Key Insights

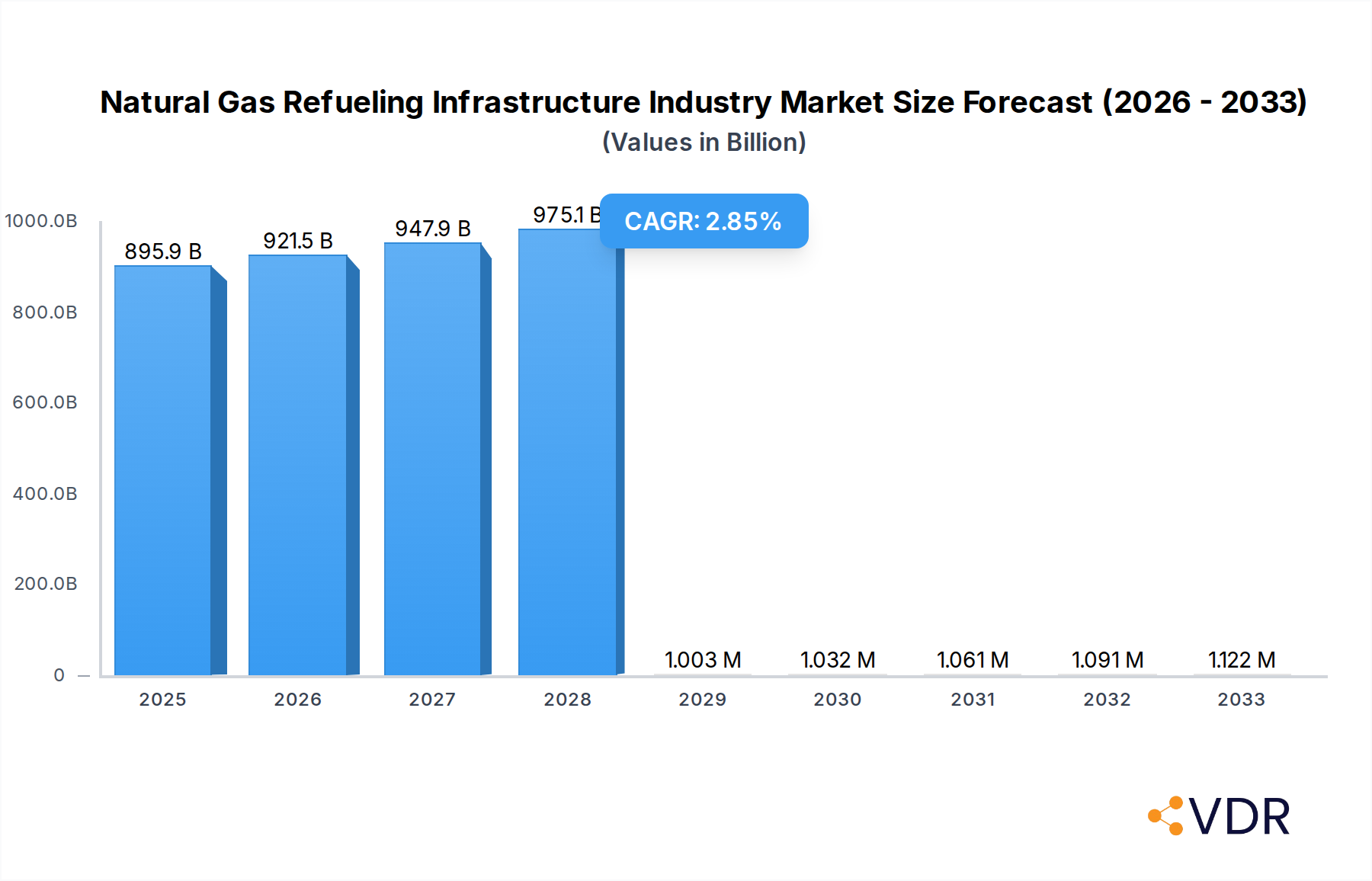

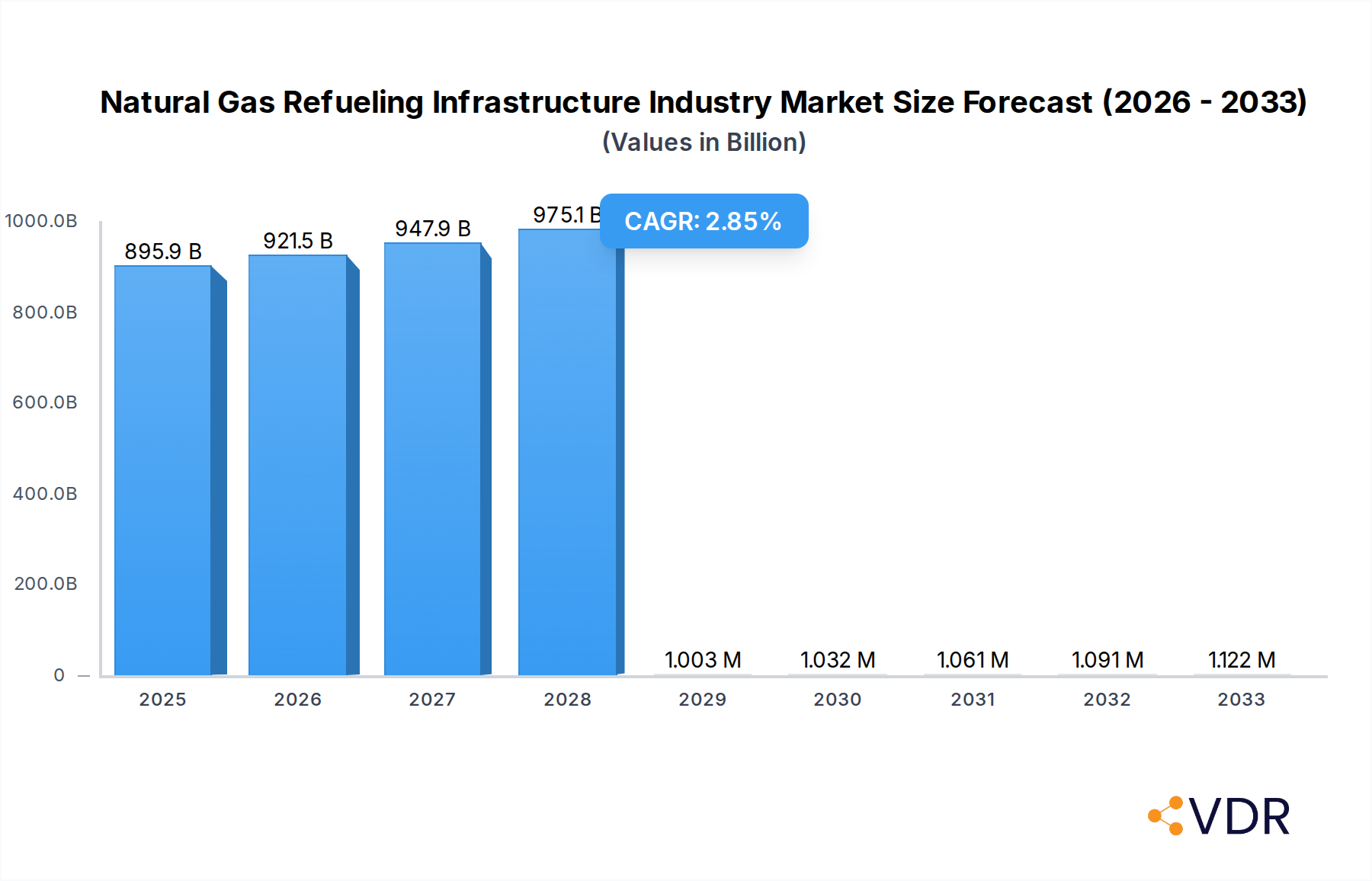

The global Natural Gas Refueling Infrastructure market is poised for steady expansion, projected to reach USD 895.86 billion in 2025. Driven by an increasing adoption of natural gas as a cleaner alternative to traditional fossil fuels, the market is expected to witness a Compound Annual Growth Rate (CAGR) of 2.9% from 2025 to 2033. This growth is propelled by supportive government policies, growing environmental consciousness, and the economic benefits offered by natural gas, particularly for heavy-duty vehicles and public transportation. The infrastructure development for Compressed Natural Gas (CNG) and Liquefied Natural Gas (LNG) is a key focus, with significant investments flowing into building more refueling stations to address range anxiety and enhance accessibility for a wider user base. Emerging economies, especially in the Asia Pacific, are anticipated to be major growth contributors, fueled by rapid industrialization and a burgeoning demand for cleaner energy solutions in the transportation sector.

Natural Gas Refueling Infrastructure Industry Market Size (In Billion)

The market dynamics are characterized by a strategic interplay between technological advancements and evolving regulatory landscapes. Companies like Greka Engineering and Technology Limited, Parker Hannifin Corp, and Clean Energy Fuels are at the forefront, innovating refueling technologies and expanding their network presence. While the market exhibits robust growth potential, it also faces certain challenges. High initial capital investment for establishing refueling infrastructure, the need for standardized safety protocols across regions, and the availability of natural gas supply can act as restraints. However, continuous innovation in gas compression, liquefaction, and storage technologies, coupled with strategic partnerships and mergers, are expected to mitigate these challenges. The forecast period of 2025-2033 will likely see a significant build-out of refueling networks, particularly in regions actively promoting natural gas vehicles, thereby solidifying its position as a crucial component of a sustainable energy future.

Natural Gas Refueling Infrastructure Industry Company Market Share

This in-depth report provides a definitive analysis of the Natural Gas Refueling Infrastructure Industry, exploring its intricate market dynamics, projected growth trajectory, and dominant regional segments. Spanning the historical period of 2019-2024, the base and estimated year of 2025, and a comprehensive forecast period of 2025-2033, this report leverages extensive data to offer actionable insights for industry stakeholders. Our analysis covers both the parent market of natural gas infrastructure and its crucial child markets, specifically focusing on Compressed Natural Gas (CNG) and Liquefied Natural Gas (LNG) refueling solutions. Expect detailed quantitative data, including market size evolution in billions, CAGR projections, and market share analysis, alongside qualitative assessments of technological innovations, regulatory frameworks, and competitive landscapes.

Natural Gas Refueling Infrastructure Industry Market Dynamics & Structure

The Natural Gas Refueling Infrastructure Industry is characterized by a moderately concentrated market structure, with key players like Greka Engineering and Technology Limited, Parker Hannifin Corp, Tulsa Gas Technologies India Pvt Ltd, Scheidt & Bachmann Gmbh, Cryostar SAS, Sanki Industry Group, Tatsuno Europe AS, Gilbarco Inc, Clean Energy Fuels, and FTI International Group Inc holding significant market shares. Technological innovation is a primary driver, with ongoing advancements in compressor technology, LNG liquefaction efficiency, and smart refueling solutions enhancing performance and reducing operational costs. The industry is heavily influenced by evolving regulatory frameworks aimed at promoting cleaner fuels and reducing carbon emissions, which directly impact the adoption of natural gas vehicles (NGVs) and, consequently, the demand for refueling stations. Competitive product substitutes, primarily electric vehicle (EV) charging infrastructure, pose a significant challenge, necessitating continuous innovation and cost-effectiveness in natural gas solutions. End-user demographics are shifting, with increasing awareness of environmental benefits and long-term fuel cost savings driving demand from both commercial fleets and individual vehicle owners. Mergers and acquisitions (M&A) are also a notable trend, with companies consolidating to enhance their market reach, technological capabilities, and to secure supply chains. For instance, recent M&A activities have seen strategic acquisitions of smaller technology providers by larger infrastructure developers, aiming to offer integrated solutions.

- Market Concentration: Moderately concentrated with established players and emerging innovators.

- Technological Innovation Drivers: Advancements in compressor efficiency, LNG storage, and digital refueling management systems.

- Regulatory Frameworks: Government incentives for NGV adoption, emissions standards, and fuel import/export policies.

- Competitive Product Substitutes: Electric vehicle charging stations, hydrogen refueling infrastructure.

- End-User Demographics: Growing adoption by commercial fleets (trucking, public transport), industrial applications, and a nascent but expanding individual consumer market.

- M&A Trends: Strategic acquisitions of technology firms, joint ventures for infrastructure development, and consolidation for market share expansion.

Natural Gas Refueling Infrastructure Industry Growth Trends & Insights

The Natural Gas Refueling Infrastructure Industry is poised for robust expansion over the forecast period, driven by a confluence of factors including escalating environmental concerns, favorable government policies, and the inherent cost advantages of natural gas as a transportation fuel. The global market size for natural gas refueling infrastructure is projected to witness significant growth, with an estimated market size of XX billion in 2025, expanding to XX billion by 2033. This represents a Compound Annual Growth Rate (CAGR) of approximately X.X% from 2025 to 2033. Adoption rates for NGVs are steadily increasing across various sectors, spurred by substantial investments in refueling station networks. Technological disruptions, such as the development of more efficient and compact refueling units and the integration of smart technologies for remote monitoring and management, are further accelerating market penetration. Consumer behavior is also shifting, with a growing preference for sustainable transportation options and a greater appreciation for the lower total cost of ownership offered by NGVs. The decline in battery technology costs for EVs, while a significant competitor, also highlights the ongoing technological evolution within the alternative fuel sector, where natural gas continues to offer a compelling and scalable solution for heavy-duty transport and long-haul applications. The report will delve into specific metrics like market penetration rates in key geographies and the impact of emerging fuel efficiency standards on NGV demand.

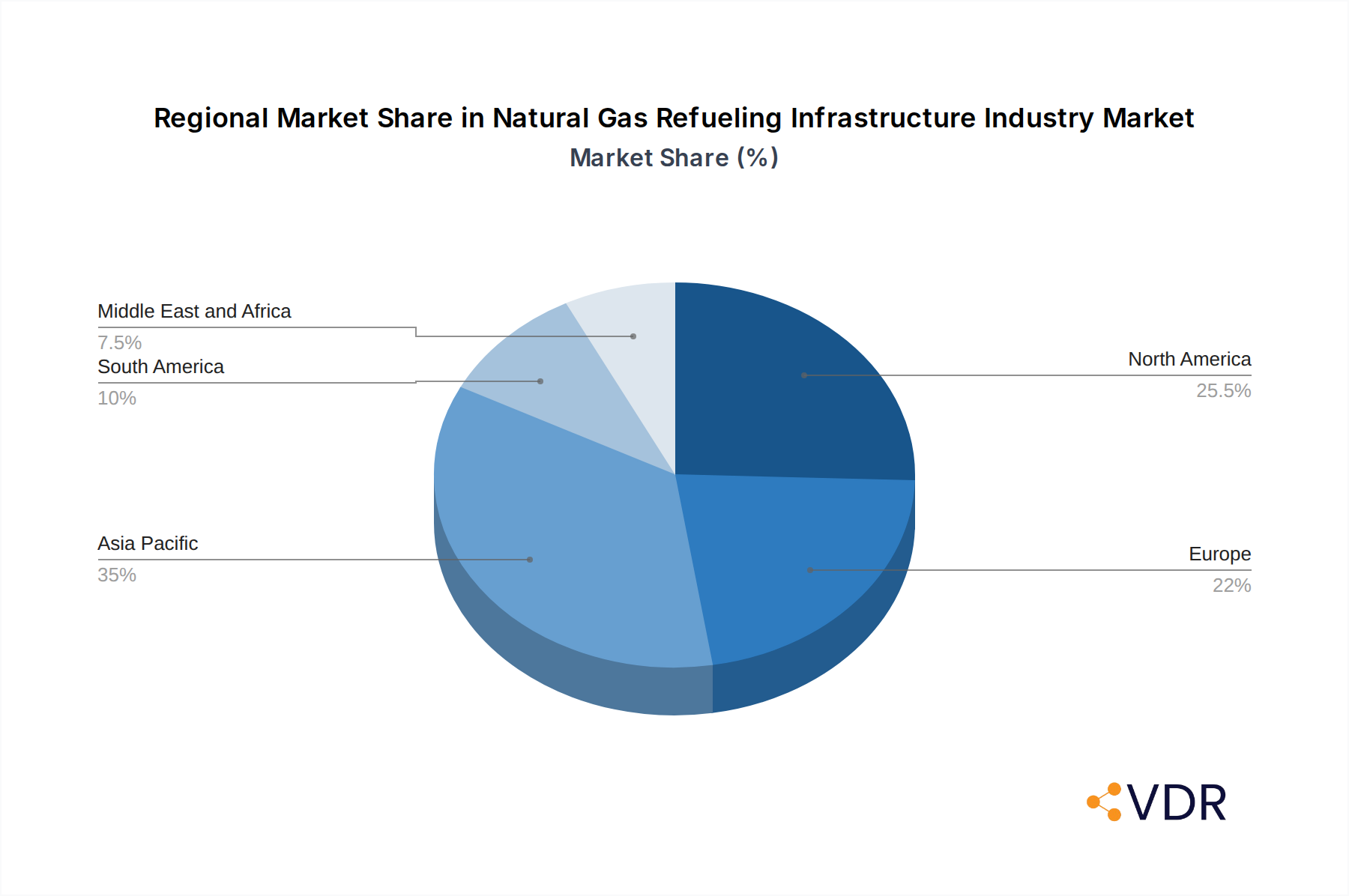

Dominant Regions, Countries, or Segments in Natural Gas Refueling Infrastructure Industry

The Compressed Natural Gas (CNG) segment is currently the dominant force within the Natural Gas Refueling Infrastructure Industry, driven by its widespread application in urban public transportation and light-to-medium duty commercial vehicles. In 2025, the global market size for natural gas refueling infrastructure is estimated at XX billion, with the CNG segment representing approximately XX% of this value, projected to reach XX billion by 2033. The dominance of CNG is attributed to its established infrastructure, lower initial investment costs for refueling stations compared to LNG, and the availability of a wide range of CNG-powered vehicle models. Key drivers for this segment's growth include stringent emission regulations in urban areas, government subsidies for CNG vehicle adoption, and the cost-effectiveness of CNG as a fuel for high-mileage vehicles. Countries like China, India, and several European nations have heavily invested in expanding their CNG refueling networks to decarbonize their transport sectors. For instance, India's push towards a gas-based economy and its ambitious targets for NGV penetration have significantly boosted CNG infrastructure development.

The Liquefied Natural Gas (LNG) segment, while currently smaller, is experiencing rapid growth and is projected to outpace CNG in terms of CAGR over the forecast period. In 2025, the LNG refueling infrastructure market is estimated at XX billion, expected to reach XX billion by 2033, with a CAGR of X.X%. LNG's dominance is increasingly evident in the heavy-duty trucking and long-haul transportation sectors, where its higher energy density and longer range capabilities are advantageous. Key drivers for LNG adoption include the development of advanced liquefaction technologies, improved storage solutions for cryogenic fuels, and the growing need for sustainable alternatives to diesel in long-distance freight movement. Government initiatives aimed at reducing emissions from heavy-duty vehicles and the potential for fuel cost savings in large fleets are also significant catalysts. Regions like North America, with its abundant natural gas reserves, and parts of Europe and Asia are witnessing substantial investments in LNG refueling stations, particularly along major trade corridors. The ongoing development of virtual pipelines and enhanced liquefaction plant capacities are further supporting the expansion of the LNG refueling ecosystem.

Natural Gas Refueling Infrastructure Industry Product Landscape

The product landscape of the Natural Gas Refueling Infrastructure Industry is characterized by continuous innovation aimed at enhancing efficiency, safety, and user experience. Key product categories include CNG compressors, LNG cryogenic pumps, dispensers, storage tanks, and integrated control systems. Manufacturers are focusing on developing more energy-efficient compressors that reduce operational costs, while advancements in LNG liquefaction technology are enabling smaller-scale, modular plants that can be deployed closer to demand centers. Smart refueling solutions, incorporating digital payment systems, remote monitoring capabilities, and real-time data analytics, are becoming standard features, improving station management and customer convenience. The performance metrics being prioritized include faster refueling times, enhanced safety features through advanced leak detection and pressure management, and increased reliability to minimize downtime. Unique selling propositions often revolve around the modularity and scalability of refueling solutions, catering to diverse project sizes and geographic locations, as well as the integration of renewable natural gas (RNG) capabilities.

Key Drivers, Barriers & Challenges in Natural Gas Refueling Infrastructure Industry

Key Drivers: The Natural Gas Refueling Infrastructure Industry is propelled by a strong set of drivers. Government policies promoting cleaner fuels, emission reduction targets, and incentives for NGV adoption are paramount. The lower cost of natural gas compared to traditional fossil fuels, particularly for high-mileage applications, provides a significant economic impetus. Technological advancements in compressor efficiency and LNG liquefaction are making natural gas refueling more accessible and cost-effective. Growing environmental awareness and corporate sustainability initiatives are also encouraging the transition to natural gas vehicles.

Barriers & Challenges: Significant barriers include the substantial capital investment required for building refueling infrastructure. The competitive landscape with rapidly advancing electric vehicle technology presents a considerable challenge, requiring natural gas solutions to remain cost-competitive and technologically superior in their niche. Regulatory hurdles and permitting processes can lead to project delays. Supply chain complexities for specialized equipment and the intermittent nature of some natural gas supply can also pose challenges. Furthermore, public perception and education regarding the safety and efficiency of natural gas as a fuel need continuous effort. The upfront cost of NGVs for consumers and fleets can also be a restraint, despite long-term savings.

Emerging Opportunities in Natural Gas Refueling Infrastructure Industry

Emerging opportunities in the Natural Gas Refueling Infrastructure Industry are concentrated in several key areas. The increasing adoption of Renewable Natural Gas (RNG), derived from organic waste, presents a significant avenue for sustainable growth, allowing for a truly circular economy in transportation fuels. The development of fast-charging LNG stations for long-haul trucking, reducing downtime and increasing efficiency for logistics companies, is another critical area. Expansion into developing economies with growing transportation needs and supportive government policies offers substantial untapped market potential. Furthermore, the integration of smart grid technologies and bi-directional charging for NGVs can create new revenue streams and enhance grid stability. The growing demand for natural gas in marine bunkering also presents an opportunity for specialized refueling infrastructure development.

Growth Accelerators in the Natural Gas Refueling Infrastructure Industry Industry

Several catalysts are accelerating long-term growth in the Natural Gas Refueling Infrastructure Industry. Technological breakthroughs in developing more compact, energy-efficient, and lower-cost refueling equipment are crucial. Strategic partnerships between NGV manufacturers, infrastructure developers, and fuel suppliers are creating integrated solutions that simplify adoption for end-users. Market expansion strategies, particularly focusing on corridors with high freight traffic and regions with significant natural gas reserves, are vital. The increasing global commitment to climate change mitigation and the pursuit of energy independence are creating a favorable policy environment. Investments in research and development for enhanced natural gas storage and dispensing technologies will further fuel adoption.

Key Players Shaping the Natural Gas Refueling Infrastructure Industry Market

- Greka Engineering and Technology Limited

- Parker Hannifin Corp

- Tulsa Gas Technologies India Pvt Ltd

- Scheidt & Bachmann Gmbh

- Cryostar SAS

- Sanki Industry Group

- Tatsuno Europe AS

- Gilbarco Inc

- Clean Energy Fuels

- FTI International Group Inc

Notable Milestones in Natural Gas Refueling Infrastructure Industry Sector

- 2019: Increased government mandates for fleet emissions reductions in major economies driving NGV adoption.

- 2020: Significant investment in RNG production and distribution infrastructure to support sustainable fueling.

- 2021: Launch of advanced, modular LNG refueling station designs for faster deployment.

- 2022: Major trucking companies announcing ambitious targets for transitioning their fleets to natural gas.

- 2023: Development of smart refueling technologies integrating payment, data analytics, and remote management.

- 2024: Expansion of natural gas bunkering infrastructure for the maritime sector in key global ports.

In-Depth Natural Gas Refueling Infrastructure Industry Market Outlook

The future outlook for the Natural Gas Refueling Infrastructure Industry is exceptionally positive, driven by the sustained global push for cleaner transportation and energy diversification. Growth accelerators, including relentless technological innovation in refueling efficiency and cost reduction, alongside strategic collaborations across the value chain, will continue to shape the market. The expansion into emerging economies and the increasing demand for natural gas in niche applications like maritime transport will unlock new avenues for growth. The industry is well-positioned to capitalize on favorable regulatory environments and the ongoing pursuit of sustainable energy solutions, ensuring a robust and expanding market for natural gas refueling infrastructure in the coming years.

Natural Gas Refueling Infrastructure Industry Segmentation

-

1. Type of Natural Gas

- 1.1. Compressed Natural Gas (CNG)

- 1.2. Liquefied Natural Gas (LNG)

Natural Gas Refueling Infrastructure Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. South America

- 5. Middle East and Africa

Natural Gas Refueling Infrastructure Industry Regional Market Share

Geographic Coverage of Natural Gas Refueling Infrastructure Industry

Natural Gas Refueling Infrastructure Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 2.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type of Natural Gas

- 5.1.1. Compressed Natural Gas (CNG)

- 5.1.2. Liquefied Natural Gas (LNG)

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. North America

- 5.2.2. Europe

- 5.2.3. Asia Pacific

- 5.2.4. South America

- 5.2.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Type of Natural Gas

- 6. Global Natural Gas Refueling Infrastructure Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type of Natural Gas

- 6.1.1. Compressed Natural Gas (CNG)

- 6.1.2. Liquefied Natural Gas (LNG)

- 6.1. Market Analysis, Insights and Forecast - by Type of Natural Gas

- 7. North America Natural Gas Refueling Infrastructure Industry Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Type of Natural Gas

- 7.1.1. Compressed Natural Gas (CNG)

- 7.1.2. Liquefied Natural Gas (LNG)

- 7.1. Market Analysis, Insights and Forecast - by Type of Natural Gas

- 8. Europe Natural Gas Refueling Infrastructure Industry Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Type of Natural Gas

- 8.1.1. Compressed Natural Gas (CNG)

- 8.1.2. Liquefied Natural Gas (LNG)

- 8.1. Market Analysis, Insights and Forecast - by Type of Natural Gas

- 9. Asia Pacific Natural Gas Refueling Infrastructure Industry Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Type of Natural Gas

- 9.1.1. Compressed Natural Gas (CNG)

- 9.1.2. Liquefied Natural Gas (LNG)

- 9.1. Market Analysis, Insights and Forecast - by Type of Natural Gas

- 10. South America Natural Gas Refueling Infrastructure Industry Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Type of Natural Gas

- 10.1.1. Compressed Natural Gas (CNG)

- 10.1.2. Liquefied Natural Gas (LNG)

- 10.1. Market Analysis, Insights and Forecast - by Type of Natural Gas

- 11. Middle East and Africa Natural Gas Refueling Infrastructure Industry Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Type of Natural Gas

- 11.1.1. Compressed Natural Gas (CNG)

- 11.1.2. Liquefied Natural Gas (LNG)

- 11.1. Market Analysis, Insights and Forecast - by Type of Natural Gas

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Greka Engineering and Technology Limited

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Parker Hannifin Corp

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Tulsa Gas Technologies India Pvt Ltd

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Scheidt & Bachmann Gmbh

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Cryostar SAS

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Sanki Industry Group

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Tatsuno Europe AS

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Gilbarco Inc

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Clean Energy Fuels

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 FTI International Group Inc

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Greka Engineering and Technology Limited

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Natural Gas Refueling Infrastructure Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Natural Gas Refueling Infrastructure Industry Revenue (billion), by Type of Natural Gas 2025 & 2033

- Figure 3: North America Natural Gas Refueling Infrastructure Industry Revenue Share (%), by Type of Natural Gas 2025 & 2033

- Figure 4: North America Natural Gas Refueling Infrastructure Industry Revenue (billion), by Country 2025 & 2033

- Figure 5: North America Natural Gas Refueling Infrastructure Industry Revenue Share (%), by Country 2025 & 2033

- Figure 6: Europe Natural Gas Refueling Infrastructure Industry Revenue (billion), by Type of Natural Gas 2025 & 2033

- Figure 7: Europe Natural Gas Refueling Infrastructure Industry Revenue Share (%), by Type of Natural Gas 2025 & 2033

- Figure 8: Europe Natural Gas Refueling Infrastructure Industry Revenue (billion), by Country 2025 & 2033

- Figure 9: Europe Natural Gas Refueling Infrastructure Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Asia Pacific Natural Gas Refueling Infrastructure Industry Revenue (billion), by Type of Natural Gas 2025 & 2033

- Figure 11: Asia Pacific Natural Gas Refueling Infrastructure Industry Revenue Share (%), by Type of Natural Gas 2025 & 2033

- Figure 12: Asia Pacific Natural Gas Refueling Infrastructure Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: Asia Pacific Natural Gas Refueling Infrastructure Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: South America Natural Gas Refueling Infrastructure Industry Revenue (billion), by Type of Natural Gas 2025 & 2033

- Figure 15: South America Natural Gas Refueling Infrastructure Industry Revenue Share (%), by Type of Natural Gas 2025 & 2033

- Figure 16: South America Natural Gas Refueling Infrastructure Industry Revenue (billion), by Country 2025 & 2033

- Figure 17: South America Natural Gas Refueling Infrastructure Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Middle East and Africa Natural Gas Refueling Infrastructure Industry Revenue (billion), by Type of Natural Gas 2025 & 2033

- Figure 19: Middle East and Africa Natural Gas Refueling Infrastructure Industry Revenue Share (%), by Type of Natural Gas 2025 & 2033

- Figure 20: Middle East and Africa Natural Gas Refueling Infrastructure Industry Revenue (billion), by Country 2025 & 2033

- Figure 21: Middle East and Africa Natural Gas Refueling Infrastructure Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Natural Gas Refueling Infrastructure Industry Revenue billion Forecast, by Type of Natural Gas 2020 & 2033

- Table 2: Global Natural Gas Refueling Infrastructure Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 3: Global Natural Gas Refueling Infrastructure Industry Revenue billion Forecast, by Type of Natural Gas 2020 & 2033

- Table 4: Global Natural Gas Refueling Infrastructure Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 5: Global Natural Gas Refueling Infrastructure Industry Revenue billion Forecast, by Type of Natural Gas 2020 & 2033

- Table 6: Global Natural Gas Refueling Infrastructure Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: Global Natural Gas Refueling Infrastructure Industry Revenue billion Forecast, by Type of Natural Gas 2020 & 2033

- Table 8: Global Natural Gas Refueling Infrastructure Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 9: Global Natural Gas Refueling Infrastructure Industry Revenue billion Forecast, by Type of Natural Gas 2020 & 2033

- Table 10: Global Natural Gas Refueling Infrastructure Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 11: Global Natural Gas Refueling Infrastructure Industry Revenue billion Forecast, by Type of Natural Gas 2020 & 2033

- Table 12: Global Natural Gas Refueling Infrastructure Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Natural Gas Refueling Infrastructure Industry?

The projected CAGR is approximately 2.9%.

2. Which companies are prominent players in the Natural Gas Refueling Infrastructure Industry?

Key companies in the market include Greka Engineering and Technology Limited, Parker Hannifin Corp, Tulsa Gas Technologies India Pvt Ltd, Scheidt & Bachmann Gmbh, Cryostar SAS, Sanki Industry Group, Tatsuno Europe AS, Gilbarco Inc, Clean Energy Fuels, FTI International Group Inc.

3. What are the main segments of the Natural Gas Refueling Infrastructure Industry?

The market segments include Type of Natural Gas.

4. Can you provide details about the market size?

The market size is estimated to be USD 895.86 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Corporate Sustainability Goals4.; Stringent Regultions and Compliance.

6. What are the notable trends driving market growth?

Compressed Natural Gas to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; High Complexity in Carbon Accounting.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Natural Gas Refueling Infrastructure Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Natural Gas Refueling Infrastructure Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Natural Gas Refueling Infrastructure Industry?

To stay informed about further developments, trends, and reports in the Natural Gas Refueling Infrastructure Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence