Key Insights

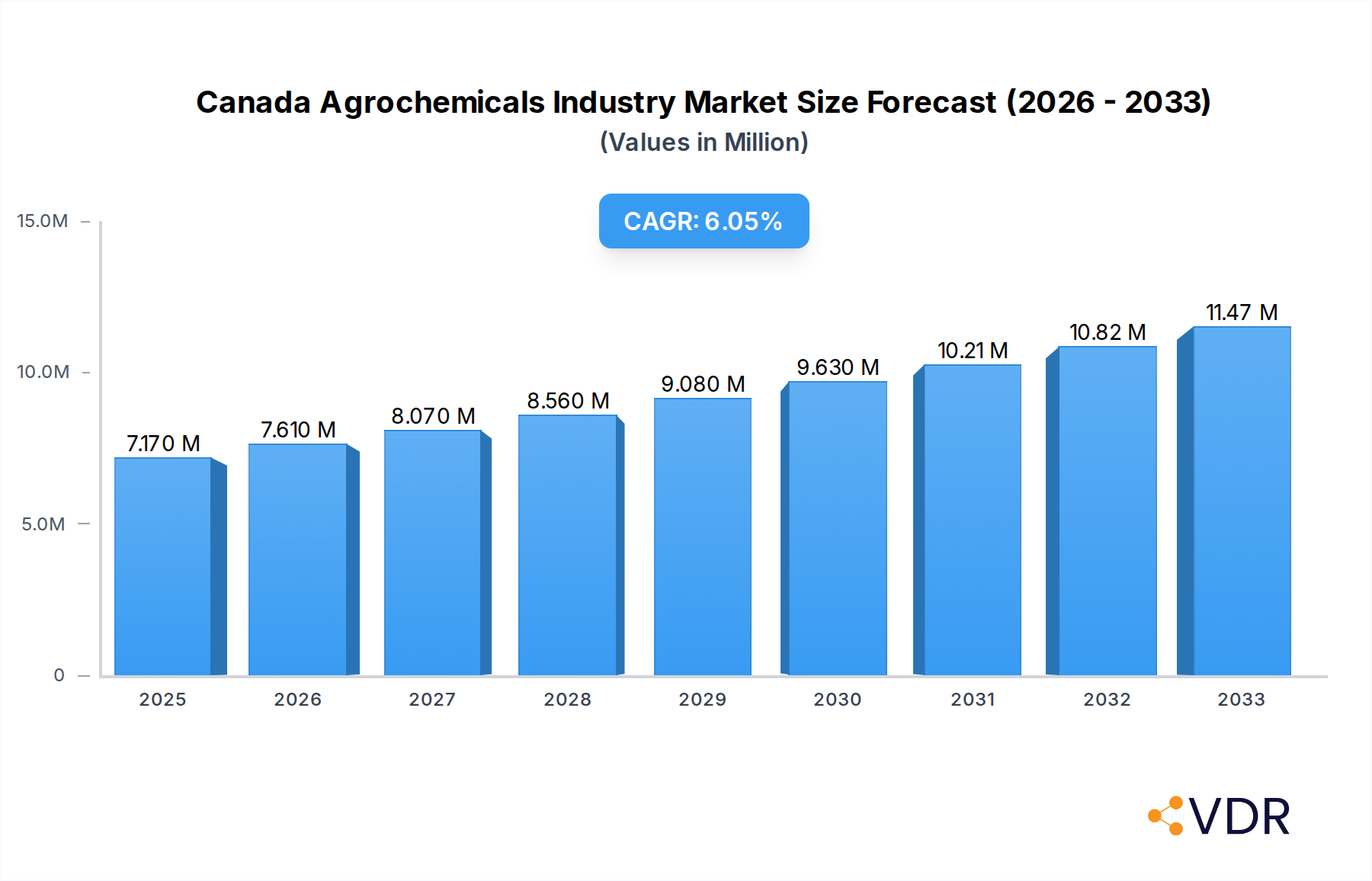

The Canadian Agrochemicals Industry is poised for significant expansion, with a current market size estimated at $7.17 million in 2025 and a projected Compound Annual Growth Rate (CAGR) of 6.10%. This robust growth is primarily driven by an increasing demand for enhanced crop yields and improved agricultural productivity to meet the rising global food requirements. Key drivers fueling this expansion include the adoption of advanced farming techniques, the continuous development of novel and more effective agrochemical formulations, and supportive government initiatives aimed at modernizing the agricultural sector. The industry's trajectory is also shaped by a growing emphasis on sustainable agriculture, leading to an increased demand for bio-based and environmentally friendly agrochemical solutions. Emerging trends such as precision agriculture, digital farming, and the integration of artificial intelligence in crop management are further stimulating innovation and market penetration for a wide array of agrochemical products.

Canada Agrochemicals Industry Market Size (In Million)

Despite the promising outlook, the industry faces certain restraints that necessitate strategic adaptation. These include escalating regulatory hurdles and environmental concerns associated with the widespread use of synthetic agrochemicals, alongside the increasing cost of raw materials and manufacturing processes. Furthermore, the growing awareness among consumers regarding food safety and the environmental impact of agricultural practices is prompting a shift towards organic and integrated pest management strategies, which could temper the growth of conventional agrochemical products. Nevertheless, the Canadian market demonstrates a strong propensity for adopting innovative agrochemical solutions that balance efficacy with environmental responsibility. The segmentation of the market into production, consumption, import/export, and price trends reveals dynamic shifts, with a notable focus on enhancing domestic production capabilities and managing international trade flows to ensure a stable supply chain. Leading global players are actively participating in this market, contributing to technological advancements and competitive offerings.

Canada Agrochemicals Industry Company Market Share

Canada Agrochemicals Industry Report: Market Dynamics, Trends, and Forecasts (2019-2033)

This comprehensive report provides an in-depth analysis of the Canadian Agrochemicals Industry, offering crucial insights into market dynamics, growth trends, regional dominance, product landscape, key players, and future outlook. Covering the historical period from 2019 to 2024, base year 2025, and a robust forecast period from 2025 to 2033, this report is an indispensable resource for stakeholders seeking to understand and capitalize on opportunities within this vital sector. The analysis delves into both parent and child markets, presenting all values in Million units for clear, actionable intelligence.

Canada Agrochemicals Industry Market Dynamics & Structure

The Canadian Agrochemicals Industry is characterized by a moderately concentrated market, with a few multinational corporations holding significant market shares. Technological innovation is a primary driver, fueled by research and development aimed at enhancing crop yields, improving pest and disease resistance, and promoting sustainable farming practices. Regulatory frameworks, overseen by Health Canada and Environment and Climate Change Canada, play a crucial role in product approval, usage guidelines, and environmental protection. Competitive product substitutes, such as biopesticides and advanced agricultural techniques, are emerging but currently represent a smaller portion of the overall market. End-user demographics are dominated by commercial farmers, with varying farm sizes and crop specializations across different regions. Merger and acquisition (M&A) trends indicate strategic consolidation and diversification by key players seeking to expand their product portfolios and market reach.

- Market Concentration: Dominated by global leaders such as Bayer CropScience AG, Syngenta, and Corteva Agriscience, with significant contributions from FMC Corporation and BASF SE.

- Technological Innovation Drivers: Focus on precision agriculture, genetically modified seeds with inherent pest resistance, and the development of more environmentally friendly and targeted chemical solutions.

- Regulatory Frameworks: Stringent approval processes for new active ingredients, ongoing reviews of existing products, and adherence to environmental stewardship guidelines.

- Competitive Product Substitutes: Growing interest in biological crop protection solutions, organic farming inputs, and integrated pest management (IPM) strategies.

- End-User Demographics: Large-scale grain producers in the Prairies, horticultural operations in Ontario and British Columbia, and specialized crop farmers across the country.

- M&A Trends: Strategic acquisitions to gain access to new technologies, expand product lines, and consolidate market presence. Recent activity has focused on acquiring smaller, innovative biotech firms and expanding into emerging markets.

Canada Agrochemicals Industry Growth Trends & Insights

The Canada Agrochemicals Industry has witnessed consistent growth, driven by the increasing demand for food security, the need to optimize agricultural productivity, and the adoption of advanced farming technologies. The market size has evolved significantly, with a steady increase in the adoption rates of both conventional and newer generation agrochemicals. Technological disruptions, such as the integration of artificial intelligence in crop management and the development of novel delivery systems for active ingredients, are reshaping the industry landscape. Consumer behavior shifts towards demanding sustainably produced food are also influencing the agrochemical market, pushing for the development and adoption of products with lower environmental impact. The industry is projected to maintain a healthy Compound Annual Growth Rate (CAGR) throughout the forecast period, reflecting ongoing innovation and the essential role of agrochemicals in Canadian agriculture.

The adoption rate of herbicides continues to be high, driven by the need to manage persistent weed challenges in large-scale farming. Fungicides are gaining importance due to changing weather patterns that favor fungal diseases. Insecticides remain critical for protecting staple crops from a wide array of pests. The market penetration of specialized products, such as plant growth regulators and micronutrient fertilizers, is expected to rise as farmers increasingly focus on precision agriculture and optimizing crop health beyond basic protection. This shift is supported by government initiatives promoting sustainable farming practices and technological advancements that enable more targeted application of inputs. The forecast period anticipates continued growth, with innovations in biologicals and precision application technologies playing an increasingly significant role in market expansion.

Dominant Regions, Countries, or Segments in Canada Agrochemicals Industry

The Prairie provinces, specifically Saskatchewan, Alberta, and Manitoba, are the dominant regions in the Canadian Agrochemicals Industry, driven by their extensive agricultural land and large-scale production of staple crops like wheat, canola, and corn. This dominance is reflected across all key market segments, including production, consumption, imports, exports, and price trends.

- Production Analysis: The Prairies host significant manufacturing facilities and formulation plants for agrochemicals, capitalizing on proximity to raw material sources and large consumer bases.

- Key Drivers: Vast arable land, government support for agriculture, and established infrastructure for storage and distribution.

- Market Share: Estimated to contribute over 60% of the national agrochemical production volume.

- Consumption Analysis: The sheer scale of farming operations in the Prairies translates to the highest consumption of herbicides, insecticides, and fungicides.

- Dominance Factors: Extensive acreage dedicated to major crops, requiring significant input for yield maximization and pest management.

- Growth Potential: Continuous demand for innovative crop protection solutions to combat evolving weed resistance and pest pressures.

- Import Market Analysis (Value & Volume): While Canada has domestic production, significant volumes of specialized active ingredients and finished products are imported to meet demand. The Prairies are the primary import destination due to their consumption levels.

- Key Drivers: Need for a diverse range of agrochemicals tailored to specific crop and regional needs, often sourced from global manufacturers.

- Value & Volume: Imports in the last historical year reached an estimated USD 2,500 Million in value and 800 Million units in volume.

- Export Market Analysis (Value & Volume): Canada exports a substantial amount of its manufactured agrochemicals, primarily to the United States and other international markets, leveraging its high-quality production standards.

- Key Drivers: Competitive pricing, quality assurance, and strong trade relationships.

- Value & Volume: Exports in the last historical year reached an estimated USD 1,800 Million in value and 550 Million units in volume.

- Price Trend Analysis: Prices in the Prairie region are influenced by global commodity prices, currency exchange rates, and supply-demand dynamics within North America. Local competition and government policies also play a role.

- Dominance Factors: The vastness of the market and the scale of operations allow for economies of scale in pricing, but also make it sensitive to international market fluctuations.

- Growth Potential: Increasing demand for higher-value, specialized products may lead to price differentiation and opportunities for premium offerings.

Canada Agrochemicals Industry Product Landscape

The Canadian agrochemical product landscape is dominated by herbicides, fungicides, and insecticides, essential for managing weeds, diseases, and pests in diverse agricultural settings. Innovations are increasingly focused on developing products with enhanced efficacy, improved safety profiles, and reduced environmental impact. This includes the development of selective herbicides that target specific weed species with minimal damage to crops, advanced fungicide formulations offering longer-lasting protection, and next-generation insecticides with targeted modes of action to mitigate resistance development. The market also sees growing interest in biopesticides and biostimulants, reflecting a trend towards sustainable agriculture and integrated pest management strategies.

Key Drivers, Barriers & Challenges in Canada Agrochemicals Industry

Key Drivers:

- Food Security and Demand: The growing global population and the need for efficient food production necessitate the use of agrochemicals to ensure high crop yields.

- Technological Advancements: Continuous innovation in product formulation, active ingredients, and application technologies enhances efficiency and sustainability.

- Government Support and R&D Investment: Favorable policies and investment in agricultural research and development foster market growth.

- Climate Change Adaptation: Agrochemicals play a role in helping crops adapt to changing environmental conditions and mitigate the impact of new pests and diseases.

Barriers & Challenges:

- Regulatory Hurdles: Stringent approval processes and evolving environmental regulations can increase development costs and time-to-market.

- Pest and Weed Resistance: The development of resistance to existing agrochemicals requires continuous innovation and the introduction of new products, posing a significant challenge.

- Public Perception and Environmental Concerns: Negative public perception and concerns regarding the environmental and health impacts of certain agrochemicals can lead to market resistance and policy changes.

- Supply Chain Disruptions: Global supply chain issues, geopolitical instability, and fluctuating raw material prices can impact the availability and cost of agrochemical inputs.

Emerging Opportunities in Canada Agrochemicals Industry

Emerging opportunities in the Canadian Agrochemicals Industry lie in the expanding market for biological crop protection solutions and biostimulants, catering to the growing demand for sustainable and organic farming practices. The development of precision agriculture technologies, including smart application systems and data-driven crop management, presents a significant avenue for growth. Furthermore, niche markets for specialized agrochemicals targeting high-value crops and addressing specific regional agricultural challenges are poised for expansion. The increasing focus on soil health and nutrient management also opens doors for innovative fertilizer and soil amendment products.

Growth Accelerators in the Canada Agrochemicals Industry Industry

Growth accelerators for the Canadian Agrochemicals Industry are primarily driven by ongoing technological breakthroughs in biotechnology and chemical synthesis, leading to the development of more effective and environmentally benign products. Strategic partnerships between agrochemical manufacturers, research institutions, and agricultural technology companies are fostering innovation and accelerating market penetration. Furthermore, market expansion strategies, including the development of integrated crop solutions and the adoption of digital platforms for farmer engagement and product distribution, are crucial growth catalysts. Government incentives promoting sustainable agriculture and investment in agricultural infrastructure also play a significant role.

Key Players Shaping the Canada Agrochemicals Industry Market

- FMC Corporation

- Archer-Daniels-Midland (ADM)

- Dow Agrosciences LLC

- Adama Agricultural Solutions Ltd

- Syngenta

- UPL Limited

- Corteva Agriscience

- Bayer CropScience AG

- Nufarm Ltd

- BASF SE

Notable Milestones in Canada Agrochemicals Industry Sector

- September 2022: Gowan Canada and ISK BioSciences launched 'Insight 339SC', a new group 14 herbicide for pre-seed burnoff applications in wheat, corn, and soybean. Insight 339SC provides rapid and effective pre-seed burndown of important broadleaf weeds like kochia, redroot pigweed, common lamb's quarters, and wild buckwheat.

- July 2022: Pivot Bio, agriculture's leading nitrogen innovator, announced its expansion into Canada, including launching the company's business operations, appointing its leadership team, and its future plans to offer sustainable nitrogen to Canadian farmers, pending regulatory approvals.

- May 2022: Protein Industries Canada announced a USD 19 million project along with a consortium of companies that will help Canadian farmers further improve their sustainability and reduce carbon emissions through the commercialization of a new micronutrient fertilizer.

In-Depth Canada Agrochemicals Industry Market Outlook

The outlook for the Canada Agrochemicals Industry is highly positive, driven by a confluence of factors including sustained demand for agricultural output, continuous innovation, and a growing emphasis on sustainable farming practices. The increasing adoption of precision agriculture technologies and the development of bio-based solutions will further fuel market growth. Strategic collaborations and government initiatives aimed at enhancing agricultural productivity and environmental stewardship are expected to create a fertile ground for expansion. Stakeholders can anticipate robust growth in specialized product segments and a continued evolution towards more targeted and environmentally conscious agrochemical solutions, ensuring the industry's vital role in supporting Canadian agriculture.

Canada Agrochemicals Industry Segmentation

- 1. Production Analysis

- 2. Consumption Analysis

- 3. Import Market Analysis (Value & Volume)

- 4. Export Market Analysis (Value & Volume)

- 5. Price Trend Analysis

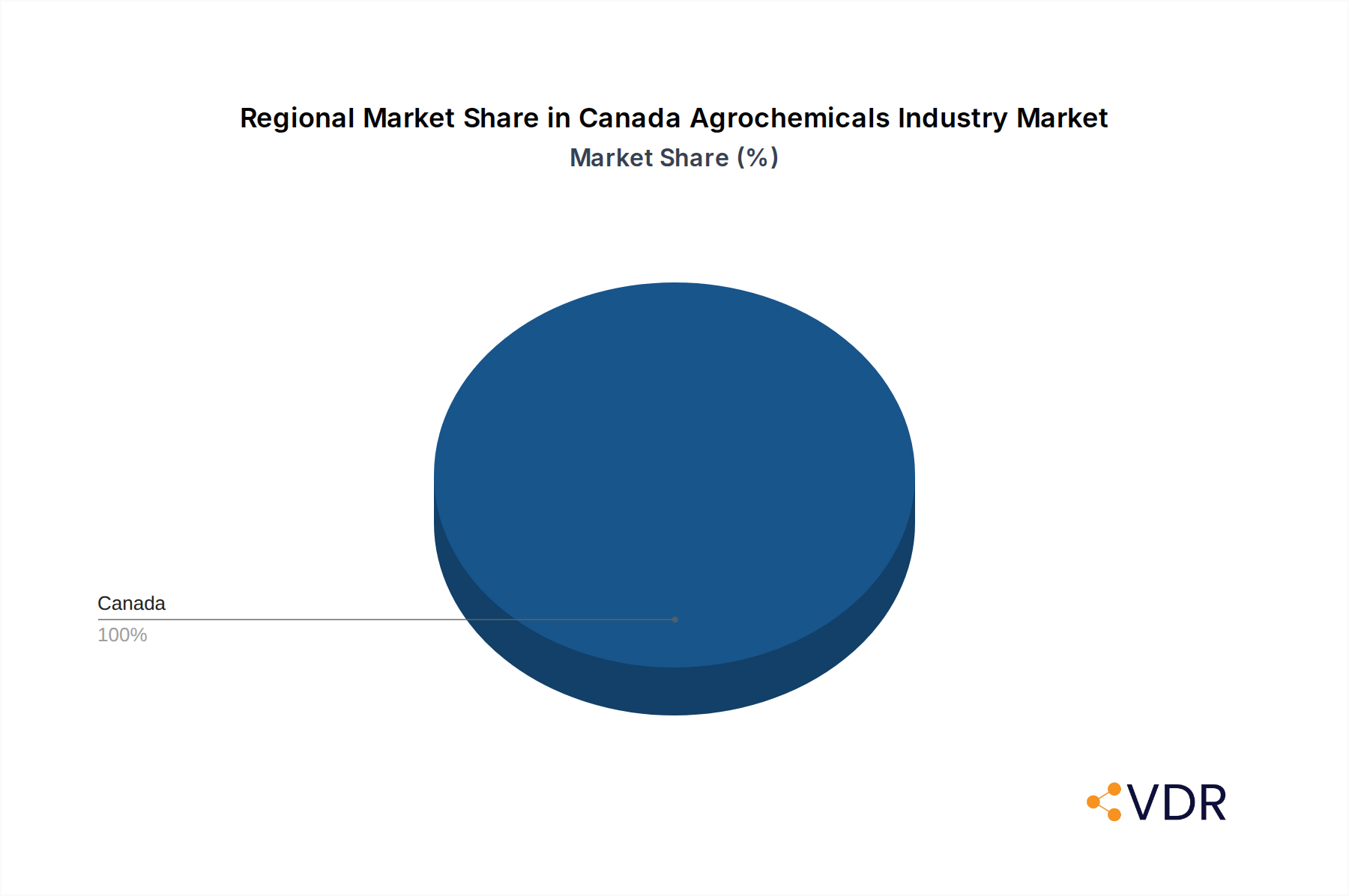

Canada Agrochemicals Industry Segmentation By Geography

- 1. Canada

Canada Agrochemicals Industry Regional Market Share

Geographic Coverage of Canada Agrochemicals Industry

Canada Agrochemicals Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.10% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Production Analysis

- 5.2. Market Analysis, Insights and Forecast - by Consumption Analysis

- 5.3. Market Analysis, Insights and Forecast - by Import Market Analysis (Value & Volume)

- 5.4. Market Analysis, Insights and Forecast - by Export Market Analysis (Value & Volume)

- 5.5. Market Analysis, Insights and Forecast - by Price Trend Analysis

- 5.6. Market Analysis, Insights and Forecast - by Region

- 5.6.1. Canada

- 6. Canada Agrochemicals Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Production Analysis

- 6.2. Market Analysis, Insights and Forecast - by Consumption Analysis

- 6.3. Market Analysis, Insights and Forecast - by Import Market Analysis (Value & Volume)

- 6.4. Market Analysis, Insights and Forecast - by Export Market Analysis (Value & Volume)

- 6.5. Market Analysis, Insights and Forecast - by Price Trend Analysis

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 FMC Corporation

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Archer-daniels-midland (ADM)

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Dow Agrosciences LL

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Adama Agricultural Solutions Ltd

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Syngenta

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 UPL Limited

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Corteva Agriscience

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Bayer CropScience AG

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Nufarm Ltd

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 BASF SE

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 FMC Corporation

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Canada Agrochemicals Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Canada Agrochemicals Industry Share (%) by Company 2025

List of Tables

- Table 1: Canada Agrochemicals Industry Revenue Million Forecast, by Production Analysis 2020 & 2033

- Table 2: Canada Agrochemicals Industry Revenue Million Forecast, by Consumption Analysis 2020 & 2033

- Table 3: Canada Agrochemicals Industry Revenue Million Forecast, by Import Market Analysis (Value & Volume) 2020 & 2033

- Table 4: Canada Agrochemicals Industry Revenue Million Forecast, by Export Market Analysis (Value & Volume) 2020 & 2033

- Table 5: Canada Agrochemicals Industry Revenue Million Forecast, by Price Trend Analysis 2020 & 2033

- Table 6: Canada Agrochemicals Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 7: Canada Agrochemicals Industry Revenue Million Forecast, by Production Analysis 2020 & 2033

- Table 8: Canada Agrochemicals Industry Revenue Million Forecast, by Consumption Analysis 2020 & 2033

- Table 9: Canada Agrochemicals Industry Revenue Million Forecast, by Import Market Analysis (Value & Volume) 2020 & 2033

- Table 10: Canada Agrochemicals Industry Revenue Million Forecast, by Export Market Analysis (Value & Volume) 2020 & 2033

- Table 11: Canada Agrochemicals Industry Revenue Million Forecast, by Price Trend Analysis 2020 & 2033

- Table 12: Canada Agrochemicals Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Canada Agrochemicals Industry?

The projected CAGR is approximately 6.10%.

2. Which companies are prominent players in the Canada Agrochemicals Industry?

Key companies in the market include FMC Corporation, Archer-daniels-midland (ADM), Dow Agrosciences LL, Adama Agricultural Solutions Ltd, Syngenta, UPL Limited, Corteva Agriscience, Bayer CropScience AG, Nufarm Ltd, BASF SE.

3. What are the main segments of the Canada Agrochemicals Industry?

The market segments include Production Analysis, Consumption Analysis, Import Market Analysis (Value & Volume), Export Market Analysis (Value & Volume), Price Trend Analysis.

4. Can you provide details about the market size?

The market size is estimated to be USD 7.17 Million as of 2022.

5. What are some drivers contributing to market growth?

Decreasing Per Capita Arable Land; Increased Demand for Food.

6. What are the notable trends driving market growth?

Need for Improving Productivity by Limiting the Crop Damage.

7. Are there any restraints impacting market growth?

High Initial Investments; Requirement of Precision Agriculture.

8. Can you provide examples of recent developments in the market?

September 2022: Gowan Canada and ISK BioSciences launched 'Insight 339SC', a new group 14 herbicide for pre-seed burnoff applications in wheat, corn, and soybean. Insight 339SC provides rapid and effective pre-seed burndown of important broadleaf weeds like kochia, redroot pigweed, common lamb's quarters, and wild buckwheat.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Canada Agrochemicals Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Canada Agrochemicals Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Canada Agrochemicals Industry?

To stay informed about further developments, trends, and reports in the Canada Agrochemicals Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence