Key Insights

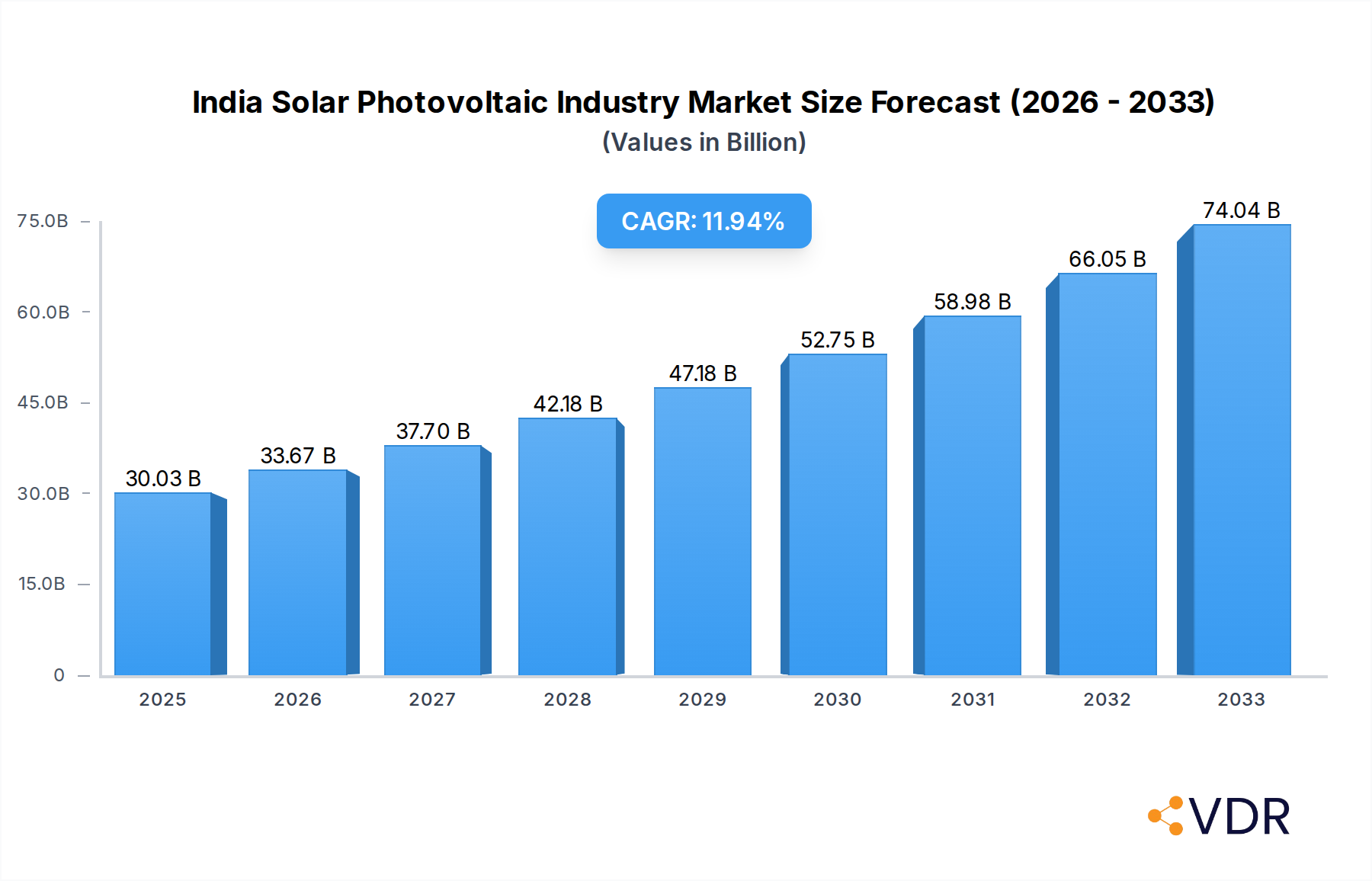

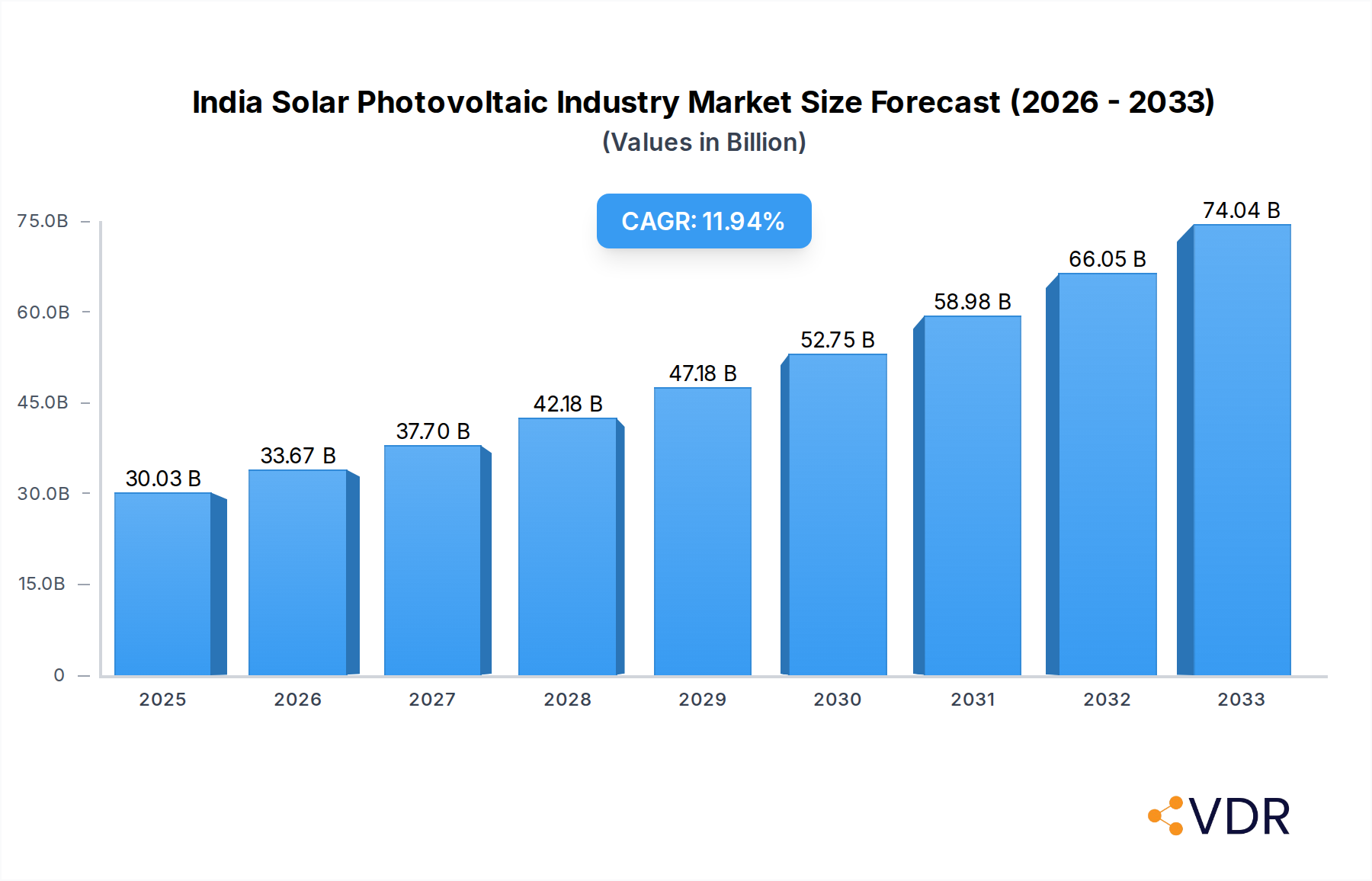

The India Solar Photovoltaic (PV) Industry is poised for remarkable growth, driven by strong government support, declining technology costs, and an increasing focus on renewable energy adoption. The market size is projected to reach USD 30,032.78 million in 2025, with a compelling Compound Annual Growth Rate (CAGR) of 13.1% from 2025 to 2033. This robust expansion is fueled by an increasing demand for clean energy solutions across residential, commercial, and industrial (C&I) sectors, as well as large-scale utility projects. Key drivers include ambitious renewable energy targets, favorable policies such as Production Linked Incentive (PLI) schemes, and significant investments in solar power infrastructure. The industry is witnessing a surge in both domestic and foreign player participation, indicating a competitive and dynamic market landscape. Innovations in thin-film and crystalline silicon technologies are further enhancing efficiency and reducing costs, making solar PV a more accessible and attractive energy source for a wider demographic.

India Solar Photovoltaic Industry Market Size (In Billion)

The market's trajectory is further shaped by evolving trends like the increasing adoption of rooftop solar installations, coupled with the development of large-scale ground-mounted solar farms. While challenges such as land acquisition complexities, grid integration issues, and raw material price volatility exist, they are being addressed through policy interventions and technological advancements. The competitive environment, featuring prominent players like Adani Group, Hanwha Q CELLS, Vikram Solar, Trina Solar, First Solar, and Tata Power Solar, is fostering innovation and efficiency. The strategic focus on expanding manufacturing capabilities within India, coupled with the growing awareness and demand for sustainable energy, are expected to propel the India Solar PV Industry to new heights, solidifying its position as a global leader in solar energy deployment and manufacturing.

India Solar Photovoltaic Industry Company Market Share

India Solar Photovoltaic Industry Report: Comprehensive Market Analysis and Future Outlook (2019-2033)

This in-depth report provides a comprehensive analysis of the India Solar Photovoltaic (PV) Industry, a rapidly expanding sector crucial for India's energy transition. Covering the study period of 2019–2033, with a base year of 2025 and a forecast period from 2025–2033, this report offers invaluable insights for stakeholders, investors, and policymakers. It delves into market dynamics, growth trends, regional dominance, product landscape, key players, and emerging opportunities, all presented with quantitative data and expert analysis. This report is essential for understanding the Indian solar power market, renewable energy in India, and the growth of solar PV technology in the region. We present all monetary values in million units.

India Solar Photovoltaic Industry Market Dynamics & Structure

The India Solar Photovoltaic Industry is characterized by dynamic market concentration and an accelerating pace of technological innovation. While a few large conglomerates like Adani Group and Hanwha Q CELLS Co Ltd hold significant market share, the presence of numerous domestic and foreign players fosters a competitive environment. Regulatory frameworks, driven by government initiatives such as the National Solar Mission and Production Linked Incentive (PLI) schemes, are pivotal in shaping investment and deployment. The competitive landscape is further influenced by the evolution of product substitutes, though solar PV's cost-effectiveness and environmental benefits provide a strong moat. End-user demographics are diversifying, with a notable surge in demand from the Residential, Commercial and Industrial (C&I), and Utility segments. Mergers and acquisitions (M&A) are a growing trend, indicating industry consolidation and strategic expansion.

- Market Concentration: Dominated by key players but with increasing participation from mid-sized and smaller companies.

- Technological Innovation Drivers: Focus on increasing efficiency, reducing costs of Crystalline Silicon and Thin Film technologies, and enhancing grid integration solutions.

- Regulatory Frameworks: Government incentives, supportive policies for rooftop solar and utility-scale projects, and evolving net-metering regulations are crucial.

- Competitive Product Substitutes: While alternatives exist, solar PV's declining cost and increasing efficiency make it a preferred renewable energy source.

- End-User Demographics: Growing demand from Residential rooftops, substantial growth in C&I sector adoption for cost savings and sustainability, and large-scale utility projects.

- M&A Trends: Strategic acquisitions to gain market share, access new technologies, and secure project pipelines.

India Solar Photovoltaic Industry Growth Trends & Insights

The India Solar Photovoltaic Industry is poised for unprecedented growth, driven by a confluence of factors including supportive government policies, declining technology costs, and an increasing awareness of environmental sustainability. The market size evolution has been remarkable, with significant increases in installed capacity year-on-year. Adoption rates, particularly in the Utility and Commercial and Industrial (C&I) segments, are accelerating due to favorable economics and corporate sustainability goals. Technological disruptions are continually enhancing the efficiency and reducing the cost of solar panels, making them more competitive against traditional energy sources. Consumer behavior shifts towards embracing cleaner energy solutions, fueled by rising electricity prices and a desire for energy independence, are also contributing to the industry's upward trajectory. The CAGR for the forecast period is projected to be robust, indicating sustained expansion and a significant increase in market penetration across all segments.

The historical period (2019-2024) has witnessed a steady increase in solar installations, laying the groundwork for future acceleration. The base year of 2025 serves as a critical benchmark, reflecting a maturing market with established players and a growing understanding of the challenges and opportunities. Moving into the forecast period (2025–2033), the industry is expected to witness a CAGR of XX%, driven by ambitious renewable energy targets and increased private sector investment. Market penetration, currently at XX% of the total energy mix, is projected to reach XX% by 2033, underscoring the transformative impact of solar PV on India's energy landscape. The adoption of advanced solar PV technology and innovative deployment strategies, such as floating solar parks and hybrid projects, will further fuel this expansion.

Dominant Regions, Countries, or Segments in India Solar Photovoltaic Industry

The dominance in the India Solar Photovoltaic Industry is multifaceted, with specific regions and segments emerging as key growth engines. Rajasthan consistently leads in terms of installed solar capacity, driven by its vast arid land availability and favorable solar irradiation. Other states like Gujarat, Tamil Nadu, and Karnataka also exhibit significant growth, supported by state-level renewable energy policies and incentives.

Among the segments, the Utility scale segment commands the largest market share, driven by large-scale solar park developments and government tenders aiming to meet national power demands. However, the Commercial and Industrial (C&I) segment is experiencing rapid expansion as businesses increasingly adopt solar power to reduce operational costs and meet sustainability targets. The Residential segment, while smaller in terms of individual installations, is crucial for distributed generation and energy independence, with growth fueled by attractive subsidies and declining panel costs.

- Leading Region: Rajasthan, due to its geographical advantage and supportive policies.

- Dominant Segment: Utility-scale projects are currently the largest contributor to installed capacity.

- High Growth Segment: Commercial and Industrial (C&I) sector is showing accelerated adoption due to economic and environmental benefits.

- Key Drivers:

- Economic Policies: Favorable tariffs, tax incentives, and PLI schemes driving investment in solar manufacturing and deployment.

- Infrastructure Development: Expansion of transmission infrastructure to evacuate power from solar-rich regions.

- Government Targets: Ambitious renewable energy targets set by the Indian government.

- Technological Advancements: Improved efficiency and reduced cost of solar panels making them economically viable.

- Market Share & Growth Potential: Utility segment holds XX% of the market share and is expected to grow at a CAGR of XX%. C&I segment, with XX% market share, is projected to grow at an even higher CAGR of XX% due to increasing corporate focus on ESG.

India Solar Photovoltaic Industry Product Landscape

The product landscape of the India Solar Photovoltaic Industry is characterized by continuous innovation focused on enhancing efficiency, durability, and cost-effectiveness. Crystalline Silicon technology, including monocrystalline and polycrystalline panels, remains the dominant choice due to its established reliability and performance. However, Thin Film technologies, such as Cadmium Telluride (CdTe) and CIGS, are gaining traction, especially for flexible and lightweight applications. Product innovations include bifacial solar panels that capture sunlight from both sides, increasing energy generation by up to 20%, and solar modules with enhanced low-light performance and superior temperature coefficients. Advancements in manufacturing processes are leading to higher power output per module and improved longevity, with warranties extending to 25-30 years.

Key Drivers, Barriers & Challenges in India Solar Photovoltaic Industry

Key Drivers: The primary forces propelling the India Solar Photovoltaic Industry include government mandates and incentives aimed at achieving renewable energy targets, a significant reduction in solar module costs due to technological advancements and economies of scale, and increasing corporate and individual demand for sustainable energy solutions. The declining levelized cost of electricity (LCOE) for solar power makes it highly competitive with fossil fuels. Technological breakthroughs in panel efficiency and storage solutions are also key accelerators.

Barriers & Challenges: Significant challenges remain, including land acquisition hurdles for large-scale projects and grid integration complexities as solar penetration increases. Supply chain vulnerabilities, particularly reliance on imported components, pose a risk. Policy inconsistencies and delays in approvals can impact project timelines. Competition from other renewable energy sources and the intermittency of solar power requiring robust energy storage solutions are also critical factors to address.

Emerging Opportunities in India Solar Photovoltaic Industry

Emerging opportunities in the India Solar Photovoltaic Industry are diverse and promising. The burgeoning demand for energy storage solutions, particularly Battery Energy Storage Systems (BESS), presents a significant avenue for growth, complementing the intermittent nature of solar power. The development of floating solar farms on reservoirs and water bodies offers a novel approach to land utilization. Furthermore, the integration of solar PV with electric vehicles (EVs) and smart grids, along with the expansion of offshore solar installations, are nascent but hold substantial future potential. The Residential and Commercial and Industrial (C&I) segments continue to offer untapped potential for distributed generation and microgrids.

Growth Accelerators in the India Solar Photovoltaic Industry Industry

Several key catalysts are driving the long-term growth of the India Solar Photovoltaic Industry. Technological breakthroughs in perovskite solar cells and tandem solar cells promise higher efficiencies at potentially lower costs. Strategic partnerships between domestic manufacturers and international technology providers are crucial for indigenous development and scaling. Market expansion strategies, including the development of solar-plus-storage projects and the increasing adoption of solar in off-grid applications in rural areas, are vital growth accelerators. The policy focus on manufacturing within India, through schemes like the PLI, will further bolster domestic production capabilities and reduce import dependency.

Key Players Shaping the India Solar Photovoltaic Industry Market

- Adani Group

- Hanwha Q CELLS Co Ltd

- Vikram Solar Limited

- EMMVEE SOLAR

- Trina Solar Limited

- Sterling And Wilson Pvt Ltd

- Tata Power Solar Systems Ltd

- Mahindra Susten Pvt Ltd

- First Solar Inc

- ABB

- ACME Solar

- Azure Power Global Limited

- SMA Solar Technology AG

Notable Milestones in India Solar Photovoltaic Industry Sector

- January 2022: SJVN (Satluj Jal Vidyut Nigam Ltd.) bagged a solar project of 125MW in Uttar Pradesh, through a bidding process held by Uttar Pradesh New and Renewable Energy Development Agency (UPNEDA). This included a 75MW grid-connected solar PV project in Jalaun and a 50MW solar project in Kanpur Dehat districts, significantly boosting the Utility segment's capacity.

- December 2021: Tata Power clinched the largest solar plus battery project in India from Solar Energy Corporation of India. The contract includes a 100MW EPC solar project and a 120MWh utility-scale Battery Energy Storage System. The total project outlay was around INR 945 crores, marking a pivotal moment in integrating solar PV with energy storage.

In-Depth India Solar Photovoltaic Industry Market Outlook

The India Solar Photovoltaic Industry market outlook is exceptionally positive, driven by sustained government commitment, robust investment inflows, and rapid technological advancements. Growth accelerators such as increasing utility-scale project pipelines, a surge in rooftop solar installations in the Residential and Commercial and Industrial (C&I) sectors, and the burgeoning adoption of energy storage solutions will define the industry's trajectory. Strategic opportunities lie in further developing domestic manufacturing capabilities, fostering innovation in advanced solar technologies, and expanding into emerging applications like agri-voltaics and solar for industrial process heat. The industry is on track to play a pivotal role in India's quest for energy security and carbon neutrality.

India Solar Photovoltaic Industry Segmentation

-

1. Type

- 1.1. Thin film

- 1.2. Crystalline Silicon

-

2. End-User

- 2.1. Residential

- 2.2. Commercial and Indudstrial (C&I)

- 2.3. Utility

-

3. Deployment

- 3.1. Ground-mounted

- 3.2. Rooftop-Solar

India Solar Photovoltaic Industry Segmentation By Geography

- 1. India

India Solar Photovoltaic Industry Regional Market Share

Geographic Coverage of India Solar Photovoltaic Industry

India Solar Photovoltaic Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 13.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Thin film

- 5.1.2. Crystalline Silicon

- 5.2. Market Analysis, Insights and Forecast - by End-User

- 5.2.1. Residential

- 5.2.2. Commercial and Indudstrial (C&I)

- 5.2.3. Utility

- 5.3. Market Analysis, Insights and Forecast - by Deployment

- 5.3.1. Ground-mounted

- 5.3.2. Rooftop-Solar

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. India

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. India Solar Photovoltaic Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Thin film

- 6.1.2. Crystalline Silicon

- 6.2. Market Analysis, Insights and Forecast - by End-User

- 6.2.1. Residential

- 6.2.2. Commercial and Indudstrial (C&I)

- 6.2.3. Utility

- 6.3. Market Analysis, Insights and Forecast - by Deployment

- 6.3.1. Ground-mounted

- 6.3.2. Rooftop-Solar

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 2 Adani Group

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 3 Hanwha Q CELLS Co Ltd

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 8 Vikram Solar Limited

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 4 EMMVEE SOLAR

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 5 Trina Solar Limited*List Not Exhaustive

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Domestic Players

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 6 Sterling And Wilson Pvt Ltd

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 7 Tata Power Solar Systems Ltd

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 5 Mahindra Susten Pvt Ltd

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Foreign Players

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 2 First Solar Inc

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 1 ABB

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 1 ACME Solar

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.14 3 Azure Power Global Limited

- 7.1.14.1. Company Overview

- 7.1.14.2. Products

- 7.1.14.3. Company Financials

- 7.1.14.4. SWOT Analysis

- 7.1.15 4 SMA Solar Technology AG

- 7.1.15.1. Company Overview

- 7.1.15.2. Products

- 7.1.15.3. Company Financials

- 7.1.15.4. SWOT Analysis

- 7.1.1 2 Adani Group

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: India Solar Photovoltaic Industry Revenue Breakdown (million, %) by Product 2025 & 2033

- Figure 2: India Solar Photovoltaic Industry Share (%) by Company 2025

List of Tables

- Table 1: India Solar Photovoltaic Industry Revenue million Forecast, by Type 2020 & 2033

- Table 2: India Solar Photovoltaic Industry Revenue million Forecast, by End-User 2020 & 2033

- Table 3: India Solar Photovoltaic Industry Revenue million Forecast, by Deployment 2020 & 2033

- Table 4: India Solar Photovoltaic Industry Revenue million Forecast, by Region 2020 & 2033

- Table 5: India Solar Photovoltaic Industry Revenue million Forecast, by Type 2020 & 2033

- Table 6: India Solar Photovoltaic Industry Revenue million Forecast, by End-User 2020 & 2033

- Table 7: India Solar Photovoltaic Industry Revenue million Forecast, by Deployment 2020 & 2033

- Table 8: India Solar Photovoltaic Industry Revenue million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the India Solar Photovoltaic Industry?

The projected CAGR is approximately 13.1%.

2. Which companies are prominent players in the India Solar Photovoltaic Industry?

Key companies in the market include 2 Adani Group, 3 Hanwha Q CELLS Co Ltd, 8 Vikram Solar Limited, 4 EMMVEE SOLAR, 5 Trina Solar Limited*List Not Exhaustive, Domestic Players, 6 Sterling And Wilson Pvt Ltd, 7 Tata Power Solar Systems Ltd, 5 Mahindra Susten Pvt Ltd, Foreign Players, 2 First Solar Inc, 1 ABB, 1 ACME Solar, 3 Azure Power Global Limited, 4 SMA Solar Technology AG.

3. What are the main segments of the India Solar Photovoltaic Industry?

The market segments include Type, End-User, Deployment.

4. Can you provide details about the market size?

The market size is estimated to be USD 30032.78 million as of 2022.

5. What are some drivers contributing to market growth?

4.; Supportive Government Policies for Developing Solar Energy4.; Declining Cost of Solar Power Technology.

6. What are the notable trends driving market growth?

Rooftop Solar PV Segment Expected to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; Unpredictability in the Continuity of Power Supply.

8. Can you provide examples of recent developments in the market?

In January 2022, SJVN (Satluj Jal Vidyut Nigam Ltd.) bagged a solar project of 125MW in Uttar Pradesh, through a bidding process held by Uttar Pradesh New and Renewable Energy Development Agency (UPNEDA). It includes a 75MW grid-connected solar PV project in Jalaun and a 50MW solar project in Kanpur Dehat districts.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "India Solar Photovoltaic Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the India Solar Photovoltaic Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the India Solar Photovoltaic Industry?

To stay informed about further developments, trends, and reports in the India Solar Photovoltaic Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence