Key Insights

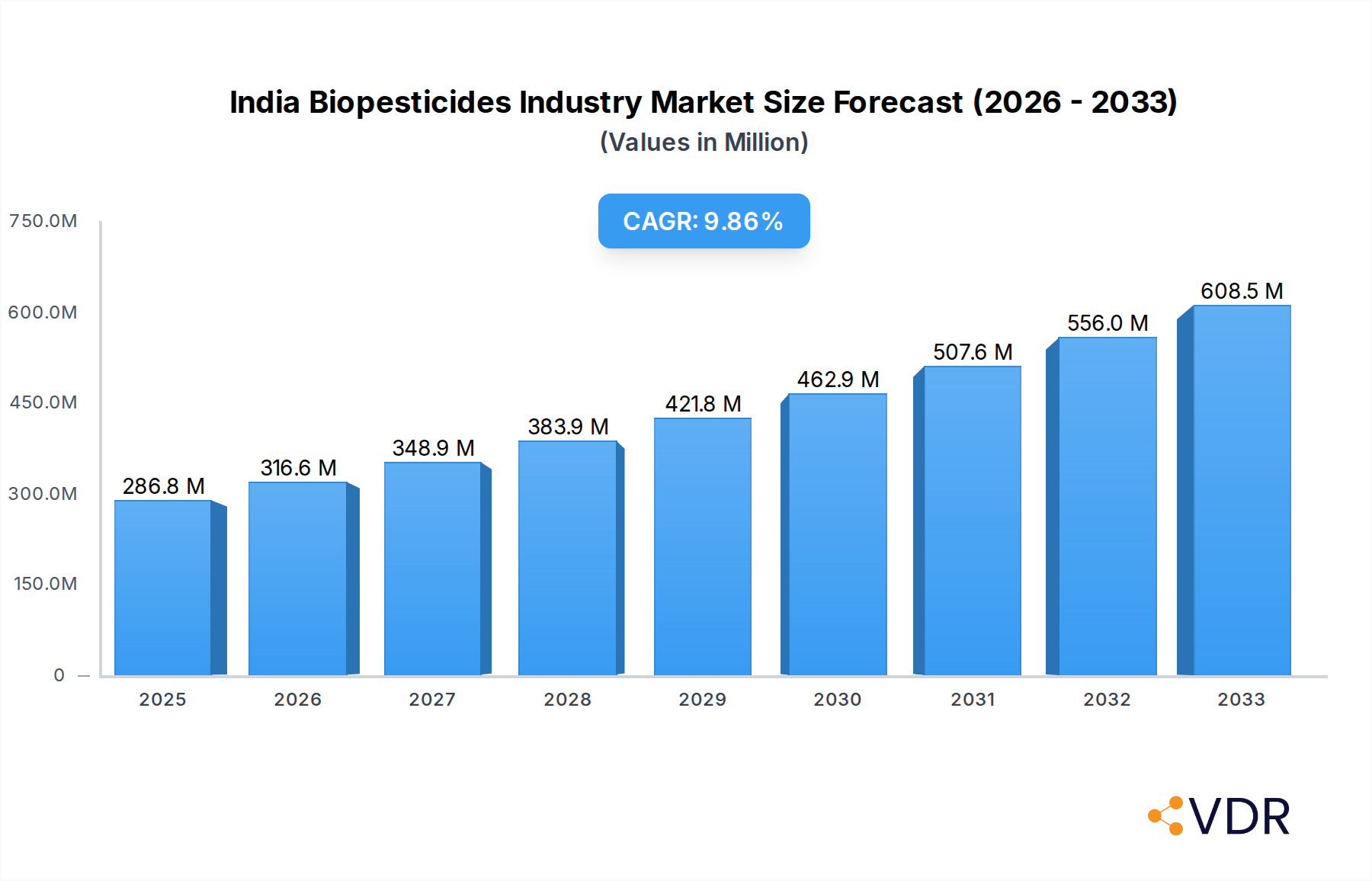

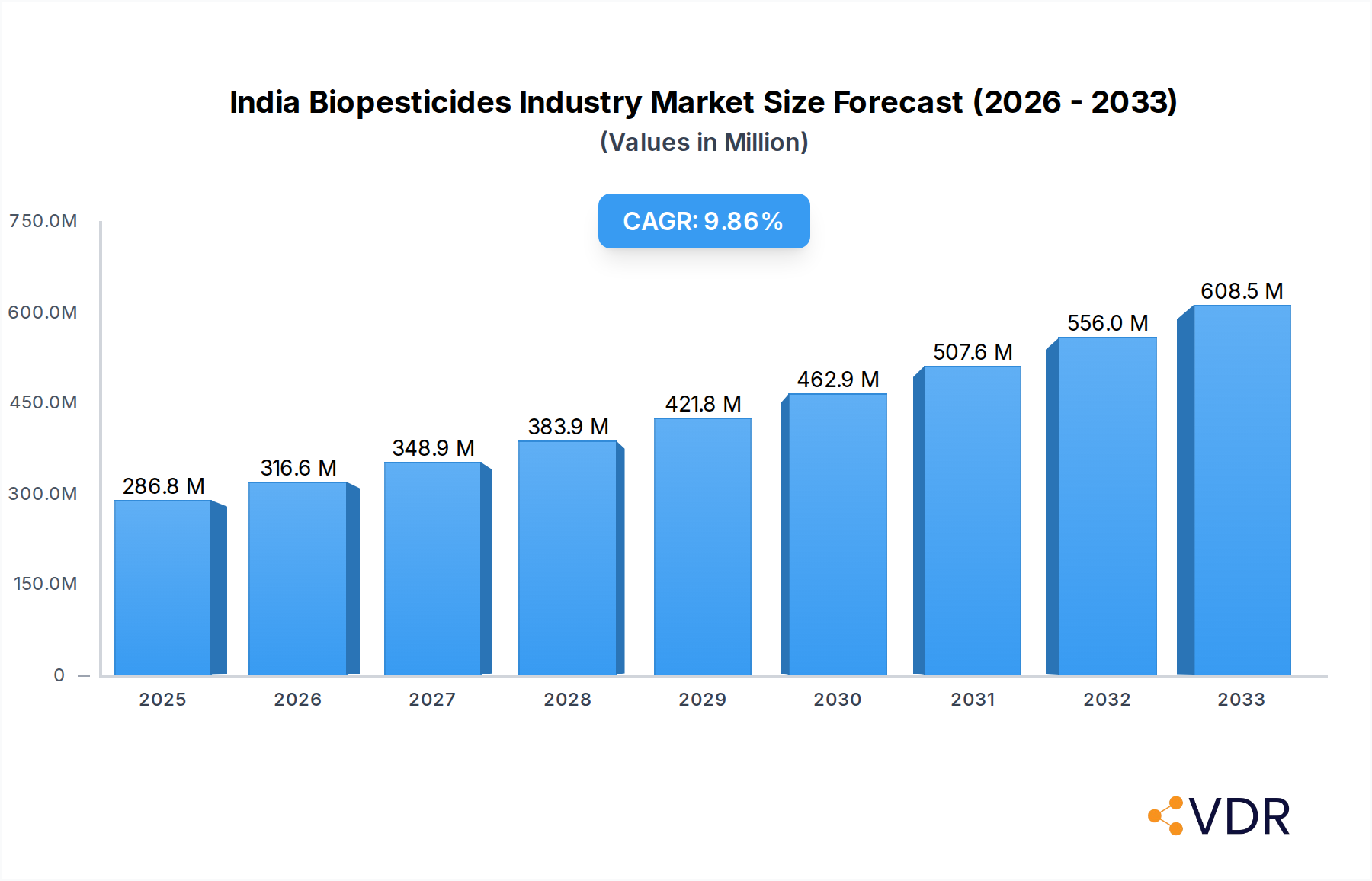

The Indian biopesticides market is poised for substantial growth, driven by a growing demand for sustainable agriculture, increasing government support for organic farming, and rising farmer awareness regarding the detrimental effects of chemical pesticides. With a projected market size of USD 286.8 million in 2025, the industry is anticipated to witness a robust CAGR of 10.49% during the forecast period of 2025-2033. This expansion is fueled by several key factors. The increasing prevalence of pest resistance to conventional chemicals necessitates the adoption of alternative solutions, with biopesticides emerging as a viable and environmentally friendly option. Furthermore, favorable policies and subsidies promoting the use of biological inputs by the Indian government are significantly boosting market penetration. Consumer preference for organically grown produce, driven by health consciousness and concerns about pesticide residues, is also a major catalyst, compelling farmers to integrate biopesticides into their crop protection strategies. The market's trajectory reflects a broader shift towards eco-friendly agricultural practices, aligning with global sustainability goals.

India Biopesticides Industry Market Size (In Million)

The Indian biopesticides market exhibits a dynamic landscape characterized by significant growth opportunities across various segments, including production, consumption, imports, and exports. Production is expected to scale up to meet the escalating domestic demand, supported by advancements in microbial and botanical pesticide technologies. Consumption patterns are evolving as farmers increasingly recognize the efficacy and safety benefits of biopesticides, leading to their wider adoption across diverse crop types. While imports may play a role in introducing novel formulations, the focus is increasingly shifting towards domestic manufacturing and R&D to cater to specific Indian agricultural needs. Price trends are likely to stabilize as production volumes increase and economies of scale are achieved, making biopesticides more accessible to a wider farmer base. Key players in the market are investing in research and development, expanding their product portfolios, and strengthening their distribution networks to capture a larger market share. The growth of companies like Coromandel International Ltd, Gujarat State Fertilizers & Chemicals Ltd, and IPL Biologicals Limited underscores the market's potential and competitive intensity.

India Biopesticides Industry Company Market Share

Unveiling the India Biopesticides Industry: A Comprehensive Market Analysis (2019–2033)

This in-depth report provides an exhaustive analysis of the India Biopesticides Industry, offering critical insights into market dynamics, growth trends, competitive landscape, and future opportunities. Covering a study period from 2019 to 2033, with a base and estimated year of 2025, this report is an indispensable resource for stakeholders seeking to understand and capitalize on the burgeoning biopesticides market in India. Leverage advanced analytical frameworks and precise data to navigate production, consumption, import/export markets, and price trends in millions of units.

India Biopesticides Industry Market Dynamics & Structure

The Indian biopesticides industry is characterized by a moderately concentrated market, driven by increasing awareness of sustainable agriculture, stringent regulations on chemical pesticides, and a growing demand for organic produce. Technological innovation remains a key driver, with ongoing research and development focused on microbial and botanical biopesticides offering enhanced efficacy and broader application. The regulatory framework, spearheaded by bodies like the Central Insecticides Board and Registration Committee (CIBRC), is progressively becoming more supportive of biopesticide registration and adoption, although the process can still be lengthy. Competitive product substitutes include a wide array of conventional chemical pesticides, which, despite environmental concerns, often offer immediate cost advantages and established distribution networks. End-user demographics are shifting, with a growing segment of progressive farmers, organic food producers, and even large-scale agricultural corporations actively seeking eco-friendly pest management solutions. Mergers and acquisitions (M&A) are becoming increasingly prevalent as companies seek to consolidate their market position, expand their product portfolios, and gain access to new technologies and distribution channels. For instance, the approved merger between Liberty Pesticides and Fertilizers Limited (LPFL) and Coromandel SQM (India) Private Limited (CSQM) in April 2022 is expected to bolster Coromandel International Ltd.'s biopesticides offerings.

- Market Concentration: Moderately concentrated, with a few key players holding significant market share, but an increasing number of smaller players and startups entering the market.

- Technological Innovation Drivers: Development of novel microbial strains, botanical extracts, and formulation technologies; emphasis on targeted pest control and improved shelf-life.

- Regulatory Frameworks: Evolving support from CIBRC, with streamlined registration processes and incentives for biopesticide development and promotion.

- Competitive Product Substitutes: Conventional chemical pesticides, integrated pest management (IPM) strategies, and other biological control agents.

- End-User Demographics: Small and marginal farmers, large agricultural enterprises, organic farmers, horticulture sector, and export-oriented producers.

- M&A Trends: Increasing consolidation to enhance market reach, diversify product offerings, and acquire advanced technologies. Expected M&A deal volumes in the biopesticides segment are projected to rise by 15% over the forecast period.

India Biopesticides Industry Growth Trends & Insights

The India Biopesticides Industry is poised for exceptional growth, driven by a confluence of favorable factors that are reshaping agricultural practices across the nation. The market size is projected to expand at a robust Compound Annual Growth Rate (CAGR) of approximately 12.5% from 2025 to 2033, reaching a significant market value of over $500 million by the end of the forecast period. This impressive growth trajectory is underpinned by a discernible shift in adoption rates of biopesticides, moving from niche applications to mainstream agricultural solutions. Farmers, increasingly educated about the long-term benefits of biological pest management, including improved soil health, reduced environmental impact, and enhanced crop quality, are actively integrating biopesticides into their crop protection strategies. Technological disruptions are continuously enhancing the efficacy and accessibility of biopesticides. Advances in fermentation technology, strain selection, and formulation techniques are leading to more potent and stable biopesticide products. Furthermore, the development of precision application technologies ensures that biopesticides are delivered effectively, maximizing their impact and minimizing wastage. Consumer behavior shifts are also playing a pivotal role. A rising demand for organic and residue-free produce, fueled by growing health consciousness and a preference for sustainably sourced food, is compelling both farmers and food manufacturers to prioritize biopesticide usage. This consumer-led demand creates a positive feedback loop, encouraging further investment and innovation within the biopesticides sector. The increasing penetration of biopesticides in key crop segments, such as fruits, vegetables, and pulses, signifies a maturing market ready for substantial expansion. The projected market penetration of biopesticides in the overall Indian pesticide market is expected to rise from 5% in 2025 to over 12% by 2033, indicating a significant transformation in pest management practices.

Dominant Regions, Countries, or Segments in India Biopesticides Industry

The Indian biopesticides industry exhibits a dynamic regional and segmental dominance, with North India emerging as a leading region in terms of both production and consumption of biopesticides. This dominance is propelled by several key drivers including favorable economic policies, a robust agricultural infrastructure, and a high concentration of progressive farming communities actively embracing sustainable practices. States like Punjab, Haryana, and Uttar Pradesh are at the forefront, benefiting from government initiatives promoting organic farming and offering subsidies for biopesticide procurement.

Within this region, the Fruits and Vegetables segment is a major driver of market growth, owing to the high demand for residue-free produce and the vulnerability of these crops to a wide range of pests. The Production Analysis in North India reflects this demand, with a significant volume of biopesticides being manufactured to cater to local and national needs. Companies like GrowTech Agri Science Private Limited and Samriddhi Crops India Pvt Ltd have established strong production bases in this region.

The Consumption Analysis also points to North India's leading position. Farmers in this region are increasingly aware of the environmental and health benefits associated with biopesticides, leading to higher adoption rates. The Import Market Analysis (Value & Volume), while showing a growing trend across India, is significantly influenced by the demand from major agricultural hubs. The Export Market Analysis (Value & Volume), though still in its nascent stages, is also gaining traction from this region, as Indian companies begin to explore international markets for their biopesticide products.

The Price Trend Analysis indicates a gradual stabilization and a potential decrease in prices as production scales up and competition intensifies, making biopesticides more accessible to a wider range of farmers. The growth potential in North India is substantial, driven by continuous government support, farmer education programs, and the increasing profitability of organic farming practices. The market share of North India in the overall biopesticides market is estimated to be around 35% in 2025, with a projected CAGR of 13% for the forecast period.

India Biopesticides Industry Product Landscape

The product landscape of the Indian biopesticides industry is rapidly evolving, showcasing a diverse array of microbial, botanical, and biochemical formulations. Microbial biopesticides, particularly those based on Bacillus thuringiensis (Bt), Trichoderma, and various entomopathogenic fungi, dominate due to their targeted action and broad-spectrum efficacy against common agricultural pests and diseases. Botanical biopesticides, derived from plants like neem and pyrethrum, are gaining traction for their dual action of pest repulsion and control, alongside their environmentally benign profiles. Innovations are focused on enhancing the shelf-life and stability of these biological agents through advanced encapsulation and formulation technologies, making them more user-friendly and cost-effective for farmers. The performance metrics are increasingly impressive, with studies demonstrating efficacy comparable to synthetic pesticides in many applications, coupled with significant benefits to soil health and biodiversity.

Key Drivers, Barriers & Challenges in India Biopesticides Industry

Key Drivers:

- Growing Demand for Organic and Residue-Free Produce: Heightened consumer awareness regarding health and environmental safety is a primary catalyst for biopesticide adoption.

- Supportive Government Policies and Initiatives: The Indian government's emphasis on promoting sustainable agriculture, coupled with financial incentives and subsidies, significantly boosts the market.

- Increasing Awareness of Environmental Concerns: The detrimental effects of chemical pesticides on ecosystems and human health are driving a paradigm shift towards eco-friendly alternatives.

- Technological Advancements: Continuous innovation in R&D, leading to improved efficacy, stability, and application methods of biopesticides.

- Expanding Biopesticide Product Portfolio: A wider range of targeted and effective biopesticides for various crops and pests.

Barriers & Challenges:

- Perceived High Cost and Slow Action: Compared to conventional pesticides, biopesticides can sometimes be perceived as more expensive and slower in their action, leading to farmer hesitancy.

- Limited Shelf-Life and Storage Requirements: Many biopesticides have a shorter shelf-life and require specific storage conditions, posing logistical challenges.

- Complex Registration and Regulatory Hurdles: While improving, the registration process for new biopesticides can still be lengthy and complex, delaying market entry.

- Lack of Farmer Awareness and Education: Insufficient knowledge and training among a segment of farmers regarding the effective use and benefits of biopesticides.

- Supply Chain and Distribution Network Gaps: Inadequate infrastructure for the widespread and timely distribution of biopesticides, particularly in remote agricultural areas. The estimated impact of supply chain issues on market growth is a 5% reduction in potential sales annually.

Emerging Opportunities in India Biopesticides Industry

Emerging opportunities within the Indian biopesticides industry lie in the untapped potential of niche crop segments and the development of innovative, multi-functional biological agents. The increasing focus on protected cultivation, including greenhouses and polyhouses, presents a significant opportunity for specialized biopesticides tailored for controlled environments. Furthermore, the development of bio-insecticides and bio-fungicides with enhanced bio-stimulant properties, offering dual benefits of pest control and crop growth enhancement, is a key area for growth. Evolving consumer preferences for sustainably produced medicinal plants and aromatic crops also open avenues for targeted biopesticide solutions. The expansion of e-commerce platforms and digital advisory services for farmers can also bridge information gaps and facilitate access to biopesticide products.

Growth Accelerators in the India Biopesticides Industry Industry

Several catalysts are accelerating the growth of the Indian biopesticides industry. Technological breakthroughs in strain isolation, genetic engineering for enhanced efficacy, and advanced formulation techniques are creating more potent and reliable products. Strategic partnerships between research institutions, biopesticide manufacturers, and agricultural universities are fostering innovation and knowledge dissemination. Market expansion strategies, including targeted farmer education programs, field demonstrations, and collaborations with farmer producer organizations (FPOs), are crucial in driving adoption. The increasing integration of biopesticides into existing Integrated Pest Management (IPM) programs, supported by government advisories, is also a significant growth accelerator, solidifying their role in modern agricultural practices.

Key Players Shaping the India Biopesticides Industry Market

- GrowTech Agri Science Private Limited

- T Stanes and Company Limited

- Coromandel International Ltd

- Gujarat State Fertilizers & Chemicals Ltd

- Samriddhi Crops India Pvt Ltd

- Jaipur Bio Fertilizers

- IPL Biologicals Limited

- Andermatt Group AG

- Volkschem Crop Science Private Limite

- Central Biotech Private Limited

Notable Milestones in India Biopesticides Industry Sector

- April 2022: Coromandel International Ltd. approved the merger between Liberty Pesticides and Fertilizers Limited (LPFL) and Coromandel SQM (India) Private Limited (CSQM). This merger, effective April 01, 2021, is anticipated to expand the company's product portfolio, including its biopesticides, in the long run, strengthening its market presence.

- January 2022: Andermatt Group AG announced the merger of Andermatt Biocontrol AG with Andermatt Group AG. This consolidation aimed to increase management effectiveness and simplify the company's structure, allowing all companies to report directly to Andermatt Group AG, potentially streamlining R&D and market strategies for biopesticides.

In-Depth India Biopesticides Industry Market Outlook

The future outlook for the India Biopesticides Industry is exceptionally bright, characterized by sustained high growth driven by a deepening commitment to sustainable agriculture. The market is projected to witness a significant expansion, fueled by robust government support, increasing farmer adoption, and continuous technological innovation. Strategic opportunities lie in exploring novel biological control agents for emerging pests, expanding the application of biopesticides in neglected crop segments, and developing integrated bio-solutions that combine pest management with crop nutrition. The increasing global demand for organic produce will further propel India's export potential in the biopesticides sector. Companies that focus on research and development, effective market penetration strategies, and building strong farmer trust will be best positioned to capitalize on this dynamic and rapidly evolving market.

India Biopesticides Industry Segmentation

- 1. Production Analysis

- 2. Consumption Analysis

- 3. Import Market Analysis (Value & Volume)

- 4. Export Market Analysis (Value & Volume)

- 5. Price Trend Analysis

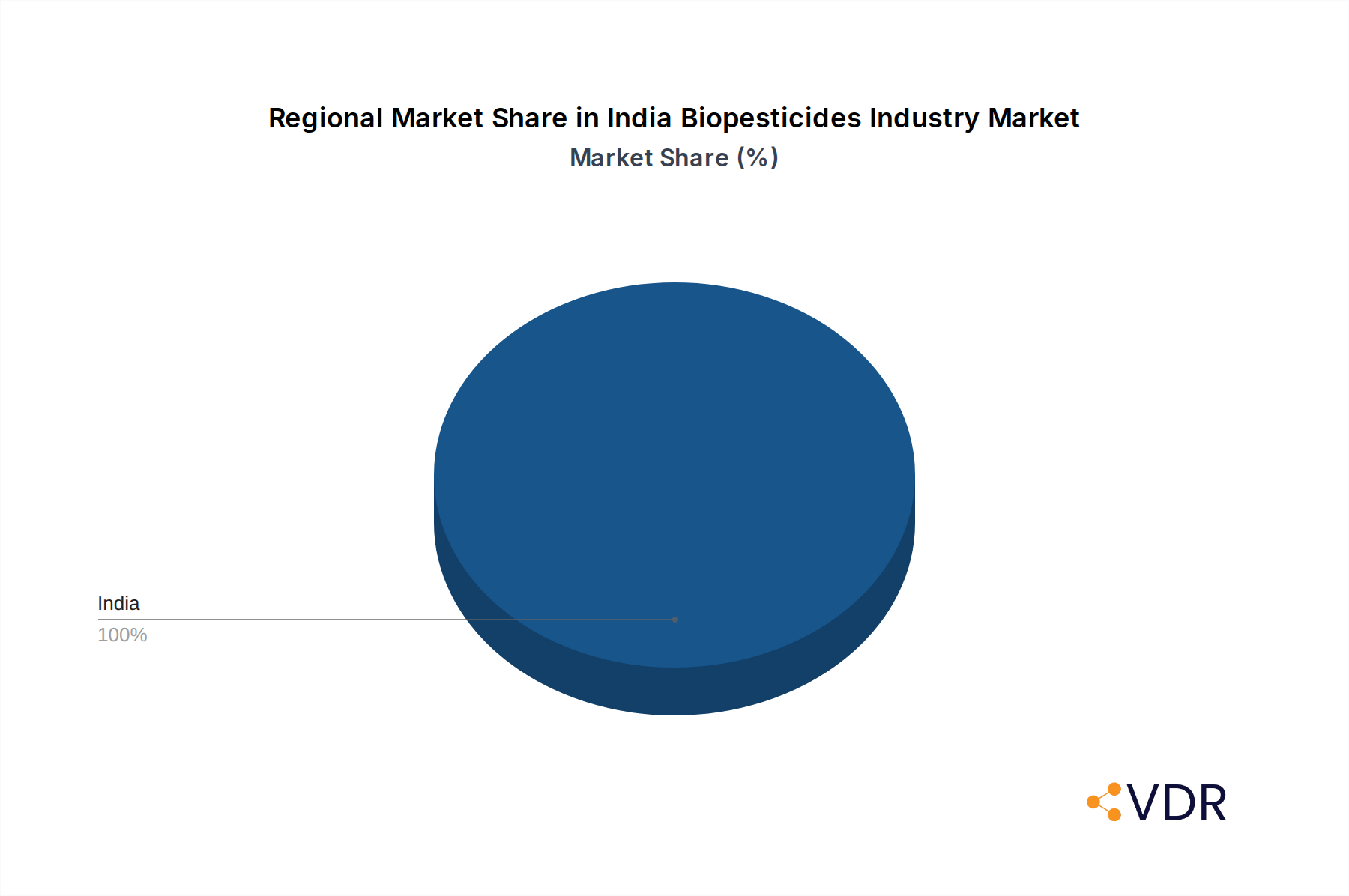

India Biopesticides Industry Segmentation By Geography

- 1. India

India Biopesticides Industry Regional Market Share

Geographic Coverage of India Biopesticides Industry

India Biopesticides Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 10.49% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Production Analysis

- 5.2. Market Analysis, Insights and Forecast - by Consumption Analysis

- 5.3. Market Analysis, Insights and Forecast - by Import Market Analysis (Value & Volume)

- 5.4. Market Analysis, Insights and Forecast - by Export Market Analysis (Value & Volume)

- 5.5. Market Analysis, Insights and Forecast - by Price Trend Analysis

- 5.6. Market Analysis, Insights and Forecast - by Region

- 5.6.1. India

- 6. India Biopesticides Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Production Analysis

- 6.2. Market Analysis, Insights and Forecast - by Consumption Analysis

- 6.3. Market Analysis, Insights and Forecast - by Import Market Analysis (Value & Volume)

- 6.4. Market Analysis, Insights and Forecast - by Export Market Analysis (Value & Volume)

- 6.5. Market Analysis, Insights and Forecast - by Price Trend Analysis

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 GrowTech Agri Science Private Limited

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 T Stanes and Company Limited

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Coromandel International Ltd

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Gujarat State Fertilizers & Chemicals Ltd

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Samriddhi Crops India Pvt Ltd

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Jaipur Bio Fertilizers

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 IPL Biologicals Limited

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Andermatt Group AG

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Volkschem Crop Science Private Limite

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Central Biotech Private Limited

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 GrowTech Agri Science Private Limited

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: India Biopesticides Industry Revenue Breakdown (million, %) by Product 2025 & 2033

- Figure 2: India Biopesticides Industry Share (%) by Company 2025

List of Tables

- Table 1: India Biopesticides Industry Revenue million Forecast, by Production Analysis 2020 & 2033

- Table 2: India Biopesticides Industry Revenue million Forecast, by Consumption Analysis 2020 & 2033

- Table 3: India Biopesticides Industry Revenue million Forecast, by Import Market Analysis (Value & Volume) 2020 & 2033

- Table 4: India Biopesticides Industry Revenue million Forecast, by Export Market Analysis (Value & Volume) 2020 & 2033

- Table 5: India Biopesticides Industry Revenue million Forecast, by Price Trend Analysis 2020 & 2033

- Table 6: India Biopesticides Industry Revenue million Forecast, by Region 2020 & 2033

- Table 7: India Biopesticides Industry Revenue million Forecast, by Production Analysis 2020 & 2033

- Table 8: India Biopesticides Industry Revenue million Forecast, by Consumption Analysis 2020 & 2033

- Table 9: India Biopesticides Industry Revenue million Forecast, by Import Market Analysis (Value & Volume) 2020 & 2033

- Table 10: India Biopesticides Industry Revenue million Forecast, by Export Market Analysis (Value & Volume) 2020 & 2033

- Table 11: India Biopesticides Industry Revenue million Forecast, by Price Trend Analysis 2020 & 2033

- Table 12: India Biopesticides Industry Revenue million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the India Biopesticides Industry?

The projected CAGR is approximately 10.49%.

2. Which companies are prominent players in the India Biopesticides Industry?

Key companies in the market include GrowTech Agri Science Private Limited, T Stanes and Company Limited, Coromandel International Ltd, Gujarat State Fertilizers & Chemicals Ltd, Samriddhi Crops India Pvt Ltd, Jaipur Bio Fertilizers, IPL Biologicals Limited, Andermatt Group AG, Volkschem Crop Science Private Limite, Central Biotech Private Limited.

3. What are the main segments of the India Biopesticides Industry?

The market segments include Production Analysis, Consumption Analysis, Import Market Analysis (Value & Volume), Export Market Analysis (Value & Volume), Price Trend Analysis.

4. Can you provide details about the market size?

The market size is estimated to be USD 286.8 million as of 2022.

5. What are some drivers contributing to market growth?

Seed Treatment As A Solution To Enhance Yield; Growing Awareness For Seed Treatment Among The Farmers; Rising Trend Of Organic Farming.

6. What are the notable trends driving market growth?

Row Crops is the largest Crop Type.

7. Are there any restraints impacting market growth?

Limitations Across Farm-Level Seed Treatment; Rising Environmental Concerns.

8. Can you provide examples of recent developments in the market?

April 2022: The company approved the merger between Liberty Pesticides and Fertilizers Limited (LPFL) and Coromandel SQM (India) Private Limited (CSQM) (wholly-owned subsidiaries), which came into effect on April 01, 2021. This merger is anticipated to expand the company's product portfolio, including its biopesticides, in the long run.January 2022: The company announced the merger of Andermatt Biocontrol AG with Andermatt Group AG. After the merger, all companies report directly to Andermatt Group AG, increasing the effectiveness of the management and simplifying the company's structure.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "India Biopesticides Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the India Biopesticides Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the India Biopesticides Industry?

To stay informed about further developments, trends, and reports in the India Biopesticides Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence