Key Insights

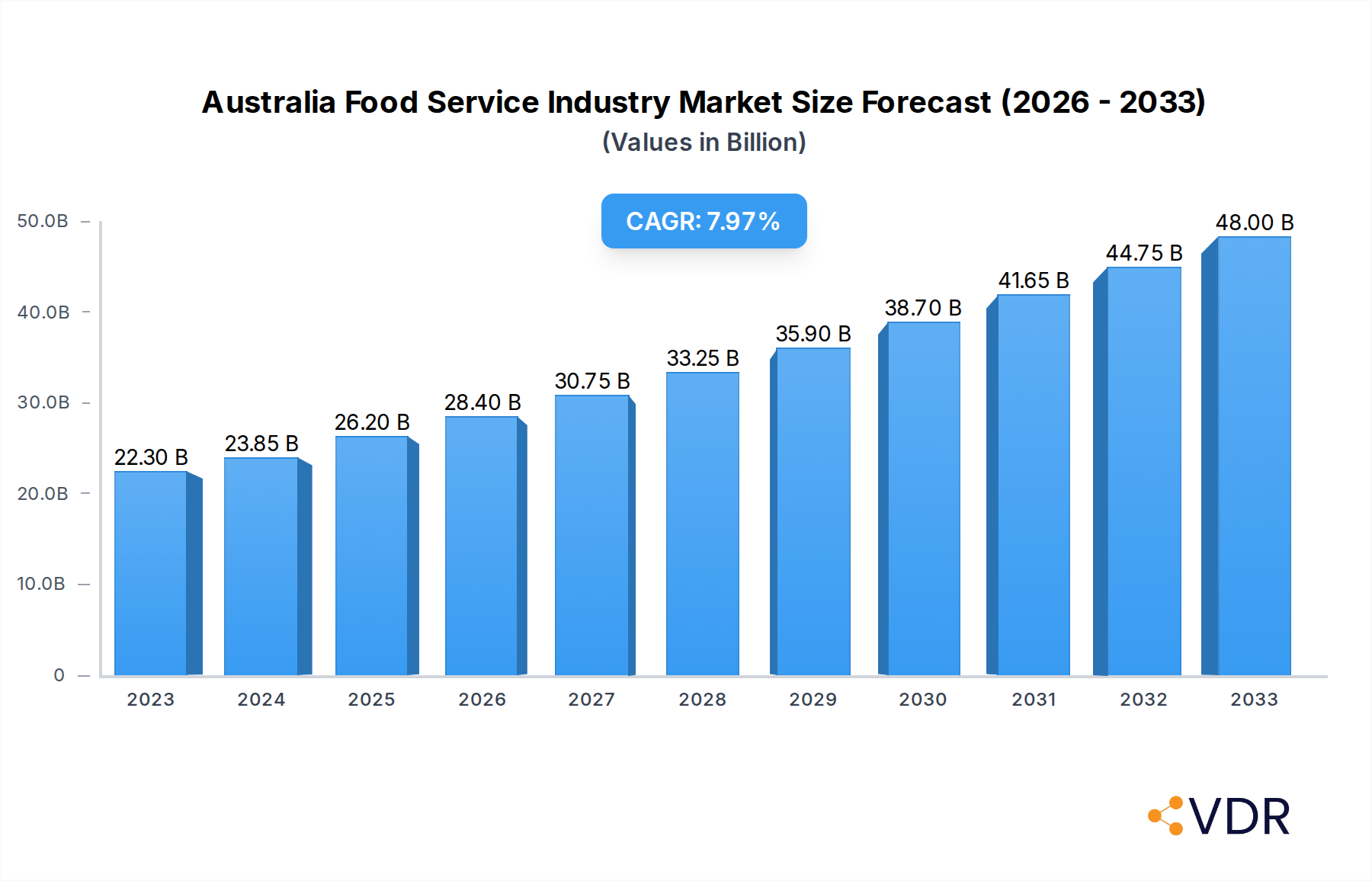

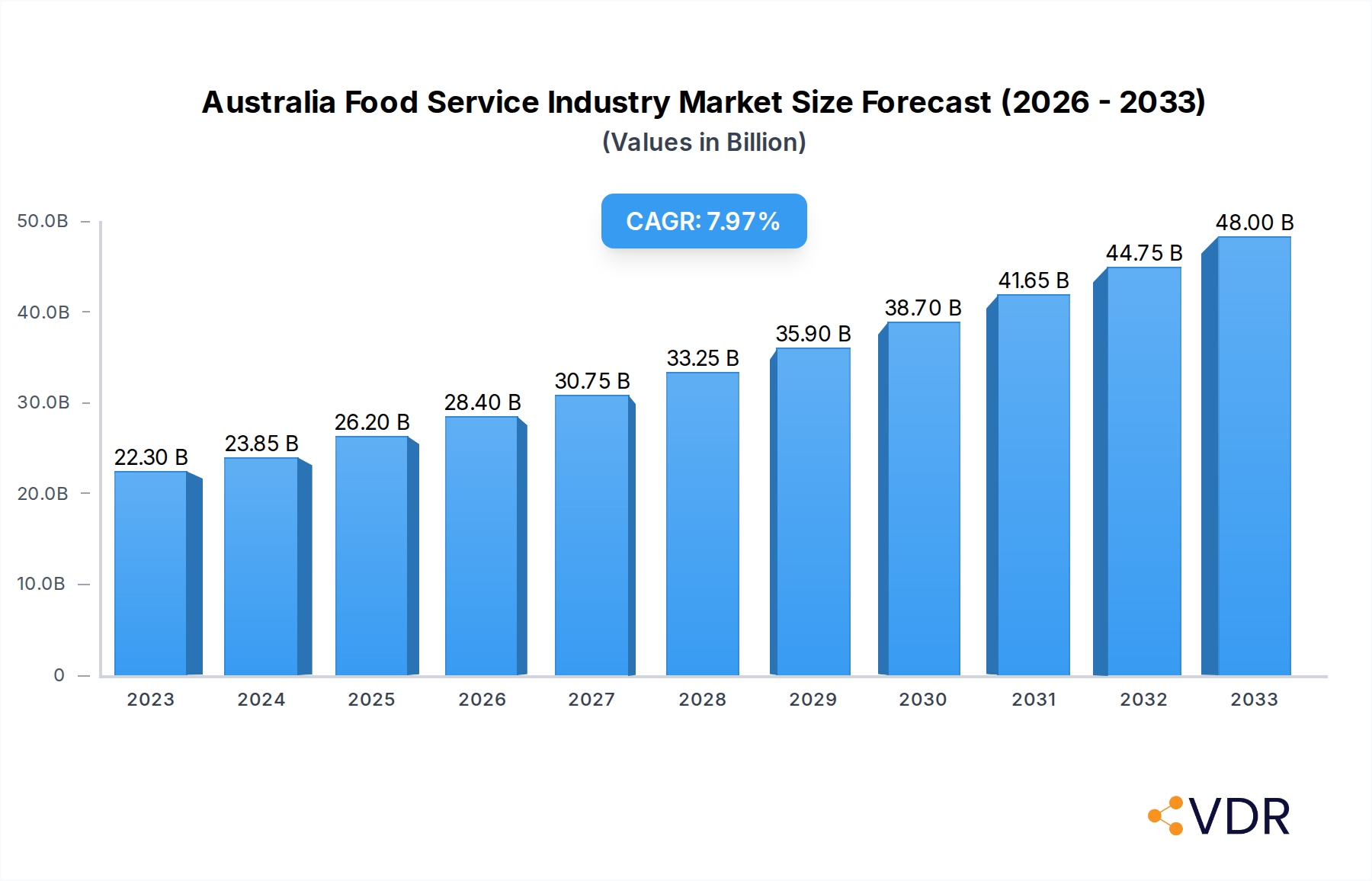

The Australian food service industry is poised for significant expansion, projected to reach AUD 26.2 billion by 2025. This robust growth is driven by a CAGR of 8.2% forecasted from 2019 to 2033, indicating sustained momentum in the market. Key drivers fueling this expansion include evolving consumer preferences for convenient and diverse dining options, a growing demand for healthy and specialized food offerings, and the increasing penetration of food delivery platforms. The foodservice sector is witnessing a surge in innovation, with cloud kitchens gaining traction due to their operational efficiency and ability to cater to the booming online food ordering segment. Furthermore, the resurgence of dine-in experiences, particularly in full-service restaurants and specialized cafes, reflects a return to social dining, bolstered by an expanding tourism sector and a general increase in disposable income.

Australia Food Service Industry Market Size (In Billion)

The market is strategically segmented to address diverse consumer needs. Cafes & Bars are a dominant segment, encompassing everything from specialist coffee shops to juice bars, reflecting a strong consumer focus on grab-and-go and niche beverage experiences. Full Service Restaurants (FSRs) are showing resilience, with cuisines like Asian and European leading the charge, alongside a growing interest in Middle Eastern and Latin American flavors. Quick Service Restaurants (QSRs) continue to innovate, with a focus on healthier options and diversified offerings beyond traditional burgers and pizza. The rise of chained outlets and the strategic placement of outlets in leisure, lodging, and travel locations underscore the industry's adaptation to consumer lifestyle shifts. While independent outlets also play a crucial role, the infrastructure and marketing power of larger chains are significant growth enablers.

Australia Food Service Industry Company Market Share

Unlocking Australia's Food Service Potential: Market Dynamics, Growth Trends, and Competitive Landscape (2019-2033)

This comprehensive report delves into the dynamic Australia food service industry, offering an in-depth analysis of its market structure, growth trajectories, and the key players shaping its future. With a study period spanning from 2019 to 2033, and a base year of 2025, this report provides invaluable insights for restaurants, cafes, bars, and cloud kitchens seeking to capitalize on burgeoning opportunities. Explore detailed breakdowns by foodservice type, including Full Service Restaurants (FSR) and Quick Service Restaurants (QSR), and understand the impact of chained outlets versus independent outlets. We project the market size to reach $xx billion in 2025, with a projected CAGR of xx% during the forecast period (2025-2033).

Australia Food Service Industry Market Dynamics & Structure

The Australian food service industry is characterized by a moderately concentrated market, with established players like McDonald's Corporation, Yum! Brands Inc., and Inspire Brands Inc. holding significant sway. Technological innovation is a key driver, particularly in areas of delivery platforms, kitchen automation, and personalized customer experiences, fostering operational efficiency. Regulatory frameworks, including food safety standards and licensing requirements, are crucial for market entry and continued operation, influencing the competitive landscape. Substitute products, such as home meal kits and convenience store offerings, present a constant challenge, necessitating continuous menu innovation and value proposition enhancement. End-user demographics are shifting, with a growing demand for healthier options, sustainable practices, and diverse culinary experiences. Mergers and acquisitions (M&A) activity is evident as larger entities seek to consolidate market share and expand their portfolios. For instance, the acquisition of Retail Food Group by Pacific Hunter Group Pty Ltd in 2024 signals ongoing consolidation.

- Market Concentration: Dominated by a few large corporations, but with ample space for agile independents.

- Technological Innovation: Delivery apps, AI-driven ordering, and sustainable packaging are key differentiators.

- Regulatory Framework: Strict food safety and hygiene standards are paramount for all operators.

- Competitive Substitutes: Home cooking, ready-to-eat meals, and ghost kitchens offer alternative dining solutions.

- End-User Demographics: Increasing preference for plant-based diets, ethical sourcing, and experiential dining.

- M&A Trends: Strategic acquisitions to gain market share and introduce new concepts.

Australia Food Service Industry Growth Trends & Insights

The Australia food service industry is on a robust growth trajectory, projected to expand significantly in the coming years. The market size, estimated at $xx billion in 2025, is expected to witness sustained expansion driven by evolving consumer preferences and an increasing disposable income. Adoption rates of digital ordering and delivery platforms have surged, becoming an integral part of the consumer experience and a vital revenue stream for businesses. Technological disruptions, such as the integration of AI in customer service and sophisticated inventory management systems, are enhancing operational efficiency and personalizing customer interactions. Consumer behavior shifts are profoundly impacting the sector, with a heightened demand for convenience, variety, and health-conscious options. The rise of cloud kitchens and ghost kitchen models is a testament to this evolving landscape, catering to the on-demand delivery economy. Furthermore, the increasing popularity of specialist coffee & tea shops and juice/smoothie/desserts bars reflects a growing focus on well-being and niche culinary experiences. The Quick Service Restaurant (QSR) segment, particularly burger and pizza outlets, continues to demonstrate resilience and growth due to its affordability and convenience. As the economy recovers and consumer confidence strengthens, the overall market penetration of the food service sector is anticipated to deepen, creating substantial opportunities for both established brands and emerging players. The projected CAGR of xx% for the forecast period (2025-2033) underscores the sector's immense growth potential.

Dominant Regions, Countries, or Segments in Australia Food Service Industry

The Quick Service Restaurant (QSR) segment, particularly the burger and pizza sub-segments, is a dominant force driving growth within the Australian food service industry. This dominance is attributed to several key factors, including consistent consumer demand for fast, affordable, and convenient meal options, making them highly resilient across economic fluctuations. Furthermore, chained outlets within the QSR sector leverage economies of scale in purchasing, marketing, and operations, allowing for competitive pricing and widespread brand recognition. Leading QSR companies like McDonald's Corporation, Hungry Jack's (owned by Competitive Foods Australia), and Domino's Pizza Enterprises Ltd have established extensive networks of outlets, particularly in high-traffic retail and standalone locations, ensuring accessibility for a broad consumer base. The ease of expansion for these chained outlets, coupled with their ability to adapt menus to local tastes, further solidifies their market leadership.

Within Full Service Restaurants (FSR), Asian and European cuisines continue to capture significant market share. The multicultural fabric of Australia fuels a strong demand for diverse culinary experiences. Established brands like Guzman y Gomez (Mexican, Latin American) and smaller, independent establishments specializing in various Asian and European dishes contribute significantly to the FSR market's vibrancy. The cafes & bars segment, encompassing bars & pubs, juice/smoothie/desserts bars, and specialist coffee & tea shops, also demonstrates robust growth. The increasing popularity of specialized coffee culture and the demand for healthy beverage options are key drivers for juice bars and dessert cafes. The leisure and travel locations are crucial for the growth of this segment, catering to tourists and locals seeking refreshment and relaxation.

The rise of cloud kitchens represents a rapidly emerging segment, driven by the proliferation of food delivery services. While currently a smaller portion of the overall market, its growth potential is immense, offering lower overheads for operators and increased convenience for consumers. Locations such as retail centres and standalone sites are increasingly being repurposed or utilized for these delivery-focused operations. The strong performance across these diverse segments, bolstered by strategic investments and an understanding of evolving consumer lifestyles, positions the Australian food service industry for continued and widespread expansion.

- Quick Service Restaurants (QSR): Dominant due to affordability, convenience, and widespread adoption of chained outlets.

- Burger & Pizza: Perennial favorites with strong brand loyalty and consistent demand.

- Chained Outlets: Benefit from economies of scale, marketing power, and standardized operations.

- Retail & Standalone Locations: High visibility and accessibility contribute to high foot traffic.

- Full Service Restaurants (FSR): Driven by Australia's multiculturalism and demand for diverse dining experiences.

- Asian & European Cuisines: Consistently popular with a broad demographic.

- Latin American (e.g., Guzman y Gomez): Rapidly growing segment reflecting international food trends.

- Cafes & Bars: Experiential consumption and niche offerings fuel growth.

- Specialist Coffee & Tea Shops: Growing demand for premium and unique beverage experiences.

- Juice/Smoothie/Desserts Bars: Capitalizing on health and wellness trends.

- Leisure & Travel Locations: Key for catering to tourist and entertainment-driven consumption.

- Cloud Kitchens: Emerging segment with high growth potential driven by delivery services.

- Operational Efficiency: Lower overheads and focus on delivery logistics.

Australia Food Service Industry Product Landscape

The Australian food service industry is witnessing a surge in product innovation driven by a desire for healthier, more sustainable, and diverse culinary options. From the introduction of innovative plant-based alternatives to the utilization of locally sourced ingredients, product development is a key differentiator. Unique selling propositions often revolve around unique flavor profiles, allergen-friendly options, and ethically sourced produce. Technological advancements are enabling new cooking techniques and ingredient preparations, enhancing the quality and appeal of dishes. For instance, advancements in sous-vide cooking and rapid chilling technologies are improving food consistency and safety. The market is also seeing a rise in ready-to-eat gourmet meals and meal kits, catering to the increasing demand for convenience without compromising on quality.

Key Drivers, Barriers & Challenges in Australia Food Service Industry

Key Drivers:

- Evolving Consumer Preferences: Growing demand for healthier, plant-based, and ethically sourced food options.

- Technological Advancements: Integration of delivery apps, online ordering systems, and kitchen automation for enhanced efficiency.

- Disposable Income & Economic Growth: Increased consumer spending power supports dining out and food service consumption.

- Tourism Influx: International and domestic tourism drives demand for diverse culinary experiences.

- Innovation in Food Delivery: Expansion of ghost kitchens and third-party delivery services enhancing accessibility.

Barriers & Challenges:

- Labor Shortages & Costs: Difficulty in recruiting and retaining skilled staff, coupled with rising wage pressures.

- Supply Chain Disruptions: Volatility in ingredient prices and availability due to global events and climate change.

- Intense Competition: High market saturation leading to price wars and the need for constant differentiation.

- Regulatory Compliance: Navigating complex food safety regulations, licensing, and environmental standards.

- Rising Operating Costs: Increasing expenses for rent, utilities, and ingredients impacting profit margins.

- Changing Consumer Lifestyles: The shift towards home cooking and meal kits poses a challenge to traditional dine-in models.

Emerging Opportunities in Australia Food Service Industry

Emerging opportunities in the Australian food service industry lie in catering to niche markets and embracing sustainable practices. The growing demand for plant-based and vegan offerings presents a significant untapped market. Furthermore, hyper-local sourcing and farm-to-table concepts are gaining traction, appealing to environmentally conscious consumers. The expansion of cloud kitchens dedicated to specific cuisines or dietary needs offers a low-overhead entry point for new ventures. Innovative applications of technology, such as personalized loyalty programs and AI-driven menu recommendations, can enhance customer engagement and retention. The rise of functional foods and beverages, addressing specific health and wellness needs, also represents a promising area for product development.

Growth Accelerators in the Australia Food Service Industry Industry

Several growth accelerators are propelling the Australian food service industry forward. Technological breakthroughs in food preparation and delivery are enhancing operational efficiency and customer convenience. Strategic partnerships between food businesses and technology providers, for instance, the collaboration between KFC Australia and drone service provider Wing for delivery pilots, are revolutionizing service models. Market expansion strategies, including franchising and international diversification, are enabling established brands to reach new consumer bases. The increasing adoption of sustainable practices, from waste reduction to ethical sourcing, is not only meeting consumer demand but also creating operational efficiencies and enhancing brand reputation, acting as a significant long-term growth catalyst.

Key Players Shaping the Australia Food Service Industry Market

- McDonald's Corporation

- Yum! Brands Inc.

- Inspire Brands Inc.

- Jab Holding Company S À R L

- Craveable Brands

- Doctor's Associate Inc

- Nando's Group Holdings Limited

- PubCo Group

- Zambrero Pty Lt

- Retail Food Group

- Domino's Pizza Enterprises Ltd

- Guzman Y Gomez Restaurant Group Pty Limited

- Starbucks Corporation

- Pacific Hunter Group Pty Ltd

- Ribs and Burgers

- Bloomin' Brands Inc

- Competitive Foods Australia

Notable Milestones in Australia Food Service Industry Sector

- April 2023: Subway added the Bizarre Creme Egg Sandwich to its subs range, a unique product innovation combining chocolate creme egg stuffed in Italian bread, generating significant consumer interest and media attention.

- January 2023: Zambrero announced its partnership with Cronulla Sharks and SurfAid for 2023, demonstrating a commitment to community engagement and corporate social responsibility, enhancing brand visibility and goodwill.

- December 2022: KFC Australia teamed up with drone service provider, Wing, to pilot a delivery service of hot and fresh menu items in Australia. This initiative aimed to explore innovative delivery solutions, potentially reducing delivery times and expanding reach, thus improving customer convenience.

In-Depth Australia Food Service Industry Market Outlook

The future outlook for the Australia food service industry is exceptionally bright, fueled by a confluence of accelerating factors. Continued technological integration, particularly in AI-powered customer service and advanced delivery logistics, will redefine operational efficiency and customer engagement. Strategic alliances and expansion efforts by key players will broaden market reach and diversify offerings. The persistent consumer shift towards sustainable and ethically produced food will create significant opportunities for businesses that prioritize these values. Furthermore, the ongoing evolution of dining habits, with an increasing appetite for diverse and experiential culinary journeys, will ensure a dynamic and growing market. The industry is poised for sustained growth, driven by innovation, strategic foresight, and an unwavering ability to adapt to the ever-changing consumer landscape, presenting substantial market potential and lucrative strategic opportunities for stakeholders.

Australia Food Service Industry Segmentation

-

1. Foodservice Type

-

1.1. Cafes & Bars

-

1.1.1. By Cuisine

- 1.1.1.1. Bars & Pubs

- 1.1.1.2. Juice/Smoothie/Desserts Bars

- 1.1.1.3. Specialist Coffee & Tea Shops

-

1.1.1. By Cuisine

- 1.2. Cloud Kitchen

-

1.3. Full Service Restaurants

- 1.3.1. Asian

- 1.3.2. European

- 1.3.3. Latin American

- 1.3.4. Middle Eastern

- 1.3.5. North American

- 1.3.6. Other FSR Cuisines

-

1.4. Quick Service Restaurants

- 1.4.1. Bakeries

- 1.4.2. Burger

- 1.4.3. Ice Cream

- 1.4.4. Meat-based Cuisines

- 1.4.5. Pizza

- 1.4.6. Other QSR Cuisines

-

1.1. Cafes & Bars

-

2. Outlet

- 2.1. Chained Outlets

- 2.2. Independent Outlets

-

3. Location

- 3.1. Leisure

- 3.2. Lodging

- 3.3. Retail

- 3.4. Standalone

- 3.5. Travel

Australia Food Service Industry Segmentation By Geography

- 1. Australia

Australia Food Service Industry Regional Market Share

Geographic Coverage of Australia Food Service Industry

Australia Food Service Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Foodservice Type

- 5.1.1. Cafes & Bars

- 5.1.1.1. By Cuisine

- 5.1.1.1.1. Bars & Pubs

- 5.1.1.1.2. Juice/Smoothie/Desserts Bars

- 5.1.1.1.3. Specialist Coffee & Tea Shops

- 5.1.1.1. By Cuisine

- 5.1.2. Cloud Kitchen

- 5.1.3. Full Service Restaurants

- 5.1.3.1. Asian

- 5.1.3.2. European

- 5.1.3.3. Latin American

- 5.1.3.4. Middle Eastern

- 5.1.3.5. North American

- 5.1.3.6. Other FSR Cuisines

- 5.1.4. Quick Service Restaurants

- 5.1.4.1. Bakeries

- 5.1.4.2. Burger

- 5.1.4.3. Ice Cream

- 5.1.4.4. Meat-based Cuisines

- 5.1.4.5. Pizza

- 5.1.4.6. Other QSR Cuisines

- 5.1.1. Cafes & Bars

- 5.2. Market Analysis, Insights and Forecast - by Outlet

- 5.2.1. Chained Outlets

- 5.2.2. Independent Outlets

- 5.3. Market Analysis, Insights and Forecast - by Location

- 5.3.1. Leisure

- 5.3.2. Lodging

- 5.3.3. Retail

- 5.3.4. Standalone

- 5.3.5. Travel

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Australia

- 5.1. Market Analysis, Insights and Forecast - by Foodservice Type

- 6. Australia Food Service Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Foodservice Type

- 6.1.1. Cafes & Bars

- 6.1.1.1. By Cuisine

- 6.1.1.1.1. Bars & Pubs

- 6.1.1.1.2. Juice/Smoothie/Desserts Bars

- 6.1.1.1.3. Specialist Coffee & Tea Shops

- 6.1.1.1. By Cuisine

- 6.1.2. Cloud Kitchen

- 6.1.3. Full Service Restaurants

- 6.1.3.1. Asian

- 6.1.3.2. European

- 6.1.3.3. Latin American

- 6.1.3.4. Middle Eastern

- 6.1.3.5. North American

- 6.1.3.6. Other FSR Cuisines

- 6.1.4. Quick Service Restaurants

- 6.1.4.1. Bakeries

- 6.1.4.2. Burger

- 6.1.4.3. Ice Cream

- 6.1.4.4. Meat-based Cuisines

- 6.1.4.5. Pizza

- 6.1.4.6. Other QSR Cuisines

- 6.1.1. Cafes & Bars

- 6.2. Market Analysis, Insights and Forecast - by Outlet

- 6.2.1. Chained Outlets

- 6.2.2. Independent Outlets

- 6.3. Market Analysis, Insights and Forecast - by Location

- 6.3.1. Leisure

- 6.3.2. Lodging

- 6.3.3. Retail

- 6.3.4. Standalone

- 6.3.5. Travel

- 6.1. Market Analysis, Insights and Forecast - by Foodservice Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Yum! Brands Inc

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Craveable Brands

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Jab Holding Company S À R L

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Inspire Brands Inc

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Nando's Group Holdings Limited

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Doctor's Associate Inc

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 PubCo Group

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Zambrero Pty Lt

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Retail Food Group

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Domino's Pizza Enterprises Ltd

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Guzman Y Gomez Restaurant Group Pty Limited

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Starbucks Corporation

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 Pacific Hunter Group Pty Ltd

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.14 Ribs and Burgers

- 7.1.14.1. Company Overview

- 7.1.14.2. Products

- 7.1.14.3. Company Financials

- 7.1.14.4. SWOT Analysis

- 7.1.15 McDonald's Corporation

- 7.1.15.1. Company Overview

- 7.1.15.2. Products

- 7.1.15.3. Company Financials

- 7.1.15.4. SWOT Analysis

- 7.1.16 Competitive Foods Australia

- 7.1.16.1. Company Overview

- 7.1.16.2. Products

- 7.1.16.3. Company Financials

- 7.1.16.4. SWOT Analysis

- 7.1.17 Bloomin' Brands Inc

- 7.1.17.1. Company Overview

- 7.1.17.2. Products

- 7.1.17.3. Company Financials

- 7.1.17.4. SWOT Analysis

- 7.1.1 Yum! Brands Inc

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Australia Food Service Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Australia Food Service Industry Share (%) by Company 2025

List of Tables

- Table 1: Australia Food Service Industry Revenue billion Forecast, by Foodservice Type 2020 & 2033

- Table 2: Australia Food Service Industry Revenue billion Forecast, by Outlet 2020 & 2033

- Table 3: Australia Food Service Industry Revenue billion Forecast, by Location 2020 & 2033

- Table 4: Australia Food Service Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 5: Australia Food Service Industry Revenue billion Forecast, by Foodservice Type 2020 & 2033

- Table 6: Australia Food Service Industry Revenue billion Forecast, by Outlet 2020 & 2033

- Table 7: Australia Food Service Industry Revenue billion Forecast, by Location 2020 & 2033

- Table 8: Australia Food Service Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Australia Food Service Industry?

The projected CAGR is approximately 8.2%.

2. Which companies are prominent players in the Australia Food Service Industry?

Key companies in the market include Yum! Brands Inc, Craveable Brands, Jab Holding Company S À R L, Inspire Brands Inc, Nando's Group Holdings Limited, Doctor's Associate Inc, PubCo Group, Zambrero Pty Lt, Retail Food Group, Domino's Pizza Enterprises Ltd, Guzman Y Gomez Restaurant Group Pty Limited, Starbucks Corporation, Pacific Hunter Group Pty Ltd, Ribs and Burgers, McDonald's Corporation, Competitive Foods Australia, Bloomin' Brands Inc.

3. What are the main segments of the Australia Food Service Industry?

The market segments include Foodservice Type, Outlet, Location.

4. Can you provide details about the market size?

The market size is estimated to be USD 26.2 billion as of 2022.

5. What are some drivers contributing to market growth?

Growing Inclination Towards Vegan/Plant-based Protein Sources; Increasing Demand for Functional Protein Beverages.

6. What are the notable trends driving market growth?

The number if restaurant visits per month grew as a result of the national spread of fast food companies..

7. Are there any restraints impacting market growth?

Competition from Substitute Products.

8. Can you provide examples of recent developments in the market?

April 2023: Subway added the latest item in its subs range, the Bizarre Creme Egg Sandwich, a combination of chocolate creme egg stuffed in Italian bread.January 2023: Zambrero announced its partnership with Cronulla Sharks and SurfAid for 2023.December 2022: KFC Australia teamed up with drone service provider, Wing, to pilot a delivery service of hot and fresh menu items in Australia to provide more convenience to customers.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Australia Food Service Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Australia Food Service Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Australia Food Service Industry?

To stay informed about further developments, trends, and reports in the Australia Food Service Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence