Key Insights

The global medical liquid filter market is poised for significant expansion, projected to reach a substantial USD 3.67 billion in 2025. This growth is driven by a robust Compound Annual Growth Rate (CAGR) of 7.2% throughout the forecast period of 2025-2033. A primary catalyst for this expansion is the increasing demand for sterile and high-purity liquids in healthcare settings. Hospitals, clinics, and research institutions are increasingly investing in advanced filtration technologies to ensure patient safety, prevent infections, and enhance the accuracy of diagnostic and therapeutic procedures. The escalating prevalence of chronic diseases and the growing emphasis on minimally invasive surgeries further augment the need for sophisticated medical filtration solutions. Technological advancements, such as the development of novel membrane materials and integrated filter systems, are also contributing to market momentum by offering improved performance and efficiency.

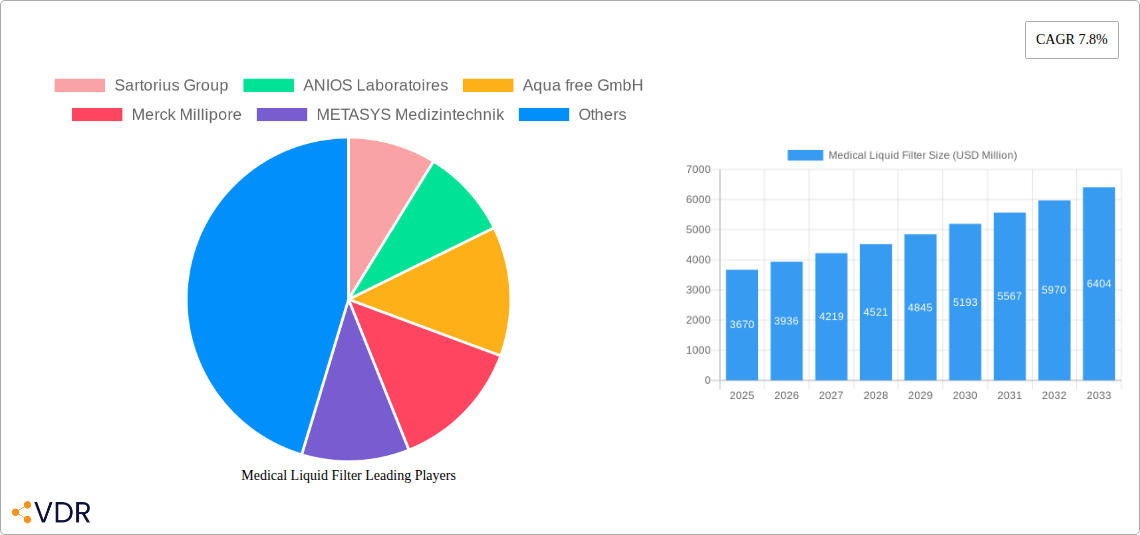

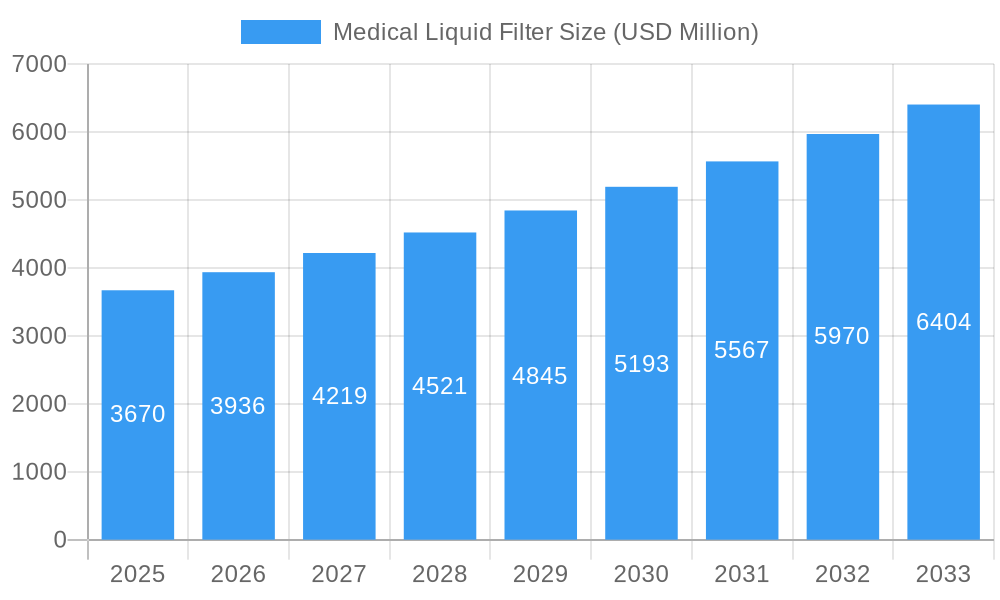

Medical Liquid Filter Market Size (In Billion)

The market segmentation by type highlights a strong preference for sterile medical liquid filters, reflecting the stringent regulatory requirements and the critical need for aseptic conditions in medical applications. While non-sterile filters find their niche in less critical applications, the demand for sterile solutions continues to dominate. Geographically, North America and Europe are anticipated to remain leading markets, owing to well-established healthcare infrastructures, high healthcare spending, and a strong presence of key market players. However, the Asia Pacific region is expected to witness the fastest growth, fueled by expanding healthcare access, increasing medical tourism, and government initiatives to upgrade healthcare facilities. Challenges such as the high cost of advanced filtration systems and stringent regulatory approvals can temper growth, but the overwhelming need for reliable and efficient medical liquid filtration solutions is set to ensure a dynamic and expanding market.

Medical Liquid Filter Company Market Share

This in-depth report provides a detailed examination of the global Medical Liquid Filter market, encompassing its historical performance, current dynamics, and future trajectory. With a study period spanning from 2019 to 2033, and a base year of 2025, this analysis offers critical insights for stakeholders seeking to understand the market's evolution, growth drivers, and competitive landscape. The report delves into parent and child market segmentation, key player strategies, technological advancements, and emerging opportunities, providing a holistic view of this vital healthcare segment.

Medical Liquid Filter Market Dynamics & Structure

The global Medical Liquid Filter market is characterized by a moderate to high concentration, driven by significant technological innovation and a complex regulatory landscape. Key drivers include the increasing demand for sterile processing in hospitals and clinics, advancements in membrane technology, and the growing prevalence of chronic diseases requiring advanced medical treatments. Competitive product substitutes, while present, are largely confined to specific niche applications, with the core market dominated by advanced filtration solutions. End-user demographics are shifting towards an aging global population with greater healthcare needs, and a rising middle class in emerging economies demanding higher quality medical care. Mergers and acquisitions (M&A) are a significant trend, as larger players seek to consolidate market share, acquire innovative technologies, and expand their product portfolios. For instance, in the historical period (2019-2024), there were approximately 15 M&A deals valued at over $1.5 billion collectively, indicating strategic consolidation within the industry. Innovation barriers include the stringent regulatory approval processes and the high cost of research and development for advanced filtration materials.

- Market Concentration: Moderate to high, with a few key players holding substantial market share.

- Technological Innovation Drivers: Advancements in membrane science, microfluidics, and materials engineering.

- Regulatory Frameworks: Stringent FDA, EMA, and other regional body approvals for medical devices.

- Competitive Product Substitutes: Limited in core applications, primarily focused on basic filtration needs.

- End-User Demographics: Aging population, rising chronic disease rates, increasing healthcare expenditure.

- M&A Trends: Strategic acquisitions for technology, market access, and portfolio expansion.

Medical Liquid Filter Growth Trends & Insights

The Medical Liquid Filter market is poised for robust growth, projected to expand at a Compound Annual Growth Rate (CAGR) of approximately 7.5% from 2025 to 2033. This growth is underpinned by a consistent increase in healthcare expenditure globally and a heightened awareness of infection control protocols across healthcare settings. The adoption rate of advanced sterile filtration solutions is accelerating, particularly in developed nations, driven by the need to prevent healthcare-associated infections (HAIs) and ensure the safety of parenteral drug administration and biopharmaceutical production. Technological disruptions, such as the development of novel filter materials with enhanced pore size control and improved flow rates, are further propelling market penetration. Consumer behavior shifts are also playing a crucial role, with healthcare providers and patients increasingly prioritizing product safety and efficacy, which directly translates into demand for high-performance medical liquid filters. The market size, valued at $8.2 billion in the base year of 2025, is anticipated to reach $14.5 billion by 2033. Key growth drivers include the expanding biopharmaceutical industry, the increasing use of advanced diagnostics and therapeutics, and the growing demand for single-use filtration systems. The market penetration of advanced medical liquid filters is estimated to be around 65% in developed countries and is projected to grow by another 10% over the forecast period.

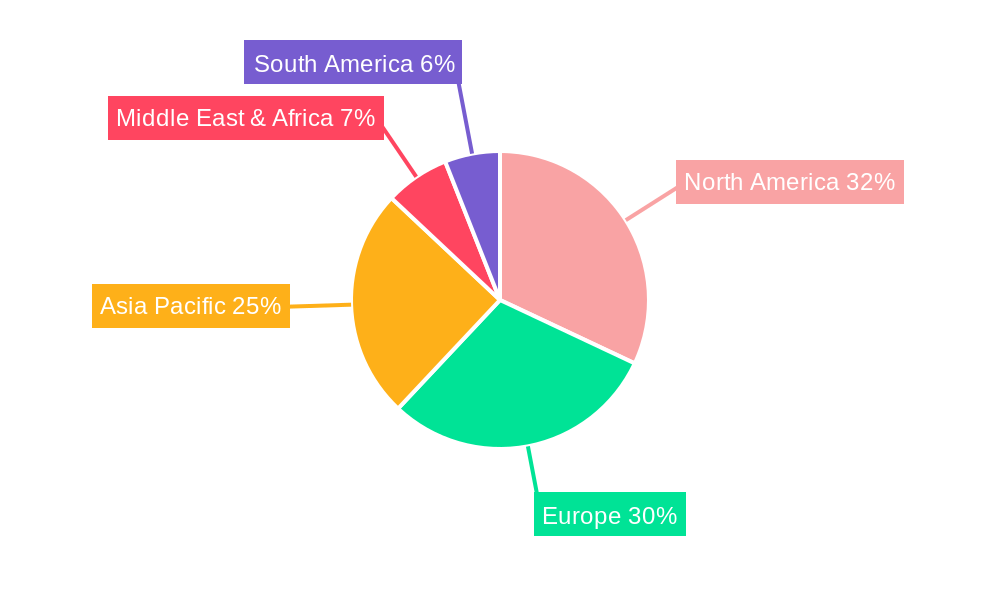

Dominant Regions, Countries, or Segments in Medical Liquid Filter

The Hospital segment, within the Application category, stands as the dominant force driving the Medical Liquid Filter market's growth. Hospitals, representing approximately 55% of the total market share in 2025, are primary consumers due to their extensive use of sterile filtration in critical applications like intravenous fluid preparation, blood product processing, and drug compounding. North America, spearheaded by the United States, holds the largest regional market share, estimated at 38% in 2025, owing to its advanced healthcare infrastructure, high per capita healthcare spending, and stringent regulatory standards. The Sterile type of medical liquid filter also commands a significant market share, estimated at 70% in 2025, reflecting the paramount importance of sterility in preventing infections within clinical settings. Key drivers for hospital segment dominance include the increasing volume of complex surgical procedures, the rising incidence of immunocompromised patients requiring meticulous care, and the continuous influx of new medical technologies demanding sterile fluid handling. Economic policies in North America, such as government incentives for improving patient safety and infection control, further bolster the region's leadership. Additionally, the robust presence of leading medical device manufacturers and research institutions in the United States fosters a conducive environment for innovation and market adoption.

- Dominant Application Segment: Hospital, accounting for approximately 55% of the market share in 2025.

- Leading Region: North America, with the United States being the primary market contributor.

- Dominant Filter Type: Sterile filters, holding an estimated 70% market share in 2025.

- Key Drivers in Hospitals: High volume of sterile procedures, immunocompromised patient population, adoption of advanced medical technologies.

- Economic Policies: Government initiatives for patient safety and infection control.

- Growth Potential: Continued expansion driven by aging populations and increasing demand for advanced medical treatments.

Medical Liquid Filter Product Landscape

The Medical Liquid Filter product landscape is characterized by continuous innovation focused on enhancing filtration efficiency, reducing particle retention, and improving fluid compatibility. Key product advancements include the development of filters with sub-micron pore sizes for ultra-purification of pharmaceutical solutions and innovative membrane materials that offer superior chemical resistance and higher throughput. Applications range from sterile filtration of intravenous solutions and biopharmaceutical products to filtration of diagnostic reagents and cell culture media. Performance metrics such as extractable levels, bacterial retention efficiency, and pressure drop are critical selling points. For instance, new generations of hydrophilic polyvinylidene fluoride (PVDF) filters offer exceptional clarity and sterility assurance for sensitive biologics, while hydrophobic polytetrafluoroethylene (PTFE) filters provide excellent chemical compatibility for aggressive solvent filtration in research settings. The integration of single-use technologies is also a prominent trend, minimizing cross-contamination risks and streamlining workflows in pharmaceutical manufacturing.

Key Drivers, Barriers & Challenges in Medical Liquid Filter

Key Drivers: The Medical Liquid Filter market is propelled by escalating global healthcare expenditures, a rising incidence of hospital-acquired infections demanding robust prevention strategies, and rapid advancements in biopharmaceutical and medical device industries. The increasing adoption of disposable filtration systems, driven by convenience and reduced risk of cross-contamination, further fuels market growth. Technological breakthroughs in membrane science, such as enhanced pore size uniformity and improved flow characteristics, are also significant accelerators.

- Rising Healthcare Spending: Increased investment in healthcare infrastructure and services.

- Infection Control Mandates: Growing emphasis on preventing HAIs.

- Biopharmaceutical Growth: Expansion of biologics manufacturing and drug development.

- Disposable Filter Adoption: Preference for single-use systems.

- Membrane Technology Advancements: Improved filtration performance and efficiency.

Barriers & Challenges: Stringent regulatory approval processes in major markets present a significant hurdle, requiring extensive validation and testing. The high cost associated with research, development, and manufacturing of advanced medical filters can also limit market entry for smaller companies. Supply chain disruptions, particularly for specialized raw materials, can impact production volumes and lead times. Furthermore, intense competition and price pressures from established players can pose a challenge for new entrants.

- Regulatory Hurdles: Lengthy and costly approval processes.

- High R&D and Manufacturing Costs: Significant investment required for advanced filtration.

- Supply Chain Volatility: Potential disruptions in raw material sourcing.

- Competitive Pricing: Pressure from established market players.

- Intellectual Property Protection: Challenges in safeguarding proprietary technologies.

Emerging Opportunities in Medical Liquid Filter

Emerging opportunities lie in the burgeoning field of personalized medicine, which demands highly specialized and precise filtration for patient-specific therapies. The increasing demand for point-of-care diagnostics also presents a significant growth avenue, requiring compact and efficient filtration solutions. Furthermore, the development of bio-compatible and degradable filter materials for regenerative medicine applications holds immense potential. Untapped markets in developing economies, with their rapidly expanding healthcare infrastructure, offer substantial growth prospects for affordable and effective medical liquid filter solutions.

- Personalized Medicine: Tailored filtration for patient-specific treatments.

- Point-of-Care Diagnostics: Development of compact filtration systems.

- Regenerative Medicine: Bio-compatible and degradable filter materials.

- Emerging Markets: Expansion into regions with growing healthcare needs.

- Advanced Sterilization Techniques: Integration with novel sterilization methods.

Growth Accelerators in the Medical Liquid Filter Industry

Long-term growth in the Medical Liquid Filter industry will be significantly accelerated by ongoing technological breakthroughs in nanofiltration and ultrafiltration, enabling even finer levels of purification for critical biopharmaceutical applications. Strategic partnerships between filter manufacturers and pharmaceutical companies are also crucial, fostering co-development of customized filtration solutions that meet evolving drug manufacturing requirements. Market expansion strategies, particularly targeting niche applications and underserved geographic regions, will further drive sustained growth. The increasing focus on sustainability within the healthcare sector is also creating opportunities for the development of eco-friendly filtration solutions and improved recyclability of filter components.

Key Players Shaping the Medical Liquid Filter Market

- Sartorius Group

- ANIOS Laboratoires

- Aqua free GmbH

- Merck Millipore

- METASYS Medizintechnik

- Asahi Kasei Medical

- Dürr Dental

- Terumo BCT

- BGS GENERAL

- Cantel

- Frisenette ApS

- GVS

- The West Group Ltd

- HAEMONETICS

- Hangzhou Tailin Bioengineering Equipments

- I3 Membrane GmbH

- Kaneka Pharma

- Kapsam Health Products

- Kawasumi

- MACHEREY-NAGEL

- MDG Engineering Srl

- MEDICA

- Nuova SB System Srl

- PURIBLOOD MEDICAL CO.,LTD.

Notable Milestones in Medical Liquid Filter Sector

- 2019: Introduction of next-generation sterile filters with enhanced throughput and reduced footprint by Sartorius Group, boosting biopharmaceutical manufacturing efficiency.

- 2020: Merck Millipore launched a new line of hydrophilic PTFE filters offering superior chemical compatibility for challenging solvent applications in research and development.

- 2021: Asahi Kasei Medical expanded its bioprocess filtration portfolio with advanced tangential flow filtration (TFF) systems, enhancing downstream processing capabilities.

- 2022: Cantel acquired a prominent supplier of disposable medical filters, consolidating its market position and expanding its product offerings in infection prevention.

- 2023: GVS introduced innovative microfiltration membranes with improved pore integrity and higher bio-burden removal capabilities for critical medical device applications.

- 2024 (Early): ANIOS Laboratoires announced significant advancements in antimicrobial filtration technology for hospital environments, aiming to reduce the incidence of HAIs.

In-Depth Medical Liquid Filter Market Outlook

The Medical Liquid Filter market outlook is exceptionally promising, driven by an unwavering commitment to patient safety and the relentless pursuit of therapeutic advancements. The forecast period from 2025 to 2033 anticipates sustained growth, fueled by strategic investments in research and development, expansion into emerging economies, and the increasing adoption of sophisticated filtration technologies. Growth accelerators such as the burgeoning biologics market, the rise of advanced diagnostics, and a global emphasis on stringent infection control will continue to propel demand. The market is expected to witness further consolidation through strategic M&A activities, leading to more integrated product offerings and enhanced market reach. Opportunities for innovation remain vast, particularly in areas like personalized medicine, point-of-care solutions, and sustainable filtration technologies, ensuring the Medical Liquid Filter market's continued evolution and its indispensable role in modern healthcare.

Medical Liquid Filter Segmentation

-

1. Application

- 1.1. Hospital

- 1.2. Clinic

- 1.3. Research Institutes

- 1.4. Other

-

2. Types

- 2.1. Sterile

- 2.2. Non-sterile

Medical Liquid Filter Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Medical Liquid Filter Regional Market Share

Geographic Coverage of Medical Liquid Filter

Medical Liquid Filter REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Medical Liquid Filter Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Hospital

- 5.1.2. Clinic

- 5.1.3. Research Institutes

- 5.1.4. Other

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Sterile

- 5.2.2. Non-sterile

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Medical Liquid Filter Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Hospital

- 6.1.2. Clinic

- 6.1.3. Research Institutes

- 6.1.4. Other

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Sterile

- 6.2.2. Non-sterile

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Medical Liquid Filter Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Hospital

- 7.1.2. Clinic

- 7.1.3. Research Institutes

- 7.1.4. Other

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Sterile

- 7.2.2. Non-sterile

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Medical Liquid Filter Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Hospital

- 8.1.2. Clinic

- 8.1.3. Research Institutes

- 8.1.4. Other

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Sterile

- 8.2.2. Non-sterile

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Medical Liquid Filter Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Hospital

- 9.1.2. Clinic

- 9.1.3. Research Institutes

- 9.1.4. Other

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Sterile

- 9.2.2. Non-sterile

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Medical Liquid Filter Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Hospital

- 10.1.2. Clinic

- 10.1.3. Research Institutes

- 10.1.4. Other

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Sterile

- 10.2.2. Non-sterile

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Sartorius Group

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 ANIOS Laboratoires

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Aqua free GmbH

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Merck Millipore

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 METASYS Medizintechnik

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Asahi Kasei Medical

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Dürr Dental

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Terumo BCT

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 BGS GENERAL

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Cantel

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Frisenette ApS

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 GVS

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 The West Group Ltd

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 HAEMONETICS

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Hangzhou Tailin Bioengineering Equipments

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 I3 Membrane GmbH

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Kaneka Pharma

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Kapsam Health Products

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 Kawasumi

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 MACHEREY-NAGEL

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.21 MDG Engineering Srl

- 11.2.21.1. Overview

- 11.2.21.2. Products

- 11.2.21.3. SWOT Analysis

- 11.2.21.4. Recent Developments

- 11.2.21.5. Financials (Based on Availability)

- 11.2.22 MEDICA

- 11.2.22.1. Overview

- 11.2.22.2. Products

- 11.2.22.3. SWOT Analysis

- 11.2.22.4. Recent Developments

- 11.2.22.5. Financials (Based on Availability)

- 11.2.23 Nuova SB System Srl

- 11.2.23.1. Overview

- 11.2.23.2. Products

- 11.2.23.3. SWOT Analysis

- 11.2.23.4. Recent Developments

- 11.2.23.5. Financials (Based on Availability)

- 11.2.24 PURIBLOOD MEDICAL CO.

- 11.2.24.1. Overview

- 11.2.24.2. Products

- 11.2.24.3. SWOT Analysis

- 11.2.24.4. Recent Developments

- 11.2.24.5. Financials (Based on Availability)

- 11.2.25 LTD.

- 11.2.25.1. Overview

- 11.2.25.2. Products

- 11.2.25.3. SWOT Analysis

- 11.2.25.4. Recent Developments

- 11.2.25.5. Financials (Based on Availability)

- 11.2.1 Sartorius Group

List of Figures

- Figure 1: Global Medical Liquid Filter Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Medical Liquid Filter Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Medical Liquid Filter Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Medical Liquid Filter Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Medical Liquid Filter Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Medical Liquid Filter Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Medical Liquid Filter Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Medical Liquid Filter Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Medical Liquid Filter Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Medical Liquid Filter Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Medical Liquid Filter Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Medical Liquid Filter Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Medical Liquid Filter Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Medical Liquid Filter Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Medical Liquid Filter Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Medical Liquid Filter Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Medical Liquid Filter Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Medical Liquid Filter Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Medical Liquid Filter Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Medical Liquid Filter Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Medical Liquid Filter Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Medical Liquid Filter Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Medical Liquid Filter Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Medical Liquid Filter Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Medical Liquid Filter Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Medical Liquid Filter Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Medical Liquid Filter Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Medical Liquid Filter Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Medical Liquid Filter Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Medical Liquid Filter Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Medical Liquid Filter Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Medical Liquid Filter Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Medical Liquid Filter Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Medical Liquid Filter Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Medical Liquid Filter Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Medical Liquid Filter Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Medical Liquid Filter Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Medical Liquid Filter Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Medical Liquid Filter Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Medical Liquid Filter Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Medical Liquid Filter Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Medical Liquid Filter Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Medical Liquid Filter Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Medical Liquid Filter Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Medical Liquid Filter Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Medical Liquid Filter Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Medical Liquid Filter Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Medical Liquid Filter Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Medical Liquid Filter Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Medical Liquid Filter Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Medical Liquid Filter Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Medical Liquid Filter Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Medical Liquid Filter Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Medical Liquid Filter Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Medical Liquid Filter Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Medical Liquid Filter Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Medical Liquid Filter Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Medical Liquid Filter Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Medical Liquid Filter Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Medical Liquid Filter Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Medical Liquid Filter Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Medical Liquid Filter Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Medical Liquid Filter Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Medical Liquid Filter Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Medical Liquid Filter Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Medical Liquid Filter Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Medical Liquid Filter Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Medical Liquid Filter Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Medical Liquid Filter Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Medical Liquid Filter Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Medical Liquid Filter Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Medical Liquid Filter Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Medical Liquid Filter Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Medical Liquid Filter Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Medical Liquid Filter Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Medical Liquid Filter Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Medical Liquid Filter Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Medical Liquid Filter?

The projected CAGR is approximately 6.3%.

2. Which companies are prominent players in the Medical Liquid Filter?

Key companies in the market include Sartorius Group, ANIOS Laboratoires, Aqua free GmbH, Merck Millipore, METASYS Medizintechnik, Asahi Kasei Medical, Dürr Dental, Terumo BCT, BGS GENERAL, Cantel, Frisenette ApS, GVS, The West Group Ltd, HAEMONETICS, Hangzhou Tailin Bioengineering Equipments, I3 Membrane GmbH, Kaneka Pharma, Kapsam Health Products, Kawasumi, MACHEREY-NAGEL, MDG Engineering Srl, MEDICA, Nuova SB System Srl, PURIBLOOD MEDICAL CO., LTD..

3. What are the main segments of the Medical Liquid Filter?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Medical Liquid Filter," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Medical Liquid Filter report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Medical Liquid Filter?

To stay informed about further developments, trends, and reports in the Medical Liquid Filter, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence