Key Insights

The Japan Car Insurance market is poised for robust growth, projected to reach an estimated USD 20.31 million by 2025, with a significant Compound Annual Growth Rate (CAGR) of 5.21%. This expansion is fueled by several key drivers, including an increasing number of vehicles on the road, a rising awareness of the necessity for comprehensive protection against accidents and damages, and evolving regulatory frameworks that mandate specific levels of coverage. The market is segmented across various coverage types, with Third-Party Liability Coverage remaining a foundational offering, while Collision/Comprehensive/Other Optional Coverage is experiencing strong demand as consumers seek enhanced protection. The application landscape spans both Personal Vehicles, which constitute the largest segment due to widespread private car ownership, and Commercial Vehicles, driven by the logistical needs of businesses. Distribution channels are diversifying, with Direct Sales and Insurance Agents continuing to be prominent, alongside a notable surge in Online platforms and Banks, reflecting a shift towards digital and integrated financial services.

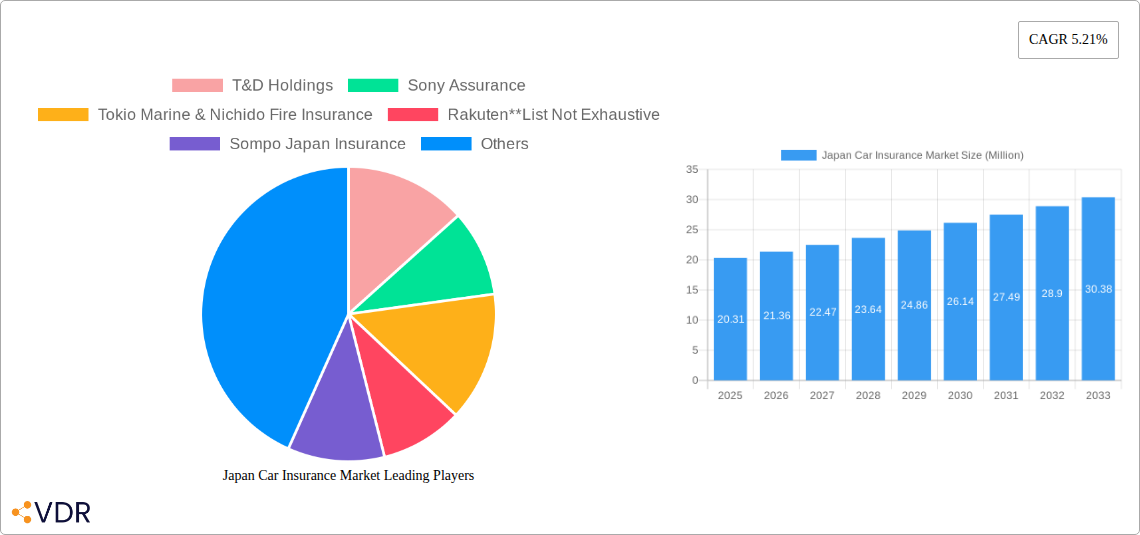

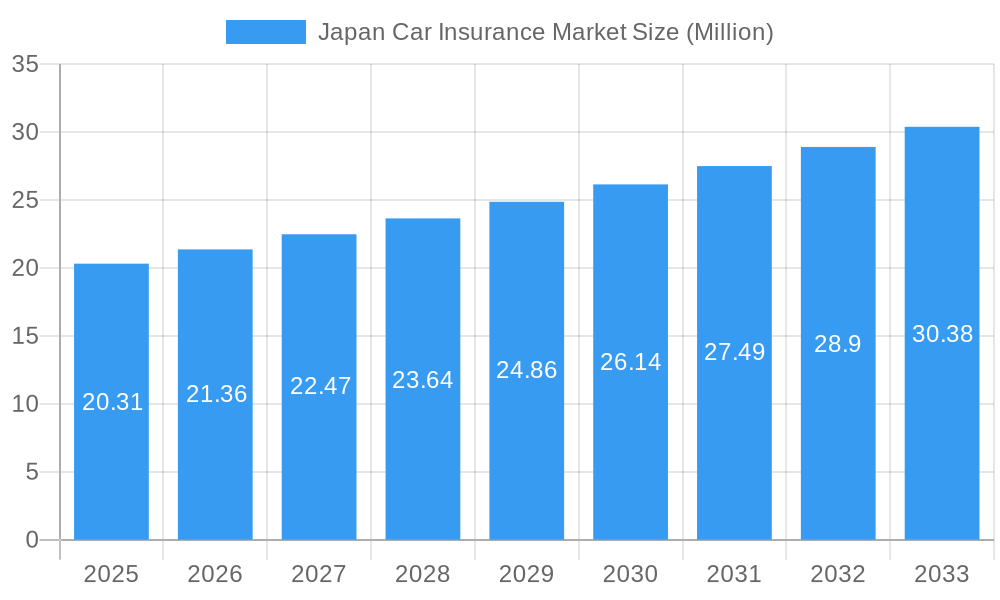

Japan Car Insurance Market Market Size (In Million)

The competitive landscape is dynamic, featuring established giants like Tokio Marine & Nichido Fire Insurance, Mitsui Sumitomo Insurance, and MS&AD Insurance Group Holdings, alongside agile digital players such as Rakuten and Sony Assurance. These companies are actively innovating to cater to evolving consumer preferences, offering personalized policies, telematics-based pricing, and streamlined claims processes. Emerging trends like the integration of AI and IoT for risk assessment and personalized insurance products are shaping the future of the market. However, certain restraints exist, including a maturing market in some traditional segments, increasing competition leading to price pressures, and the potential impact of economic slowdowns on consumer discretionary spending. Despite these challenges, the underlying demand for reliable and accessible car insurance in Japan, coupled with technological advancements and a growing emphasis on safety, ensures a promising outlook for continued market expansion throughout the forecast period of 2025-2033.

Japan Car Insurance Market Company Market Share

Japan Car Insurance Market: Comprehensive Report & Future Outlook (2019-2033)

This in-depth report provides a comprehensive analysis of the Japan Car Insurance Market, examining its dynamics, growth trends, regional dominance, product landscape, key drivers, barriers, challenges, emerging opportunities, and future outlook. With a study period spanning from 2019 to 2033, a base year of 2025, and a forecast period from 2025 to 2033, this report offers invaluable insights for industry professionals, investors, and stakeholders seeking to understand the intricacies and future trajectory of this vital sector. The report integrates high-traffic keywords and analyzes parent and child markets to maximize search engine visibility and deliver targeted information, presenting all values in Million units.

Japan Car Insurance Market Market Dynamics & Structure

The Japan Car Insurance Market exhibits a dynamic landscape characterized by a moderate level of market concentration, with a few key players holding significant market share, alongside a growing number of niche providers. Technological innovation is a pivotal driver, with insurers increasingly leveraging data analytics, telematics, and artificial intelligence to refine underwriting, personalize pricing, and enhance customer experience. Regulatory frameworks, primarily overseen by the Financial Services Agency (FSA), emphasize consumer protection, solvency, and fair market practices, influencing product development and distribution strategies. Competitive product substitutes are present, including extended warranty programs and vehicle maintenance packages, though mandatory third-party liability coverage remains a cornerstone. End-user demographics are shifting, with an aging population and an increasing demand for digital-first insurance solutions. Mergers and Acquisitions (M&A) trends indicate a consolidation drive among established players seeking to gain economies of scale and expand their service portfolios.

- Market Concentration: Dominated by a few large insurers but with growing competition from insurtech startups.

- Technological Innovation: Telematics, AI-driven claims processing, and digital platforms are transforming the market.

- Regulatory Framework: Focus on consumer protection, data privacy, and financial stability.

- Competitive Substitutes: Extended warranties and service contracts offer alternative risk mitigation.

- End-User Demographics: Evolving preferences driven by an aging population and younger generations' digital fluency.

- M&A Trends: Strategic acquisitions aimed at expanding market reach and technological capabilities.

Japan Car Insurance Market Growth Trends & Insights

The Japan Car Insurance Market has demonstrated a steady upward trajectory, propelled by increasing vehicle ownership and a heightened awareness of the importance of financial protection against road-related risks. The market size evolution has been consistent, with a projected Compound Annual Growth Rate (CAGR) of approximately 3.5% during the forecast period. Adoption rates for comprehensive and optional coverage are steadily increasing as consumers become more aware of the benefits beyond basic liability. Technological disruptions are significantly impacting the industry, with the integration of IoT devices and AI facilitating the development of usage-based insurance (UBI) and pay-as-you-drive (PAYD) policies, leading to more personalized premiums and proactive risk management. Consumer behavior shifts are evident, with a growing preference for online channels for policy comparison, purchase, and claims management, driven by convenience and transparency. The market penetration for car insurance in Japan stands at an impressive 90%, indicating a mature but still evolving landscape.

The increasing sophistication of data analytics plays a crucial role in understanding consumer behavior and tailoring product offerings. Insurers are investing heavily in digital transformation to streamline operations and offer seamless customer journeys. The adoption of telematics data, for instance, allows for the assessment of driving habits, leading to more accurate risk profiling and potentially lower premiums for safe drivers. This data-driven approach not only enhances operational efficiency but also fosters greater customer engagement and loyalty. Furthermore, the evolving mobility landscape, including the rise of shared mobility services and autonomous driving technologies, presents both challenges and opportunities for insurers, necessitating adaptation of existing product lines and the development of new coverage solutions. The emphasis on preventative measures, facilitated by technology, is becoming a key differentiator for insurers.

Dominant Regions, Countries, or Segments in Japan Car Insurance Market

Within the Japan Car Insurance Market, Personal Vehicles represent the dominant application segment, accounting for an estimated 85% of the total market share. This dominance is driven by the high penetration of private car ownership across the country, particularly in urban and suburban areas. The primary coverage type driving market growth is Collision/Comprehensive/Other Optional Coverage, which has seen a significant surge in adoption rates as consumers increasingly seek robust protection against a wider range of risks, including theft, natural disasters, and accidental damage. This segment is expected to grow at a CAGR of 4.2% during the forecast period, outpacing the growth of third-party liability coverage.

The Online distribution channel is rapidly emerging as a key growth driver, fueled by increasing internet penetration and a growing preference among consumers for digital platforms for policy comparison, purchase, and management. This channel is projected to experience a CAGR of 6.1%, reflecting its disruptive potential.

Application Dominance:

- Personal Vehicles: The cornerstone of the market, driven by widespread private car ownership.

- Commercial Vehicles: A significant, though secondary, segment with steady growth influenced by logistics and business needs.

Coverage Dominance:

- Collision/Comprehensive/Other Optional Coverage: Experiencing robust growth due to enhanced consumer awareness and desire for holistic protection.

- Third-Party Liability Coverage: Remains a mandatory and foundational segment, ensuring basic financial protection.

Distribution Channel Dominance:

- Online: Rapidly gaining traction, offering convenience, transparency, and competitive pricing, becoming a preferred channel for a growing segment of the population.

- Insurance Agents: Still a vital channel, providing personalized advice and support, particularly for complex policy needs.

- Direct Sales: Insurers are increasingly investing in direct-to-consumer models, leveraging digital platforms and call centers.

The economic policies of the Japanese government, which encourage vehicle ownership and infrastructure development, further bolster the personal vehicles segment. The increasing sophistication of risk assessment tools allows insurers to offer more attractive comprehensive coverage options, appealing to a broader demographic. The convenience and competitive pricing offered through online platforms are reshaping consumer purchasing habits, pushing insurers to enhance their digital capabilities and user experience.

Japan Car Insurance Market Product Landscape

The product landscape of the Japan Car Insurance Market is characterized by innovation and customization. Insurers are actively developing and refining policies to meet evolving consumer needs and technological advancements. Key product innovations include usage-based insurance (UBI) leveraging telematics for personalized premiums based on driving behavior, and enhanced coverage for electric and hybrid vehicles. The integration of AI for faster claims processing and fraud detection is a significant performance metric being prioritized. Unique selling propositions often revolve around competitive pricing, extensive coverage options, and responsive customer service, with many providers offering bundled packages for greater value.

Key Drivers, Barriers & Challenges in Japan Car Insurance Market

Key Drivers:

- Increasing Vehicle Ownership: A steady rise in the number of registered vehicles fuels demand for insurance.

- Technological Advancements: Telematics and AI enable personalized pricing and improved risk management, attracting tech-savvy consumers.

- Enhanced Consumer Awareness: Greater understanding of the financial implications of accidents and vehicle damage drives demand for comprehensive coverage.

- Government Initiatives: Policies supporting road safety and vehicle registration indirectly boost the insurance market.

Barriers & Challenges:

- Intense Competition: A mature market with numerous players leads to price sensitivity and pressure on profit margins.

- Regulatory Compliance: Adhering to stringent regulations requires significant investment and operational adjustments.

- Aging Population: While a significant segment, an aging demographic may have different risk profiles and insurance preferences.

- Cybersecurity Threats: The increasing reliance on digital platforms exposes insurers to cyber risks and data breaches.

- Economic Slowdown: Potential economic downturns could impact disposable income and the affordability of insurance premiums.

Emerging Opportunities in Japan Car Insurance Market

Emerging opportunities in the Japan Car Insurance Market are abundant, driven by evolving consumer preferences and technological disruptions. The growing demand for sustainable mobility presents a significant avenue, with opportunities in specialized insurance for electric vehicles (EVs) and hybrid cars, including battery coverage and charging infrastructure protection. The expansion of usage-based insurance (UBI) and pay-as-you-drive (PAYD) models, leveraging telematics and IoT data, offers a chance to capture a younger, tech-oriented demographic seeking personalized and cost-effective solutions. Furthermore, the integration of AI and machine learning in claims management and customer service can create a competitive edge by offering faster, more efficient, and personalized experiences, fostering customer loyalty.

Growth Accelerators in the Japan Car Insurance Market Industry

Several catalysts are accelerating long-term growth in the Japan Car Insurance Market. Technological breakthroughs, particularly in telematics and artificial intelligence, are enabling insurers to offer more sophisticated and personalized products, such as usage-based insurance (UBI), which appeals to a broad segment of drivers. Strategic partnerships between traditional insurers and insurtech startups are fostering innovation and expanding distribution channels, bringing new digital-first solutions to the market. The increasing focus on preventative services, facilitated by connected car technology, allows insurers to move beyond traditional risk transfer to risk mitigation, creating new value propositions. Market expansion strategies, including the development of tailored policies for emerging mobility trends like shared services and autonomous vehicles, are also crucial growth drivers.

Key Players Shaping the Japan Car Insurance Market Market

- T&D Holdings

- Sony Assurance

- Tokio Marine & Nichido Fire Insurance

- Rakuten

- Sompo Japan Insurance

- Mitsui Sumitomo Insurance

- MS&AD Insurance Group Holdings

- Japan Post Insurance

- Aioi Nissay Dowa Insurance

- Chubb

Notable Milestones in Japan Car Insurance Market Sector

- December 2022: OCTO Telematics, a data analytics firm for the insurance sector, launched its Tokyo office, strengthening its presence and expanding partnerships with Japanese insurance providers, including a commercial partnership with Tokio Marine.

- January 2023: Tokio Marine & Nichido Fire Insurance initiated the sale of insurance products through the Metaverse, allowing virtual avatar interactions for offering car insurance.

In-Depth Japan Car Insurance Market Market Outlook

The Japan Car Insurance Market is poised for continued robust growth, driven by a confluence of technological advancements, evolving consumer behaviors, and strategic market initiatives. The increasing adoption of digital channels and personalized insurance solutions, such as usage-based insurance (UBI) enabled by telematics, will be key growth accelerators. Insurers are expected to deepen their investments in AI and data analytics to enhance underwriting accuracy, streamline claims processing, and deliver superior customer experiences. The growing demand for coverage tailored to emerging mobility trends, including electric vehicles and autonomous driving, presents significant untapped potential. Strategic collaborations between established players and agile insurtech firms will continue to foster innovation and expand market reach, ensuring the sector remains dynamic and responsive to the evolving needs of Japanese consumers.

Japan Car Insurance Market Segmentation

-

1. Coverage

- 1.1. Third-Party Liability Coverage

- 1.2. Collision/Comprehensive/Other Optional Coverage

-

2. Application

- 2.1. Personal Vehicles

- 2.2. Commercial Vehicles

-

3. Distribution Channel

- 3.1. Direct Sales

- 3.2. Insurance Agents

- 3.3. Brokers

- 3.4. Banks

- 3.5. Online

- 3.6. Other Distribution Channels

Japan Car Insurance Market Segmentation By Geography

- 1. Japan

Japan Car Insurance Market Regional Market Share

Geographic Coverage of Japan Car Insurance Market

Japan Car Insurance Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.21% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Coverage

- 5.1.1. Third-Party Liability Coverage

- 5.1.2. Collision/Comprehensive/Other Optional Coverage

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Personal Vehicles

- 5.2.2. Commercial Vehicles

- 5.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.3.1. Direct Sales

- 5.3.2. Insurance Agents

- 5.3.3. Brokers

- 5.3.4. Banks

- 5.3.5. Online

- 5.3.6. Other Distribution Channels

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Japan

- 5.1. Market Analysis, Insights and Forecast - by Coverage

- 6. Japan Car Insurance Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Coverage

- 6.1.1. Third-Party Liability Coverage

- 6.1.2. Collision/Comprehensive/Other Optional Coverage

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Personal Vehicles

- 6.2.2. Commercial Vehicles

- 6.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.3.1. Direct Sales

- 6.3.2. Insurance Agents

- 6.3.3. Brokers

- 6.3.4. Banks

- 6.3.5. Online

- 6.3.6. Other Distribution Channels

- 6.1. Market Analysis, Insights and Forecast - by Coverage

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 T&D Holdings

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Sony Assurance

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Tokio Marine & Nichido Fire Insurance

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Rakuten**List Not Exhaustive

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Sompo Japan Insurance

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Mitsui Sumitomo Insurance

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 MS&AD Insurance Group Holdings

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Japan Post Insurance

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Aioi Nissay Dowa Insurance

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Chubb

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 T&D Holdings

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Japan Car Insurance Market Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Japan Car Insurance Market Share (%) by Company 2025

List of Tables

- Table 1: Japan Car Insurance Market Revenue Million Forecast, by Coverage 2020 & 2033

- Table 2: Japan Car Insurance Market Revenue Million Forecast, by Application 2020 & 2033

- Table 3: Japan Car Insurance Market Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 4: Japan Car Insurance Market Revenue Million Forecast, by Region 2020 & 2033

- Table 5: Japan Car Insurance Market Revenue Million Forecast, by Coverage 2020 & 2033

- Table 6: Japan Car Insurance Market Revenue Million Forecast, by Application 2020 & 2033

- Table 7: Japan Car Insurance Market Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 8: Japan Car Insurance Market Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Japan Car Insurance Market?

The projected CAGR is approximately 5.21%.

2. Which companies are prominent players in the Japan Car Insurance Market?

Key companies in the market include T&D Holdings, Sony Assurance, Tokio Marine & Nichido Fire Insurance, Rakuten**List Not Exhaustive, Sompo Japan Insurance, Mitsui Sumitomo Insurance, MS&AD Insurance Group Holdings, Japan Post Insurance, Aioi Nissay Dowa Insurance, Chubb.

3. What are the main segments of the Japan Car Insurance Market?

The market segments include Coverage, Application, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 20.31 Million as of 2022.

5. What are some drivers contributing to market growth?

Rising Sales of Cars in the Japan; Decline in Car Insurance Premium Rates.

6. What are the notable trends driving market growth?

Rising Gross Written Premium with Declining Insurance Premium Rates.

7. Are there any restraints impacting market growth?

Lack of Awareness on Car Insurance Policies; Increase in False Insurance Claims and Scams.

8. Can you provide examples of recent developments in the market?

December 2022: OCTO Telematics, existing as a data analytics firm for the insurance sector, launched its office in Tokyo (Japan) to strengthen its presence and expand its partnership with insurance providers. The company has a commercial partnership with Tokio Marine which is having its operation in Japan car insurance.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Japan Car Insurance Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Japan Car Insurance Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Japan Car Insurance Market?

To stay informed about further developments, trends, and reports in the Japan Car Insurance Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence