Key Insights

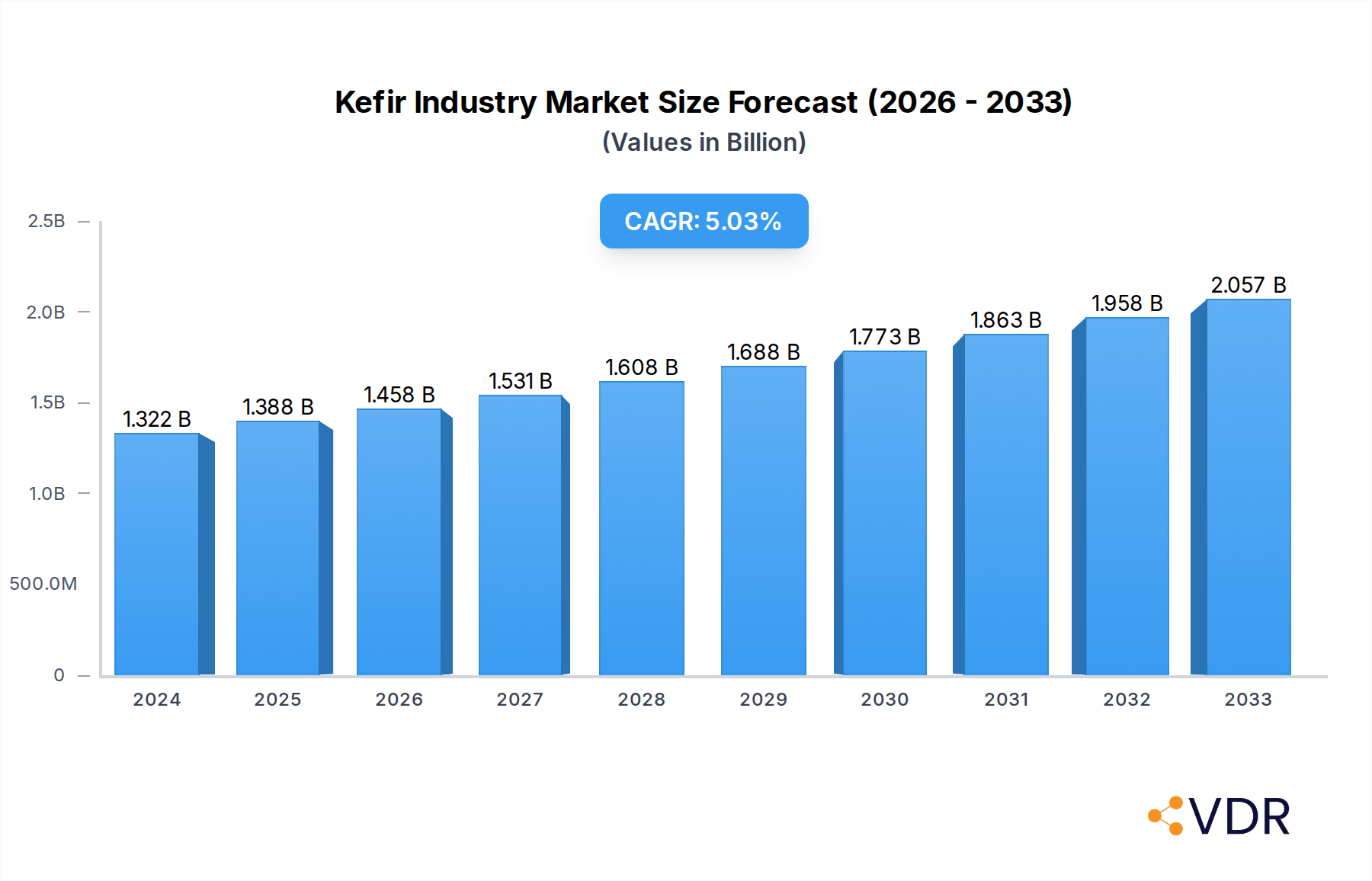

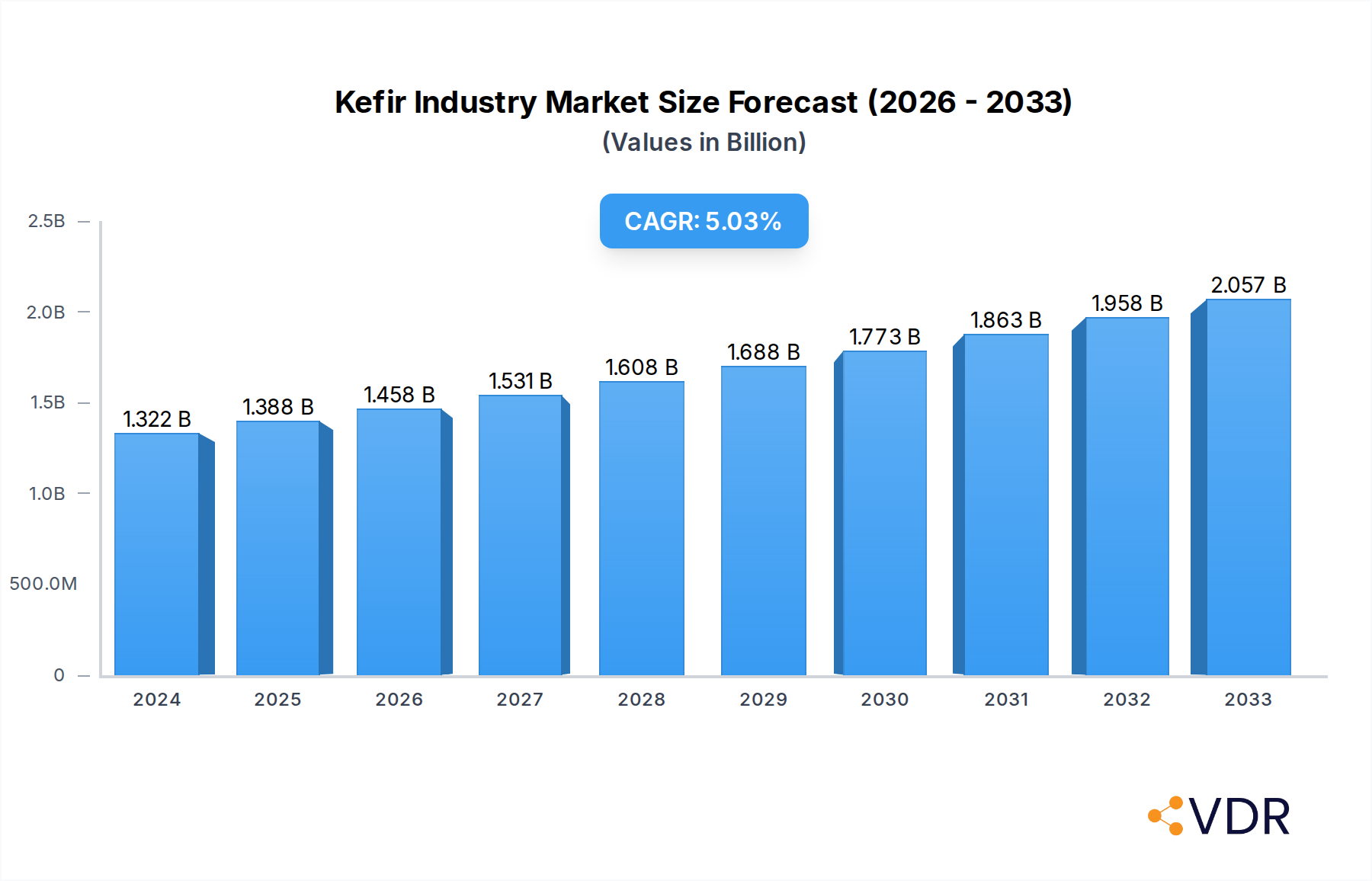

The global Kefir market is poised for significant expansion, projected to reach an estimated $1322.24 million in 2024 with a robust Compound Annual Growth Rate (CAGR) of 5% through 2033. This growth is fueled by increasing consumer awareness regarding the health benefits of fermented foods, particularly probiotics, and a rising demand for convenient, nutrient-dense beverages. The market's expansion is also significantly influenced by a growing preference for organic and natural products, as consumers actively seek healthier alternatives to conventional dairy and processed drinks. The expansion of flavored kefir options, catering to diverse palates, further stimulates demand, broadening its appeal beyond traditional consumers. Key market drivers include the escalating prevalence of gut health concerns and the subsequent adoption of probiotic-rich foods and beverages as a dietary staple.

Kefir Industry Market Size (In Billion)

The market landscape for kefir is characterized by a dynamic interplay of product innovation and evolving consumer preferences. While milk kefir, encompassing both dairy and non-dairy variations, currently holds a dominant position, water kefir is emerging as a noteworthy segment, driven by its perceived lighter profile and dairy-free appeal. The distribution channel analysis reveals a strong reliance on supermarkets and hypermarkets, underscoring the importance of widespread retail accessibility. However, the rapid growth of online retail stores indicates a significant shift in consumer purchasing habits, offering both convenience and a wider selection. Restraints such as the shelf-life limitations of fermented products and the need for specialized storage conditions are being addressed through advancements in packaging and preservation technologies. Emerging trends point towards the integration of novel flavors, functional ingredients, and sustainable sourcing practices, all contributing to the sustained and promising trajectory of the kefir industry.

Kefir Industry Company Market Share

Kefir Industry Report: Market Dynamics, Growth Trends, and Key Player Analysis (2019–2033)

This comprehensive report offers an in-depth analysis of the global Kefir market, encompassing its current dynamics, future growth trajectory, and competitive landscape. Covering the study period from 2019 to 2033, with a base year of 2025, this report provides actionable insights for stakeholders seeking to capitalize on the burgeoning demand for fermented dairy and non-dairy beverages. We delve into the intricate structure of parent and child markets, examining how innovations and consumer preferences in sub-segments influence the overall market. The report utilizes high-traffic keywords relevant to the kefir industry, ensuring maximum search engine visibility for industry professionals and researchers. All quantitative values are presented in million units for clarity and ease of understanding.

Kefir Industry Market Dynamics & Structure

The global kefir market exhibits a moderately concentrated structure, characterized by the presence of both established multinational corporations and nimble regional players. Technological innovation is a significant driver, with advancements in fermentation techniques, probiotic strain development, and non-dairy alternatives continuously reshaping the product offerings. Regulatory frameworks, particularly concerning food safety, labeling, and health claims, play a crucial role in market entry and product development. Competitive product substitutes, including yogurt, kombucha, and other fermented beverages, pose a constant challenge, necessitating continuous product differentiation and marketing efforts. End-user demographics are shifting towards health-conscious consumers, millennials, and Gen Z, who are increasingly seeking functional foods with perceived health benefits. Mergers and acquisitions (M&A) trends are evident as larger companies aim to expand their portfolios and gain market share, while smaller innovative brands seek strategic partnerships or acquisitions for growth. For instance, the past five years have seen approximately 10-15 significant M&A deals within the broader fermented foods sector, with kefir brands being frequent targets. Innovation barriers include the capital-intensive nature of scaling up production and achieving consistent quality, alongside navigating diverse international food regulations.

- Market Concentration: Moderately concentrated, with a few key players holding significant market share.

- Technological Innovation Drivers: Probiotic advancements, non-dairy fermentation, and novel flavor development.

- Regulatory Frameworks: Stringent food safety standards and evolving health claim regulations.

- Competitive Product Substitutes: Yogurt, kombucha, other fermented drinks.

- End-User Demographics: Health-conscious consumers, millennials, Gen Z.

- M&A Trends: Increasing consolidation and strategic acquisitions of innovative brands.

- Innovation Barriers: Capital investment, quality control, regulatory navigation.

Kefir Industry Growth Trends & Insights

The global kefir market is poised for substantial growth, projected to witness a Compound Annual Growth Rate (CAGR) of approximately 7.5% during the forecast period of 2025–2033. This robust expansion is fueled by a confluence of escalating consumer awareness regarding the health benefits of probiotics and fermented foods, coupled with a growing demand for convenient and functional beverage options. The market size, estimated at approximately $3,500 million units in 2025, is expected to reach upwards of $6,300 million units by 2033. Adoption rates of kefir are rapidly increasing across both developed and emerging economies, driven by its perceived positive impact on gut health, immunity, and digestion. Technological disruptions, such as the development of more shelf-stable kefir products and the expansion of non-dairy kefir varieties, are broadening its appeal to a wider consumer base, including those with lactose intolerance or vegan dietary preferences.

Consumer behavior shifts are playing a pivotal role, with a marked preference for natural ingredients, transparent labeling, and products that align with wellness trends. The "gut health" narrative has become a significant marketing advantage for kefir, positioning it as a key component of a healthy lifestyle. Market penetration is deepening, moving beyond niche health food stores into mainstream supermarkets and convenience stores. The increasing availability of flavored kefir options, catering to diverse palates, is also a major contributor to this growth. Furthermore, the online retail channel is emerging as a significant avenue for kefir sales, offering greater convenience and accessibility to consumers. The historical growth from 2019 to 2024, estimated at a CAGR of 6.8%, laid a strong foundation for the accelerated growth anticipated in the coming years. This trajectory is supported by continuous product innovation and increasing consumer education about the multifaceted benefits of kefir.

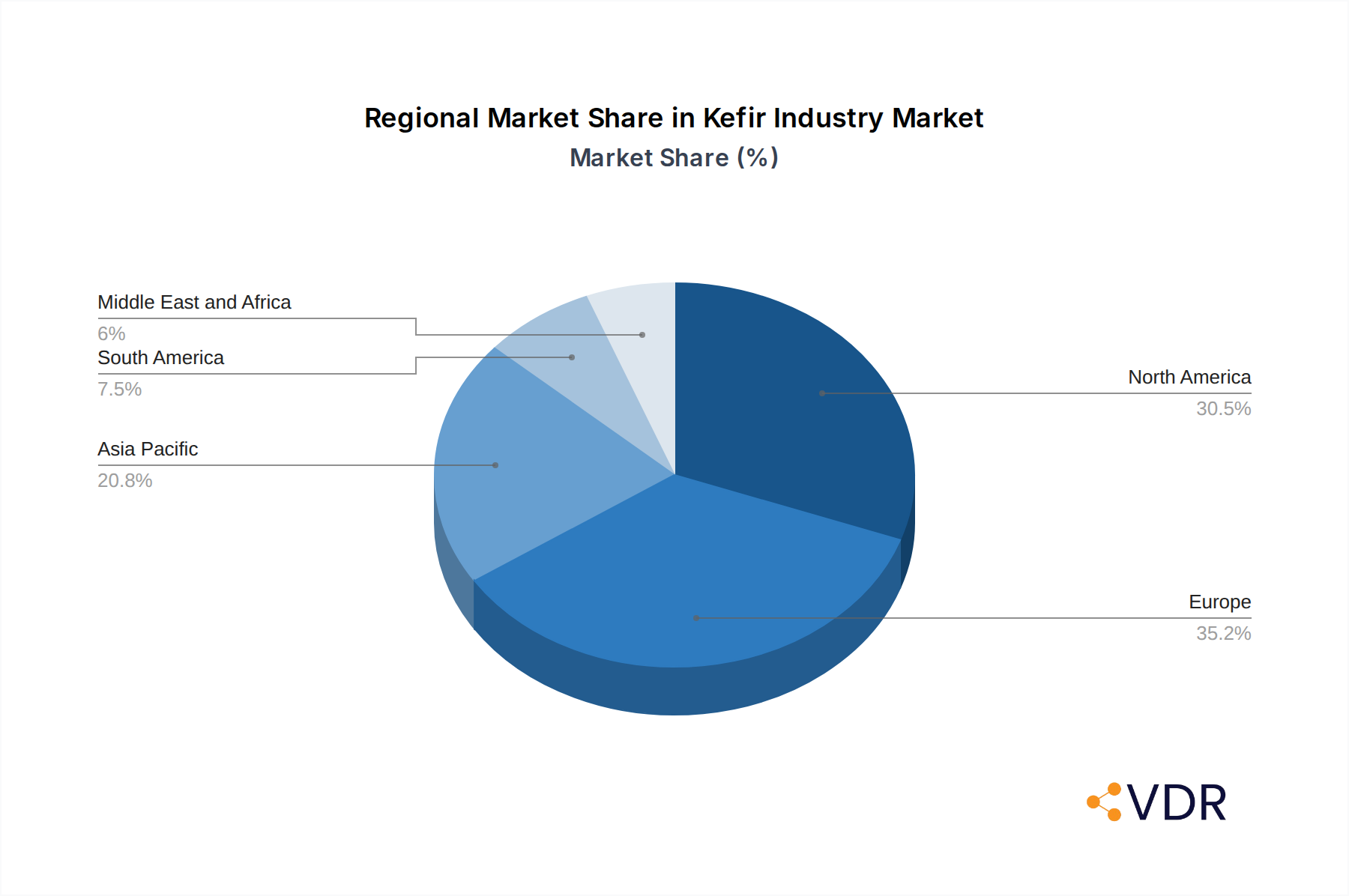

Dominant Regions, Countries, or Segments in Kefir Industry

North America currently stands as the dominant region in the global kefir market, driven by high consumer awareness of gut health and a well-established market for fermented dairy products. Within North America, the United States leads the charge, accounting for a significant portion of the market share. The Organic segment within the Form category is a key growth driver, reflecting a broader consumer trend towards natural and minimally processed foods. This segment is projected to witness a CAGR of approximately 8.2% during the forecast period.

The Flavored kefir category is outperforming its non-flavored counterpart, with a projected CAGR of 7.9%, as manufacturers introduce an array of innovative and appealing flavors to attract a wider demographic, particularly younger consumers. Milk Kefir, especially Dairy-based Milk Kefir, remains the most prevalent Product Type, benefiting from established consumer familiarity and a wide range of flavor profiles. However, Non-dairy based Milk Kefir is experiencing exceptionally high growth rates, estimated at a CAGR of 9.5%, as it caters to the burgeoning vegan and lactose-intolerant populations. Water Kefir is also carving out its niche, offering a lighter, more refreshing alternative with a projected CAGR of 7.2%.

In terms of Distribution Channels, Supermarkets/Hypermarkets continue to dominate, providing broad accessibility and high sales volumes, with an estimated 55% market share. However, Online Retail Stores are exhibiting the fastest growth, with a projected CAGR of 10.1%, driven by the convenience and expanding reach of e-commerce platforms. Key drivers for dominance in these regions and segments include robust economic policies supporting the food and beverage industry, advanced cold-chain infrastructure crucial for perishable goods, and proactive marketing campaigns highlighting the health benefits of kefir. The market share of the dominant segments is expected to see continued expansion as consumer preferences align with these product attributes and distribution strategies.

Kefir Industry Product Landscape

The kefir product landscape is characterized by a dynamic array of innovations focused on enhancing taste, texture, and functional benefits. Product development is increasingly targeting specific health needs, such as improved digestion, immune support, and even mood enhancement, through the strategic inclusion of specialized probiotic strains. Unique selling propositions often revolve around the purity of ingredients, the ethical sourcing of milk for dairy-based kefirs, and the creative fusion of exotic fruits and superfoods in flavored varieties. Technological advancements are enabling the creation of shelf-stable kefir products, expanding their reach beyond refrigerated sections and into more convenient formats. The performance metrics for new product launches are closely monitored, with a strong emphasis on consumer trial and repeat purchase rates driven by taste profiles and perceived health outcomes.

Key Drivers, Barriers & Challenges in Kefir Industry

The kefir industry is propelled by a confluence of potent drivers. The escalating global awareness of gut health and the role of probiotics in overall well-being is paramount. Consumers are actively seeking functional foods, and kefir's proven benefits in this regard are a significant draw. Technological advancements in fermentation processes are enabling the production of more diverse and appealing kefir products, including non-dairy and water-based alternatives. The increasing prevalence of lactose intolerance and veganism further fuels the demand for non-dairy kefir.

However, the industry faces several barriers and challenges. Supply chain complexities, particularly for maintaining the cold chain and ensuring product freshness across extended distribution networks, remain a significant hurdle. Stringent and varied regulatory hurdles across different countries can impede market entry and product innovation. Intense competitive pressures from established dairy products and emerging fermented beverages like kombucha necessitate continuous differentiation and marketing efforts. The cost of high-quality ingredients and sophisticated production processes can also impact pricing and market accessibility for some consumer segments.

Emerging Opportunities in Kefir Industry

Emerging opportunities in the kefir industry are multifaceted and promising. The untapped potential of emerging markets in Asia and Latin America presents a significant growth avenue as consumer awareness of health and wellness increases. Innovative applications of kefir beyond traditional beverages, such as in culinary products, baked goods, and even beauty products, offer novel avenues for market penetration. Evolving consumer preferences are leaning towards personalized nutrition, creating opportunities for customized kefir formulations with specific probiotic blends tailored to individual health needs. The development of plant-based kefir with novel ingredients beyond soy and almond, such as oat, coconut, or even blends, holds substantial promise to capture a larger share of the non-dairy market.

Growth Accelerators in the Kefir Industry Industry

Several key catalysts are accelerating the long-term growth of the kefir industry. Technological breakthroughs in probiotic strain research are leading to the development of kefir with enhanced health benefits and novel functionalities, attracting a wider consumer base. Strategic partnerships between kefir manufacturers and research institutions are driving innovation and validating health claims. Furthermore, market expansion strategies, including increased penetration into mainstream retail channels and targeted marketing campaigns emphasizing the health and taste appeal of kefir, are crucial growth accelerators. The growing trend of functional beverages and the increasing consumer demand for products that support a healthy lifestyle are creating a fertile ground for sustained and accelerated growth in the global kefir market.

Key Players Shaping the Kefir Industry Market

- Green Valley Creamery

- The Icelandic Milk and Skyr Corporation

- Emmi AG (Redwood Hill Farm & Creamery)

- The Hain Celestial Group Inc

- Lifeway Foods Inc

- Danone S A

- Maple Hill Creamery LLC

- Biotiful Dairy

- Evolve Kefir

- Nestlé S A

Notable Milestones in Kefir Industry Sector

- 2019: Increased consumer interest in gut health drives significant sales growth for probiotic-rich foods like kefir.

- 2020: Expansion of non-dairy kefir options gains traction, catering to vegan and lactose-intolerant consumers.

- 2021: Introduction of new flavor innovations and functional ingredient additions to kefir products.

- 2022: Online retail sales of kefir experience a substantial surge due to convenience and wider accessibility.

- 2023: Growing emphasis on sustainability and ethical sourcing in dairy production influences consumer choices in the kefir market.

- 2024: Regulatory bodies begin to clarify guidelines for health claims associated with probiotic foods, impacting marketing strategies.

In-Depth Kefir Industry Market Outlook

The future outlook for the kefir industry is exceptionally bright, with growth accelerators pointing towards sustained expansion. The increasing consumer demand for functional and health-promoting foods, coupled with the continuous innovation in product development, particularly in the non-dairy and specialized probiotic segments, will be key drivers. Strategic market expansion through enhanced distribution networks and effective consumer education campaigns will further solidify kefir's position. The industry is well-positioned to capitalize on global wellness trends, offering significant strategic opportunities for market players to innovate, differentiate, and capture substantial market share in the coming years.

Kefir Industry Segmentation

-

1. Form

- 1.1. Organic

- 1.2. Conventional

-

2. Category

- 2.1. Flavored kefir

- 2.2. Non-flavored kefir

-

3. Product Type

-

3.1. Milk Kefir

- 3.1.1. Dairy based

- 3.1.2. Non-dairy based

- 3.2. Water Kefir

-

3.1. Milk Kefir

-

4. Distribution Channel

- 4.1. Supermarkets/Hypermarkets

- 4.2. Convenience Stores

- 4.3. Online Retail Stores

- 4.4. Other Distribution Channels

Kefir Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

- 1.4. Rest of North America

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. Italy

- 2.4. Spain

- 2.5. France

- 2.6. Russia

- 2.7. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. Rest of Asia Pacific

-

4. South America

- 4.1. Brazil

- 4.2. Argentina

- 4.3. Rest of South America

-

5. Middle East and Africa

- 5.1. South Africa

- 5.2. United Arab Emirates

- 5.3. Rest of Middle East and Africa

Kefir Industry Regional Market Share

Geographic Coverage of Kefir Industry

Kefir Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Form

- 5.1.1. Organic

- 5.1.2. Conventional

- 5.2. Market Analysis, Insights and Forecast - by Category

- 5.2.1. Flavored kefir

- 5.2.2. Non-flavored kefir

- 5.3. Market Analysis, Insights and Forecast - by Product Type

- 5.3.1. Milk Kefir

- 5.3.1.1. Dairy based

- 5.3.1.2. Non-dairy based

- 5.3.2. Water Kefir

- 5.3.1. Milk Kefir

- 5.4. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.4.1. Supermarkets/Hypermarkets

- 5.4.2. Convenience Stores

- 5.4.3. Online Retail Stores

- 5.4.4. Other Distribution Channels

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. North America

- 5.5.2. Europe

- 5.5.3. Asia Pacific

- 5.5.4. South America

- 5.5.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Form

- 6. Global Kefir Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Form

- 6.1.1. Organic

- 6.1.2. Conventional

- 6.2. Market Analysis, Insights and Forecast - by Category

- 6.2.1. Flavored kefir

- 6.2.2. Non-flavored kefir

- 6.3. Market Analysis, Insights and Forecast - by Product Type

- 6.3.1. Milk Kefir

- 6.3.1.1. Dairy based

- 6.3.1.2. Non-dairy based

- 6.3.2. Water Kefir

- 6.3.1. Milk Kefir

- 6.4. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.4.1. Supermarkets/Hypermarkets

- 6.4.2. Convenience Stores

- 6.4.3. Online Retail Stores

- 6.4.4. Other Distribution Channels

- 6.1. Market Analysis, Insights and Forecast - by Form

- 7. North America Kefir Industry Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Form

- 7.1.1. Organic

- 7.1.2. Conventional

- 7.2. Market Analysis, Insights and Forecast - by Category

- 7.2.1. Flavored kefir

- 7.2.2. Non-flavored kefir

- 7.3. Market Analysis, Insights and Forecast - by Product Type

- 7.3.1. Milk Kefir

- 7.3.1.1. Dairy based

- 7.3.1.2. Non-dairy based

- 7.3.2. Water Kefir

- 7.3.1. Milk Kefir

- 7.4. Market Analysis, Insights and Forecast - by Distribution Channel

- 7.4.1. Supermarkets/Hypermarkets

- 7.4.2. Convenience Stores

- 7.4.3. Online Retail Stores

- 7.4.4. Other Distribution Channels

- 7.1. Market Analysis, Insights and Forecast - by Form

- 8. Europe Kefir Industry Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Form

- 8.1.1. Organic

- 8.1.2. Conventional

- 8.2. Market Analysis, Insights and Forecast - by Category

- 8.2.1. Flavored kefir

- 8.2.2. Non-flavored kefir

- 8.3. Market Analysis, Insights and Forecast - by Product Type

- 8.3.1. Milk Kefir

- 8.3.1.1. Dairy based

- 8.3.1.2. Non-dairy based

- 8.3.2. Water Kefir

- 8.3.1. Milk Kefir

- 8.4. Market Analysis, Insights and Forecast - by Distribution Channel

- 8.4.1. Supermarkets/Hypermarkets

- 8.4.2. Convenience Stores

- 8.4.3. Online Retail Stores

- 8.4.4. Other Distribution Channels

- 8.1. Market Analysis, Insights and Forecast - by Form

- 9. Asia Pacific Kefir Industry Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Form

- 9.1.1. Organic

- 9.1.2. Conventional

- 9.2. Market Analysis, Insights and Forecast - by Category

- 9.2.1. Flavored kefir

- 9.2.2. Non-flavored kefir

- 9.3. Market Analysis, Insights and Forecast - by Product Type

- 9.3.1. Milk Kefir

- 9.3.1.1. Dairy based

- 9.3.1.2. Non-dairy based

- 9.3.2. Water Kefir

- 9.3.1. Milk Kefir

- 9.4. Market Analysis, Insights and Forecast - by Distribution Channel

- 9.4.1. Supermarkets/Hypermarkets

- 9.4.2. Convenience Stores

- 9.4.3. Online Retail Stores

- 9.4.4. Other Distribution Channels

- 9.1. Market Analysis, Insights and Forecast - by Form

- 10. South America Kefir Industry Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Form

- 10.1.1. Organic

- 10.1.2. Conventional

- 10.2. Market Analysis, Insights and Forecast - by Category

- 10.2.1. Flavored kefir

- 10.2.2. Non-flavored kefir

- 10.3. Market Analysis, Insights and Forecast - by Product Type

- 10.3.1. Milk Kefir

- 10.3.1.1. Dairy based

- 10.3.1.2. Non-dairy based

- 10.3.2. Water Kefir

- 10.3.1. Milk Kefir

- 10.4. Market Analysis, Insights and Forecast - by Distribution Channel

- 10.4.1. Supermarkets/Hypermarkets

- 10.4.2. Convenience Stores

- 10.4.3. Online Retail Stores

- 10.4.4. Other Distribution Channels

- 10.1. Market Analysis, Insights and Forecast - by Form

- 11. Middle East and Africa Kefir Industry Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Form

- 11.1.1. Organic

- 11.1.2. Conventional

- 11.2. Market Analysis, Insights and Forecast - by Category

- 11.2.1. Flavored kefir

- 11.2.2. Non-flavored kefir

- 11.3. Market Analysis, Insights and Forecast - by Product Type

- 11.3.1. Milk Kefir

- 11.3.1.1. Dairy based

- 11.3.1.2. Non-dairy based

- 11.3.2. Water Kefir

- 11.3.1. Milk Kefir

- 11.4. Market Analysis, Insights and Forecast - by Distribution Channel

- 11.4.1. Supermarkets/Hypermarkets

- 11.4.2. Convenience Stores

- 11.4.3. Online Retail Stores

- 11.4.4. Other Distribution Channels

- 11.1. Market Analysis, Insights and Forecast - by Form

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Green Valley Creamery

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 The Icelandic Milk and Skyr Corporatio

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Emmi AG (Redwood Hill Farm & Creamery)

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 The Hain Celestial Group Inc

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Lifeway Foods Inc

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Danone S A

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Maple Hill Creamery LLC

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Biotiful Dairy

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Evolve Kefir

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Nestlé S A

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Green Valley Creamery

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Kefir Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Kefir Industry Revenue (billion), by Form 2025 & 2033

- Figure 3: North America Kefir Industry Revenue Share (%), by Form 2025 & 2033

- Figure 4: North America Kefir Industry Revenue (billion), by Category 2025 & 2033

- Figure 5: North America Kefir Industry Revenue Share (%), by Category 2025 & 2033

- Figure 6: North America Kefir Industry Revenue (billion), by Product Type 2025 & 2033

- Figure 7: North America Kefir Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 8: North America Kefir Industry Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 9: North America Kefir Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 10: North America Kefir Industry Revenue (billion), by Country 2025 & 2033

- Figure 11: North America Kefir Industry Revenue Share (%), by Country 2025 & 2033

- Figure 12: Europe Kefir Industry Revenue (billion), by Form 2025 & 2033

- Figure 13: Europe Kefir Industry Revenue Share (%), by Form 2025 & 2033

- Figure 14: Europe Kefir Industry Revenue (billion), by Category 2025 & 2033

- Figure 15: Europe Kefir Industry Revenue Share (%), by Category 2025 & 2033

- Figure 16: Europe Kefir Industry Revenue (billion), by Product Type 2025 & 2033

- Figure 17: Europe Kefir Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 18: Europe Kefir Industry Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 19: Europe Kefir Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 20: Europe Kefir Industry Revenue (billion), by Country 2025 & 2033

- Figure 21: Europe Kefir Industry Revenue Share (%), by Country 2025 & 2033

- Figure 22: Asia Pacific Kefir Industry Revenue (billion), by Form 2025 & 2033

- Figure 23: Asia Pacific Kefir Industry Revenue Share (%), by Form 2025 & 2033

- Figure 24: Asia Pacific Kefir Industry Revenue (billion), by Category 2025 & 2033

- Figure 25: Asia Pacific Kefir Industry Revenue Share (%), by Category 2025 & 2033

- Figure 26: Asia Pacific Kefir Industry Revenue (billion), by Product Type 2025 & 2033

- Figure 27: Asia Pacific Kefir Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 28: Asia Pacific Kefir Industry Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 29: Asia Pacific Kefir Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 30: Asia Pacific Kefir Industry Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Kefir Industry Revenue Share (%), by Country 2025 & 2033

- Figure 32: South America Kefir Industry Revenue (billion), by Form 2025 & 2033

- Figure 33: South America Kefir Industry Revenue Share (%), by Form 2025 & 2033

- Figure 34: South America Kefir Industry Revenue (billion), by Category 2025 & 2033

- Figure 35: South America Kefir Industry Revenue Share (%), by Category 2025 & 2033

- Figure 36: South America Kefir Industry Revenue (billion), by Product Type 2025 & 2033

- Figure 37: South America Kefir Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 38: South America Kefir Industry Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 39: South America Kefir Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 40: South America Kefir Industry Revenue (billion), by Country 2025 & 2033

- Figure 41: South America Kefir Industry Revenue Share (%), by Country 2025 & 2033

- Figure 42: Middle East and Africa Kefir Industry Revenue (billion), by Form 2025 & 2033

- Figure 43: Middle East and Africa Kefir Industry Revenue Share (%), by Form 2025 & 2033

- Figure 44: Middle East and Africa Kefir Industry Revenue (billion), by Category 2025 & 2033

- Figure 45: Middle East and Africa Kefir Industry Revenue Share (%), by Category 2025 & 2033

- Figure 46: Middle East and Africa Kefir Industry Revenue (billion), by Product Type 2025 & 2033

- Figure 47: Middle East and Africa Kefir Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 48: Middle East and Africa Kefir Industry Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 49: Middle East and Africa Kefir Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 50: Middle East and Africa Kefir Industry Revenue (billion), by Country 2025 & 2033

- Figure 51: Middle East and Africa Kefir Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Kefir Industry Revenue billion Forecast, by Form 2020 & 2033

- Table 2: Global Kefir Industry Revenue billion Forecast, by Category 2020 & 2033

- Table 3: Global Kefir Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 4: Global Kefir Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 5: Global Kefir Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Global Kefir Industry Revenue billion Forecast, by Form 2020 & 2033

- Table 7: Global Kefir Industry Revenue billion Forecast, by Category 2020 & 2033

- Table 8: Global Kefir Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 9: Global Kefir Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 10: Global Kefir Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 11: United States Kefir Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Canada Kefir Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Mexico Kefir Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Rest of North America Kefir Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Global Kefir Industry Revenue billion Forecast, by Form 2020 & 2033

- Table 16: Global Kefir Industry Revenue billion Forecast, by Category 2020 & 2033

- Table 17: Global Kefir Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 18: Global Kefir Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 19: Global Kefir Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 20: Germany Kefir Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: United Kingdom Kefir Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Kefir Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Kefir Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: France Kefir Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Russia Kefir Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Rest of Europe Kefir Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Global Kefir Industry Revenue billion Forecast, by Form 2020 & 2033

- Table 28: Global Kefir Industry Revenue billion Forecast, by Category 2020 & 2033

- Table 29: Global Kefir Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 30: Global Kefir Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 31: Global Kefir Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 32: China Kefir Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: Japan Kefir Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: India Kefir Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: Australia Kefir Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Asia Pacific Kefir Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Kefir Industry Revenue billion Forecast, by Form 2020 & 2033

- Table 38: Global Kefir Industry Revenue billion Forecast, by Category 2020 & 2033

- Table 39: Global Kefir Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 40: Global Kefir Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 41: Global Kefir Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 42: Brazil Kefir Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: Argentina Kefir Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: Rest of South America Kefir Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Global Kefir Industry Revenue billion Forecast, by Form 2020 & 2033

- Table 46: Global Kefir Industry Revenue billion Forecast, by Category 2020 & 2033

- Table 47: Global Kefir Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 48: Global Kefir Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 49: Global Kefir Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 50: South Africa Kefir Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 51: United Arab Emirates Kefir Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 52: Rest of Middle East and Africa Kefir Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Kefir Industry?

The projected CAGR is approximately 5%.

2. Which companies are prominent players in the Kefir Industry?

Key companies in the market include Green Valley Creamery, The Icelandic Milk and Skyr Corporatio, Emmi AG (Redwood Hill Farm & Creamery), The Hain Celestial Group Inc, Lifeway Foods Inc, Danone S A, Maple Hill Creamery LLC, Biotiful Dairy, Evolve Kefir, Nestlé S A.

3. What are the main segments of the Kefir Industry?

The market segments include Form, Category, Product Type, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.26 billion as of 2022.

5. What are some drivers contributing to market growth?

Wide Applications and Functionality; Low Price and Easy Availability of Synthetic Phenethyl Alcohol.

6. What are the notable trends driving market growth?

Increasing Demand For Probiotics Drinks.

7. Are there any restraints impacting market growth?

Availability of Substitutes.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Kefir Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Kefir Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Kefir Industry?

To stay informed about further developments, trends, and reports in the Kefir Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence