Key Insights

The North American automotive camera market is set for substantial growth, propelled by the increasing integration of Advanced Driver-Assistance Systems (ADAS) and continuous advancements in vehicle safety and convenience. The market is projected to reach $8.4 billion by 2025, with a Compound Annual Growth Rate (CAGR) of over 9% from 2025 to 2033. This expansion is driven by consumer demand for enhanced safety features like automatic emergency braking and lane keeping assist, which heavily depend on sophisticated camera systems. Regulatory initiatives promoting vehicle safety are further accelerating the adoption of these technologies across all vehicle types. The market is also seeing increased deployment of sensing cameras for environmental perception and drive cameras for in-cabin monitoring, highlighting the critical role of automotive cameras in modern vehicles.

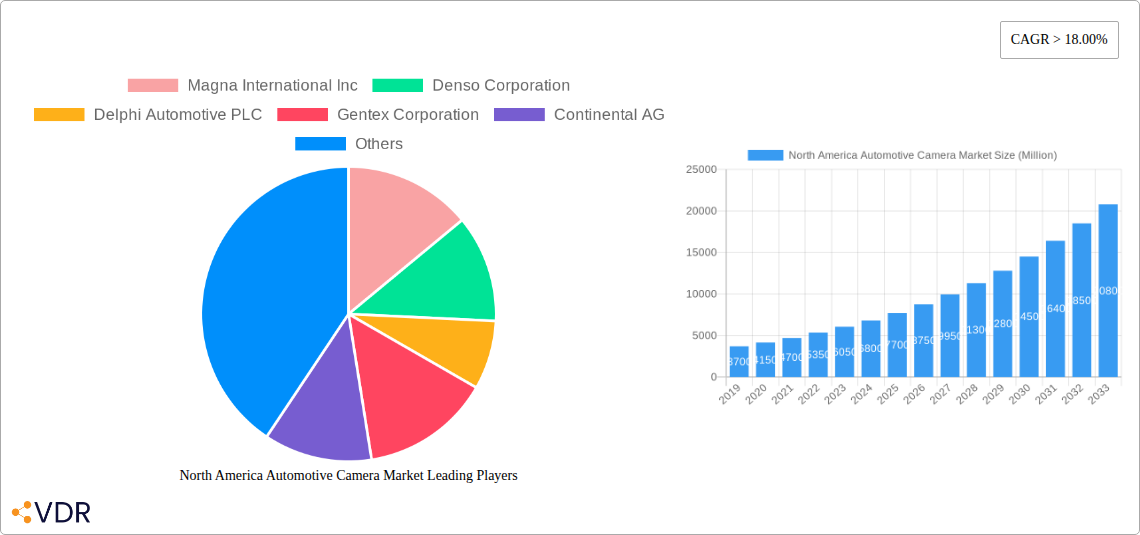

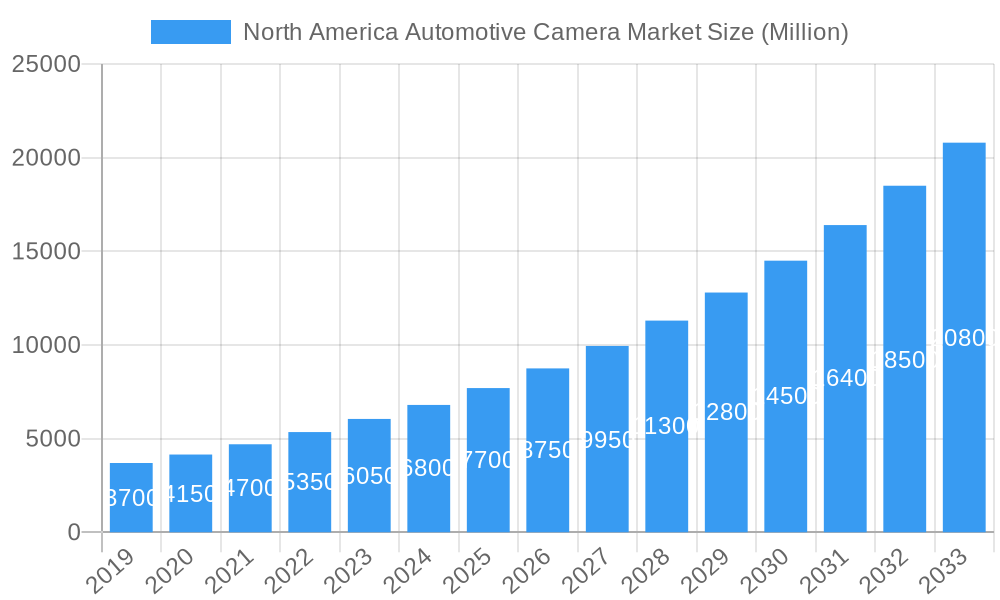

North America Automotive Camera Market Market Size (In Billion)

Key players in the North American automotive camera market include Magna International Inc., Denso Corporation, Delphi Automotive PLC, Gentex Corporation, Continental AG, Valeo SA, Hella KGaA Hueck & Co, Robert Bosch GmbH, Panasonic Corporation, and ZF Friedrichshafen AG. These companies are focusing on R&D to innovate camera solutions for autonomous driving, driver monitoring, and parking assistance. Dominant market trends include camera component miniaturization, advanced image processing, AI/ML integration for object recognition, and demand for high-resolution, low-light cameras. Potential challenges include the cost of advanced camera systems, extensive validation requirements, and cybersecurity concerns. The United States, Canada, and Mexico are the leading markets in North America, each with unique adoption patterns and technological preferences.

North America Automotive Camera Market Company Market Share

North America Automotive Camera Market Report: Comprehensive Analysis and Future Outlook (2019-2033)

This comprehensive report provides an in-depth analysis of the North America automotive camera market, exploring its dynamics, growth trends, regional dominance, product landscape, and key players. With a focus on high-traffic keywords and a structured format, this report is designed to maximize search engine visibility and deliver actionable insights to industry professionals. The study covers the historical period from 2019 to 2024, the base and estimated year of 2025, and forecasts growth through 2033, presenting all values in Million units.

North America Automotive Camera Market Market Dynamics & Structure

The North America automotive camera market is characterized by moderate concentration, with a few key players holding significant market share. Technological innovation serves as a primary driver, fueled by the relentless pursuit of advanced driver-assistance systems (ADAS) and autonomous driving capabilities. Robust regulatory frameworks, mandating safety features like backup cameras and electronic stability control, further bolster market expansion. While competitive product substitutes exist, such as radar and lidar, the cost-effectiveness and versatility of cameras for a wide range of applications continue to solidify their position. End-user demographics are increasingly favoring vehicles equipped with sophisticated camera systems due to growing awareness of safety and convenience features. Mergers and acquisitions (M&A) play a crucial role in market consolidation and technology integration.

- Market Concentration: Dominated by a few Tier-1 automotive suppliers and camera manufacturers.

- Technological Innovation Drivers: Advancements in image processing, sensor technology, AI, and machine learning for object detection and recognition.

- Regulatory Frameworks: Mandates for rearview cameras, advanced emergency braking systems, and increasing focus on ADAS features by NHTSA.

- Competitive Product Substitutes: Radar, lidar, and ultrasonic sensors, though cameras offer unique visual data.

- End-User Demographics: Growing demand for safety, convenience, and advanced features across various vehicle segments.

- M&A Trends: Strategic acquisitions to gain access to specialized technologies, expand product portfolios, and enhance market presence. For instance, an estimated 5-10 M&A deals are anticipated annually within the broader automotive electronics sector, with a portion directly impacting camera suppliers.

North America Automotive Camera Market Growth Trends & Insights

The North America automotive camera market is poised for substantial growth, driven by the escalating adoption of ADAS and the progressive march towards autonomous vehicles. The market size, valued at approximately 3,500 million units in 2025, is projected to witness a Compound Annual Growth Rate (CAGR) of around 8.5% during the forecast period of 2025–2033. This impressive expansion is underpinned by several critical trends. The increasing consumer demand for enhanced vehicle safety, coupled with stringent government regulations, is a primary catalyst. Features like forward-collision warning, lane-keeping assist, and pedestrian detection are becoming standard in new vehicle models, directly boosting the demand for drive cameras and sensing cameras.

Technological disruptions, particularly in sensor miniaturization, improved image resolution, and enhanced low-light performance, are making automotive cameras more capable and cost-effective. This allows for the integration of more advanced camera systems, including surround-view cameras and in-cabin monitoring systems, further broadening the application spectrum. Consumer behavior is also shifting, with a greater appreciation for the convenience and security offered by parking assist cameras and 360-degree camera systems. As vehicle electrification accelerates, there's a concurrent push for smarter vehicle technologies, where cameras play a pivotal role in everything from battery management to driver monitoring. The evolution of the automotive ecosystem towards connected and intelligent mobility solutions directly translates to increased reliance on robust camera systems. By 2033, the penetration of advanced camera systems in new vehicles is expected to exceed 80 million units annually.

Dominant Regions, Countries, or Segments in North America Automotive Camera Market

Within the North America automotive camera market, the United States stands out as the dominant country, driven by its large automotive manufacturing base, significant consumer demand for advanced vehicle technologies, and a proactive regulatory environment that encourages the adoption of safety features. The ADAS segment is the primary growth engine, accounting for an estimated 60% of the total market value in 2025. This dominance is fueled by increasing safety mandates, consumer preference for semi-autonomous driving capabilities, and the ongoing development of more sophisticated ADAS features that rely heavily on camera data.

The "Drive Camera" sub-segment within the Type category is also exhibiting robust growth, encompassing forward-facing cameras used for ADAS functions like lane departure warning, traffic sign recognition, and adaptive cruise control. This segment is projected to reach over 25 million units in 2025. The "Parking" application type, including rearview cameras and surround-view systems, continues to be a significant contributor, driven by the need for enhanced maneuverability and safety in urban environments. The market penetration for rearview cameras is already high, but the adoption of multi-camera parking assist systems is rapidly increasing.

- Dominant Country: United States, with its substantial automotive production and consumption.

- Leading Segment (Application Type): ADAS, driven by safety regulations and consumer demand for semi-autonomous features.

- Key Drivers for ADAS Dominance:

- NHTSA's New Car Assessment Program (NCAP) encouraging advanced safety features.

- Increasing consumer awareness and willingness to pay for safety technologies.

- Technological advancements enabling more sophisticated ADAS functionalities.

- Strong Performing Segment (Type): Drive Camera, critical for forward-facing ADAS applications.

- Growth in Parking Segment: Driven by increasing urbanization and the demand for ease of vehicle maneuvering.

- Market Share Snapshot (Estimated 2025): ADAS Applications: ~60%, Parking Applications: ~30%, Other Applications: ~10%.

- Growth Potential: Continued innovation in sensor fusion and AI algorithms for ADAS will sustain high growth.

North America Automotive Camera Market Product Landscape

The North America automotive camera market showcases a dynamic product landscape characterized by continuous innovation in sensor technology, image processing, and integration capabilities. Manufacturers are focusing on developing high-resolution cameras with enhanced low-light performance, wider dynamic range, and superior temperature resilience. Key product innovations include AI-powered vision systems capable of real-time object detection, classification, and tracking, crucial for advanced ADAS functionalities. Furthermore, the integration of cameras with other sensors, such as radar and lidar, is leading to more robust and redundant perception systems. Unique selling propositions often revolve around miniaturization, power efficiency, and robust environmental sealing to withstand demanding automotive conditions. The performance metrics are increasingly measured by frames per second, resolution, field of view, and accuracy in diverse weather and lighting scenarios.

Key Drivers, Barriers & Challenges in North America Automotive Camera Market

Key Drivers:

- Mandatory Safety Regulations: Government mandates for rearview cameras and evolving ADAS safety requirements are primary growth drivers.

- Advancements in ADAS and Autonomous Driving: The continuous development and adoption of sophisticated ADAS features and the pursuit of autonomous driving technology necessitate advanced camera systems.

- Increasing Consumer Demand for Safety and Convenience: Buyers are increasingly prioritizing vehicles equipped with advanced safety features and driver convenience technologies.

- Technological Innovation: Ongoing improvements in sensor technology, image processing, and AI algorithms are making cameras more capable and cost-effective.

Key Barriers & Challenges:

- High Development and Integration Costs: The research, development, and integration of complex camera systems into vehicles can be substantial.

- Supply Chain Disruptions: Geopolitical events, natural disasters, and component shortages can disrupt the supply of critical camera components.

- Cybersecurity Concerns: The increasing connectivity of vehicles raises concerns about the cybersecurity of camera systems and the data they collect.

- Harsh Environmental Conditions: Cameras must perform reliably under extreme temperatures, humidity, and vibration, requiring robust engineering and materials.

- Intensifying Competition: The market is highly competitive, with pressure on pricing and margins from both established players and new entrants.

Emerging Opportunities in North America Automotive Camera Market

Emerging opportunities in the North America automotive camera market lie in the increasing demand for in-cabin monitoring systems for driver attentiveness and passenger safety. The growth of the commercial vehicle sector, with its unique safety requirements and the need for enhanced visibility, presents another significant avenue. Furthermore, the development of specialized cameras for electric vehicles (EVs), such as those for battery health monitoring and thermal imaging, offers a niche yet growing market. The integration of cameras with augmented reality (AR) displays for advanced navigation and driver information is also an exciting frontier. Finally, the increasing adoption of camera-based solutions for vehicle-to-everything (V2X) communication further expands the application landscape and market potential.

Growth Accelerators in the North America Automotive Camera Market Industry

Several key catalysts are accelerating the growth of the North America automotive camera market. The ongoing technological breakthroughs in artificial intelligence and machine learning are enabling cameras to perform more complex tasks, moving beyond simple object recognition to nuanced environmental understanding. Strategic partnerships between automotive manufacturers, Tier-1 suppliers, and technology companies are fostering rapid innovation and product development. Market expansion strategies, including the penetration of camera systems into lower-cost vehicle segments and the development of more affordable yet capable solutions, are broadening the addressable market. The continuous push for higher levels of vehicle autonomy, even if gradual, directly translates into a demand for more advanced and redundant camera systems.

Key Players Shaping the North America Automotive Camera Market Market

- Magna International Inc.

- Denso Corporation

- Delphi Automotive PLC

- Gentex Corporation

- Continental AG

- Valeo SA

- Hella KGaA Hueck & Co.

- Robert Bosch GmbH

- Panasonic Corporation

- ZF Friedrichshafen AG

Notable Milestones in North America Automotive Camera Market Sector

- 2019: Increased adoption of standard rearview cameras mandated in the US.

- 2020: Introduction of advanced camera-based ADAS features in mainstream vehicle models.

- 2021: Significant advancements in AI algorithms for object detection and tracking in challenging conditions.

- 2022: Growing interest and investment in in-cabin camera systems for driver monitoring.

- 2023: Enhanced sensor fusion technologies combining camera data with radar and lidar for improved ADAS performance.

- 2024: Focus on high-resolution, automotive-grade cameras with improved low-light capabilities.

In-Depth North America Automotive Camera Market Market Outlook

The future outlook for the North America automotive camera market is exceptionally promising, driven by the relentless pursuit of enhanced vehicle safety and the inevitable progression towards autonomous driving. Growth accelerators such as continuous advancements in AI-powered perception systems, strategic collaborations between key industry players, and the expansion of camera applications into new vehicle segments are set to define the market's trajectory. The increasing integration of camera technology within the broader intelligent transportation ecosystem, coupled with evolving consumer preferences for sophisticated vehicle features, will further solidify the market's robust growth potential. Strategic opportunities lie in developing specialized camera solutions for electric vehicles, commercial fleets, and the nascent in-cabin sensing market.

North America Automotive Camera Market Segmentation

-

1. Type

- 1.1. Drive Camera

- 1.2. Sensing Camera

-

2. Application Type

- 2.1. ADAS

- 2.2. Parking

North America Automotive Camera Market Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

North America Automotive Camera Market Regional Market Share

Geographic Coverage of North America Automotive Camera Market

North America Automotive Camera Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Drive Camera

- 5.1.2. Sensing Camera

- 5.2. Market Analysis, Insights and Forecast - by Application Type

- 5.2.1. ADAS

- 5.2.2. Parking

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. North America Automotive Camera Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Drive Camera

- 6.1.2. Sensing Camera

- 6.2. Market Analysis, Insights and Forecast - by Application Type

- 6.2.1. ADAS

- 6.2.2. Parking

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Magna International Inc

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Denso Corporation

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Delphi Automotive PLC

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Gentex Corporation

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Continental AG

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Valeo SA

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Hella KGaA Hueck & Co

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Robert Bosch Gmb

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Panasonic Corporation

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 ZF Friedrichshafen AG

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Magna International Inc

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: North America Automotive Camera Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: North America Automotive Camera Market Share (%) by Company 2025

List of Tables

- Table 1: North America Automotive Camera Market Revenue billion Forecast, by Type 2020 & 2033

- Table 2: North America Automotive Camera Market Revenue billion Forecast, by Application Type 2020 & 2033

- Table 3: North America Automotive Camera Market Revenue billion Forecast, by Region 2020 & 2033

- Table 4: North America Automotive Camera Market Revenue billion Forecast, by Type 2020 & 2033

- Table 5: North America Automotive Camera Market Revenue billion Forecast, by Application Type 2020 & 2033

- Table 6: North America Automotive Camera Market Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States North America Automotive Camera Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada North America Automotive Camera Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico North America Automotive Camera Market Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Automotive Camera Market?

The projected CAGR is approximately 9%.

2. Which companies are prominent players in the North America Automotive Camera Market?

Key companies in the market include Magna International Inc, Denso Corporation, Delphi Automotive PLC, Gentex Corporation, Continental AG, Valeo SA, Hella KGaA Hueck & Co, Robert Bosch Gmb, Panasonic Corporation, ZF Friedrichshafen AG.

3. What are the main segments of the North America Automotive Camera Market?

The market segments include Type, Application Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 8.4 billion as of 2022.

5. What are some drivers contributing to market growth?

Growing Emphasis On Improving Vehicle Safety; Advancements in Camera Technologies; Others.

6. What are the notable trends driving market growth?

ADAS application is projected to lead the market.

7. Are there any restraints impacting market growth?

High Cost Of Camera System; Others.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Automotive Camera Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Automotive Camera Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Automotive Camera Market?

To stay informed about further developments, trends, and reports in the North America Automotive Camera Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence