Key Insights

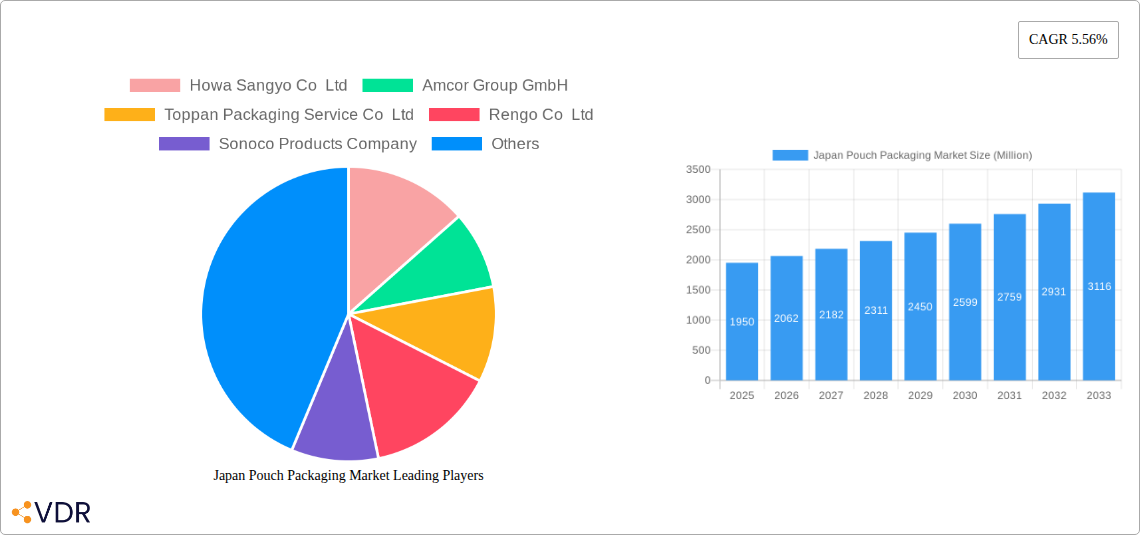

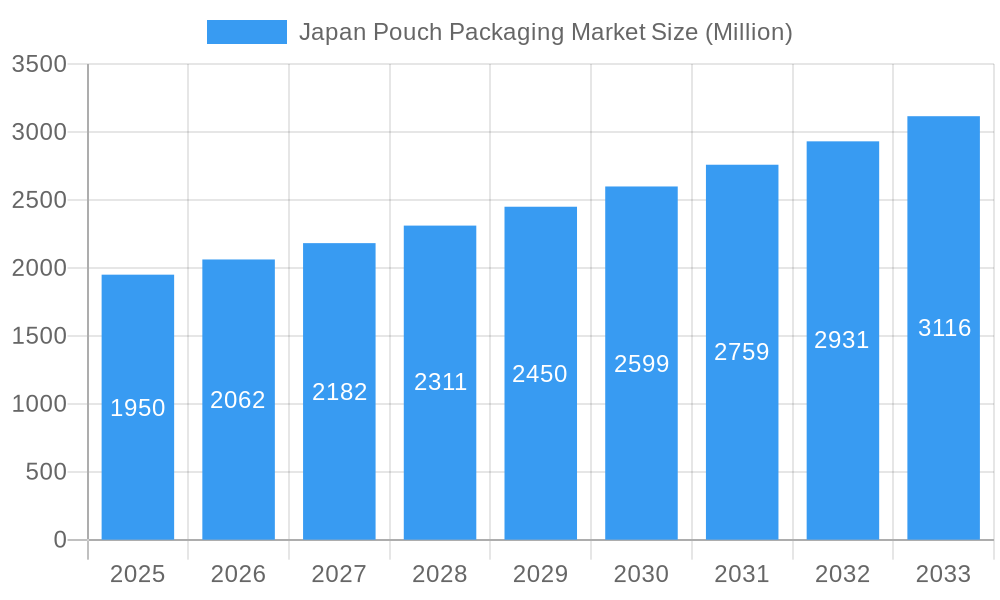

The Japan pouch packaging market is poised for robust expansion, projecting a current market size of approximately USD 1.95 billion and a Compound Annual Growth Rate (CAGR) of 5.56% through 2033. This steady growth trajectory is primarily fueled by a confluence of evolving consumer preferences and significant advancements in packaging technology. Consumers in Japan are increasingly demanding convenience, extended shelf life, and visually appealing packaging solutions, all of which pouches effectively deliver. The inherent versatility of pouch packaging, from single-serving sachets to larger stand-up pouches, caters to a wide array of product categories, including food, beverages, medical supplies, and personal care items. Furthermore, the ongoing innovation in materials science is enabling the development of more sustainable and functional pouches, incorporating features like enhanced barrier properties, tamper-evidence, and improved recyclability, thereby addressing growing environmental concerns and regulatory pressures.

Japan Pouch Packaging Market Market Size (In Billion)

The market's dynamism is further underscored by key drivers such as the escalating demand for premium and convenient food options, including confectionery, frozen foods, and ready-to-eat meals, where pouches offer optimal product protection and ease of use. The burgeoning e-commerce sector also plays a crucial role, as pouches provide a lightweight, space-efficient, and durable solution for shipping and handling a variety of goods. However, the market is not without its challenges. Potential restraints include the fluctuating costs of raw materials, particularly plastics and aluminum, which can impact manufacturers' profit margins and influence pricing strategies. Stringent environmental regulations, while driving innovation towards sustainable alternatives, can also present compliance hurdles and necessitate significant investment in new technologies and materials. Despite these challenges, the continuous innovation in pouch designs and materials, coupled with strategic collaborations among key industry players like Amcor Group GmbH and Toppan Packaging Service Co Ltd, is expected to propel the Japan pouch packaging market forward.

Japan Pouch Packaging Market Company Market Share

Japan Pouch Packaging Market: Comprehensive Analysis and Forecast (2019-2033)

This in-depth report offers a definitive analysis of the Japan pouch packaging market, providing critical insights into market dynamics, growth trends, regional dominance, product innovations, key drivers, challenges, and emerging opportunities. With a meticulous study period spanning 2019 to 2033, featuring a base year of 2025 and a forecast period from 2025 to 2033, this report is an indispensable resource for industry professionals seeking to navigate and capitalize on the evolving landscape of flexible packaging solutions in Japan.

Key High-Traffic Keywords: Japan pouch packaging, flexible packaging Japan, food packaging Japan, beverage packaging Japan, medical packaging Japan, pharmaceutical packaging Japan, stand-up pouches Japan, retort pouches Japan, recyclable packaging Japan, sustainable packaging Japan, plastic packaging Japan, paper packaging Japan, aluminum packaging Japan, pouch packaging market size Japan, pouch packaging market share Japan, Japan packaging industry, packaging innovations Japan, market growth Japan, CAGR Japan, market dynamics Japan.

Parent & Child Market Focus: This report delves into the intricacies of the Japan pouch packaging market, examining its relationship with broader flexible packaging markets and dissecting the growth within specific product types like stand-up pouches and flat pouches (pillow & side-seal), and their adoption across diverse end-user industries.

All values presented in Million units unless otherwise specified.

Japan Pouch Packaging Market Market Dynamics & Structure

The Japan pouch packaging market exhibits a moderate level of market concentration, with a few key players holding significant market share, yet fostering healthy competition. Technological innovation is a primary driver, fueled by a strong emphasis on sustainable packaging and advanced barrier properties essential for the food packaging Japan and pharmaceutical packaging Japan sectors. Regulatory frameworks, particularly those promoting recyclability and waste reduction, are increasingly shaping product development and material choices, impacting the plastic packaging Japan segment. Competitive product substitutes, such as rigid containers, continue to pose a challenge, though the inherent advantages of flexible packaging Japan in terms of material efficiency and convenience are gaining traction. End-user demographics are shifting towards convenience-seeking consumers and a growing aging population, driving demand for easy-to-open and portion-controlled pouch packaging Japan. Mergers and acquisitions (M&A) activity, while not exceptionally high, are strategically focused on expanding capabilities in sustainable materials and specialized pouch formats.

- Market Concentration: Dominated by a blend of multinational corporations and strong domestic players, with an estimated market concentration ratio of approximately 60-70% held by the top 5-7 companies.

- Technological Innovation Drivers: Focus on high-barrier films, retortable pouches for extended shelf life, advanced printing technologies, and the development of mono-material solutions for enhanced recyclability.

- Regulatory Frameworks: Stringent regulations surrounding food safety, environmental impact, and waste management are encouraging the adoption of eco-friendly pouch materials.

- Competitive Product Substitutes: Glass jars, metal cans, and rigid plastic containers.

- End-User Demographics: Increasing demand from the convenience food sector, the growing elderly population requiring easy-to-use packaging, and a rising awareness of health and wellness.

- M&A Trends: Acquisitions aimed at bolstering capabilities in recyclable materials and specialized functional pouches.

Japan Pouch Packaging Market Growth Trends & Insights

The Japan pouch packaging market is poised for robust growth, driven by evolving consumer preferences, technological advancements, and a persistent push towards sustainability. The market size is projected to expand significantly, reflecting an increasing adoption rate of pouch formats across various industries. Technological disruptions, particularly in material science and manufacturing processes, are enabling the creation of pouches with enhanced functionalities, such as improved barrier properties, retortability, and tamper-evidence, directly impacting the food packaging Japan and medical packaging Japan sectors. Consumer behavior shifts are a pivotal factor; the demand for convenience, smaller portion sizes, and on-the-go consumption further fuels the adoption of stand-up pouches Japan and other flexible formats.

The historical period (2019-2024) has witnessed a steady upward trajectory, influenced by the growing popularity of processed and ready-to-eat meals, alongside a greater emphasis on aesthetically pleasing and informative packaging. The base year, 2025, serves as a critical benchmark for future projections. The forecast period (2025-2033) is expected to see an accelerated compound annual growth rate (CAGR) of approximately 5.5% to 7.0%. This growth will be underpinned by continued innovation in recyclable and compostable materials, addressing environmental concerns and aligning with government initiatives. The penetration of flexible packaging Japan is set to deepen, challenging traditional packaging methods. Furthermore, the expanding e-commerce landscape necessitates robust and lightweight packaging solutions, a domain where pouches excel. The integration of smart packaging features, such as track-and-trace capabilities and shelf-life indicators, will also contribute to market expansion, particularly in the pharmaceutical packaging Japan and high-value food product segments. The shift towards premiumization in categories like snacks and specialty foods is also driving demand for high-quality, visually appealing pouches.

Dominant Regions, Countries, or Segments in Japan Pouch Packaging Market

The Japan pouch packaging market is predominantly driven by the Food end-user industry segment, which accounts for a substantial share of the market's volume and value. Within the food sector, specific sub-segments exhibit particularly strong demand for pouch packaging. Dry Foods, including rice, grains, and snacks, consistently represent a major consumer of flat and stand-up pouches due to their excellent barrier properties, shelf-stability, and cost-effectiveness. Frozen Foods also present a significant growth area, with specialized retortable pouches and freezer-grade flexible packaging becoming increasingly prevalent to maintain product quality and extend shelf life. The burgeoning market for Pet Food is another key driver, where resealable stand-up pouches offer convenience and freshness preservation for pet owners.

The Plastic material segment, specifically Polyethylene (PE) and Polypropylene (PP), dominates the Japan pouch packaging market. These versatile polymers offer a balance of cost, performance, and flexibility, making them suitable for a wide range of applications. PET (Polyethylene Terephthalate) is frequently used for its clarity and barrier properties, especially in premium food and beverage applications. The ongoing research and development in advanced resins like EVOH (Ethylene Vinyl Alcohol) are crucial for achieving superior gas and moisture barriers, which are vital for extending the shelf life of perishable goods, thus driving demand for specialized pouches in segments like Dairy Products and Meat, Poultry, and Seafood.

Geographically, while the entire nation benefits from the growth in pouch packaging, the Kanto region, encompassing Tokyo and its surrounding prefectures, is a major hub for consumption and manufacturing. This region's dense population, high concentration of food processing companies, and advanced logistics infrastructure contribute to its dominance. The focus on convenience and the presence of major retail chains in this area further amplify the demand for various pouch formats. The development of advanced manufacturing facilities and a strong research and development ecosystem within the Kanto region also position it as a leader in adopting and driving new packaging technologies.

- Dominant End-User Industry: Food (approx. 60-70% market share)

- Key Sub-segments: Dry Foods, Frozen Foods, Pet Food, Dairy Products, Meat, Poultry, and Seafood.

- Drivers: Convenience, shelf-life extension, product protection, portion control.

- Dominant Material Segment: Plastic (approx. 70-80% market share)

- Key Resins: Polyethylene (PE), Polypropylene (PP), PET.

- Emerging Resins: EVOH for enhanced barrier properties.

- Drivers: Cost-effectiveness, versatility, barrier properties, printability.

- Dominant Geographic Region: Kanto Region

- Drivers: High population density, concentration of food manufacturers and retailers, advanced logistics, strong R&D capabilities.

Japan Pouch Packaging Market Product Landscape

The Japan pouch packaging market is characterized by a dynamic product landscape driven by innovation and the pursuit of enhanced functionality. Stand-up pouches continue to gain significant traction due to their excellent shelf presence, consumer convenience, and resealability, making them ideal for snacks, confectionery, and dry foods. Flat pouches, including pillow and side-seal varieties, remain a staple for a wide array of products, particularly in the food and personal care sectors, where cost-effectiveness and high-speed filling are paramount. The increasing demand for retortable pouches is a notable trend, enabling the sterilization of food products and extending shelf life without refrigeration, crucial for items like ready-to-eat meals and certain medical supplies. Material innovation is also a key differentiator, with a growing emphasis on mono-material structures for improved recyclability and the incorporation of advanced barrier films like EVOH to protect sensitive contents from oxygen and moisture. The market also sees ongoing developments in specialty pouches, including those with unique dispensing mechanisms, tamper-evident features, and enhanced sustainability profiles.

Key Drivers, Barriers & Challenges in Japan Pouch Packaging Market

Key Drivers:

- Growing demand for convenience: Consumers increasingly prefer easy-to-open, single-serving, and portable packaging formats like pouches, driving adoption in the food, beverage, and personal care sectors.

- Sustainability initiatives: Strong government policies and growing consumer awareness are pushing for recyclable, biodegradable, and compostable pouch solutions, creating opportunities for eco-friendly materials and designs.

- Technological advancements: Innovations in material science, printing, and converting technologies are enabling the development of pouches with superior barrier properties, extended shelf life, and enhanced functionality.

- E-commerce growth: The expansion of online retail necessitates lightweight, durable, and protective packaging, where pouches offer significant advantages.

- Product differentiation: Pouches offer excellent branding and visual appeal, allowing manufacturers to differentiate their products on retail shelves.

Barriers & Challenges:

- Recyclability concerns for multi-material pouches: While progress is being made, the recyclability of complex multi-material pouches remains a challenge, requiring significant investment in recycling infrastructure and consumer education.

- Competition from rigid packaging: Traditional rigid containers still hold a significant market share and can be perceived as more robust for certain applications.

- Raw material price volatility: Fluctuations in the cost of plastic resins and other raw materials can impact manufacturing costs and profit margins.

- Food safety regulations: Meeting stringent food safety standards for packaging materials requires continuous investment in quality control and compliance.

- Infrastructure limitations for specialized recycling: The widespread collection and processing of specific types of recyclable pouches require further development of dedicated recycling facilities.

Emerging Opportunities in Japan Pouch Packaging Market

Emerging opportunities in the Japan pouch packaging market are largely centered around sustainability and specialized applications. The development and adoption of fully recyclable and compostable mono-material pouches present a significant growth avenue, aligning with Japan's ambitious environmental targets. The increasing demand for shelf-stable, ready-to-eat meals and specialty food products is creating a need for advanced retortable and barrier pouches, offering a unique selling proposition for manufacturers. Furthermore, the expansion of e-commerce provides opportunities for lightweight, protective, and tamper-evident pouch solutions. The medical and pharmaceutical packaging Japan sector is another fertile ground for innovation, with demand for sterile, single-dose pouches and specialized delivery systems. As consumer preferences lean towards smaller portion sizes and personalized nutrition, opportunities arise for customized and highly functional pouch designs.

Growth Accelerators in the Japan Pouch Packaging Market Industry

Several key catalysts are accelerating the growth of the Japan pouch packaging market. Technological breakthroughs in material science, particularly in the development of high-performance, sustainable polymers and barrier technologies, are enabling the creation of pouches that meet increasingly stringent performance and environmental demands. Strategic partnerships between material suppliers, packaging converters, and end-users are fostering collaborative innovation and speeding up the market introduction of novel pouch solutions. Market expansion strategies, including the development of pouches for emerging product categories and the penetration into underserved regions, are also contributing to overall growth. The increasing focus on circular economy principles within the packaging industry is a powerful growth accelerator, driving investment in recycling technologies and the design of easily recyclable pouch structures.

Key Players Shaping the Japan Pouch Packaging Market Market

- Howa Sangyo Co Ltd

- Amcor Group GmbH

- Toppan Packaging Service Co Ltd

- Rengo Co Ltd

- Sonoco Products Company

- Hosokawa Yoko Co Ltd

- Sealed Air Corporation

- Takigawa Corporation

Notable Milestones in Japan Pouch Packaging Market Sector

- February 2024: Rengo Co. Ltd, a prominent Japanese packaging company, clinched two prestigious accolades at the 2024 WorldStar Packaging Awards, highlighting their commitment to innovation and quality in packaging solutions.

- April 2023: Toppan Packaging Service Co. Ltd, a Japanese company, secured gold at the 2023 Australasian Packaging Innovation and Design Awards (PIDA). Its winning entry was a retortable PP mono-material packaging tailored to the food sector. This innovative packaging not only boasts recyclability but also offers an exceptional barrier performance, catering to the stringent demands of the food industry.

In-Depth Japan Pouch Packaging Market Market Outlook

The future outlook for the Japan pouch packaging market is exceptionally positive, driven by a confluence of factors that align with global trends in sustainability, convenience, and technological advancement. The ongoing shift towards a circular economy and stringent environmental regulations will continue to fuel innovation in recyclable and compostable materials, creating significant opportunities for companies offering eco-friendly pouch solutions. The robust growth of the food and beverage sector, coupled with evolving consumer preferences for on-the-go consumption and portion-controlled packaging, will sustain demand for versatile pouch formats like stand-up and retort pouches. Strategic investments in advanced manufacturing technologies and collaborative efforts across the value chain will accelerate the development and adoption of next-generation pouches with enhanced functionalities. The expanding e-commerce landscape will further solidify the importance of lightweight, durable, and protective packaging solutions, where pouches are ideally positioned. The Japan pouch packaging market is therefore set to witness sustained growth, presenting lucrative prospects for stakeholders committed to innovation and sustainability.

Japan Pouch Packaging Market Segmentation

-

1. Material

-

1.1. Plastic

- 1.1.1. Polyethylene

- 1.1.2. Polypropylene

- 1.1.3. PET

- 1.1.4. PVC

- 1.1.5. EVOH

- 1.1.6. Other Resins

- 1.2. Paper

- 1.3. Aluminum

-

1.1. Plastic

-

2. Product

- 2.1. Flat (Pillow & Side-Seal)

- 2.2. Stand-up

-

3. End-User Industry

-

3.1. Food

- 3.1.1. Candy & Confectionery

- 3.1.2. Frozen Foods

- 3.1.3. Fresh Produce

- 3.1.4. Dairy Products

- 3.1.5. Dry Foods

- 3.1.6. Meat, Poultry, And Seafood

- 3.1.7. Pet Food

- 3.1.8. Other Fo

- 3.2. Beverage

- 3.3. Medical and Pharmaceutical

- 3.4. Personal Care and Household Care

- 3.5. Other En

-

3.1. Food

Japan Pouch Packaging Market Segmentation By Geography

- 1. Japan

Japan Pouch Packaging Market Regional Market Share

Geographic Coverage of Japan Pouch Packaging Market

Japan Pouch Packaging Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.56% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Material

- 5.1.1. Plastic

- 5.1.1.1. Polyethylene

- 5.1.1.2. Polypropylene

- 5.1.1.3. PET

- 5.1.1.4. PVC

- 5.1.1.5. EVOH

- 5.1.1.6. Other Resins

- 5.1.2. Paper

- 5.1.3. Aluminum

- 5.1.1. Plastic

- 5.2. Market Analysis, Insights and Forecast - by Product

- 5.2.1. Flat (Pillow & Side-Seal)

- 5.2.2. Stand-up

- 5.3. Market Analysis, Insights and Forecast - by End-User Industry

- 5.3.1. Food

- 5.3.1.1. Candy & Confectionery

- 5.3.1.2. Frozen Foods

- 5.3.1.3. Fresh Produce

- 5.3.1.4. Dairy Products

- 5.3.1.5. Dry Foods

- 5.3.1.6. Meat, Poultry, And Seafood

- 5.3.1.7. Pet Food

- 5.3.1.8. Other Fo

- 5.3.2. Beverage

- 5.3.3. Medical and Pharmaceutical

- 5.3.4. Personal Care and Household Care

- 5.3.5. Other En

- 5.3.1. Food

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Japan

- 5.1. Market Analysis, Insights and Forecast - by Material

- 6. Japan Pouch Packaging Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Material

- 6.1.1. Plastic

- 6.1.1.1. Polyethylene

- 6.1.1.2. Polypropylene

- 6.1.1.3. PET

- 6.1.1.4. PVC

- 6.1.1.5. EVOH

- 6.1.1.6. Other Resins

- 6.1.2. Paper

- 6.1.3. Aluminum

- 6.1.1. Plastic

- 6.2. Market Analysis, Insights and Forecast - by Product

- 6.2.1. Flat (Pillow & Side-Seal)

- 6.2.2. Stand-up

- 6.3. Market Analysis, Insights and Forecast - by End-User Industry

- 6.3.1. Food

- 6.3.1.1. Candy & Confectionery

- 6.3.1.2. Frozen Foods

- 6.3.1.3. Fresh Produce

- 6.3.1.4. Dairy Products

- 6.3.1.5. Dry Foods

- 6.3.1.6. Meat, Poultry, And Seafood

- 6.3.1.7. Pet Food

- 6.3.1.8. Other Fo

- 6.3.2. Beverage

- 6.3.3. Medical and Pharmaceutical

- 6.3.4. Personal Care and Household Care

- 6.3.5. Other En

- 6.3.1. Food

- 6.1. Market Analysis, Insights and Forecast - by Material

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Howa Sangyo Co Ltd

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Amcor Group GmbH

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Toppan Packaging Service Co Ltd

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Rengo Co Ltd

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Sonoco Products Company

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Hosokawa Yoko Co Ltd

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Sealed Air Corporation

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Takigawa Corporation10 2 Heat Map Analysi

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.1 Howa Sangyo Co Ltd

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Japan Pouch Packaging Market Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Japan Pouch Packaging Market Share (%) by Company 2025

List of Tables

- Table 1: Japan Pouch Packaging Market Revenue Million Forecast, by Material 2020 & 2033

- Table 2: Japan Pouch Packaging Market Volume Billion Forecast, by Material 2020 & 2033

- Table 3: Japan Pouch Packaging Market Revenue Million Forecast, by Product 2020 & 2033

- Table 4: Japan Pouch Packaging Market Volume Billion Forecast, by Product 2020 & 2033

- Table 5: Japan Pouch Packaging Market Revenue Million Forecast, by End-User Industry 2020 & 2033

- Table 6: Japan Pouch Packaging Market Volume Billion Forecast, by End-User Industry 2020 & 2033

- Table 7: Japan Pouch Packaging Market Revenue Million Forecast, by Region 2020 & 2033

- Table 8: Japan Pouch Packaging Market Volume Billion Forecast, by Region 2020 & 2033

- Table 9: Japan Pouch Packaging Market Revenue Million Forecast, by Material 2020 & 2033

- Table 10: Japan Pouch Packaging Market Volume Billion Forecast, by Material 2020 & 2033

- Table 11: Japan Pouch Packaging Market Revenue Million Forecast, by Product 2020 & 2033

- Table 12: Japan Pouch Packaging Market Volume Billion Forecast, by Product 2020 & 2033

- Table 13: Japan Pouch Packaging Market Revenue Million Forecast, by End-User Industry 2020 & 2033

- Table 14: Japan Pouch Packaging Market Volume Billion Forecast, by End-User Industry 2020 & 2033

- Table 15: Japan Pouch Packaging Market Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Japan Pouch Packaging Market Volume Billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Japan Pouch Packaging Market?

The projected CAGR is approximately 5.56%.

2. Which companies are prominent players in the Japan Pouch Packaging Market?

Key companies in the market include Howa Sangyo Co Ltd, Amcor Group GmbH, Toppan Packaging Service Co Ltd, Rengo Co Ltd, Sonoco Products Company, Hosokawa Yoko Co Ltd, Sealed Air Corporation, Takigawa Corporation10 2 Heat Map Analysi.

3. What are the main segments of the Japan Pouch Packaging Market?

The market segments include Material, Product, End-User Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.95 Million as of 2022.

5. What are some drivers contributing to market growth?

Growing Demand of Pouch Packaging in Food Industry; Increasing Popularity of Standard Pouches for Various Industries.

6. What are the notable trends driving market growth?

The Standard Pouch Segment is Expected to Register the Fastest Growth.

7. Are there any restraints impacting market growth?

Growing Demand of Pouch Packaging in Food Industry; Increasing Popularity of Standard Pouches for Various Industries.

8. Can you provide examples of recent developments in the market?

February 2024: Rengo Co. Ltd, a prominent Japanese packaging company, clinched two prestigious accolades at the 2024 WorldStar Packaging Awards.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in Billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Japan Pouch Packaging Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Japan Pouch Packaging Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Japan Pouch Packaging Market?

To stay informed about further developments, trends, and reports in the Japan Pouch Packaging Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence