Key Insights

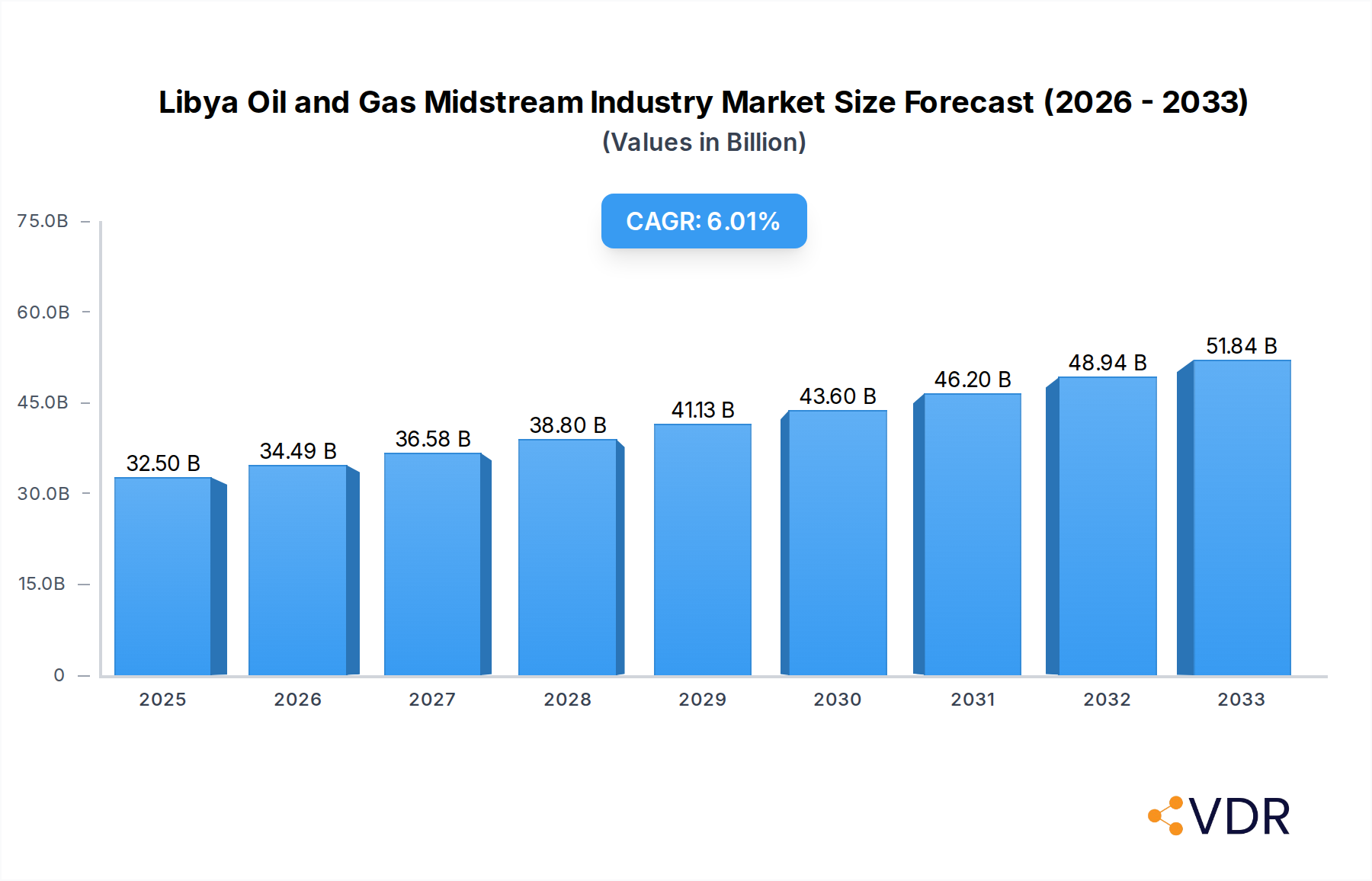

The Libyan oil and gas midstream industry is poised for significant growth, projected to reach USD 32.5 billion in 2025, driven by a robust CAGR of 6.1% during the forecast period. This expansion is primarily fueled by crucial investments in the transportation and storage segments, critical for efficient movement and safeguarding of hydrocarbon resources. Existing infrastructure, though facing challenges, is being augmented by an ambitious pipeline of projects and upcoming developments designed to enhance capacity and modernize operations. The strategic importance of LNG terminals also plays a pivotal role, facilitating the export of liquefied natural gas and contributing to the nation's energy trade. Key market drivers include the nation's substantial hydrocarbon reserves, a growing global demand for energy, and government initiatives aimed at revitalizing the energy sector. These factors collectively underscore the industry's potential for sustained expansion and increased economic contribution.

Libya Oil and Gas Midstream Industry Market Size (In Billion)

The midstream sector in Libya is characterized by its integral role in unlocking the full potential of the country's vast oil and gas reserves. While the sector benefits from significant natural resource endowments and increasing global energy needs, it also navigates specific restraints. These may include geopolitical complexities, the need for advanced technological integration, and the imperative for continuous infrastructure upgrades to meet international standards. The market is segmented into Transportation, Storage, and LNG Terminals, each presenting unique opportunities and challenges. Companies such as TotalEnergies, ConocoPhillips, National Oil Corporation, Suncor Energy, and Eni are key players, their strategic investments and operational expertise shaping the industry's trajectory. The ongoing development of projects in the pipeline and the anticipation of new ventures are indicative of a proactive approach to capitalize on market opportunities and solidify Libya's position as a significant energy producer.

Libya Oil and Gas Midstream Industry Company Market Share

Libya Oil and Gas Midstream Industry Market Dynamics & Structure

The Libya oil and gas midstream industry is characterized by a dynamic interplay of existing infrastructure, ongoing development projects, and evolving regulatory landscapes. Market concentration is influenced by the significant role of the National Oil Corporation (NOC), which dominates a substantial portion of the midstream assets. However, international oil companies (IOCs) like Eni SpA, Total SA, ConocoPhillips Corporation, and Suncor Energy Inc. also hold considerable influence, particularly in strategic joint ventures and project development. Technological innovation drivers in this sector primarily revolve around enhancing operational efficiency, improving safety standards, and reducing environmental impact. This includes the adoption of advanced pipeline monitoring systems, corrosion prevention technologies, and more efficient storage solutions.

- Market Concentration: Dominated by NOC, with significant participation from IOCs.

- Technological Innovation: Focus on efficiency, safety, and environmental sustainability.

- Regulatory Frameworks: Evolving policies aimed at attracting foreign investment and ensuring resource security.

- Competitive Product Substitutes: Limited direct substitutes for hydrocarbon transportation and storage, but efficiency gains can be considered competitive advantages.

- End-User Demographics: Primarily consists of domestic refineries, export terminals, and international buyers of crude oil, refined products, and LNG.

- M&A Trends: While large-scale M&A is less prevalent, strategic partnerships and asset acquisitions by IOCs are key. For example, joint ventures with NOC for specific pipeline or terminal projects are common. The overall M&A deal volume in the midstream sector in Libya is estimated to be in the low billions.

Libya Oil and Gas Midstream Industry Growth Trends & Insights

The Libya oil and gas midstream industry is poised for significant growth over the forecast period of 2025–2033, driven by the nation's vast hydrocarbon reserves and the strategic imperative to efficiently transport and process these resources. The market size evolution is intrinsically linked to the upstream production levels and global demand for oil and gas. Historical data from 2019–2024 indicates a period of recovery and gradual expansion, with the base year of 2025 serving as a critical pivot point for accelerated development. The estimated market size in 2025 is projected to be in the tens of billions of dollars, with steady annual growth rates anticipated.

Adoption rates for advanced midstream technologies are on the rise, spurred by the need for operational resilience and adherence to international standards. Technological disruptions, such as the increasing use of digital twins for pipeline management and predictive maintenance, are expected to enhance efficiency and reduce downtime. Furthermore, shifts in consumer behavior globally, favoring cleaner energy sources, indirectly influence the midstream sector by necessitating investments in efficient processing and transportation of both traditional hydrocarbons and, in the longer term, potentially transitional fuels. The market penetration of modern infrastructure solutions is expected to deepen as the country prioritizes energy security and export diversification. This growth trajectory is further supported by substantial investment plans outlined for the upcoming years, focusing on expanding existing networks and developing new capacities to meet projected demand. The compound annual growth rate (CAGR) for the Libya oil and gas midstream industry is projected to be in the high single digits during the forecast period.

Dominant Regions, Countries, or Segments in Libya Oil and Gas Midstream Industry

Within the Libya oil and gas midstream sector, the Transportation segment stands out as the dominant driver of market growth. This segment encompasses the crucial infrastructure required to move crude oil and refined products from production sites to refineries and export terminals. The extensive network of existing pipelines, coupled with ambitious projects in the pipeline and upcoming initiatives, underscores its pivotal role. Economic policies that prioritize the maximization of oil and gas exports directly translate into heightened demand for efficient transportation solutions. The National Oil Corporation (NOC), alongside international players like Eni SpA and Total SA, are heavily invested in expanding and modernizing this critical infrastructure.

- Transportation: Overview

- Existing Infrastructure: A comprehensive network of crude oil and refined product pipelines crisscrossing key production and consumption areas. This includes major trunk lines connecting oil fields to coastal terminals. The existing infrastructure is valued in the tens of billions of dollars.

- Projects in Pipeline: Significant ongoing projects focused on extending pipeline networks, upgrading existing lines for increased capacity and safety, and developing new routes to bypass potential bottlenecks. These projects represent billions of dollars in investment.

- Upcoming Projects: Future plans involve the development of new pipelines to access unexplored reserves and enhance export capabilities, potentially including cross-border links and specialized product lines. These are projected to involve investments in the billions of dollars.

The Storage segment also plays a vital role, though its growth is intrinsically linked to the transportation and refining capacity. Existing storage facilities, including tank farms at production sites and terminals, are essential for managing supply fluctuations and ensuring uninterrupted operations. Projects in the pipeline and upcoming developments aim to increase storage capacity to support higher production levels and meet growing export demands. The market share in storage is significant, with investments projected in the billions.

The LNG Terminals segment, while currently less developed than transportation or storage, holds immense future potential. Libya's ambition to become a significant exporter of liquefied natural gas necessitates the development and expansion of LNG terminal infrastructure. Existing infrastructure is limited, but projects in the pipeline and upcoming projects are designed to capitalize on the global demand for natural gas. This segment represents a substantial growth opportunity, with projected investments in the billions of dollars over the forecast period. The dominance of the transportation segment is a testament to the immediate need to monetize Libya's vast oil and gas reserves, while LNG terminals represent a strategic long-term growth frontier.

Libya Oil and Gas Midstream Industry Product Landscape

The Libya oil and gas midstream industry's product landscape is primarily defined by the efficient and safe transportation and storage of crude oil, refined petroleum products, and, increasingly, liquefied natural gas (LNG). Innovations focus on optimizing the flow of these commodities through extensive pipeline networks, ensuring product integrity in storage facilities, and enhancing the liquefaction and regasification processes for LNG. Advanced monitoring technologies, corrosion-resistant materials, and intelligent pipeline automation systems are key performance indicators for the transportation segment. For storage, capacity optimization, leak detection, and environmental containment are paramount. In the emerging LNG sector, efficient liquefaction and regasification technologies are critical for competitiveness.

Key Drivers, Barriers & Challenges in Libya Oil and Gas Midstream Industry

Key Drivers: The primary forces propelling the Libya oil and gas midstream industry are Libya's immense proven hydrocarbon reserves, driving the need for robust transportation and export infrastructure. Government initiatives aimed at revitalizing the energy sector and attracting foreign direct investment are critical. Furthermore, the global demand for oil and gas, coupled with efforts to diversify export markets, acts as a significant catalyst. Technological advancements in pipeline integrity management and storage solutions enhance operational efficiency and safety, making them key drivers.

Key Barriers & Challenges: Significant challenges include the ongoing geopolitical instability and security concerns that can disrupt operations and deter investment. Aging infrastructure in some areas necessitates substantial upgrades and maintenance, posing a considerable financial burden. Regulatory complexities and bureaucratic hurdles can slow down project approvals and execution. Supply chain disruptions, particularly for specialized equipment and skilled labor, remain a persistent issue. Competitive pressures from other global energy suppliers also influence market dynamics. The estimated cost of addressing these challenges could run into billions.

Emerging Opportunities in Libya Oil and Gas Midstream Industry

Emerging opportunities in the Libya oil and gas midstream industry lie in the expansion of LNG export capabilities, catering to the growing global demand for natural gas. Developing specialized infrastructure for transporting and storing refined petroleum products to meet regional market needs presents another avenue. Furthermore, leveraging advancements in digital technologies for enhanced pipeline monitoring, predictive maintenance, and supply chain optimization offers significant efficiency gains and cost reductions. The potential for developing infrastructure to support cleaner energy transition, such as carbon capture and storage (CCS) pipelines, also represents a long-term opportunity.

Growth Accelerators in the Libya Oil and Gas Midstream Industry Industry

Growth accelerators for the Libya oil and gas midstream industry are multifaceted. Strategic partnerships between the National Oil Corporation (NOC) and international oil companies (IOCs) are vital for injecting capital, technology, and expertise into large-scale projects. The successful completion of ongoing pipeline expansion and modernization initiatives will unlock new production capacities and enhance export volumes. Government commitment to creating a more stable and attractive investment climate will further boost confidence and attract further capital. Moreover, the integration of advanced digital technologies and automation across the midstream value chain will optimize operations, reduce costs, and improve overall efficiency, acting as a significant growth accelerator.

Key Players Shaping the Libya Oil and Gas Midstream Industry Market

- Total SA

- ConocoPhillips Corporation

- National Oil Corporation

- Suncor Energy Inc.

- Eni SpA

Notable Milestones in Libya Oil and Gas Midstream Industry Sector

- 2019: Resumption of operations at key export terminals following security improvements.

- 2020: Initiation of feasibility studies for new pipeline projects to enhance production capacity.

- 2021: Agreement signed for the upgrade of critical oil infrastructure, involving billions in investment.

- 2022: Commencement of construction on a major gas pipeline project to increase domestic supply.

- 2023: Exploration of new partnerships for LNG terminal development.

- 2024: Successful commissioning of upgraded storage facilities at a major export hub.

In-Depth Libya Oil and Gas Midstream Industry Market Outlook

The Libya oil and gas midstream industry is set for a robust growth trajectory driven by substantial investment in infrastructure and the strategic importance of its hydrocarbon resources. The outlook is characterized by an increased focus on expanding transportation networks, enhancing storage capacities, and developing advanced LNG export facilities. Strategic alliances and technological advancements will be key to unlocking the full potential of Libya's midstream sector. The market is expected to witness significant activity in project execution and infrastructure modernization, positioning Libya as a key player in the global energy supply chain. The forecast period signifies a crucial phase of development and expansion, promising substantial returns and increased operational efficiency.

Libya Oil and Gas Midstream Industry Segmentation

-

1. Transportation

-

1.1. Overview

- 1.1.1. Existing Infrastructure

- 1.1.2. Projects in Pipeline

- 1.1.3. Upcoming Projects

-

1.1. Overview

-

2. Storage

-

2.1. Overview

- 2.1.1. Existing Infrastructure

- 2.1.2. Projects in Pipeline

- 2.1.3. Upcoming Projects

-

2.1. Overview

-

3. LNG Terminals

-

3.1. Overview

- 3.1.1. Existing Infrastructure

- 3.1.2. Projects in Pipeline

- 3.1.3. Upcoming Projects

-

3.1. Overview

Libya Oil and Gas Midstream Industry Segmentation By Geography

- 1. Libya

Libya Oil and Gas Midstream Industry Regional Market Share

Geographic Coverage of Libya Oil and Gas Midstream Industry

Libya Oil and Gas Midstream Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Transportation

- 5.1.1. Overview

- 5.1.1.1. Existing Infrastructure

- 5.1.1.2. Projects in Pipeline

- 5.1.1.3. Upcoming Projects

- 5.1.1. Overview

- 5.2. Market Analysis, Insights and Forecast - by Storage

- 5.2.1. Overview

- 5.2.1.1. Existing Infrastructure

- 5.2.1.2. Projects in Pipeline

- 5.2.1.3. Upcoming Projects

- 5.2.1. Overview

- 5.3. Market Analysis, Insights and Forecast - by LNG Terminals

- 5.3.1. Overview

- 5.3.1.1. Existing Infrastructure

- 5.3.1.2. Projects in Pipeline

- 5.3.1.3. Upcoming Projects

- 5.3.1. Overview

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Libya

- 5.1. Market Analysis, Insights and Forecast - by Transportation

- 6. Libya Oil and Gas Midstream Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Transportation

- 6.1.1. Overview

- 6.1.1.1. Existing Infrastructure

- 6.1.1.2. Projects in Pipeline

- 6.1.1.3. Upcoming Projects

- 6.1.1. Overview

- 6.2. Market Analysis, Insights and Forecast - by Storage

- 6.2.1. Overview

- 6.2.1.1. Existing Infrastructure

- 6.2.1.2. Projects in Pipeline

- 6.2.1.3. Upcoming Projects

- 6.2.1. Overview

- 6.3. Market Analysis, Insights and Forecast - by LNG Terminals

- 6.3.1. Overview

- 6.3.1.1. Existing Infrastructure

- 6.3.1.2. Projects in Pipeline

- 6.3.1.3. Upcoming Projects

- 6.3.1. Overview

- 6.1. Market Analysis, Insights and Forecast - by Transportation

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Total SA

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 ConocoPhillips Corporation

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 National Oil Corporation

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Suncor Energy Inc

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Eni SpA

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.1 Total SA

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Libya Oil and Gas Midstream Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Libya Oil and Gas Midstream Industry Share (%) by Company 2025

List of Tables

- Table 1: Libya Oil and Gas Midstream Industry Revenue billion Forecast, by Transportation 2020 & 2033

- Table 2: Libya Oil and Gas Midstream Industry Volume K Tons Forecast, by Transportation 2020 & 2033

- Table 3: Libya Oil and Gas Midstream Industry Revenue billion Forecast, by Storage 2020 & 2033

- Table 4: Libya Oil and Gas Midstream Industry Volume K Tons Forecast, by Storage 2020 & 2033

- Table 5: Libya Oil and Gas Midstream Industry Revenue billion Forecast, by LNG Terminals 2020 & 2033

- Table 6: Libya Oil and Gas Midstream Industry Volume K Tons Forecast, by LNG Terminals 2020 & 2033

- Table 7: Libya Oil and Gas Midstream Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 8: Libya Oil and Gas Midstream Industry Volume K Tons Forecast, by Region 2020 & 2033

- Table 9: Libya Oil and Gas Midstream Industry Revenue billion Forecast, by Transportation 2020 & 2033

- Table 10: Libya Oil and Gas Midstream Industry Volume K Tons Forecast, by Transportation 2020 & 2033

- Table 11: Libya Oil and Gas Midstream Industry Revenue billion Forecast, by Storage 2020 & 2033

- Table 12: Libya Oil and Gas Midstream Industry Volume K Tons Forecast, by Storage 2020 & 2033

- Table 13: Libya Oil and Gas Midstream Industry Revenue billion Forecast, by LNG Terminals 2020 & 2033

- Table 14: Libya Oil and Gas Midstream Industry Volume K Tons Forecast, by LNG Terminals 2020 & 2033

- Table 15: Libya Oil and Gas Midstream Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 16: Libya Oil and Gas Midstream Industry Volume K Tons Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Libya Oil and Gas Midstream Industry?

The projected CAGR is approximately 6.1%.

2. Which companies are prominent players in the Libya Oil and Gas Midstream Industry?

Key companies in the market include Total SA, ConocoPhillips Corporation, National Oil Corporation, Suncor Energy Inc, Eni SpA.

3. What are the main segments of the Libya Oil and Gas Midstream Industry?

The market segments include Transportation, Storage, LNG Terminals.

4. Can you provide details about the market size?

The market size is estimated to be USD 32.5 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Abundant Oil and Gas Reserves4.; Favorable Investment in Upstream Sector.

6. What are the notable trends driving market growth?

Growth of the Pipeline Sector to Remain Stagnant.

7. Are there any restraints impacting market growth?

4.; Volatility of Crude Oil Prices.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K Tons.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Libya Oil and Gas Midstream Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Libya Oil and Gas Midstream Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Libya Oil and Gas Midstream Industry?

To stay informed about further developments, trends, and reports in the Libya Oil and Gas Midstream Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence