Key Insights

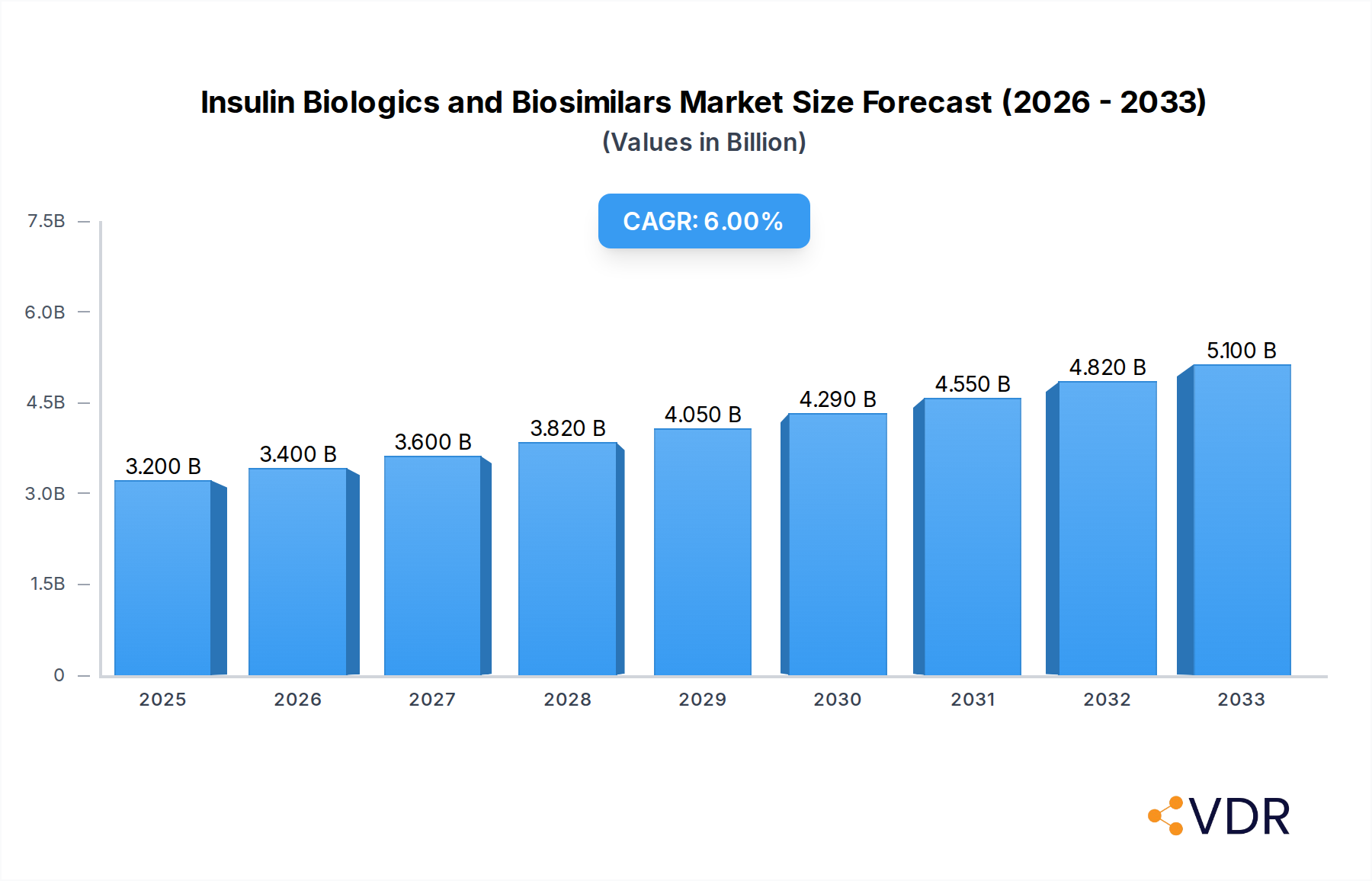

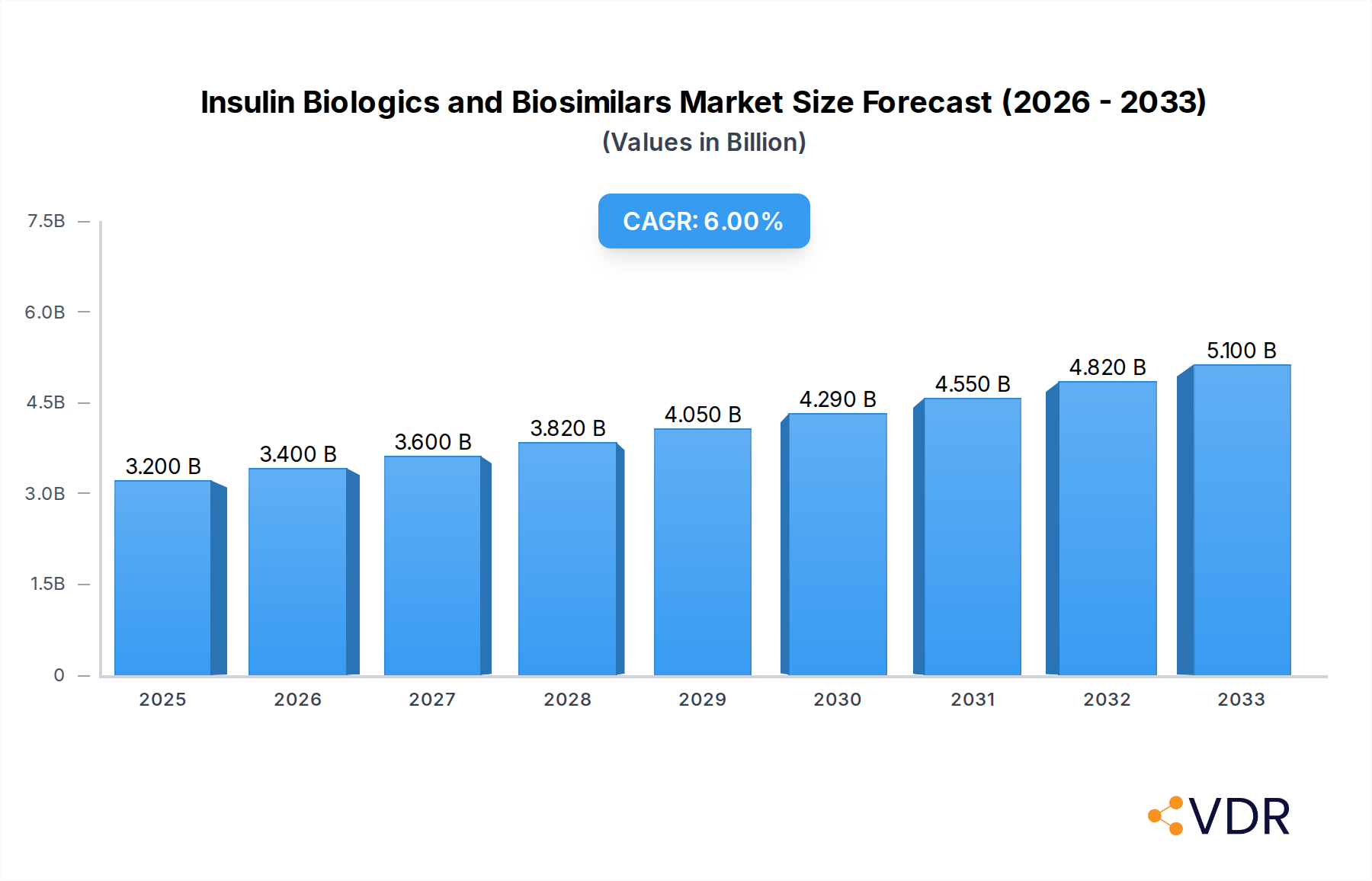

The global market for Insulin Biologics and Biosimilars is poised for significant expansion, projected to reach $3.2 billion in 2025 with a robust CAGR of 6.2% through 2033. This growth is fundamentally driven by the escalating prevalence of diabetes worldwide, a complex metabolic disorder necessitating consistent and effective insulin management. The increasing burden of diabetes, particularly Type 2, is a primary catalyst, pushing demand for both novel biologic insulins and their more affordable biosimilar alternatives. Furthermore, advancements in biopharmaceutical manufacturing technologies have enhanced the efficacy and safety profiles of these treatments, making them more accessible and appealing to a broader patient demographic. The growing awareness among healthcare providers and patients regarding the therapeutic benefits and cost-effectiveness of biosimilars, in particular, is a key trend that is reshaping the market landscape, encouraging greater adoption and contributing to market expansion.

Insulin Biologics and Biosimilars Market Size (In Billion)

The market is experiencing a dynamic evolution driven by several key trends, including a shift towards personalized medicine and the development of advanced insulin formulations. The rise of biosimilars is a dominant force, offering substantial cost savings and improving access to essential diabetes care, especially in emerging economies. Innovations in delivery devices, such as smart insulin pens and continuous glucose monitoring systems, are also augmenting the growth trajectory by improving patient convenience and adherence. However, the market faces certain restraints, including stringent regulatory pathways for biosimilar approval, which can prolong time-to-market and increase development costs. Additionally, the high initial investment required for the research and development of novel biologics, coupled with ongoing price pressures from payers and governments seeking to control healthcare expenditures, presents ongoing challenges. Despite these hurdles, the market is projected to witness sustained growth as the global demand for effective diabetes management solutions continues to rise.

Insulin Biologics and Biosimilars Company Market Share

Unlock critical insights into the dynamic global insulin biologics and biosimilars market. This in-depth report, spanning from 2019 to 2033 with a base year of 2025, provides a detailed examination of market structure, growth trajectories, regional dominance, product innovations, key players, and emerging opportunities. Discover the forces shaping the future of diabetes management and insulin therapy, with quantitative data and expert analysis for strategic decision-making.

Insulin Biologics and Biosimilars Market Dynamics & Structure

The global insulin biologics and biosimilars market is characterized by a moderate to high concentration, with a few key players dominating the landscape. Technological innovation remains a primary driver, fueled by ongoing research and development in novel insulin formulations and delivery systems, alongside the increasing sophistication of biosimilar manufacturing. Regulatory frameworks, while stringent, are evolving to facilitate biosimilar approval, fostering greater competition. Competitive product substitutes include other therapeutic classes for diabetes management, though insulin remains foundational for many patients. End-user demographics are expanding due to the rising global prevalence of diabetes, driven by aging populations and lifestyle changes. Mergers and acquisitions (M&A) are a significant trend, with larger pharmaceutical companies acquiring biosimilar developers to bolster their portfolios and expand market reach.

- Market Concentration: Dominated by major insulin manufacturers and an increasing number of biosimilar developers.

- Technological Innovation: Focus on long-acting insulins, rapid-acting insulins, and advanced delivery devices.

- Regulatory Frameworks: Evolving pathways for biosimilar approval in key markets such as the US and EU.

- Competitive Product Substitutes: Oral antidiabetics, GLP-1 receptor agonists, and other novel diabetes therapies.

- End-User Demographics: Growing patient pool due to rising diabetes incidence and prevalence.

- M&A Trends: Strategic acquisitions and partnerships to gain market access and diversify product offerings.

Insulin Biologics and Biosimilars Growth Trends & Insights

The global insulin biologics and biosimilars market is poised for robust growth, driven by the escalating global burden of diabetes and advancements in therapeutic options. Market size is projected to expand significantly, from an estimated XXX billion units in the historical period to XXX billion units by 2033, exhibiting a compelling Compound Annual Growth Rate (CAGR) of approximately XX%. Adoption rates of both biologics and biosimilars are on an upward trajectory, propelled by increasing physician familiarity, enhanced clinical evidence, and growing payer acceptance of biosimilar cost-effectiveness. Technological disruptions are continuously reshaping the market, with the development of more sophisticated insulin analogs, smart insulin pens, and closed-loop insulin delivery systems enhancing patient convenience and glycemic control. Consumer behavior shifts are also evident, with patients seeking more personalized and convenient treatment regimens, favoring innovative delivery methods and accessible biosimilar options. Market penetration is expected to deepen across both developed and emerging economies as healthcare infrastructure improves and the demand for affordable yet effective diabetes management solutions intensifies. The penetration of biosimilars, in particular, is a key growth driver, offering substantial cost savings without compromising therapeutic efficacy, thereby broadening access to essential insulin therapies.

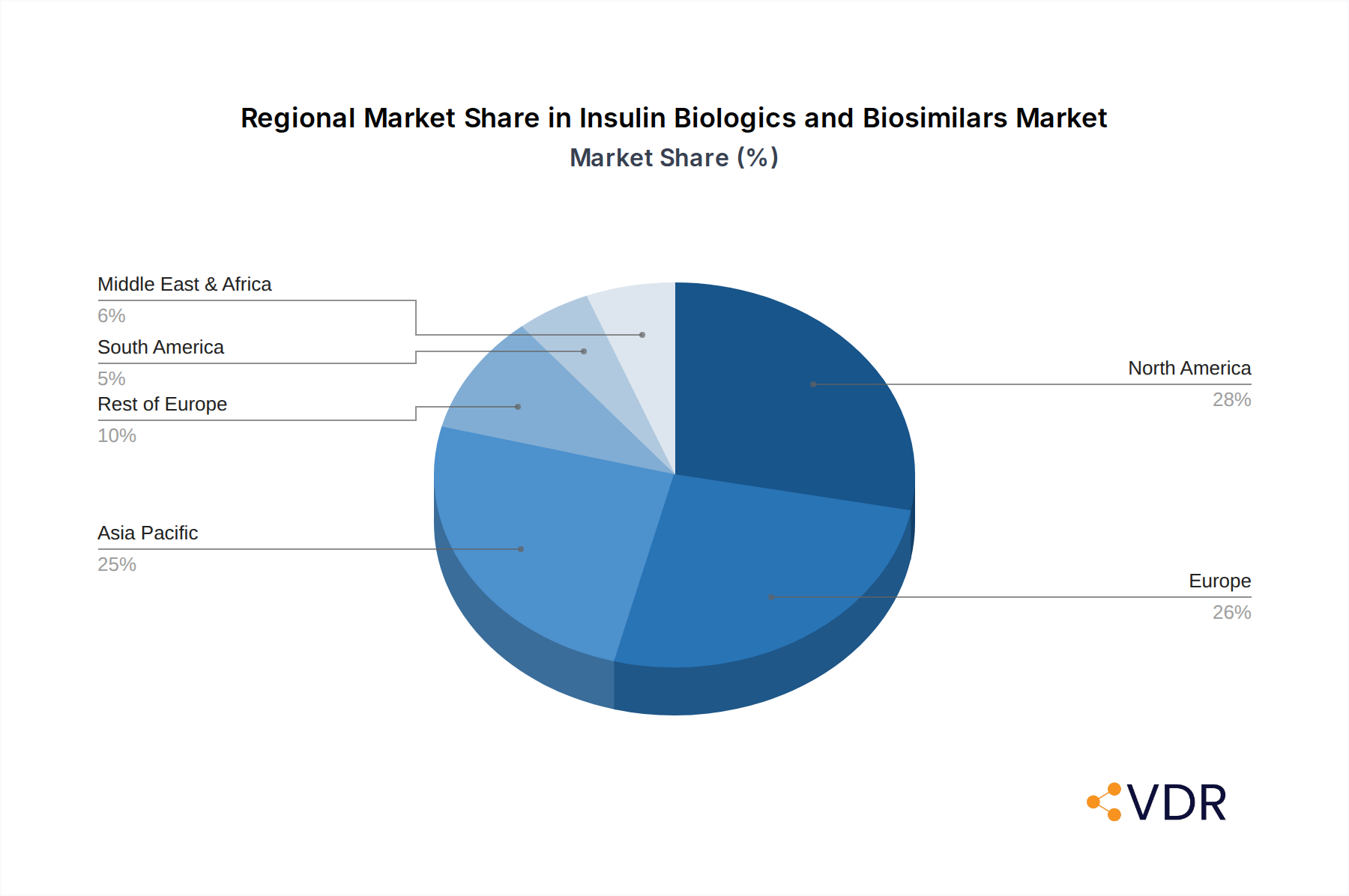

Dominant Regions, Countries, or Segments in Insulin Biologics and Biosimilars

The Hospital application segment is a significant driver of growth within the insulin biologics and biosimilars market, commanding a substantial market share. This dominance is attributed to the critical role hospitals play in the initial diagnosis, initiation of treatment, and management of complex diabetes cases, including acute diabetic emergencies. Hospitals are primary consumers of both branded insulin biologics for critical care and a growing volume of insulin biosimilars, reflecting their cost-effectiveness in inpatient settings. The increasing prevalence of diabetes and its complications necessitates extensive hospitalizations, further bolstering demand.

- Application: Hospital: Leading segment due to inpatient diabetes management, critical care, and initial treatment initiation. High volume of both biologics and biosimilars utilized.

- Key Drivers for Hospital Dominance:

- Rising Diabetes Prevalence and Complications: Increased hospital admissions for diabetes-related issues.

- Cost-Effectiveness of Biosimilars: Hospitals leverage biosimilars to manage budgets and improve access for a larger patient population.

- Specialized Diabetes Care Units: Dedicated facilities within hospitals that drive demand for a wide range of insulin products.

- Government and Payer Initiatives: Policies encouraging the use of cost-effective treatments in institutional settings.

- Market Share & Growth Potential: Hospitals represent a substantial portion of the insulin market, with continued growth projected due to ongoing healthcare reforms and the persistent need for diabetes management.

The Insulin Biologics type segment currently holds a larger market share compared to insulin biosimilars, driven by established brand loyalty, extensive clinical data, and physician familiarity. However, the Insulin Biosimilars segment is experiencing rapid growth due to increasing regulatory approvals, expanding product portfolios, and a strong emphasis on cost reduction in healthcare systems globally. As more biosimilar insulin products enter the market and gain traction, their market share is expected to rise considerably, leading to a more competitive landscape.

- Types: Insulin Biologics & Insulin Biosimilars:

- Insulin Biologics: Continue to hold a significant share due to established brands and long-standing clinical use.

- Insulin Biosimilars: Experiencing rapid growth, driven by cost advantages and increasing market penetration.

- Growth Potential for Biosimilars: Significant as patent cliffs approach for blockbuster biologic insulins, opening doors for biosimilar competition and wider patient access.

Leading Countries: The United States and European countries, particularly Germany and the United Kingdom, are key regions driving market growth. The high prevalence of diabetes, advanced healthcare infrastructure, favorable regulatory pathways for biosimilars, and the presence of major pharmaceutical and biosimilar companies contribute to their dominance. Emerging markets such as China and India are also showing significant growth potential due to their large populations and increasing awareness and diagnosis of diabetes.

Insulin Biologics and Biosimilars Product Landscape

The insulin biologics and biosimilars market is rich with innovative products designed to improve glycemic control and patient convenience. This includes a spectrum of rapid-acting insulins (e.g., insulin lispro, insulin aspart), short-acting insulins (e.g., regular human insulin), intermediate-acting insulins (e.g., NPH insulin), and long-acting insulins (e.g., insulin glargine, insulin detemir, insulin degludec). The development of fixed-ratio combination insulins offers simplified dosing regimens. Furthermore, advancements in delivery devices, such as pre-filled pens and smart insulin pens that track dosage and timing, enhance adherence and treatment efficacy. Biosimilar insulins are becoming increasingly prevalent, mirroring the efficacy and safety profiles of their originator counterparts, thereby offering more affordable treatment options.

Key Drivers, Barriers & Challenges in Insulin Biologics and Biosimilars

Key Drivers: The primary forces propelling the insulin biologics and biosimilars market include the escalating global prevalence of diabetes, driven by aging populations and lifestyle factors, leading to a consistent and growing demand for insulin therapies. Technological advancements in insulin formulations and delivery systems enhance efficacy and patient convenience, encouraging adoption. The introduction and increasing acceptance of biosimilar insulins are critical drivers, offering significant cost savings and expanding access to treatment, particularly in resource-limited settings. Supportive regulatory pathways for biosimilars in major markets facilitate market entry and competition.

Key Barriers & Challenges: Despite the growth drivers, the market faces several challenges. High research and development costs associated with novel insulin biologics and the intricate manufacturing processes for biosimilars represent significant financial barriers. Stringent regulatory approval processes, though evolving, can still be lengthy and complex, delaying market entry. Intense competition from both established biologic manufacturers and a growing number of biosimilar players can lead to pricing pressures. Physician and patient education regarding the efficacy and safety of biosimilar insulins is crucial to overcome any lingering skepticism and drive widespread adoption. Supply chain complexities, ensuring consistent availability and quality of these life-saving medications globally, also pose a challenge.

Emerging Opportunities in Insulin Biologics and Biosimilars

Emerging opportunities in the insulin biologics and biosimilars market lie in expanding access to advanced insulin therapies in underserved emerging economies where the prevalence of diabetes is rapidly rising. The development of novel insulin formulations with even longer durations of action or improved pharmacokinetic profiles presents a significant opportunity for differentiation. Furthermore, the integration of insulin therapy with digital health solutions, such as continuous glucose monitoring (CGM) systems and smart insulin pens, offers a compelling avenue for enhancing patient engagement and treatment outcomes. Innovations in delivery devices, including needle-free injection systems, could address patient preferences and improve adherence.

Growth Accelerators in the Insulin Biologics and Biosimilars Industry

Key growth accelerators in the insulin biologics and biosimilars industry include the relentless progression of scientific research leading to the development of next-generation insulins with enhanced patient benefits. Strategic partnerships and collaborations between originator biologic companies and biosimilar developers, as well as between pharmaceutical firms and technology companies, are crucial for market expansion and innovation. Furthermore, aggressive market expansion strategies by key players into high-growth emerging markets, coupled with favorable government policies promoting the adoption of biosimilars and cost-effective diabetes management, are significant catalysts for sustained growth.

Key Players Shaping the Insulin Biologics and Biosimilars Market

- Novo Nordisk

- Eli Lilly

- Sanofi

- Gan&Lee

- Tonghua Dongbao

- United Laboratory

- Geropharm

- Biocon

- Wockhardt

Notable Milestones in Insulin Biologics and Biosimilars Sector

- 2019-2024: Numerous regulatory approvals for insulin biosimilars in major markets like the US and EU, increasing market competition.

- 2020: Significant advancements in smart insulin pen technology, enhancing patient monitoring and data collection.

- 2021: Expansion of clinical trials for novel insulin formulations demonstrating improved efficacy and patient-reported outcomes.

- 2022: Key acquisitions and mergers of biosimilar companies by larger pharmaceutical players to strengthen their diabetes portfolios.

- 2023: Increased focus on digital health integration for diabetes management, including insulin therapy.

- 2024: Launch of several new long-acting insulin biosimilars, offering more affordable alternatives to originator biologics.

In-Depth Insulin Biologics and Biosimilars Market Outlook

The outlook for the insulin biologics and biosimilars market remains exceptionally positive, driven by a confluence of factors that are poised to accelerate growth. The increasing global diabetes epidemic ensures a persistent and expanding demand for effective insulin therapies. The ongoing advancements in biosimilar development and regulatory approvals will continue to drive down costs, significantly enhancing accessibility for millions worldwide. Strategic investments in research and development for innovative insulin formulations and cutting-edge delivery systems will further fuel market expansion and patient satisfaction. Companies that can effectively navigate the evolving regulatory landscapes, forge strategic alliances, and focus on patient-centric solutions will be well-positioned to capitalize on the immense growth potential within this vital therapeutic area.

Insulin Biologics and Biosimilars Segmentation

-

1. Application

- 1.1. Hospital

- 1.2. Retail Pharmacy

- 1.3. Other

-

2. Types

- 2.1. Insulin Biologics

- 2.2. Insulin Biosimilars

Insulin Biologics and Biosimilars Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Insulin Biologics and Biosimilars Regional Market Share

Geographic Coverage of Insulin Biologics and Biosimilars

Insulin Biologics and Biosimilars REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Insulin Biologics and Biosimilars Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Hospital

- 5.1.2. Retail Pharmacy

- 5.1.3. Other

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Insulin Biologics

- 5.2.2. Insulin Biosimilars

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Insulin Biologics and Biosimilars Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Hospital

- 6.1.2. Retail Pharmacy

- 6.1.3. Other

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Insulin Biologics

- 6.2.2. Insulin Biosimilars

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Insulin Biologics and Biosimilars Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Hospital

- 7.1.2. Retail Pharmacy

- 7.1.3. Other

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Insulin Biologics

- 7.2.2. Insulin Biosimilars

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Insulin Biologics and Biosimilars Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Hospital

- 8.1.2. Retail Pharmacy

- 8.1.3. Other

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Insulin Biologics

- 8.2.2. Insulin Biosimilars

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Insulin Biologics and Biosimilars Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Hospital

- 9.1.2. Retail Pharmacy

- 9.1.3. Other

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Insulin Biologics

- 9.2.2. Insulin Biosimilars

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Insulin Biologics and Biosimilars Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Hospital

- 10.1.2. Retail Pharmacy

- 10.1.3. Other

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Insulin Biologics

- 10.2.2. Insulin Biosimilars

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Novo Nordisk

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Eli Lilly

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Sanofi

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Gan&Lee

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Tonghua Dongbao

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 United Laboratory

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Geropharm

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Biocon

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Wockhardt

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.1 Novo Nordisk

List of Figures

- Figure 1: Global Insulin Biologics and Biosimilars Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Insulin Biologics and Biosimilars Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Insulin Biologics and Biosimilars Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Insulin Biologics and Biosimilars Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Insulin Biologics and Biosimilars Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Insulin Biologics and Biosimilars Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Insulin Biologics and Biosimilars Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Insulin Biologics and Biosimilars Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Insulin Biologics and Biosimilars Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Insulin Biologics and Biosimilars Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Insulin Biologics and Biosimilars Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Insulin Biologics and Biosimilars Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Insulin Biologics and Biosimilars Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Insulin Biologics and Biosimilars Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Insulin Biologics and Biosimilars Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Insulin Biologics and Biosimilars Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Insulin Biologics and Biosimilars Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Insulin Biologics and Biosimilars Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Insulin Biologics and Biosimilars Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Insulin Biologics and Biosimilars Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Insulin Biologics and Biosimilars Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Insulin Biologics and Biosimilars Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Insulin Biologics and Biosimilars Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Insulin Biologics and Biosimilars Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Insulin Biologics and Biosimilars Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Insulin Biologics and Biosimilars Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Insulin Biologics and Biosimilars Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Insulin Biologics and Biosimilars Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Insulin Biologics and Biosimilars Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Insulin Biologics and Biosimilars Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Insulin Biologics and Biosimilars Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Insulin Biologics and Biosimilars Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Insulin Biologics and Biosimilars Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Insulin Biologics and Biosimilars Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Insulin Biologics and Biosimilars Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Insulin Biologics and Biosimilars Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Insulin Biologics and Biosimilars Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Insulin Biologics and Biosimilars Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Insulin Biologics and Biosimilars Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Insulin Biologics and Biosimilars Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Insulin Biologics and Biosimilars Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Insulin Biologics and Biosimilars Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Insulin Biologics and Biosimilars Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Insulin Biologics and Biosimilars Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Insulin Biologics and Biosimilars Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Insulin Biologics and Biosimilars Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Insulin Biologics and Biosimilars Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Insulin Biologics and Biosimilars Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Insulin Biologics and Biosimilars Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Insulin Biologics and Biosimilars Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Insulin Biologics and Biosimilars Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Insulin Biologics and Biosimilars Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Insulin Biologics and Biosimilars Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Insulin Biologics and Biosimilars Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Insulin Biologics and Biosimilars Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Insulin Biologics and Biosimilars Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Insulin Biologics and Biosimilars Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Insulin Biologics and Biosimilars Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Insulin Biologics and Biosimilars Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Insulin Biologics and Biosimilars Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Insulin Biologics and Biosimilars Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Insulin Biologics and Biosimilars Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Insulin Biologics and Biosimilars Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Insulin Biologics and Biosimilars Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Insulin Biologics and Biosimilars Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Insulin Biologics and Biosimilars Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Insulin Biologics and Biosimilars Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Insulin Biologics and Biosimilars Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Insulin Biologics and Biosimilars Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Insulin Biologics and Biosimilars Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Insulin Biologics and Biosimilars Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Insulin Biologics and Biosimilars Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Insulin Biologics and Biosimilars Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Insulin Biologics and Biosimilars Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Insulin Biologics and Biosimilars Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Insulin Biologics and Biosimilars Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Insulin Biologics and Biosimilars Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Insulin Biologics and Biosimilars?

The projected CAGR is approximately 6.2%.

2. Which companies are prominent players in the Insulin Biologics and Biosimilars?

Key companies in the market include Novo Nordisk, Eli Lilly, Sanofi, Gan&Lee, Tonghua Dongbao, United Laboratory, Geropharm, Biocon, Wockhardt.

3. What are the main segments of the Insulin Biologics and Biosimilars?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 3.2 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3350.00, USD 5025.00, and USD 6700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Insulin Biologics and Biosimilars," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Insulin Biologics and Biosimilars report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Insulin Biologics and Biosimilars?

To stay informed about further developments, trends, and reports in the Insulin Biologics and Biosimilars, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence