Key Insights

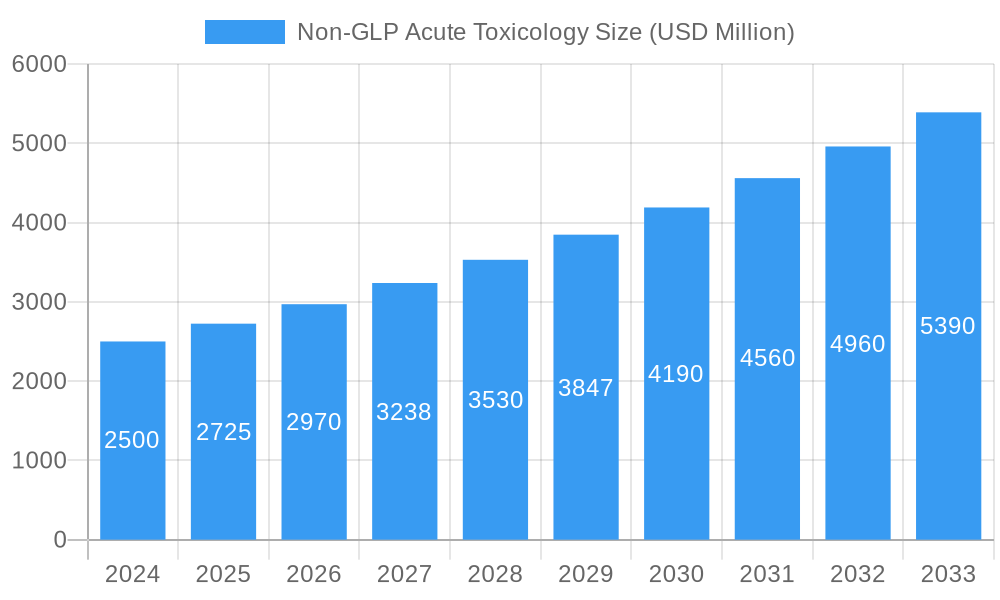

The Non-GLP Acute Toxicology market is poised for significant expansion, projected to reach $2.5 billion in 2024 and grow at a robust CAGR of 9.2% through 2033. This upward trajectory is primarily fueled by an increasing demand for rapid and cost-effective toxicology assessments in the early stages of drug development and product safety testing. Pharmaceutical and biotechnology companies, in particular, are leveraging these services to streamline their R&D pipelines and quickly identify potential safety concerns before committing to more extensive and expensive regulatory studies. The growing emphasis on animal welfare and the drive towards reducing animal testing are also indirect contributors, as Non-GLP studies often serve as a preliminary screening tool, potentially reducing the overall number of animals used in later GLP-compliant testing. Furthermore, the expanding global pharmaceutical industry, coupled with stringent product safety regulations across various sectors like agrochemicals and cosmetics, is creating a continuous need for reliable acute toxicology data, thereby solidifying the market's growth potential.

Non-GLP Acute Toxicology Market Size (In Billion)

The market's growth is further propelled by advancements in testing methodologies, leading to more accurate and efficient Non-GLP acute toxicology evaluations. While the market is characterized by a diverse range of applications, including testing for rodents, canines, and rabbits, the Acute Toxicity Testing segment is expected to remain dominant due to its fundamental role in initial safety assessments. Emerging trends indicate a growing interest in integrating in vitro cytotoxicity testing as a complementary approach, offering a faster and more cost-effective preliminary screen. However, the market also faces certain restraints, such as the increasing scrutiny on the predictive accuracy of Non-GLP data for regulatory submissions and the ongoing ethical debates surrounding animal testing. Nevertheless, the substantial investment in pharmaceutical R&D and the continuous launch of new chemical entities and biologics are expected to outweigh these challenges, ensuring a dynamic and growing Non-GLP Acute Toxicology market.

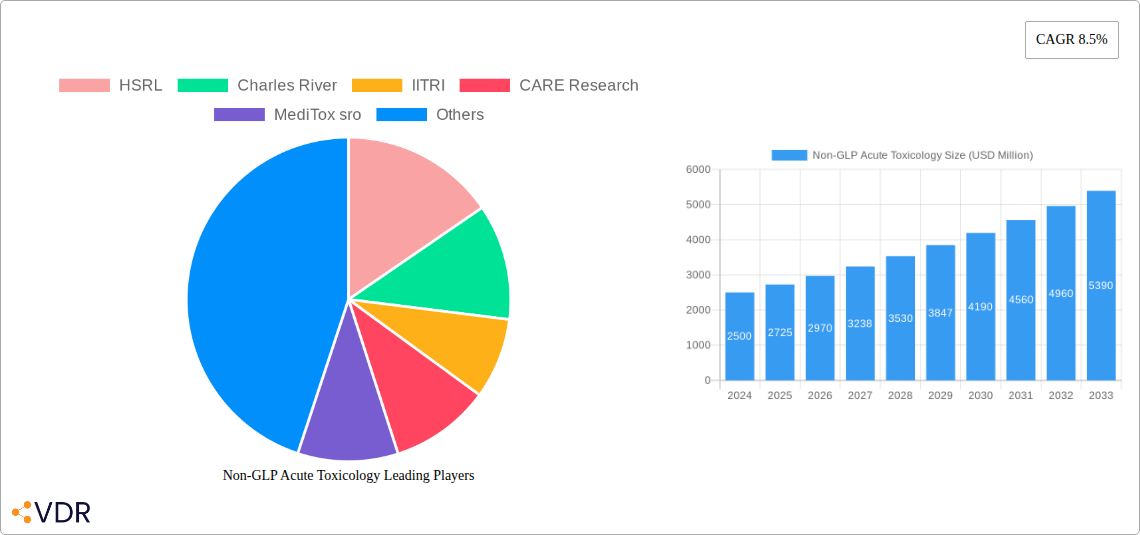

Non-GLP Acute Toxicology Company Market Share

Non-GLP Acute Toxicology Market Report Description

This comprehensive report delves into the intricate landscape of the Non-GLP Acute Toxicology market, providing an in-depth analysis of its dynamics, growth trends, and future outlook. Designed to empower pharmaceutical companies, contract research organizations (CROs), and regulatory bodies, this report offers actionable insights into drug safety testing, pre-clinical toxicology, and in vitro toxicology. We explore the critical role of animal testing alternatives, biocompatibility testing, and chemical safety assessment in shaping the future of drug development.

The report is structured to cater to both the parent market of global toxicology services and the specialized child market of Non-GLP Acute Toxicology. Leveraging extensive historical data from 2019–2024 and a robust forecast period of 2025–2033, with 2025 serving as both the base and estimated year, this research provides a forward-looking perspective on market evolution. We meticulously examine market concentration, technological innovation drivers, evolving regulatory frameworks, competitive product substitutes, end-user demographics, and strategic merger and acquisition (M&A) trends. Quantitative insights, including market share percentages and M&A deal volumes, are integrated with qualitative factors such as innovation barriers to offer a holistic view.

This report is crucial for understanding the projected market size, adoption rates of novel toxicological testing methods, technological disruptions within the industry, and shifts in consumer behavior influencing demand for safer products. With an estimated market size of $4.2 billion in 2025, growing at a Compound Annual Growth Rate (CAGR) of 6.5%, the Non-GLP Acute Toxicology market presents significant opportunities for stakeholders.

Non-GLP Acute Toxicology Market Dynamics & Structure

The Non-GLP Acute Toxicology market exhibits a moderate to high concentration, with leading Contract Research Organizations (CROs) dominating a significant portion of the market share. Technological innovation is a primary driver, fueled by the increasing demand for faster, more cost-effective, and ethically conscious toxicology testing. Advancements in in vitro methods, such as cell-based assays and organ-on-a-chip technology, are progressively complementing and, in some instances, replacing traditional in vivo studies. Regulatory frameworks, while evolving, continue to influence study design and acceptance, with a growing emphasis on New Approach Methodologies (NAMs) and reduced animal use. Competitive product substitutes, primarily in the form of advanced in vitro and in silico models, pose a significant challenge to traditional in vivo testing, particularly for early-stage screening. End-user demographics are increasingly skewed towards pharmaceutical and biotechnology companies, as well as cosmetic and chemical industries seeking efficient safety assessments. M&A trends indicate a consolidation phase, with larger CROs acquiring smaller, specialized service providers to expand their service portfolios and geographical reach.

- Market Concentration: Dominated by key players with an estimated 55% market share held by the top five CROs.

- Technological Innovation Drivers: Rise of in vitro and in silico models, automation in testing, and development of predictive toxicology tools.

- Regulatory Frameworks: Evolving guidelines promoting animal welfare and the adoption of NAMs, impacting study designs.

- Competitive Product Substitutes: Growing efficacy of cell-based assays and high-throughput screening methods reducing reliance on animal models.

- End-User Demographics: Primarily pharmaceutical, biotech, cosmetic, and chemical industries.

- M&A Trends: Strategic acquisitions to enhance capabilities and market presence, with approximately 15 significant deals recorded in the historical period.

Non-GLP Acute Toxicology Growth Trends & Insights

The Non-GLP Acute Toxicology market is poised for substantial growth, driven by an escalating need for comprehensive safety evaluations across diverse industries. The market size is projected to expand from an estimated $4.2 billion in 2025 to reach $7.1 billion by 2033, exhibiting a robust CAGR of 6.5% during the forecast period. This expansion is underpinned by a continuous increase in drug discovery pipelines, the development of novel chemicals, and stringent regulatory demands for product safety. Adoption rates of advanced in vitro toxicology testing are accelerating, as they offer faster turnaround times, reduced costs, and better ethical alignment compared to traditional animal studies. Technological disruptions, including the integration of artificial intelligence (AI) and machine learning (ML) in predicting toxicological outcomes, are further revolutionizing the field. These technologies enable more accurate risk assessments and a deeper understanding of dose-response relationships. Consumer behavior is also playing an instrumental role, with a growing preference for products verified for safety and ethical manufacturing practices, thereby pushing industries to invest more in rigorous toxicology assessments. The market penetration of Non-GLP acute toxicology services is expected to rise, particularly in emerging economies where regulatory landscapes are maturing, and manufacturing sectors are expanding.

The increasing complexity of chemical compounds and biologics necessitates sophisticated acute toxicity evaluations to identify potential hazards early in the development lifecycle. This is especially critical for new chemical entities (NCEs) and biologics entering pre-clinical development. The demand for specialized toxicology services, including those offered under non-GLP conditions for early screening and research purposes, is outpacing the growth of general toxicology services. This niche focus allows for greater flexibility and speed, which are paramount in competitive R&D environments. The strategic imperative for companies to minimize the attrition rate of drug candidates, which is often linked to unforeseen toxicity, further amplifies the importance of reliable acute toxicology data. Furthermore, the growing awareness and implementation of the 3Rs principle (Replacement, Reduction, Refinement) in animal testing are indirectly spurring innovation and adoption of alternative methods within the Non-GLP acute toxicology framework, albeit with a continued reliance on certain in vivo models for specific endpoints. The global health landscape, with its continuous emergence of new diseases and the need for novel therapeutics, also contributes to sustained demand for acute toxicology services.

The market is witnessing a paradigm shift where predictive toxicology is gaining prominence, leveraging advanced computational models and high-throughput screening to forecast potential toxic effects before conducting extensive in vivo studies. This not only optimizes resource allocation but also expedites the drug development process. The increasing outsourcing of toxicology studies by pharmaceutical companies to specialized CROs also acts as a significant growth catalyst, enabling these organizations to focus on their core competencies of drug discovery and development. The expanding scope of applications, from pharmaceuticals and medical devices to agrochemicals and consumer products, broadens the market's reach. The integration of sophisticated data analytics in interpreting toxicology results allows for more nuanced understanding of mechanisms of toxicity and better informed decision-making. The overall trajectory of the Non-GLP Acute Toxicology market is indicative of a dynamic and expanding sector, critical to ensuring the safety and efficacy of a wide array of products that impact human health and the environment.

Dominant Regions, Countries, or Segments in Non-GLP Acute Toxicology

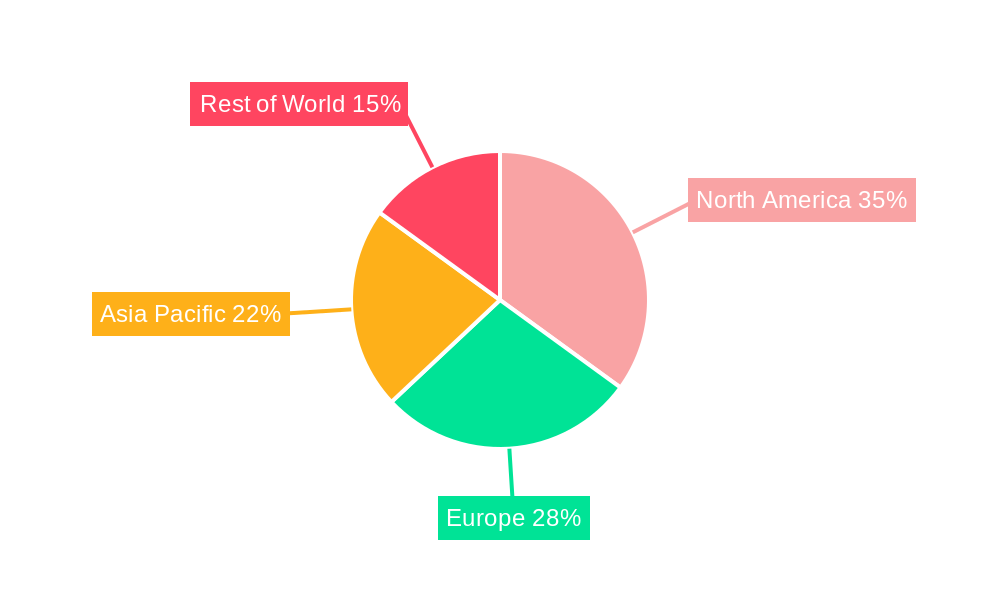

North America currently holds a dominant position in the Non-GLP Acute Toxicology market, driven by a robust pharmaceutical and biotechnology industry, significant R&D investments, and a well-established regulatory framework that encourages early-stage safety testing. The United States, in particular, is a powerhouse, with a high concentration of leading pharmaceutical companies and CROs, contributing approximately 65% of the regional market value. The region's proactive approach to adopting new testing methodologies and its strong emphasis on drug safety and efficacy have cemented its leadership.

Within the Application segment, Rodents continue to be the most dominant, accounting for an estimated 55% of the market share. This is attributed to their physiological similarities to humans, cost-effectiveness, and well-established protocols for acute toxicity studies. However, the growth in demand for Canine and Rabbit studies, particularly for specific drug classes and higher-tier studies, is also noteworthy, with these segments collectively representing around 25% of the application market. The "Others" segment, which includes studies in non-rodent species like primates and various in vitro models, is experiencing the fastest growth, driven by the increasing need for species-specific data and the advancement of alternative testing methods.

In terms of Types, Acute Toxicity Testing remains the largest segment, comprising an estimated 45% of the market. This is due to its foundational role in early drug development and chemical risk assessment. In vitro Cytotoxicity Testing is rapidly gaining traction, with an estimated 30% market share, driven by its efficiency, ethical advantages, and ability to provide mechanistic insights. Genotoxicity Testing, while a smaller segment at an estimated 25%, is crucial for assessing the potential of substances to damage genetic material, making it an indispensable part of safety evaluations.

Economic policies in North America, such as tax incentives for R&D and favorable venture capital funding for biotech startups, further bolster market growth. The sophisticated healthcare infrastructure and high per capita healthcare expenditure also contribute to the demand for advanced drug safety testing. Regulatory bodies like the FDA play a crucial role in setting standards and guidelines, fostering a demand for high-quality toxicology data, even in non-GLP settings for research and early development. The presence of a highly skilled scientific workforce adept at conducting and interpreting complex toxicology studies is another key factor driving dominance.

In conclusion, North America's leadership in the Non-GLP Acute Toxicology market is a multifaceted phenomenon, stemming from its robust industrial base, forward-thinking regulatory environment, and continuous adoption of innovative scientific approaches. While rodents remain central to acute toxicity testing, the rising influence of in vitro and other species-specific studies signals a dynamic evolution within the application and type segments, promising diversified growth opportunities.

Non-GLP Acute Toxicology Product Landscape

The Non-GLP Acute Toxicology product landscape is characterized by a range of sophisticated testing services and innovative methodologies. Companies are offering comprehensive acute oral, dermal, and inhalation toxicity studies designed to rapidly assess the potential hazards of substances. Innovations include the development of high-throughput screening platforms that utilize advanced cell-based assays and automation to accelerate testing cycles and reduce animal usage. Performance metrics are increasingly focused on speed, cost-effectiveness, and the generation of robust, mechanistically informative data. Unique selling propositions often lie in specialized expertise for specific compound classes or regulatory requirements, alongside integrated in vitro and in silico approaches that provide a more holistic safety assessment.

Key Drivers, Barriers & Challenges in Non-GLP Acute Toxicology

Key Drivers:

- Escalating R&D Investments: Pharmaceutical, biotech, and chemical industries are increasing their investment in new product development, necessitating robust safety evaluations.

- Demand for Faster Timelines: The competitive landscape requires accelerated drug development and chemical registration, driving the need for efficient toxicology testing.

- Advancements in Alternative Methods: Development and validation of in vitro and in silico models offer faster, cheaper, and ethically preferable alternatives to traditional animal testing.

- Increasing Regulatory Scrutiny: Global regulatory bodies are continuously refining safety standards, demanding more comprehensive toxicology data.

- Growth in Outsourcing: Pharmaceutical and biotech companies are increasingly outsourcing toxicology studies to specialized CROs to optimize resources and focus on core competencies.

Barriers & Challenges:

- Regulatory Acceptance of Novel Methods: While evolving, the full acceptance and validation of new approach methodologies (NAMs) by all regulatory bodies can be a lengthy process.

- Cost of Advanced Technologies: Investment in cutting-edge in vitro and in silico technologies can be substantial for smaller organizations.

- Complexity of Biological Systems: Mimicking the complexity of in vivo biological responses in in vitro models remains a significant scientific challenge.

- Data Interpretation and Standardization: Ensuring consistency and comparability of data generated from diverse methodologies can be challenging.

- Skilled Workforce Shortage: A need for highly trained scientists proficient in both traditional and novel toxicology techniques exists.

Emerging Opportunities in Non-GLP Acute Toxicology

Emerging opportunities in Non-GLP Acute Toxicology lie in the continued development and validation of New Approach Methodologies (NAMs), particularly organ-on-a-chip technology and advanced computational toxicology. The growing demand for personalized medicine necessitates tailored toxicology assessments for individual patient responses. Furthermore, the expansion of the market into niche sectors like cosmetics, food additives, and industrial chemicals presents significant untapped potential. The increasing global emphasis on environmental safety and sustainability is also creating opportunities for specialized ecotoxicology assessments. Leveraging AI and machine learning for predictive toxicology offers a profound opportunity to streamline safety assessments and reduce experimental burden.

Growth Accelerators in the Non-GLP Acute Toxicology Industry

Several key catalysts are accelerating the growth of the Non-GLP Acute Toxicology industry. Technological breakthroughs in high-throughput screening, automation, and advanced cell culture techniques are significantly enhancing efficiency and data quality. Strategic partnerships between CROs and technology providers are fostering innovation and market penetration of novel solutions. The increasing trend of outsourcing by pharmaceutical and biotech companies to specialized CROs allows for greater focus on R&D, driving demand for reliable toxicology services. Furthermore, market expansion into emerging economies, coupled with their evolving regulatory landscapes, presents substantial growth avenues.

Key Players Shaping the Non-GLP Acute Toxicology Market

- HSRL

- Charles River

- IITRI

- CARE Research

- MediTox sro

- VivoPharm

- Celerion

- Bienta

- Eurofins Scientific

- WuXi AppTec

- Labcorp Drug Development

- PPD, Inc.

- Syngene International Limited

Notable Milestones in Non-GLP Acute Toxicology Sector

- 2019: Increased regulatory focus on New Approach Methodologies (NAMs) adoption globally.

- 2020: Significant investment in AI and ML for predictive toxicology by major CROs.

- 2021: Launch of advanced organ-on-a-chip platforms for simulating human physiology.

- 2022: Growing number of M&A activities as larger CROs acquire specialized service providers.

- 2023: Increased demand for in vitro genotoxicity testing services driven by regulatory pressures.

- 2024: Expansion of services by key players to include comprehensive in silico toxicology assessments.

In-Depth Non-GLP Acute Toxicology Market Outlook

The future of the Non-GLP Acute Toxicology market is exceptionally promising, driven by ongoing technological innovation and evolving regulatory landscapes. Growth accelerators, including the widespread adoption of AI-powered predictive models and advanced in vitro testing platforms, will continue to enhance efficiency and reduce reliance on traditional methods. Strategic collaborations between research institutions and industry players will further drive the development and validation of novel assays. The market's trajectory is set towards greater precision, speed, and ethical considerations in safety assessments, positioning Non-GLP acute toxicology as an indispensable component of modern drug and chemical development.

Non-GLP Acute Toxicology Segmentation

-

1. Application

- 1.1. Rodents

- 1.2. Canine

- 1.3. Rabbit

- 1.4. Others

-

2. Types

- 2.1. Acute Toxicity Testing

- 2.2. In vitro Cytotoxicity Testing

- 2.3. Genotoxicity Testing

Non-GLP Acute Toxicology Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Non-GLP Acute Toxicology Regional Market Share

Geographic Coverage of Non-GLP Acute Toxicology

Non-GLP Acute Toxicology REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Non-GLP Acute Toxicology Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Rodents

- 5.1.2. Canine

- 5.1.3. Rabbit

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Acute Toxicity Testing

- 5.2.2. In vitro Cytotoxicity Testing

- 5.2.3. Genotoxicity Testing

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Non-GLP Acute Toxicology Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Rodents

- 6.1.2. Canine

- 6.1.3. Rabbit

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Acute Toxicity Testing

- 6.2.2. In vitro Cytotoxicity Testing

- 6.2.3. Genotoxicity Testing

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Non-GLP Acute Toxicology Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Rodents

- 7.1.2. Canine

- 7.1.3. Rabbit

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Acute Toxicity Testing

- 7.2.2. In vitro Cytotoxicity Testing

- 7.2.3. Genotoxicity Testing

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Non-GLP Acute Toxicology Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Rodents

- 8.1.2. Canine

- 8.1.3. Rabbit

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Acute Toxicity Testing

- 8.2.2. In vitro Cytotoxicity Testing

- 8.2.3. Genotoxicity Testing

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Non-GLP Acute Toxicology Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Rodents

- 9.1.2. Canine

- 9.1.3. Rabbit

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Acute Toxicity Testing

- 9.2.2. In vitro Cytotoxicity Testing

- 9.2.3. Genotoxicity Testing

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Non-GLP Acute Toxicology Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Rodents

- 10.1.2. Canine

- 10.1.3. Rabbit

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Acute Toxicity Testing

- 10.2.2. In vitro Cytotoxicity Testing

- 10.2.3. Genotoxicity Testing

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 HSRL

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Charles River

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 IITRI

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 CARE Research

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 MediTox sro

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 VivoPharm

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Celerion

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Bienta

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.1 HSRL

List of Figures

- Figure 1: Global Non-GLP Acute Toxicology Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Non-GLP Acute Toxicology Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Non-GLP Acute Toxicology Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Non-GLP Acute Toxicology Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Non-GLP Acute Toxicology Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Non-GLP Acute Toxicology Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Non-GLP Acute Toxicology Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Non-GLP Acute Toxicology Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Non-GLP Acute Toxicology Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Non-GLP Acute Toxicology Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Non-GLP Acute Toxicology Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Non-GLP Acute Toxicology Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Non-GLP Acute Toxicology Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Non-GLP Acute Toxicology Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Non-GLP Acute Toxicology Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Non-GLP Acute Toxicology Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Non-GLP Acute Toxicology Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Non-GLP Acute Toxicology Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Non-GLP Acute Toxicology Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Non-GLP Acute Toxicology Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Non-GLP Acute Toxicology Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Non-GLP Acute Toxicology Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Non-GLP Acute Toxicology Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Non-GLP Acute Toxicology Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Non-GLP Acute Toxicology Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Non-GLP Acute Toxicology Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Non-GLP Acute Toxicology Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Non-GLP Acute Toxicology Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Non-GLP Acute Toxicology Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Non-GLP Acute Toxicology Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Non-GLP Acute Toxicology Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Non-GLP Acute Toxicology Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Non-GLP Acute Toxicology Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Non-GLP Acute Toxicology Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Non-GLP Acute Toxicology Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Non-GLP Acute Toxicology Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Non-GLP Acute Toxicology Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Non-GLP Acute Toxicology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Non-GLP Acute Toxicology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Non-GLP Acute Toxicology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Non-GLP Acute Toxicology Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Non-GLP Acute Toxicology Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Non-GLP Acute Toxicology Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Non-GLP Acute Toxicology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Non-GLP Acute Toxicology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Non-GLP Acute Toxicology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Non-GLP Acute Toxicology Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Non-GLP Acute Toxicology Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Non-GLP Acute Toxicology Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Non-GLP Acute Toxicology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Non-GLP Acute Toxicology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Non-GLP Acute Toxicology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Non-GLP Acute Toxicology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Non-GLP Acute Toxicology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Non-GLP Acute Toxicology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Non-GLP Acute Toxicology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Non-GLP Acute Toxicology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Non-GLP Acute Toxicology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Non-GLP Acute Toxicology Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Non-GLP Acute Toxicology Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Non-GLP Acute Toxicology Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Non-GLP Acute Toxicology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Non-GLP Acute Toxicology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Non-GLP Acute Toxicology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Non-GLP Acute Toxicology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Non-GLP Acute Toxicology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Non-GLP Acute Toxicology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Non-GLP Acute Toxicology Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Non-GLP Acute Toxicology Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Non-GLP Acute Toxicology Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Non-GLP Acute Toxicology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Non-GLP Acute Toxicology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Non-GLP Acute Toxicology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Non-GLP Acute Toxicology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Non-GLP Acute Toxicology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Non-GLP Acute Toxicology Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Non-GLP Acute Toxicology Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Non-GLP Acute Toxicology?

The projected CAGR is approximately 8.5%.

2. Which companies are prominent players in the Non-GLP Acute Toxicology?

Key companies in the market include HSRL, Charles River, IITRI, CARE Research, MediTox sro, VivoPharm, Celerion, Bienta.

3. What are the main segments of the Non-GLP Acute Toxicology?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 5600.00, USD 8400.00, and USD 11200.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Non-GLP Acute Toxicology," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Non-GLP Acute Toxicology report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Non-GLP Acute Toxicology?

To stay informed about further developments, trends, and reports in the Non-GLP Acute Toxicology, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence