Key Insights

The global meat, poultry, and seafood packaging market is poised for significant expansion, driven by robust consumer demand for convenient, safe, and sustainable solutions. With a projected Compound Annual Growth Rate (CAGR) of 5.2%, the market is expected to reach $15.62 billion by 2025. Key growth drivers include a rising global population, increasing demand for processed and ready-to-eat meals, and a strong emphasis on extending the shelf life of perishable products. The growing adoption of sustainable packaging materials, such as biodegradable and recyclable options, is also a significant contributor. While polypropylene (PP) and polystyrene (PS) currently dominate material types due to cost-effectiveness, environmental concerns are fostering a shift towards alternatives like PET and bio-based materials. The application segment is characterized by high demand for fresh and frozen products, processed foods, and ready-to-eat meals. Rigid packaging holds a larger share due to superior protection, though flexible options are gaining traction. Leading players are driving innovation and market dynamics through strategic acquisitions and advancements in barrier technologies and smart packaging solutions. While North America and Europe are established markets, the Asia-Pacific region offers substantial growth potential driven by economic development and rising disposable incomes. Challenges include fluctuating raw material prices and stringent regulatory requirements.

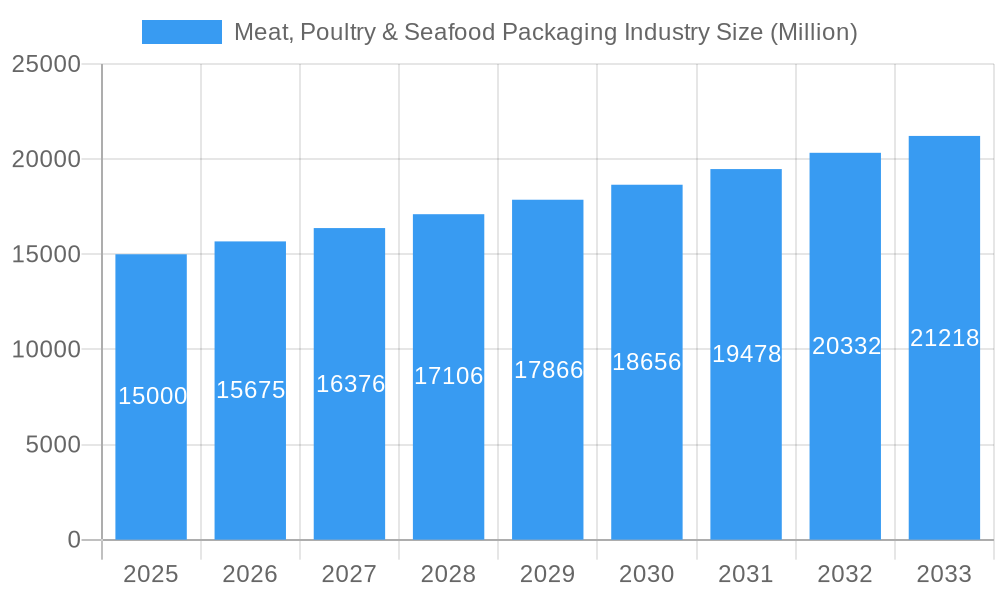

Meat, Poultry & Seafood Packaging Industry Market Size (In Billion)

The competitive landscape features a mix of multinational corporations and specialized firms focused on innovative packaging to meet evolving consumer preferences and sustainability goals. Advancements in barrier technologies and smart packaging are enhancing product freshness and providing consumers with real-time quality information. Strategic partnerships and mergers & acquisitions are key to expanding market reach and strengthening supply chains. While precise market figures for 2025 and beyond are subject to further data analysis, current trends and CAGR indicate substantial market value growth. Regional growth will be influenced by economic development, regulatory shifts, and consumer behavior, making a nuanced understanding of each market essential for successful penetration and sustainable growth.

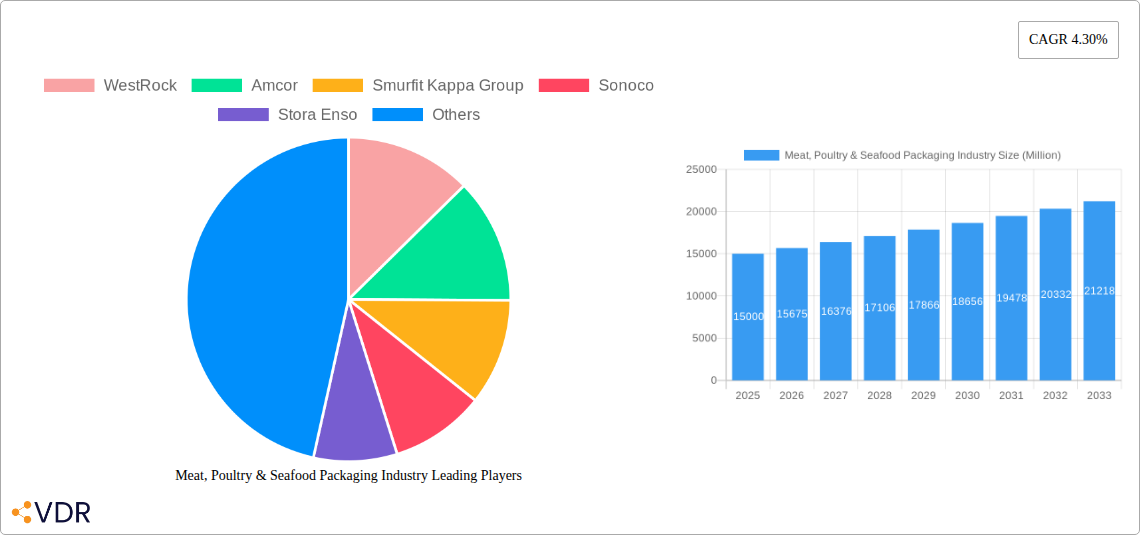

Meat, Poultry & Seafood Packaging Industry Company Market Share

Meat, Poultry & Seafood Packaging Industry: Market Analysis & Forecast 2019-2033

This comprehensive report provides a detailed analysis of the Meat, Poultry & Seafood Packaging market, encompassing market size, growth trends, competitive landscape, and future outlook. The study period covers 2019-2033, with 2025 as the base year and a forecast period of 2025-2033. The report offers invaluable insights for industry professionals, investors, and stakeholders seeking to understand and capitalize on opportunities within this dynamic sector. The market is segmented by material type, application, packaging type, and product type, providing a granular view of market dynamics. The total market value in 2025 is estimated at XX Million units.

Meat, Poultry & Seafood Packaging Industry Market Dynamics & Structure

The Meat, Poultry & Seafood Packaging market is characterized by a moderately consolidated structure with several major players holding significant market share. WestRock, Amcor, Smurfit Kappa Group, Sonoco, Stora Enso, Mondi Group, Can-Pack SA, Crown Holdings, Berry Global, DS Smith, and Sealed Air are some of the key players shaping the landscape. However, the market also includes numerous smaller regional players, particularly in developing economies.

- Market Concentration: The top 5 players hold an estimated xx% market share in 2025, indicating a moderately concentrated market.

- Technological Innovation: Drivers include advancements in barrier technologies, sustainable packaging solutions (e.g., recyclable and compostable materials), and smart packaging incorporating sensors for improved food safety and shelf-life. Barriers include high R&D costs and the need for regulatory approvals for new materials.

- Regulatory Frameworks: Growing emphasis on food safety regulations and sustainability mandates influences packaging choices and material selection. Compliance costs and potential for penalties act as constraints.

- Competitive Product Substitutes: Alternatives include modified atmosphere packaging (MAP) and vacuum packaging, impacting the demand for traditional packaging formats.

- End-User Demographics: Changing consumer preferences, particularly towards convenience and sustainability, drive demand for innovative packaging solutions.

- M&A Trends: The industry witnesses strategic mergers and acquisitions to enhance market share, expand product portfolios, and access new technologies. An estimated xx M&A deals occurred between 2019 and 2024, with a projected xx deals for 2025-2033.

Meat, Poultry & Seafood Packaging Industry Growth Trends & Insights

The global Meat, Poultry & Seafood Packaging market has experienced steady growth over the past few years, driven by factors such as increasing meat consumption, expansion of the processed food industry, and rising demand for convenient ready-to-eat meals. The market size was valued at approximately XX Million units in 2019, rising to XX Million units in 2024 and is projected to reach XX Million units by 2033, showcasing a Compound Annual Growth Rate (CAGR) of xx% during the forecast period. This growth is fuelled by several key trends: Increased adoption of flexible packaging for its cost-effectiveness and convenience. Rising demand for sustainable and eco-friendly packaging solutions, prompted by growing environmental concerns. Technological advancements leading to innovative packaging materials and designs. The shift in consumer preferences toward ready-to-eat meals and convenience products further fuels market growth. Market penetration of innovative packaging solutions, such as modified atmosphere packaging (MAP) and active packaging, continues to increase, further contributing to market expansion. The projected growth trajectory incorporates considerations for potential economic fluctuations and evolving consumer behavior.

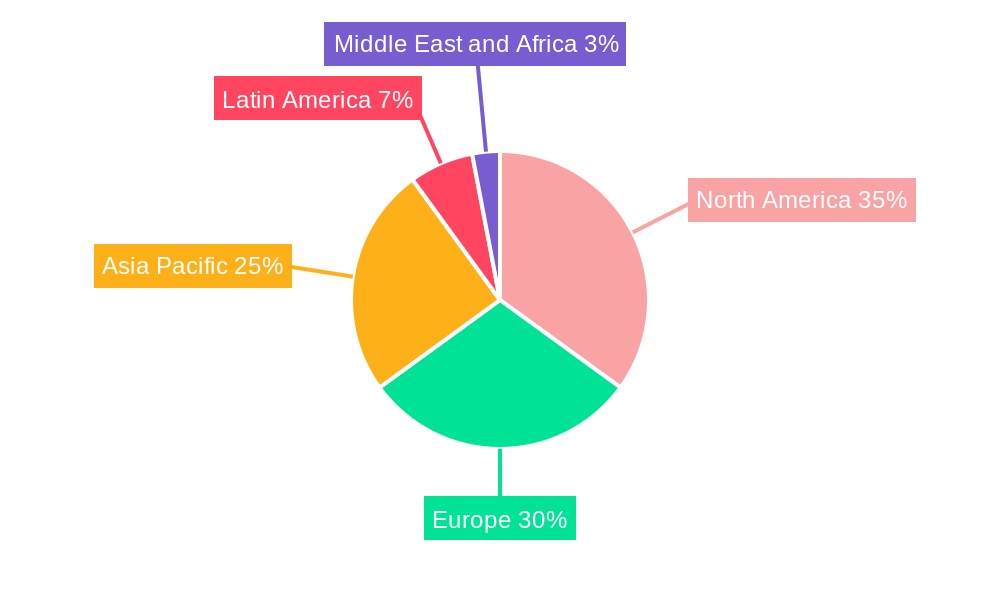

Dominant Regions, Countries, or Segments in Meat, Poultry & Seafood Packaging Industry

The North American and European regions currently dominate the Meat, Poultry & Seafood Packaging market due to high meat consumption, established food processing industries, and stringent food safety regulations. However, Asia-Pacific is expected to witness the fastest growth during the forecast period, driven by rising disposable incomes, urbanization, and increasing demand for convenience foods.

Leading Segments:

- Material Type: Flexible packaging (primarily Polypropylene (PP) and Polyester (PET)) currently holds the largest market share, driven by its cost-effectiveness and versatility. However, demand for sustainable alternatives like Aluminium and other eco-friendly materials is increasing.

- Application: Fresh and frozen products dominate the application segment due to higher volume compared to processed and ready-to-eat products.

- Packaging Type: Flexible packaging holds a larger market share than rigid packaging due to its adaptability and reduced material usage.

- Product Type: Containers represent the dominant product type due to their wide application across various meat, poultry, and seafood products.

Key Growth Drivers:

- Economic Growth: Rising disposable incomes, especially in developing economies, drive demand for packaged meat, poultry, and seafood.

- Infrastructure Development: Improved cold chain infrastructure enhances the preservation and distribution of perishable food products, further boosting packaging demand.

- Government Regulations: Stringent food safety and labeling regulations promote the use of high-quality, safe packaging materials.

Meat, Poultry & Seafood Packaging Industry Product Landscape

The Meat, Poultry & Seafood Packaging market offers a diverse range of products, encompassing rigid and flexible packaging solutions made from various materials like polypropylene (PP), polystyrene (PS), polyester (PET), thermoform, aluminum, and other materials. Recent innovations focus on improving barrier properties, extending shelf life, enhancing product preservation, and minimizing environmental impact. Unique selling propositions include improved recyclability, enhanced shelf appeal, and functionalities such as modified atmosphere packaging (MAP) and active packaging that extend the product’s life. Technological advancements like high-speed printing, advanced lamination techniques, and automated packaging systems drive efficiency and cost reductions.

Key Drivers, Barriers & Challenges in Meat, Poultry & Seafood Packaging Industry

Key Drivers:

- Growing demand for convenient and ready-to-eat meals.

- Increasing focus on food safety and hygiene.

- Rising consumer preference for sustainable and eco-friendly packaging.

- Technological advancements leading to innovative packaging solutions.

Challenges & Restraints:

- Fluctuations in raw material prices, impacting production costs.

- Stringent regulations and compliance requirements.

- Growing competition from other packaging types.

- Supply chain disruptions impacting production and distribution. An estimated xx% decrease in production output was observed in 2022 due to supply chain bottlenecks.

Emerging Opportunities in Meat, Poultry & Seafood Packaging Industry

- Expanding into emerging markets with high growth potential.

- Developing innovative packaging solutions for specific product types and applications.

- Focusing on sustainable and eco-friendly packaging options to meet evolving consumer demand.

- Exploring opportunities in smart packaging technologies for improved product traceability and food safety.

Growth Accelerators in the Meat, Poultry & Seafood Packaging Industry Industry

Long-term growth will be fueled by continuous innovation in materials science and packaging technologies, creating sustainable and cost-effective solutions. Strategic partnerships between packaging companies and food producers will facilitate the development and adoption of new technologies. Expansion into untapped markets, particularly in developing regions, will unlock significant growth potential.

Key Players Shaping the Meat, Poultry & Seafood Packaging Market

- WestRock

- Amcor

- Smurfit Kappa Group

- Sonoco

- Stora Enso

- Mondi Group

- Can-Pack SA

- Crown Holdings

- Berry Global

- DS Smith

- Sealed Air

Notable Milestones in Meat, Poultry & Seafood Packaging Industry Sector

- December 2022: Amcor opened a new state-of-the-art flexible packaging plant in Huizhou, China, significantly boosting its capacity in the Asia-Pacific region.

- October 2022: Berry Global and Printpack partnered to introduce the Preserve PE PCR recyclable polyethylene pouch, highlighting a commitment to sustainable packaging solutions.

In-Depth Meat, Poultry & Seafood Packaging Industry Market Outlook

The Meat, Poultry & Seafood Packaging market presents significant opportunities for growth over the coming years, driven by factors like increasing consumption, innovation in packaging materials, and a rising focus on sustainability. Strategic investments in R&D and strategic partnerships will be crucial for companies seeking to capitalize on this expanding market. The focus on sustainable and eco-friendly packaging will continue to drive demand. Companies that can adapt to changing consumer demands and technological advancements will be well-positioned for success.

Meat, Poultry & Seafood Packaging Industry Segmentation

-

1. Packaging Type

- 1.1. Rigid Packaging

- 1.2. Flexible Packaging

-

2. Product Type

-

2.1. Containers

- 2.1.1. Aluminium Foil Container

- 2.1.2. Plastic Container

- 2.1.3. Board Container

- 2.2. Pre-made Bags

- 2.3. Food Cans

- 2.4. Coated Films

- 2.5. Other Product Types

-

2.1. Containers

-

3. Material Type

- 3.1. Polypropylene (PP)

- 3.2. Polystrene (PS)

- 3.3. Polyester (PET)

- 3.4. Thermoform

- 3.5. Aluminium

- 3.6. Other Material Types

-

4. Application

- 4.1. Fresh and Frozen Products

- 4.2. Processed Products

- 4.3. Read-to-eat Products

Meat, Poultry & Seafood Packaging Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Latin America

- 5. Middle East and Africa

Meat, Poultry & Seafood Packaging Industry Regional Market Share

Geographic Coverage of Meat, Poultry & Seafood Packaging Industry

Meat, Poultry & Seafood Packaging Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Packaging Type

- 5.1.1. Rigid Packaging

- 5.1.2. Flexible Packaging

- 5.2. Market Analysis, Insights and Forecast - by Product Type

- 5.2.1. Containers

- 5.2.1.1. Aluminium Foil Container

- 5.2.1.2. Plastic Container

- 5.2.1.3. Board Container

- 5.2.2. Pre-made Bags

- 5.2.3. Food Cans

- 5.2.4. Coated Films

- 5.2.5. Other Product Types

- 5.2.1. Containers

- 5.3. Market Analysis, Insights and Forecast - by Material Type

- 5.3.1. Polypropylene (PP)

- 5.3.2. Polystrene (PS)

- 5.3.3. Polyester (PET)

- 5.3.4. Thermoform

- 5.3.5. Aluminium

- 5.3.6. Other Material Types

- 5.4. Market Analysis, Insights and Forecast - by Application

- 5.4.1. Fresh and Frozen Products

- 5.4.2. Processed Products

- 5.4.3. Read-to-eat Products

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. North America

- 5.5.2. Europe

- 5.5.3. Asia Pacific

- 5.5.4. Latin America

- 5.5.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Packaging Type

- 6. Global Meat, Poultry & Seafood Packaging Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Packaging Type

- 6.1.1. Rigid Packaging

- 6.1.2. Flexible Packaging

- 6.2. Market Analysis, Insights and Forecast - by Product Type

- 6.2.1. Containers

- 6.2.1.1. Aluminium Foil Container

- 6.2.1.2. Plastic Container

- 6.2.1.3. Board Container

- 6.2.2. Pre-made Bags

- 6.2.3. Food Cans

- 6.2.4. Coated Films

- 6.2.5. Other Product Types

- 6.2.1. Containers

- 6.3. Market Analysis, Insights and Forecast - by Material Type

- 6.3.1. Polypropylene (PP)

- 6.3.2. Polystrene (PS)

- 6.3.3. Polyester (PET)

- 6.3.4. Thermoform

- 6.3.5. Aluminium

- 6.3.6. Other Material Types

- 6.4. Market Analysis, Insights and Forecast - by Application

- 6.4.1. Fresh and Frozen Products

- 6.4.2. Processed Products

- 6.4.3. Read-to-eat Products

- 6.1. Market Analysis, Insights and Forecast - by Packaging Type

- 7. North America Meat, Poultry & Seafood Packaging Industry Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Packaging Type

- 7.1.1. Rigid Packaging

- 7.1.2. Flexible Packaging

- 7.2. Market Analysis, Insights and Forecast - by Product Type

- 7.2.1. Containers

- 7.2.1.1. Aluminium Foil Container

- 7.2.1.2. Plastic Container

- 7.2.1.3. Board Container

- 7.2.2. Pre-made Bags

- 7.2.3. Food Cans

- 7.2.4. Coated Films

- 7.2.5. Other Product Types

- 7.2.1. Containers

- 7.3. Market Analysis, Insights and Forecast - by Material Type

- 7.3.1. Polypropylene (PP)

- 7.3.2. Polystrene (PS)

- 7.3.3. Polyester (PET)

- 7.3.4. Thermoform

- 7.3.5. Aluminium

- 7.3.6. Other Material Types

- 7.4. Market Analysis, Insights and Forecast - by Application

- 7.4.1. Fresh and Frozen Products

- 7.4.2. Processed Products

- 7.4.3. Read-to-eat Products

- 7.1. Market Analysis, Insights and Forecast - by Packaging Type

- 8. Europe Meat, Poultry & Seafood Packaging Industry Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Packaging Type

- 8.1.1. Rigid Packaging

- 8.1.2. Flexible Packaging

- 8.2. Market Analysis, Insights and Forecast - by Product Type

- 8.2.1. Containers

- 8.2.1.1. Aluminium Foil Container

- 8.2.1.2. Plastic Container

- 8.2.1.3. Board Container

- 8.2.2. Pre-made Bags

- 8.2.3. Food Cans

- 8.2.4. Coated Films

- 8.2.5. Other Product Types

- 8.2.1. Containers

- 8.3. Market Analysis, Insights and Forecast - by Material Type

- 8.3.1. Polypropylene (PP)

- 8.3.2. Polystrene (PS)

- 8.3.3. Polyester (PET)

- 8.3.4. Thermoform

- 8.3.5. Aluminium

- 8.3.6. Other Material Types

- 8.4. Market Analysis, Insights and Forecast - by Application

- 8.4.1. Fresh and Frozen Products

- 8.4.2. Processed Products

- 8.4.3. Read-to-eat Products

- 8.1. Market Analysis, Insights and Forecast - by Packaging Type

- 9. Asia Pacific Meat, Poultry & Seafood Packaging Industry Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Packaging Type

- 9.1.1. Rigid Packaging

- 9.1.2. Flexible Packaging

- 9.2. Market Analysis, Insights and Forecast - by Product Type

- 9.2.1. Containers

- 9.2.1.1. Aluminium Foil Container

- 9.2.1.2. Plastic Container

- 9.2.1.3. Board Container

- 9.2.2. Pre-made Bags

- 9.2.3. Food Cans

- 9.2.4. Coated Films

- 9.2.5. Other Product Types

- 9.2.1. Containers

- 9.3. Market Analysis, Insights and Forecast - by Material Type

- 9.3.1. Polypropylene (PP)

- 9.3.2. Polystrene (PS)

- 9.3.3. Polyester (PET)

- 9.3.4. Thermoform

- 9.3.5. Aluminium

- 9.3.6. Other Material Types

- 9.4. Market Analysis, Insights and Forecast - by Application

- 9.4.1. Fresh and Frozen Products

- 9.4.2. Processed Products

- 9.4.3. Read-to-eat Products

- 9.1. Market Analysis, Insights and Forecast - by Packaging Type

- 10. Latin America Meat, Poultry & Seafood Packaging Industry Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Packaging Type

- 10.1.1. Rigid Packaging

- 10.1.2. Flexible Packaging

- 10.2. Market Analysis, Insights and Forecast - by Product Type

- 10.2.1. Containers

- 10.2.1.1. Aluminium Foil Container

- 10.2.1.2. Plastic Container

- 10.2.1.3. Board Container

- 10.2.2. Pre-made Bags

- 10.2.3. Food Cans

- 10.2.4. Coated Films

- 10.2.5. Other Product Types

- 10.2.1. Containers

- 10.3. Market Analysis, Insights and Forecast - by Material Type

- 10.3.1. Polypropylene (PP)

- 10.3.2. Polystrene (PS)

- 10.3.3. Polyester (PET)

- 10.3.4. Thermoform

- 10.3.5. Aluminium

- 10.3.6. Other Material Types

- 10.4. Market Analysis, Insights and Forecast - by Application

- 10.4.1. Fresh and Frozen Products

- 10.4.2. Processed Products

- 10.4.3. Read-to-eat Products

- 10.1. Market Analysis, Insights and Forecast - by Packaging Type

- 11. Middle East and Africa Meat, Poultry & Seafood Packaging Industry Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Packaging Type

- 11.1.1. Rigid Packaging

- 11.1.2. Flexible Packaging

- 11.2. Market Analysis, Insights and Forecast - by Product Type

- 11.2.1. Containers

- 11.2.1.1. Aluminium Foil Container

- 11.2.1.2. Plastic Container

- 11.2.1.3. Board Container

- 11.2.2. Pre-made Bags

- 11.2.3. Food Cans

- 11.2.4. Coated Films

- 11.2.5. Other Product Types

- 11.2.1. Containers

- 11.3. Market Analysis, Insights and Forecast - by Material Type

- 11.3.1. Polypropylene (PP)

- 11.3.2. Polystrene (PS)

- 11.3.3. Polyester (PET)

- 11.3.4. Thermoform

- 11.3.5. Aluminium

- 11.3.6. Other Material Types

- 11.4. Market Analysis, Insights and Forecast - by Application

- 11.4.1. Fresh and Frozen Products

- 11.4.2. Processed Products

- 11.4.3. Read-to-eat Products

- 11.1. Market Analysis, Insights and Forecast - by Packaging Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 WestRock

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Amcor

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Smurfit Kappa Group

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Sonoco

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Stora Enso

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Mondi Group

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Can-Pack SA*List Not Exhaustive

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Crown Holdings

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Berry Global

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 DS Smith

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Sealed Air

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.1 WestRock

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Meat, Poultry & Seafood Packaging Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Meat, Poultry & Seafood Packaging Industry Revenue (billion), by Packaging Type 2025 & 2033

- Figure 3: North America Meat, Poultry & Seafood Packaging Industry Revenue Share (%), by Packaging Type 2025 & 2033

- Figure 4: North America Meat, Poultry & Seafood Packaging Industry Revenue (billion), by Product Type 2025 & 2033

- Figure 5: North America Meat, Poultry & Seafood Packaging Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 6: North America Meat, Poultry & Seafood Packaging Industry Revenue (billion), by Material Type 2025 & 2033

- Figure 7: North America Meat, Poultry & Seafood Packaging Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 8: North America Meat, Poultry & Seafood Packaging Industry Revenue (billion), by Application 2025 & 2033

- Figure 9: North America Meat, Poultry & Seafood Packaging Industry Revenue Share (%), by Application 2025 & 2033

- Figure 10: North America Meat, Poultry & Seafood Packaging Industry Revenue (billion), by Country 2025 & 2033

- Figure 11: North America Meat, Poultry & Seafood Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 12: Europe Meat, Poultry & Seafood Packaging Industry Revenue (billion), by Packaging Type 2025 & 2033

- Figure 13: Europe Meat, Poultry & Seafood Packaging Industry Revenue Share (%), by Packaging Type 2025 & 2033

- Figure 14: Europe Meat, Poultry & Seafood Packaging Industry Revenue (billion), by Product Type 2025 & 2033

- Figure 15: Europe Meat, Poultry & Seafood Packaging Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 16: Europe Meat, Poultry & Seafood Packaging Industry Revenue (billion), by Material Type 2025 & 2033

- Figure 17: Europe Meat, Poultry & Seafood Packaging Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 18: Europe Meat, Poultry & Seafood Packaging Industry Revenue (billion), by Application 2025 & 2033

- Figure 19: Europe Meat, Poultry & Seafood Packaging Industry Revenue Share (%), by Application 2025 & 2033

- Figure 20: Europe Meat, Poultry & Seafood Packaging Industry Revenue (billion), by Country 2025 & 2033

- Figure 21: Europe Meat, Poultry & Seafood Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 22: Asia Pacific Meat, Poultry & Seafood Packaging Industry Revenue (billion), by Packaging Type 2025 & 2033

- Figure 23: Asia Pacific Meat, Poultry & Seafood Packaging Industry Revenue Share (%), by Packaging Type 2025 & 2033

- Figure 24: Asia Pacific Meat, Poultry & Seafood Packaging Industry Revenue (billion), by Product Type 2025 & 2033

- Figure 25: Asia Pacific Meat, Poultry & Seafood Packaging Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 26: Asia Pacific Meat, Poultry & Seafood Packaging Industry Revenue (billion), by Material Type 2025 & 2033

- Figure 27: Asia Pacific Meat, Poultry & Seafood Packaging Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 28: Asia Pacific Meat, Poultry & Seafood Packaging Industry Revenue (billion), by Application 2025 & 2033

- Figure 29: Asia Pacific Meat, Poultry & Seafood Packaging Industry Revenue Share (%), by Application 2025 & 2033

- Figure 30: Asia Pacific Meat, Poultry & Seafood Packaging Industry Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Meat, Poultry & Seafood Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 32: Latin America Meat, Poultry & Seafood Packaging Industry Revenue (billion), by Packaging Type 2025 & 2033

- Figure 33: Latin America Meat, Poultry & Seafood Packaging Industry Revenue Share (%), by Packaging Type 2025 & 2033

- Figure 34: Latin America Meat, Poultry & Seafood Packaging Industry Revenue (billion), by Product Type 2025 & 2033

- Figure 35: Latin America Meat, Poultry & Seafood Packaging Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 36: Latin America Meat, Poultry & Seafood Packaging Industry Revenue (billion), by Material Type 2025 & 2033

- Figure 37: Latin America Meat, Poultry & Seafood Packaging Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 38: Latin America Meat, Poultry & Seafood Packaging Industry Revenue (billion), by Application 2025 & 2033

- Figure 39: Latin America Meat, Poultry & Seafood Packaging Industry Revenue Share (%), by Application 2025 & 2033

- Figure 40: Latin America Meat, Poultry & Seafood Packaging Industry Revenue (billion), by Country 2025 & 2033

- Figure 41: Latin America Meat, Poultry & Seafood Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 42: Middle East and Africa Meat, Poultry & Seafood Packaging Industry Revenue (billion), by Packaging Type 2025 & 2033

- Figure 43: Middle East and Africa Meat, Poultry & Seafood Packaging Industry Revenue Share (%), by Packaging Type 2025 & 2033

- Figure 44: Middle East and Africa Meat, Poultry & Seafood Packaging Industry Revenue (billion), by Product Type 2025 & 2033

- Figure 45: Middle East and Africa Meat, Poultry & Seafood Packaging Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 46: Middle East and Africa Meat, Poultry & Seafood Packaging Industry Revenue (billion), by Material Type 2025 & 2033

- Figure 47: Middle East and Africa Meat, Poultry & Seafood Packaging Industry Revenue Share (%), by Material Type 2025 & 2033

- Figure 48: Middle East and Africa Meat, Poultry & Seafood Packaging Industry Revenue (billion), by Application 2025 & 2033

- Figure 49: Middle East and Africa Meat, Poultry & Seafood Packaging Industry Revenue Share (%), by Application 2025 & 2033

- Figure 50: Middle East and Africa Meat, Poultry & Seafood Packaging Industry Revenue (billion), by Country 2025 & 2033

- Figure 51: Middle East and Africa Meat, Poultry & Seafood Packaging Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Packaging Type 2020 & 2033

- Table 2: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 3: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Material Type 2020 & 2033

- Table 4: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Packaging Type 2020 & 2033

- Table 7: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 8: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Material Type 2020 & 2033

- Table 9: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 10: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 11: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Packaging Type 2020 & 2033

- Table 12: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 13: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Material Type 2020 & 2033

- Table 14: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 15: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 16: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Packaging Type 2020 & 2033

- Table 17: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 18: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Material Type 2020 & 2033

- Table 19: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 20: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 21: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Packaging Type 2020 & 2033

- Table 22: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 23: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Material Type 2020 & 2033

- Table 24: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 25: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 26: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Packaging Type 2020 & 2033

- Table 27: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 28: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Material Type 2020 & 2033

- Table 29: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 30: Global Meat, Poultry & Seafood Packaging Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Meat, Poultry & Seafood Packaging Industry?

The projected CAGR is approximately 5.2%.

2. Which companies are prominent players in the Meat, Poultry & Seafood Packaging Industry?

Key companies in the market include WestRock, Amcor, Smurfit Kappa Group, Sonoco, Stora Enso, Mondi Group, Can-Pack SA*List Not Exhaustive, Crown Holdings, Berry Global, DS Smith, Sealed Air.

3. What are the main segments of the Meat, Poultry & Seafood Packaging Industry?

The market segments include Packaging Type, Product Type, Material Type, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 15.62 billion as of 2022.

5. What are some drivers contributing to market growth?

Increase in Population May Increase the Demand; Government Regulations for Improved and Better Packaging Materials.

6. What are the notable trends driving market growth?

Flexible Packaging to Witness Growth.

7. Are there any restraints impacting market growth?

Contamination Due to Poor Packaging or Mishandling.

8. Can you provide examples of recent developments in the market?

December 2022 - Amcor announced the opening of its new state-of-the-art manufacturing plant in Huizhou, China. With an investment of over USD 100 million, the 590,000 sq ft factory is the largest flexible packaging plant in China by production capacity, substantially enhancing Amcor's capabilities to fulfill rising client demand throughout Asia-Pacific. The facility has China's first automated packaging production line, resulting in double-digit decreases in production cycle time, together with high-speed printing presses, laminators, and bag-making equipment.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Meat, Poultry & Seafood Packaging Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Meat, Poultry & Seafood Packaging Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Meat, Poultry & Seafood Packaging Industry?

To stay informed about further developments, trends, and reports in the Meat, Poultry & Seafood Packaging Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence