Key Insights

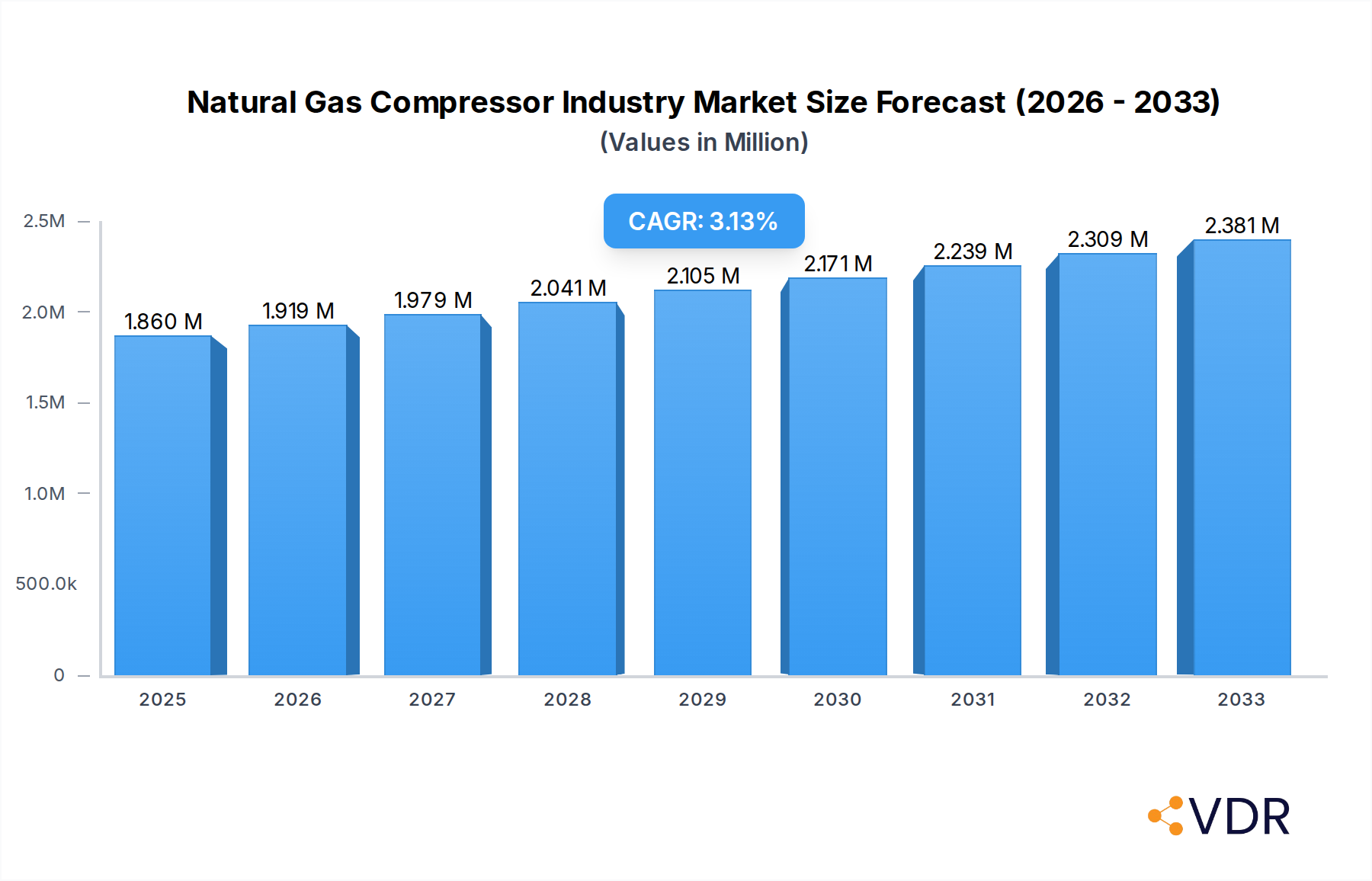

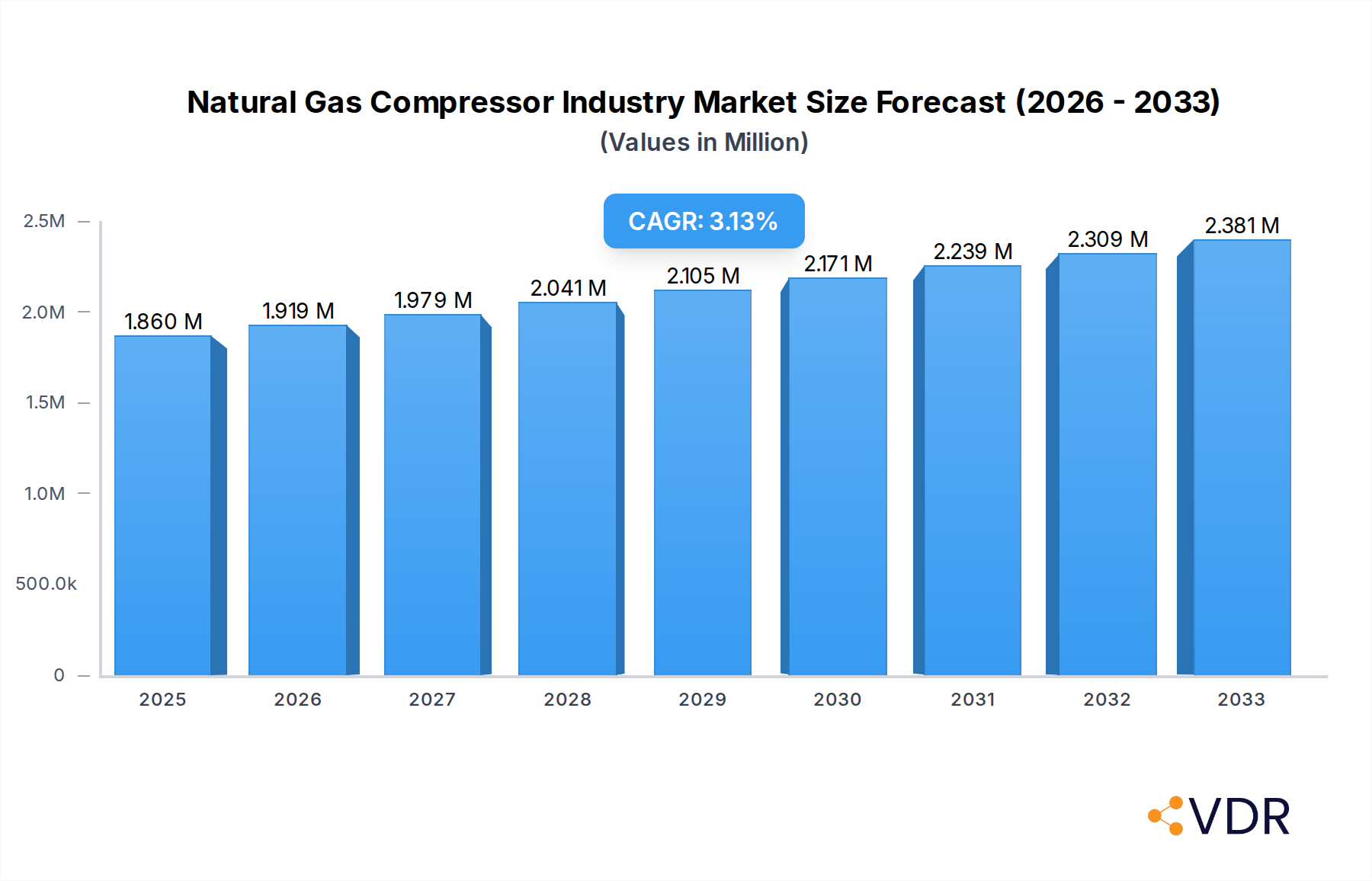

The Natural Gas Compressor Industry is poised for significant expansion, with a projected market size of 1.86 Million in 2025, growing at a Compound Annual Growth Rate (CAGR) of 3.13% through 2033. This robust growth is fueled by escalating global demand for natural gas as a cleaner alternative to fossil fuels, particularly in power generation, industrial processes, and residential heating. The upstream sector, encompassing exploration and production, remains a primary driver, necessitating efficient compression for gas extraction and transportation. Concurrently, the midstream sector, crucial for the transportation of natural gas via pipelines, and the downstream sector, focusing on processing and distribution, also present substantial opportunities. Technological advancements in compressor efficiency, reliability, and noise reduction, alongside the increasing adoption of digital solutions for remote monitoring and predictive maintenance, are further propelling market dynamics. The industry is witnessing a shift towards more energy-efficient and environmentally friendly compressor technologies, aligning with global sustainability initiatives.

Natural Gas Compressor Industry Market Size (In Million)

The market is segmented by type into Reciprocating and Screw compressors, with each type catering to specific operational needs and pressure requirements within the natural gas value chain. Applications span the entire spectrum from upstream extraction to downstream refining and distribution. Key players like Atlas Corporation AB, Siemens AG, and Ingersoll Rand PLC are actively engaged in innovation and strategic partnerships to capture market share. Geographically, North America, driven by extensive shale gas production, and Asia Pacific, with its rapidly growing energy demands, are expected to be major growth hubs. Europe and other regions are also contributing to market expansion, albeit at different paces. While the market is characterized by strong growth drivers, it also faces certain restraints. These may include fluctuating natural gas prices, stringent environmental regulations that could increase operational costs, and the significant capital investment required for compressor infrastructure. Nevertheless, the overarching trend towards natural gas as a transitional fuel and the ongoing expansion of global gas infrastructure will continue to underpin the industry's positive trajectory.

Natural Gas Compressor Industry Company Market Share

Natural Gas Compressor Market Report: Powering the Energy Transition

This comprehensive report delves into the dynamic natural gas compressor market, examining its intricate dynamics, growth trajectory, and the strategic landscape shaping its future. With a focus on upstream, downstream, and midstream applications, this analysis offers unparalleled insights into the evolution of reciprocating compressors and screw compressors, crucial components for efficient natural gas transportation and processing. We analyze the parent and child market segments, revealing opportunities and challenges across the entire value chain. This report is an indispensable resource for stakeholders seeking to navigate the complexities of the global oil and gas equipment sector, specifically targeting LNG compressor and gas processing compressor procurement and development.

Natural Gas Compressor Industry Market Dynamics & Structure

The natural gas compressor industry is characterized by a moderately concentrated market structure, with a few key global players holding significant market share, estimated at over 65% of the total market value in 2025. Technological innovation serves as a primary driver, fueled by the increasing demand for energy efficiency, reduced emissions, and enhanced operational reliability. Regulatory frameworks, particularly those promoting decarbonization and stringent environmental standards, are also shaping product development and adoption rates. Competitive product substitutes, such as electric-driven compressors in certain niche applications, exist but are currently limited in widespread adoption for large-scale natural gas compression. End-user demographics are shifting towards proactive environmental stewardship and operational cost optimization. Mergers and acquisitions (M&A) trends are evident, with larger entities consolidating their market positions and expanding their technological portfolios. For instance, the past five years have seen approximately 15 major M&A deals valued at over $500 million each, primarily focused on acquiring specialized compression technologies and expanding geographical reach.

- Market Concentration: Dominated by a few large players, creating a competitive but structured market.

- Technological Innovation: Driven by energy efficiency mandates, emission reduction goals, and advanced diagnostic capabilities.

- Regulatory Influence: Stringent environmental policies are pushing for cleaner and more efficient compression solutions.

- Competitive Landscape: While substitutes exist, specialized natural gas compressors maintain a dominant position.

- M&A Activity: Strategic acquisitions are common for expanding technological offerings and market penetration.

Natural Gas Compressor Industry Growth Trends & Insights

The natural gas compressor market size is projected for substantial growth, driven by the ever-increasing global demand for natural gas as a cleaner transitional fuel and its pivotal role in power generation, industrial processes, and residential heating. This report, leveraging extensive market research, forecasts a robust Compound Annual Growth Rate (CAGR) of approximately 5.8% from 2025 to 2033. The market penetration of advanced and energy-efficient compressor technologies is accelerating, fueled by both economic incentives and regulatory pressures. Technological disruptions, such as the development of hyper-efficient variable speed drives and advanced sealing technologies, are significantly enhancing operational performance and reducing energy consumption. Consumer behavior shifts are also playing a crucial role, with end-users prioritizing long-term operational cost savings, reduced environmental impact, and enhanced safety features in their procurement decisions. The global natural gas compressor market value is estimated to reach $18.5 billion by 2025, with significant expansion anticipated in the forecast period. The increasing reliance on natural gas infrastructure for energy security, coupled with ongoing exploration and production activities, will continue to bolster demand for new compressor installations and upgrades. The child market segments, focusing on specific applications within upstream, midstream, and downstream sectors, are exhibiting varied but consistently positive growth patterns. For instance, the midstream segment, crucial for natural gas transportation via pipelines, is expected to witness the highest growth in demand for large-scale centrifugal compressors.

Dominant Regions, Countries, or Segments in Natural Gas Compressor Industry

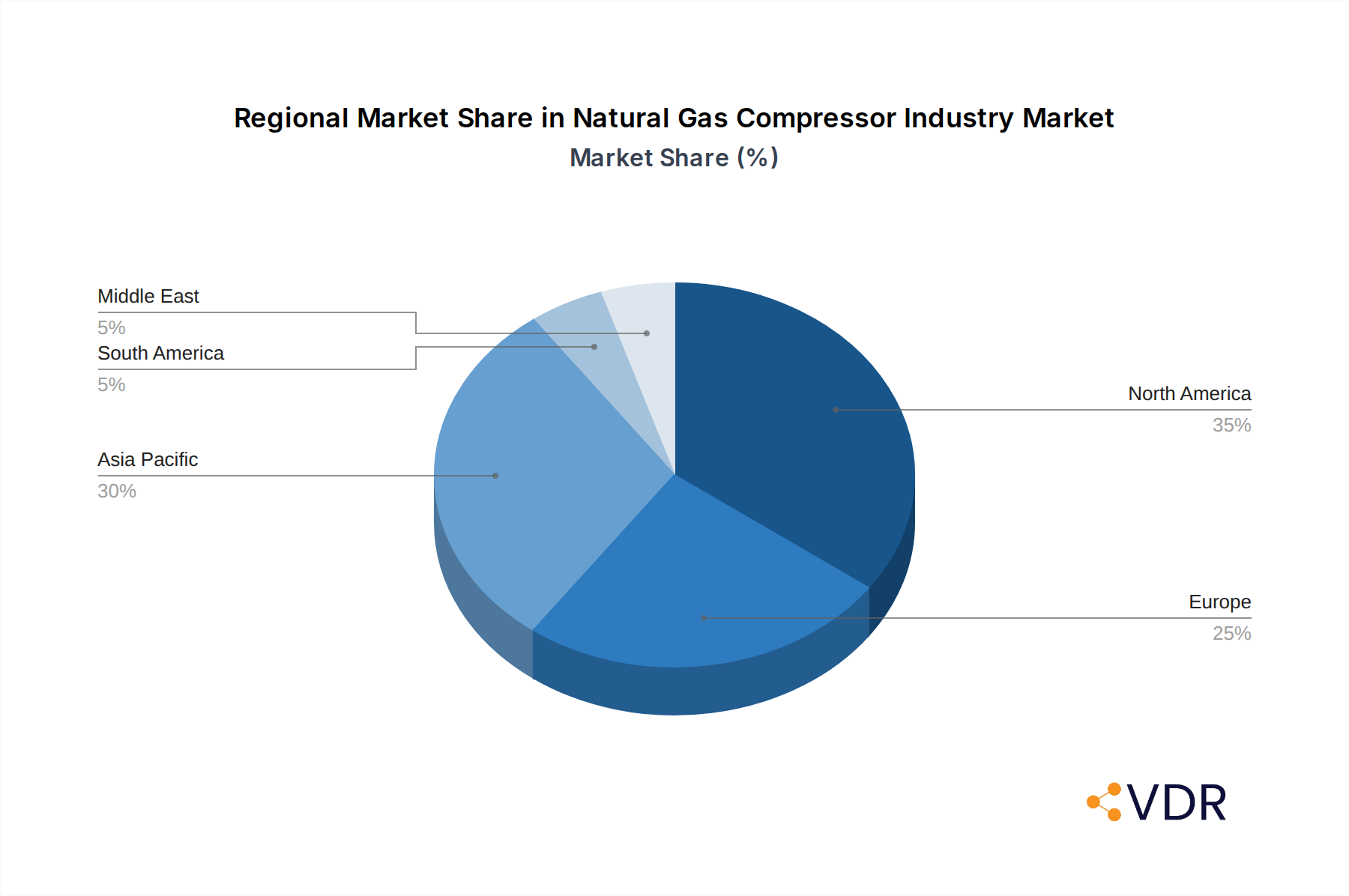

North America, specifically the United States, currently dominates the natural gas compressor industry, driven by its extensive shale gas reserves and well-developed midstream infrastructure. The midstream application segment is the primary growth engine within this region, accounting for an estimated 45% of the total market share in 2025. The region's robust pipeline network necessitates a continuous demand for high-capacity compressors for efficient gas transmission and storage.

- North America Dominance: Characterized by significant shale gas production and extensive natural gas infrastructure.

- Market Share: Approximately 38% of the global natural gas compressor market in 2025.

- Key Drivers: Abundant natural gas reserves, government incentives for cleaner energy, and ongoing pipeline expansion projects.

- Midstream Segment Leadership: This segment, encompassing gas gathering, processing, and transmission, exhibits the strongest demand for advanced compression solutions.

- Growth Potential: Fueled by the need to transport increasing volumes of natural gas from production sites to consumption centers.

- Technological Adoption: High uptake of energy-efficient and low-emission compressors.

- Asia Pacific as a Growth Frontier: The Asia Pacific region is emerging as a significant growth market, propelled by rapidly expanding energy demands and investments in natural gas infrastructure.

- Emerging Market Share: Expected to grow at a CAGR of 7.2% during the forecast period.

- Key Countries: China, India, and Southeast Asian nations are investing heavily in LNG regasification terminals and domestic pipeline networks.

- Europe's Focus on Sustainability: Europe is witnessing a strong demand for compressors that meet stringent environmental regulations, prioritizing low-emission and energy-efficient models, particularly for downstream applications and industrial processes.

- Segment Dominance: Downstream and industrial applications are significant.

- Regulatory Impact: Strict emissions standards are driving the adoption of advanced technologies.

- Reciprocating vs. Screw Compressors: While reciprocating compressors maintain a significant presence in upstream applications due to their robustness, screw compressors are gaining traction in midstream and downstream sectors due to their higher efficiency and continuous flow capabilities. The child market for screw compressors is expected to grow at a CAGR of 6.5%.

Natural Gas Compressor Industry Product Landscape

The product landscape of the natural gas compressor industry is characterized by continuous innovation aimed at enhancing efficiency, reducing emissions, and improving reliability. Key product advancements include the development of high-efficiency centrifugal compressors with advanced impeller designs and low-loss diffusers, and sophisticated reciprocating compressors featuring improved sealing technologies and advanced control systems. The integration of digital monitoring and predictive maintenance capabilities is a significant trend, allowing for optimized performance and reduced downtime. Applications span the entire natural gas value chain, from upstream extraction and processing to midstream transportation and downstream distribution and industrial use. Unique selling propositions often revolve around lower fuel consumption, reduced greenhouse gas emissions, and extended operational lifespans. Technological advancements are also focusing on modular designs for easier installation and maintenance, and specialized compressors for demanding environments like offshore operations and remote locations.

Key Drivers, Barriers & Challenges in Natural Gas Compressor Industry

Key Drivers:

- Growing Global Natural Gas Demand: As a transition fuel and a vital energy source, demand for natural gas continues to rise, necessitating more efficient compression solutions.

- Infrastructure Development: Expansion of pipelines, LNG facilities, and gas processing plants drives demand for new compressor installations.

- Energy Efficiency Mandates: Stringent regulations and economic incentives push for compressors that minimize energy consumption.

- Technological Advancements: Innovations in compressor design, materials, and control systems enhance performance and reduce environmental impact.

- Environmental Regulations: Policies aimed at reducing methane emissions and overall carbon footprint favor advanced compression technologies.

Key Barriers & Challenges:

- High Capital Investment: The initial cost of advanced natural gas compressors can be substantial, posing a barrier for smaller operators.

- Supply Chain Volatility: Geopolitical factors and global demand fluctuations can impact the availability of raw materials and components, leading to extended lead times and increased costs. For instance, recent disruptions have extended delivery times for critical components by up to 30%.

- Skilled Workforce Shortage: A lack of trained personnel for installation, operation, and maintenance of sophisticated compression systems can hinder adoption.

- Regulatory Uncertainty: Evolving environmental regulations can create uncertainty for long-term investment decisions.

- Competition from Renewables: While a transition fuel, the long-term growth of natural gas faces competition from rapidly advancing renewable energy sources.

Emerging Opportunities in Natural Gas Compressor Industry

Emerging opportunities in the natural gas compressor industry lie in the development and deployment of ultra-low emission compression technologies, particularly those designed to minimize methane slip. The increasing focus on carbon capture, utilization, and storage (CCUS) presents a significant opportunity for specialized compressors adapted for these new processes. Furthermore, the growing demand for compressed natural gas (CNG) and liquefied natural gas (LNG) as transportation fuels in heavy-duty vehicles and maritime applications is opening up new avenues for smaller, more localized compression solutions. The digitalization of compressor operations, enabling remote monitoring, predictive maintenance, and optimized performance through AI and IoT integration, represents a substantial growth area. Untapped markets in developing economies with expanding natural gas grids also offer considerable potential.

Growth Accelerators in the Natural Gas Compressor Industry Industry

Growth accelerators in the natural gas compressor industry are primarily driven by technological breakthroughs in efficiency and emissions reduction, coupled with strategic partnerships and market expansion initiatives. The increasing adoption of digital twin technology for compressor performance optimization and predictive maintenance is a key catalyst, reducing operational costs and enhancing reliability. Strategic partnerships between compressor manufacturers and energy companies are crucial for developing bespoke solutions tailored to specific project needs and regulatory environments. Furthermore, the expanding global LNG trade and the development of new export and import terminals are creating significant demand for high-capacity, advanced compression systems. Investments in research and development for hydrogen compression technologies, as the industry explores hydrogen as a future energy carrier, also represent a significant long-term growth accelerator.

Key Players Shaping the Natural Gas Compressor Industry Market

- Atlas Corporation AB

- Clean Energy Fuels Corp

- Bauer Compressors Inc

- Ariel Corporation

- Siemens AG

- Burckhardt Compression Holding AG

- Ingersoll Rand PLC

- General Electric Company

- HMS Group

- Howden Group Ltd

Notable Milestones in Natural Gas Compressor Industry Sector

- April 2023: Oilfield services specialist Baker Hughes has been awarded a contract to supply partner QatarEnergy with two main refrigerant compressors (MRCs) for Qatar's North Field South (NFS) project. Qatargas will execute the expansion project. Each MRC train will consist of three Frame 9E DLN Ultra Low NOx gas turbines and six centrifugal compressors across two LNG trains for a total scope of supply of six gas turbines to drive 12 compressors, significantly bolstering the LNG sector's compression capabilities.

- January 2022: Industrial gas technology specialist Burckhardt Compression (Burckhardt) bagged a gas compressor supply contract from TECNIMONT SpA and Tecnimont Private Ltd. to provide compression solutions for the IOCL's upcoming polypropylene plant in Bihar, India. The company is expected to provide EPC and commissioning services for the compression systems, highlighting the growing demand for specialized compressors in the petrochemical industry.

In-Depth Natural Gas Compressor Industry Market Outlook

The in-depth market outlook for the natural gas compressor industry is exceptionally positive, driven by sustained global energy demand and the critical role of natural gas in the ongoing energy transition. Growth accelerators, including the widespread adoption of digital technologies for enhanced operational efficiency and the development of ultra-low emission compressors, are set to propel the market forward. Strategic partnerships between leading manufacturers and energy giants are crucial for innovation and market penetration, ensuring that the industry remains at the forefront of technological advancements. The expanding LNG infrastructure and the increasing use of natural gas in transportation are further solidifying the market's growth trajectory. Future investments will likely focus on developing solutions for hydrogen compression and CCUS applications, positioning the industry to capitalize on evolving energy landscapes and contribute significantly to global decarbonization efforts. The market is poised for sustained expansion, offering considerable strategic opportunities for stakeholders across the value chain.

Natural Gas Compressor Industry Segmentation

-

1. Type

- 1.1. Reciprocating

- 1.2. Screw

-

2. Application

- 2.1. Upstream

- 2.2. Downstream

- 2.3. Midstream

Natural Gas Compressor Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. France

- 2.3. Spain

- 2.4. United Kingdom

- 2.5. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. India

- 3.3. Malaysia

- 3.4. Indonesia

- 3.5. Rest of Asia Pacifc

-

4. South America

- 4.1. Brazil

- 4.2. Argentina

- 4.3. Colombia

- 4.4. Rest of South America

- 5. Middle East

-

6. Saudi Arabia

- 6.1. United Arab Emirated

- 6.2. Nigeria

- 6.3. South Africa

- 6.4. Rest of Middle East

Natural Gas Compressor Industry Regional Market Share

Geographic Coverage of Natural Gas Compressor Industry

Natural Gas Compressor Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.13% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Reciprocating

- 5.1.2. Screw

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Upstream

- 5.2.2. Downstream

- 5.2.3. Midstream

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. South America

- 5.3.5. Middle East

- 5.3.6. Saudi Arabia

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Global Natural Gas Compressor Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Reciprocating

- 6.1.2. Screw

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Upstream

- 6.2.2. Downstream

- 6.2.3. Midstream

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. North America Natural Gas Compressor Industry Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Reciprocating

- 7.1.2. Screw

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Upstream

- 7.2.2. Downstream

- 7.2.3. Midstream

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Europe Natural Gas Compressor Industry Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Reciprocating

- 8.1.2. Screw

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Upstream

- 8.2.2. Downstream

- 8.2.3. Midstream

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Asia Pacific Natural Gas Compressor Industry Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Reciprocating

- 9.1.2. Screw

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Upstream

- 9.2.2. Downstream

- 9.2.3. Midstream

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. South America Natural Gas Compressor Industry Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Reciprocating

- 10.1.2. Screw

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Upstream

- 10.2.2. Downstream

- 10.2.3. Midstream

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Middle East Natural Gas Compressor Industry Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Reciprocating

- 11.1.2. Screw

- 11.2. Market Analysis, Insights and Forecast - by Application

- 11.2.1. Upstream

- 11.2.2. Downstream

- 11.2.3. Midstream

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Saudi Arabia Natural Gas Compressor Industry Analysis, Insights and Forecast, 2021-2033

- 12.1. Market Analysis, Insights and Forecast - by Type

- 12.1.1. Reciprocating

- 12.1.2. Screw

- 12.2. Market Analysis, Insights and Forecast - by Application

- 12.2.1. Upstream

- 12.2.2. Downstream

- 12.2.3. Midstream

- 12.1. Market Analysis, Insights and Forecast - by Type

- 13. Competitive Analysis

- 13.1. Company Profiles

- 13.1.1 Atlas Corporation AB

- 13.1.1.1. Company Overview

- 13.1.1.2. Products

- 13.1.1.3. Company Financials

- 13.1.1.4. SWOT Analysis

- 13.1.2 Clean Energy Fuels Corp

- 13.1.2.1. Company Overview

- 13.1.2.2. Products

- 13.1.2.3. Company Financials

- 13.1.2.4. SWOT Analysis

- 13.1.3 Bauer Compressors Inc

- 13.1.3.1. Company Overview

- 13.1.3.2. Products

- 13.1.3.3. Company Financials

- 13.1.3.4. SWOT Analysis

- 13.1.4 Ariel Corporation

- 13.1.4.1. Company Overview

- 13.1.4.2. Products

- 13.1.4.3. Company Financials

- 13.1.4.4. SWOT Analysis

- 13.1.5 Siemens AG*List Not Exhaustive

- 13.1.5.1. Company Overview

- 13.1.5.2. Products

- 13.1.5.3. Company Financials

- 13.1.5.4. SWOT Analysis

- 13.1.6 Burckhardt Compression Holding AG

- 13.1.6.1. Company Overview

- 13.1.6.2. Products

- 13.1.6.3. Company Financials

- 13.1.6.4. SWOT Analysis

- 13.1.7 Ingersoll Rand PLC

- 13.1.7.1. Company Overview

- 13.1.7.2. Products

- 13.1.7.3. Company Financials

- 13.1.7.4. SWOT Analysis

- 13.1.8 General Electric Company

- 13.1.8.1. Company Overview

- 13.1.8.2. Products

- 13.1.8.3. Company Financials

- 13.1.8.4. SWOT Analysis

- 13.1.9 HMS Group

- 13.1.9.1. Company Overview

- 13.1.9.2. Products

- 13.1.9.3. Company Financials

- 13.1.9.4. SWOT Analysis

- 13.1.10 Howden Group Ltd

- 13.1.10.1. Company Overview

- 13.1.10.2. Products

- 13.1.10.3. Company Financials

- 13.1.10.4. SWOT Analysis

- 13.1.1 Atlas Corporation AB

- 13.2. Market Entropy

- 13.2.1 Company's Key Areas Served

- 13.2.2 Recent Developments

- 13.3. Company Market Share Analysis 2025

- 13.3.1 Top 5 Companies Market Share Analysis

- 13.3.2 Top 3 Companies Market Share Analysis

- 13.4. List of Potential Customers

- 14. Research Methodology

List of Figures

- Figure 1: Global Natural Gas Compressor Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Natural Gas Compressor Industry Revenue (Million), by Type 2025 & 2033

- Figure 3: North America Natural Gas Compressor Industry Revenue Share (%), by Type 2025 & 2033

- Figure 4: North America Natural Gas Compressor Industry Revenue (Million), by Application 2025 & 2033

- Figure 5: North America Natural Gas Compressor Industry Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Natural Gas Compressor Industry Revenue (Million), by Country 2025 & 2033

- Figure 7: North America Natural Gas Compressor Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Natural Gas Compressor Industry Revenue (Million), by Type 2025 & 2033

- Figure 9: Europe Natural Gas Compressor Industry Revenue Share (%), by Type 2025 & 2033

- Figure 10: Europe Natural Gas Compressor Industry Revenue (Million), by Application 2025 & 2033

- Figure 11: Europe Natural Gas Compressor Industry Revenue Share (%), by Application 2025 & 2033

- Figure 12: Europe Natural Gas Compressor Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: Europe Natural Gas Compressor Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Natural Gas Compressor Industry Revenue (Million), by Type 2025 & 2033

- Figure 15: Asia Pacific Natural Gas Compressor Industry Revenue Share (%), by Type 2025 & 2033

- Figure 16: Asia Pacific Natural Gas Compressor Industry Revenue (Million), by Application 2025 & 2033

- Figure 17: Asia Pacific Natural Gas Compressor Industry Revenue Share (%), by Application 2025 & 2033

- Figure 18: Asia Pacific Natural Gas Compressor Industry Revenue (Million), by Country 2025 & 2033

- Figure 19: Asia Pacific Natural Gas Compressor Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: South America Natural Gas Compressor Industry Revenue (Million), by Type 2025 & 2033

- Figure 21: South America Natural Gas Compressor Industry Revenue Share (%), by Type 2025 & 2033

- Figure 22: South America Natural Gas Compressor Industry Revenue (Million), by Application 2025 & 2033

- Figure 23: South America Natural Gas Compressor Industry Revenue Share (%), by Application 2025 & 2033

- Figure 24: South America Natural Gas Compressor Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: South America Natural Gas Compressor Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East Natural Gas Compressor Industry Revenue (Million), by Type 2025 & 2033

- Figure 27: Middle East Natural Gas Compressor Industry Revenue Share (%), by Type 2025 & 2033

- Figure 28: Middle East Natural Gas Compressor Industry Revenue (Million), by Application 2025 & 2033

- Figure 29: Middle East Natural Gas Compressor Industry Revenue Share (%), by Application 2025 & 2033

- Figure 30: Middle East Natural Gas Compressor Industry Revenue (Million), by Country 2025 & 2033

- Figure 31: Middle East Natural Gas Compressor Industry Revenue Share (%), by Country 2025 & 2033

- Figure 32: Saudi Arabia Natural Gas Compressor Industry Revenue (Million), by Type 2025 & 2033

- Figure 33: Saudi Arabia Natural Gas Compressor Industry Revenue Share (%), by Type 2025 & 2033

- Figure 34: Saudi Arabia Natural Gas Compressor Industry Revenue (Million), by Application 2025 & 2033

- Figure 35: Saudi Arabia Natural Gas Compressor Industry Revenue Share (%), by Application 2025 & 2033

- Figure 36: Saudi Arabia Natural Gas Compressor Industry Revenue (Million), by Country 2025 & 2033

- Figure 37: Saudi Arabia Natural Gas Compressor Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Natural Gas Compressor Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 2: Global Natural Gas Compressor Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 3: Global Natural Gas Compressor Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Global Natural Gas Compressor Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 5: Global Natural Gas Compressor Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 6: Global Natural Gas Compressor Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: United States Natural Gas Compressor Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: Canada Natural Gas Compressor Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Natural Gas Compressor Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Global Natural Gas Compressor Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 11: Global Natural Gas Compressor Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 12: Global Natural Gas Compressor Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Germany Natural Gas Compressor Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: France Natural Gas Compressor Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: Spain Natural Gas Compressor Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: United Kingdom Natural Gas Compressor Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: Rest of Europe Natural Gas Compressor Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Global Natural Gas Compressor Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 19: Global Natural Gas Compressor Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 20: Global Natural Gas Compressor Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 21: China Natural Gas Compressor Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: India Natural Gas Compressor Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 23: Malaysia Natural Gas Compressor Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: Indonesia Natural Gas Compressor Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 25: Rest of Asia Pacifc Natural Gas Compressor Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: Global Natural Gas Compressor Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 27: Global Natural Gas Compressor Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 28: Global Natural Gas Compressor Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 29: Brazil Natural Gas Compressor Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: Argentina Natural Gas Compressor Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 31: Colombia Natural Gas Compressor Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Rest of South America Natural Gas Compressor Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 33: Global Natural Gas Compressor Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 34: Global Natural Gas Compressor Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 35: Global Natural Gas Compressor Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 36: Global Natural Gas Compressor Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 37: Global Natural Gas Compressor Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 38: Global Natural Gas Compressor Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 39: United Arab Emirated Natural Gas Compressor Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 40: Nigeria Natural Gas Compressor Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 41: South Africa Natural Gas Compressor Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 42: Rest of Middle East Natural Gas Compressor Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Natural Gas Compressor Industry?

The projected CAGR is approximately 3.13%.

2. Which companies are prominent players in the Natural Gas Compressor Industry?

Key companies in the market include Atlas Corporation AB, Clean Energy Fuels Corp, Bauer Compressors Inc, Ariel Corporation, Siemens AG*List Not Exhaustive, Burckhardt Compression Holding AG, Ingersoll Rand PLC, General Electric Company, HMS Group, Howden Group Ltd.

3. What are the main segments of the Natural Gas Compressor Industry?

The market segments include Type, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.86 Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Growth in Natural Gas Consumption for Various Applications.

6. What are the notable trends driving market growth?

Midstream Sector Expected to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; Growing Penetration of Renewables in the Energy Sector.

8. Can you provide examples of recent developments in the market?

April 2023: Oilfield services specialist Baker Hughes has been awarded a contract to supply partner QatarEnergy with two main refrigerant compressors (MRCs) for Qatar's North Field South (NFS) project. Qatargas will execute the expansion project. Each MRC train will consist of three Frame 9E DLN Ultra Low NOx gas turbines and six centrifugal compressors across two LNG trains for a total scope of supply of six gas turbines to drive 12 compressors.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Natural Gas Compressor Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Natural Gas Compressor Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Natural Gas Compressor Industry?

To stay informed about further developments, trends, and reports in the Natural Gas Compressor Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence