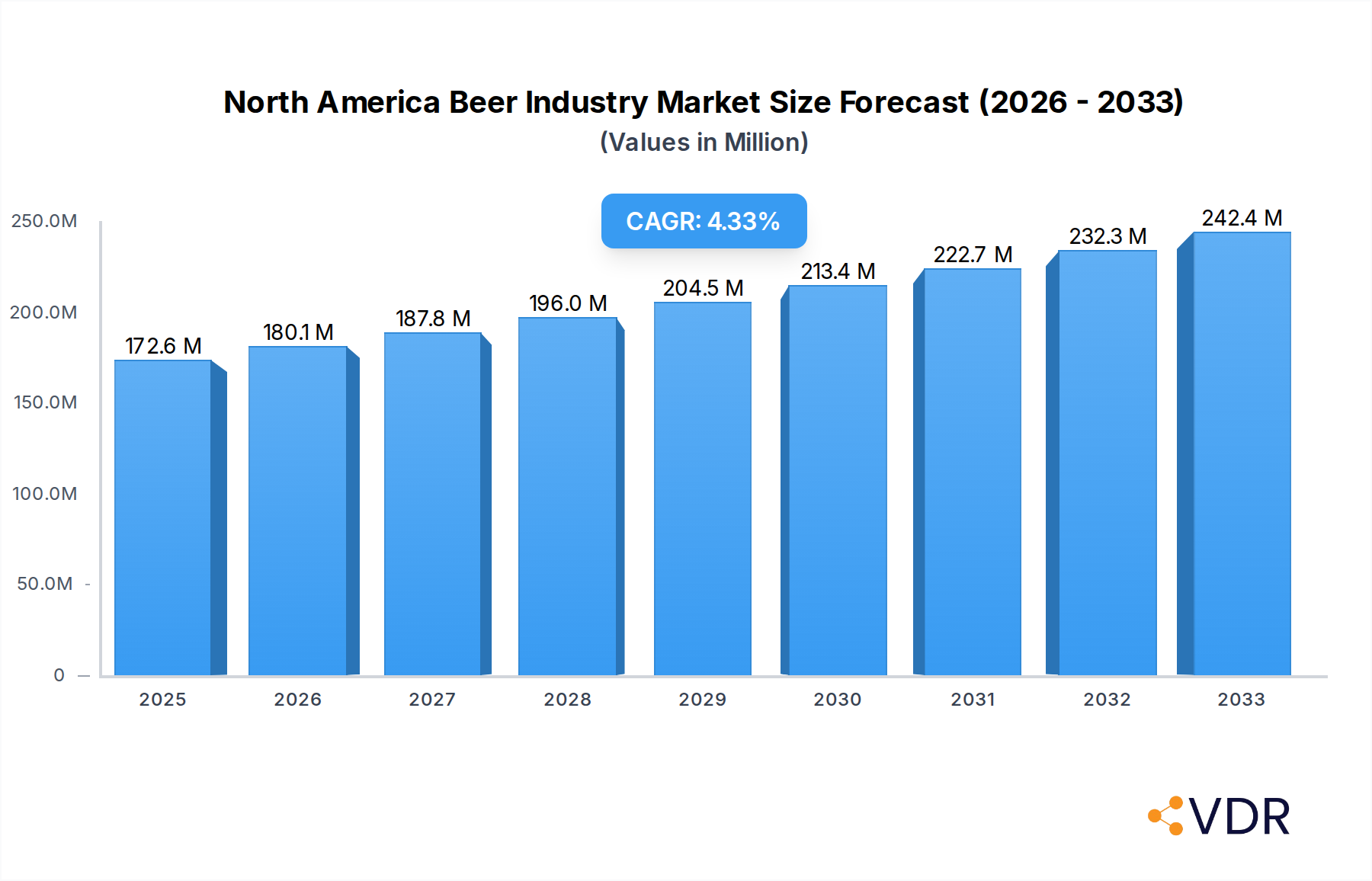

The North American beer market is poised for steady expansion, projected to reach $172.63 million by 2025, with a compelling Compound Annual Growth Rate (CAGR) of 4.39% through 2033. This growth is underpinned by a confluence of evolving consumer preferences and a dynamic industry landscape. Key drivers fueling this upward trajectory include the increasing demand for craft and premium beer varieties, a testament to consumers seeking novel flavor profiles and higher quality experiences. Furthermore, the growing popularity of ready-to-drink (RTD) alcoholic beverages, often categorized within the broader beer market, is contributing significantly to market penetration, particularly among younger demographics. The robust performance of the off-trade distribution channel, driven by convenience and at-home consumption trends amplified by recent global events, continues to be a dominant force. Conversely, the on-trade sector, encompassing bars and restaurants, is experiencing a resurgence as social gatherings and entertainment activities rebound. Despite these positive trends, challenges such as rising raw material costs and increasing excise duties in certain regions pose potential restraints to even more rapid growth, necessitating strategic pricing and operational efficiencies from market players.

North America Beer Industry Market Size (In Million)

The North American beer industry is characterized by intense competition and a strategic focus on product innovation and market diversification. Leading companies like Anheuser-Busch InBev, Molson Coors Beverage Company, and Heineken Holding N.V. are actively engaged in expanding their portfolios, acquiring or investing in craft breweries, and leveraging their established distribution networks to capture market share across diverse consumer segments. The market is segmenting further, with Lager retaining its dominance due to widespread appeal, while Ale and other specialty brews are experiencing significant growth, driven by consumer curiosity and a desire for unique taste experiences. The regional focus on North America, particularly the United States, Canada, and Mexico, highlights these key markets' substantial consumption patterns and economic influence. The interplay between on-trade recovery and the enduring strength of off-trade sales creates a complex yet opportunity-rich environment for beverage manufacturers and distributors navigating the evolving tastes and habits of North American beer enthusiasts.

North America Beer Industry Company Market Share

Dive deep into the dynamic North American beer market with this exhaustive report, covering critical insights from 2019 through 2033. Analyze parent and child market segments, understand evolving consumer preferences, and identify key growth drivers and challenges. This report provides quantitative data in million units, CAGR projections, and strategic analysis essential for industry professionals.

North America Beer Industry Market Dynamics & Structure

The North American beer industry is characterized by a moderate market concentration, with a few dominant players like Anheuser-Busch InBev and Molson Coors Beverage Company holding significant shares, alongside a burgeoning landscape of craft breweries. Technological innovation is primarily driven by advancements in brewing processes, packaging, and the integration of digital platforms for sales and marketing. Regulatory frameworks, encompassing excise taxes, labeling laws, and distribution regulations, play a crucial role in shaping market entry and operational strategies across the United States, Canada, and Mexico. Competitive product substitutes, including wine, spirits, and non-alcoholic beverages, exert constant pressure, necessitating continuous product development and brand differentiation. End-user demographics are shifting, with a growing preference for premiumization, low-calorie options, and unique flavor profiles, particularly among millennial and Gen Z consumers. Mergers and acquisitions (M&A) remain a strategic tool for consolidation and market expansion.

- Market Concentration: Dominated by global giants but with increasing influence from regional and craft players.

- Technological Innovation: Focus on brewing efficiency, sustainable packaging, and direct-to-consumer (DTC) models.

- Regulatory Frameworks: Complex state and federal regulations influencing production, distribution, and taxation.

- Product Substitutes: Growing competition from craft spirits, hard seltzers, and ready-to-drink (RTD) cocktails.

- End-User Demographics: Shifting preferences towards craft, premium, and healthier beverage options.

- M&A Trends: Strategic acquisitions by major players to expand craft portfolios and market reach.

North America Beer Industry Growth Trends & Insights

The North American beer market is poised for steady growth, projected to expand significantly over the forecast period. This expansion is fueled by evolving consumer behavior, a sustained demand for premium and craft offerings, and innovative product development. The market size is anticipated to witness a Compound Annual Growth Rate (CAGR) of approximately 3.5% from the base year 2025. Adoption rates for innovative segments like low-alcohol and no-alcohol beers are steadily increasing, reflecting a growing health-conscious consumer base. Technological disruptions are manifesting in enhanced brewing techniques that allow for greater flavor complexity and consistency, alongside the adoption of advanced data analytics for better consumer targeting and inventory management. Consumer behavior shifts are marked by a move towards experiential consumption, a greater appreciation for brand stories and provenance, and an increasing reliance on e-commerce and delivery services for purchasing beer. The market penetration of specialty and craft beers continues to rise, encroaching on the market share traditionally held by mass-market lagers. Furthermore, the growing popularity of RTD beverages, often categorized alongside beer in off-trade channels, presents both a challenge and an opportunity for traditional brewers to innovate and diversify their portfolios. The influence of social media and influencer marketing is also playing a more significant role in shaping consumer preferences and driving product discovery. The pursuit of unique flavor profiles and limited-edition releases further contributes to market dynamism and consumer engagement.

Dominant Regions, Countries, or Segments in North America Beer Industry

The United States unequivocally dominates the North American beer industry, driven by its sheer market size, diverse consumer base, and robust economic landscape. Within the US, the Lager segment, encompassing a wide array of styles from light lagers to traditional pilsners, continues to hold the largest market share, catering to a broad spectrum of consumer preferences and occasions. However, the Ale segment, particularly craft ales, has witnessed remarkable growth and innovation, capturing significant consumer attention and driving premiumization trends. The Off-Trade distribution channel consistently leads in volume sales, owing to the convenience of retail purchasing for home consumption. Key drivers for the US market dominance include a well-established distribution infrastructure, a high disposable income, and a deeply ingrained beer-drinking culture. Economic policies that support small businesses have fostered the growth of independent craft breweries, further diversifying the market.

- Dominant Country: United States, accounting for approximately 75% of the North American beer market volume.

- Dominant Segment (Type): Lager remains the largest segment, with an estimated market share of 55% in 2025.

- Dominant Segment (Distribution Channel): Off-Trade channels are projected to hold over 60% of the market volume in 2025.

- Key Growth Drivers in the US:

- High disposable income and consumer spending power.

- Extensive retail and distribution networks.

- Strong craft beer culture and consumer demand for variety.

- Innovation in product development and marketing.

- Canada's Contribution: Canada represents a significant portion of the market, with a growing craft beer scene and increasing preference for premium and imported brands.

- Mexico's Market Dynamics: Mexico, while smaller in overall volume, exhibits strong growth potential, particularly driven by the popularity of its indigenous brands and increasing demand for imported beers.

- Segment Growth Potential: The Ale segment, especially craft ales, is expected to exhibit the highest CAGR over the forecast period, driven by evolving consumer tastes and premiumization.

North America Beer Industry Product Landscape

The North American beer product landscape is characterized by continuous innovation and diversification. Lagers, including light and premium variants, remain foundational, while the Ale segment thrives on creativity, with IPAs, stouts, and sours gaining significant traction. The "Others" category encompasses growing segments like hard seltzers and ready-to-drink (RTD) cocktails, which are increasingly competing for share. Product innovations focus on unique flavor infusions, healthier options (low-calorie, low-carb, gluten-free), and sustainable packaging solutions. For instance, Anheuser-Busch InBev is continually exploring new flavor profiles in its core brands, while Boston Beer Company's Truly Hard Seltzer continues to capture market share with its diverse flavor offerings.

Key Drivers, Barriers & Challenges in North America Beer Industry

Key Drivers:

- Premiumization and Craft Beer Demand: Consumers are willing to pay more for higher-quality, unique, and artisanal beer experiences.

- Product Innovation: Development of new styles, flavors, and healthier alternatives like low-alcohol and no-alcohol beers.

- Evolving Consumer Lifestyles: Increased demand for convenient, on-the-go beverage options and a growing appreciation for craft and local brands.

Barriers & Challenges:

- Intense Competition: High saturation of brands and segments, including competition from wine, spirits, and non-alcoholic beverages.

- Regulatory Hurdles: Stringent alcohol-related regulations, excise taxes, and varying state/provincial laws impacting production and distribution.

- Supply Chain Disruptions: Volatility in raw material prices (hops, barley) and potential logistical challenges can impact costs and availability.

- Shifting Consumer Preferences: Rapid changes in consumer tastes and the emergence of new beverage categories require constant adaptation.

Emerging Opportunities in North America Beer Industry

Emerging opportunities lie in the continued growth of the low-alcohol and no-alcohol (NA) beer segment, catering to health-conscious consumers and those seeking to reduce alcohol consumption without sacrificing taste. The craft and specialty beer market offers ample room for differentiation through unique ingredients, brewing techniques, and limited-edition releases. Furthermore, the direct-to-consumer (DTC) e-commerce channel presents significant potential for breweries to engage directly with customers, build brand loyalty, and offer exclusive products, especially with evolving online sales regulations. Expanding into underserved geographic markets within North America and exploring innovative packaging solutions that emphasize sustainability and convenience also represent key growth avenues.

Growth Accelerators in the North America Beer Industry Industry

Growth in the North American beer industry is being significantly accelerated by strategic partnerships and collaborations between established brewers and emerging craft breweries, fostering innovation and market penetration. Technological advancements in brewing are enabling greater efficiency, consistency, and the creation of novel flavor profiles, driving consumer interest. The expansion of e-commerce and direct-to-consumer sales channels provides brewers with new avenues to reach consumers and bypass traditional distribution bottlenecks. Moreover, investments in marketing and brand storytelling that resonate with younger demographics and emphasize craftmanship and authenticity are proving highly effective in capturing market share and fostering long-term brand loyalty.

Key Players Shaping the North America Beer Industry Market

- Anheuser-Busch InBev

- Molson Coors Beverage Company

- Heineken Holding N V

- Diageo Plc

- Constellation Brands Inc

- Suntory Beverage & Food Limited

- FIFCO USA

- Carlsberg Group

- Boston Beer Company

- D G Yuengling & Son Inc

Notable Milestones in North America Beer Industry Sector

- November 2022: Goose Island Beer Company's Canada branch launched the 2022 edition of Bourbon County Stout, officially introduced in the United States on Black Friday. The 2022 Original Bourbon County Stout was aged in a mix of bourbon barrels from Buffalo Trace, Heaven Hill, and Wild Turkey distilleries, highlighting premium aging techniques and limited releases.

- July 2022: Royal Unibrew acquired the entire stock of Toronto-based Amsterdam Brewery Co. Ltd. This strategic acquisition, aimed at serving Canada and a portion of the US, involved increasing capacity in Canada to reduce shipping costs and carbon footprint, demonstrating M&A activity focused on regional expansion and operational efficiency.

- March 2022: Modelo declared the launch of Modelo Oro, a premium light beer. This move targeted the expansion of their product portfolio with new flavors and aimed to bolster their leadership in the high-end beverage category, showcasing new product development to capture market share in a competitive segment.

In-Depth North America Beer Industry Market Outlook

The North American beer industry's outlook is characterized by sustained growth driven by consumer-led trends toward premiumization, craft offerings, and healthier beverage choices. Growth accelerators such as e-commerce expansion and technological innovations in brewing will continue to reshape the market landscape. Strategic partnerships and a focus on unique brand narratives will be crucial for capturing the attention of evolving demographics. The industry is poised to witness significant opportunities in the low- and no-alcohol segments, as well as through the continuous innovation of ale varieties and the exploration of niche consumer preferences.

North America Beer Industry Segmentation

-

1. Type

- 1.1. Lager

- 1.2. Ale

- 1.3. Others

-

2. Distribution Channel

- 2.1. On-Trade

- 2.2. Off-Trade

North America Beer Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

North America Beer Industry Regional Market Share

Geographic Coverage of North America Beer Industry

North America Beer Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.39% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Lager

- 5.1.2. Ale

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. On-Trade

- 5.2.2. Off-Trade

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. North America Beer Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Lager

- 6.1.2. Ale

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.2.1. On-Trade

- 6.2.2. Off-Trade

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Anheuser-Busch InBev

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 D G Yuengling & Son Inc *List Not Exhaustive

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Molson Coors Beverage Company

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Heineken Holding N V

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Diageo Plc

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Constellation Brands Inc

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Suntory Beverage & Food Limited

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 FIFCO USA

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Carlsberg Group

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Boston Beer Company

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Anheuser-Busch InBev

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: North America Beer Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: North America Beer Industry Share (%) by Company 2025

List of Tables

- Table 1: North America Beer Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 2: North America Beer Industry Volume liter Forecast, by Type 2020 & 2033

- Table 3: North America Beer Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 4: North America Beer Industry Volume liter Forecast, by Distribution Channel 2020 & 2033

- Table 5: North America Beer Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 6: North America Beer Industry Volume liter Forecast, by Region 2020 & 2033

- Table 7: North America Beer Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 8: North America Beer Industry Volume liter Forecast, by Type 2020 & 2033

- Table 9: North America Beer Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 10: North America Beer Industry Volume liter Forecast, by Distribution Channel 2020 & 2033

- Table 11: North America Beer Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 12: North America Beer Industry Volume liter Forecast, by Country 2020 & 2033

- Table 13: United States North America Beer Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: United States North America Beer Industry Volume (liter ) Forecast, by Application 2020 & 2033

- Table 15: Canada North America Beer Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Canada North America Beer Industry Volume (liter ) Forecast, by Application 2020 & 2033

- Table 17: Mexico North America Beer Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Mexico North America Beer Industry Volume (liter ) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Beer Industry?

The projected CAGR is approximately 4.39%.

2. Which companies are prominent players in the North America Beer Industry?

Key companies in the market include Anheuser-Busch InBev, D G Yuengling & Son Inc *List Not Exhaustive, Molson Coors Beverage Company, Heineken Holding N V, Diageo Plc, Constellation Brands Inc, Suntory Beverage & Food Limited, FIFCO USA, Carlsberg Group, Boston Beer Company.

3. What are the main segments of the North America Beer Industry?

The market segments include Type, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 172.63 Million as of 2022.

5. What are some drivers contributing to market growth?

Growing Demand for Nutricosmetics Among Millennials; Growing Beauty and Wellness Trend.

6. What are the notable trends driving market growth?

Growing Demand for Beer Across the United States.

7. Are there any restraints impacting market growth?

Stringent Government Regulations and Product Guidelines.

8. Can you provide examples of recent developments in the market?

In November 2022, Goose Island Beer Company's Canada branch announced the launch of the 2022 edition of Bourbon County Stout. It was officially introduced in the United States on Black Friday. The 2022 Original Bourbon County Stout was aged in a mix of bourbon barrels from Buffalo Trace, Heaven Hill, and Wild Turkey distilleries.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in liter .

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Beer Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Beer Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Beer Industry?

To stay informed about further developments, trends, and reports in the North America Beer Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence