Key Insights

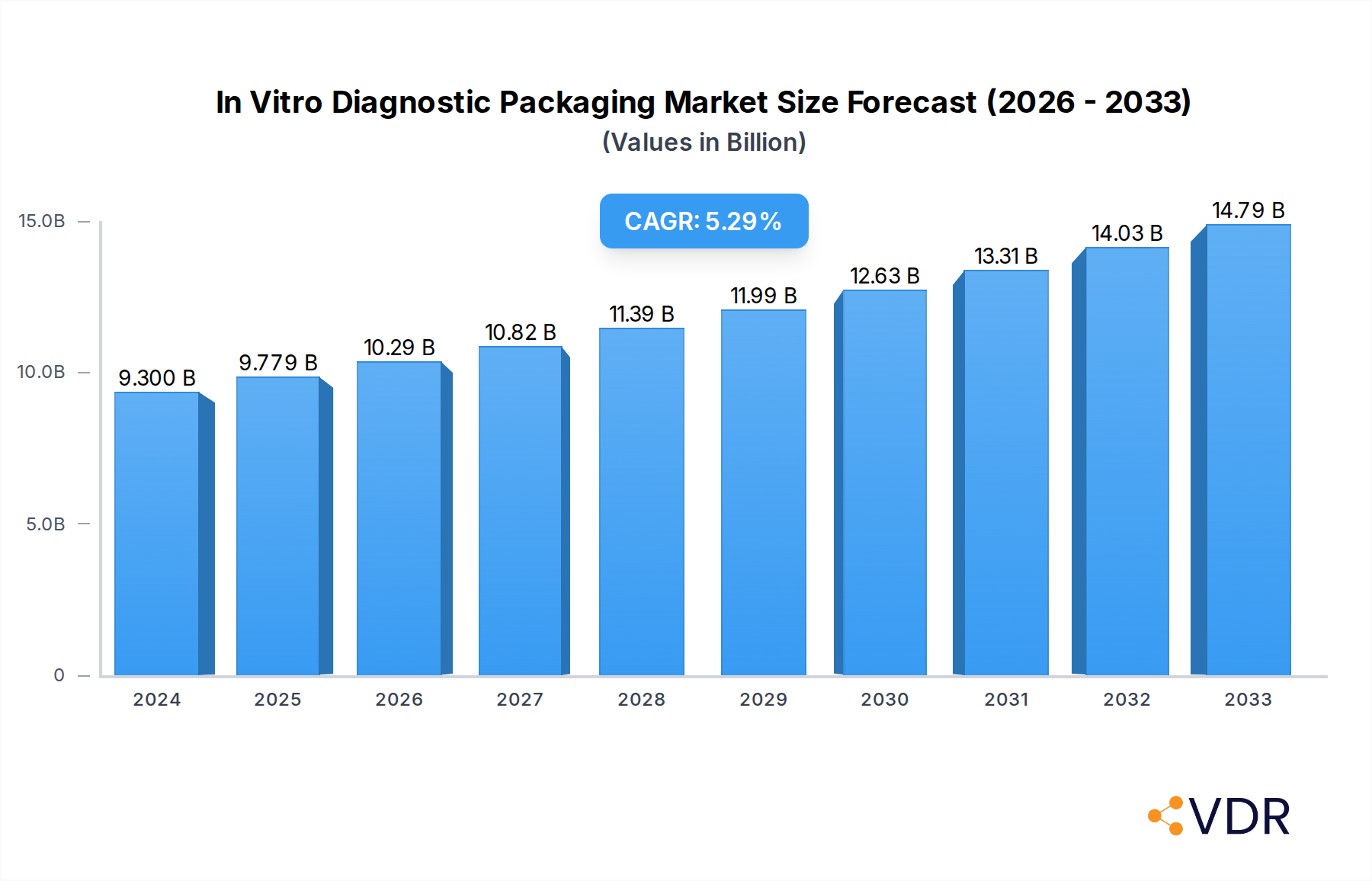

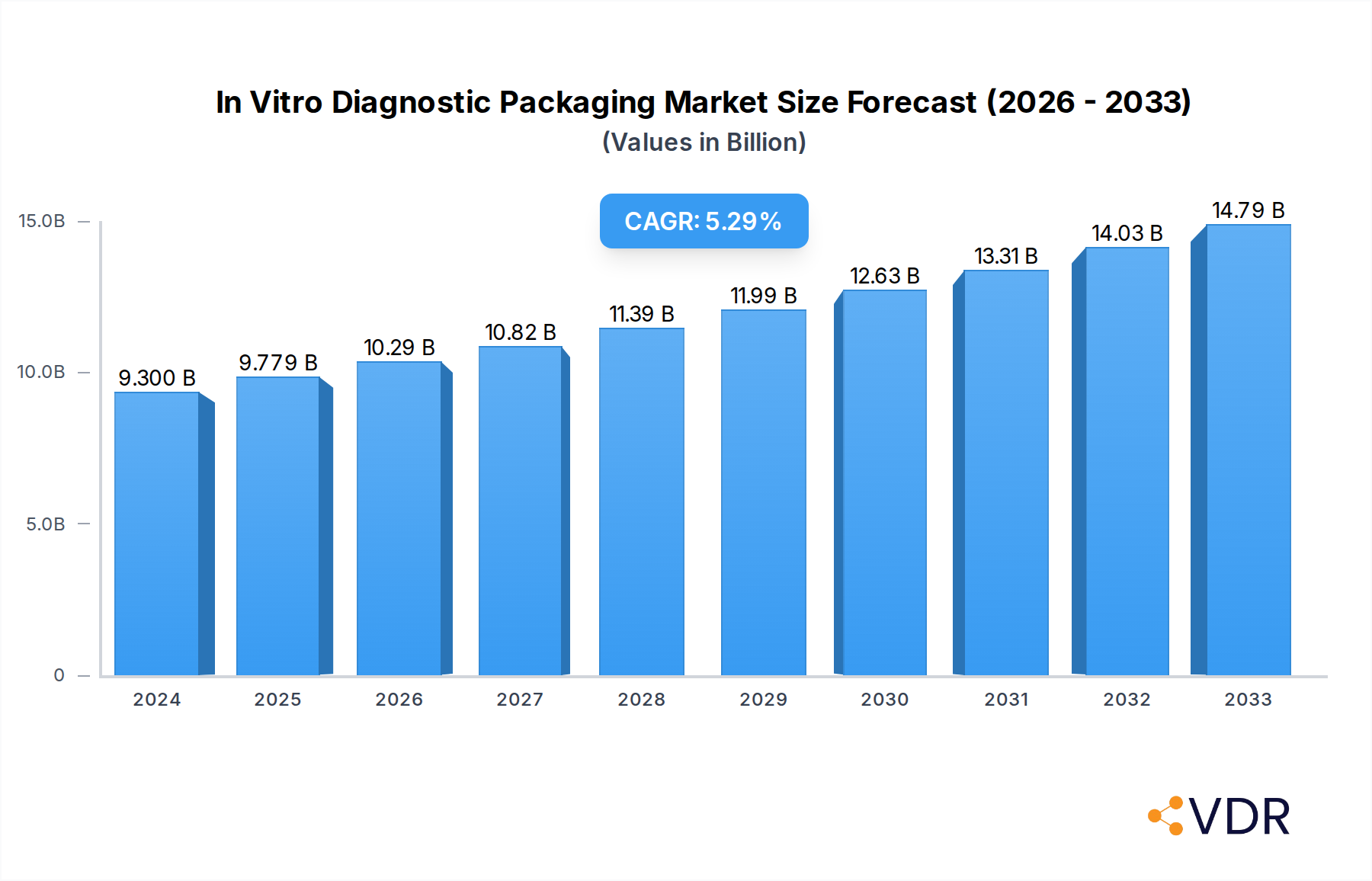

The global In Vitro Diagnostic (IVD) packaging market is poised for significant expansion, projected to reach an estimated $9.3 billion in 2024, demonstrating a robust Compound Annual Growth Rate (CAGR) of 5.1% through to 2033. This growth trajectory is underpinned by an increasing demand for accurate and reliable diagnostic testing across healthcare settings. Key market drivers include the rising prevalence of chronic diseases, a growing aging population, and advancements in diagnostic technologies that necessitate specialized packaging solutions to maintain sample integrity and ensure user safety. The expanding healthcare infrastructure in emerging economies also contributes significantly to market growth, as diagnostic capabilities become more accessible. Furthermore, the escalating focus on personalized medicine and companion diagnostics is fueling the need for highly specific and secure IVD packaging, capable of preserving the sensitive nature of biological samples from collection to analysis.

In Vitro Diagnostic Packaging Market Size (In Billion)

The IVD packaging market is characterized by a diverse range of applications and product types. Hospitals and diagnostic laboratories represent the largest application segments, driven by high testing volumes. Academic and research institutes also contribute to demand, particularly for specialized research-grade packaging. In terms of product types, bottles and tubes are the dominant categories, essential for collecting and storing various biological specimens such as blood, urine, and tissue. The market is also witnessing a growing demand for specialized containers for complex diagnostic assays and point-of-care testing. Key market players are actively engaged in innovation, focusing on materials that offer enhanced chemical resistance, improved sealing capabilities, and advanced traceability features. The industry is also increasingly prioritizing sustainable packaging solutions, responding to global environmental concerns. Restraints, such as stringent regulatory compliance and the high cost of specialized materials, are being navigated through technological advancements and strategic partnerships.

In Vitro Diagnostic Packaging Company Market Share

In Vitro Diagnostic Packaging Market Dynamics & Structure

The in vitro diagnostic (IVD) packaging market is characterized by a moderate to high concentration, with key players like Amcor, Bio-Rad Laboratories, Corning, Greiner, Aptar, and Duran Group holding significant market shares. Technological innovation is a primary driver, fueled by advancements in material science for enhanced sample integrity, sterile barrier systems, and tamper-evident solutions. Stringent regulatory frameworks, such as those from the FDA and EMA, dictate packaging compliance, safety, and efficacy, influencing material choices and design. Competitive product substitutes primarily include alternative container types and advancements in point-of-care diagnostics that might reduce the need for traditional packaging. End-user demographics, encompassing hospitals, diagnostic laboratories, and academic research institutes, exhibit varying demands for specialized packaging solutions based on application and sample volume. Mergers and acquisitions (M&A) trends are observed, with larger packaging manufacturers acquiring smaller, specialized firms to expand their product portfolios and geographical reach. For instance, the acquisition of specialized medical packaging companies by Amcor aims to bolster their presence in the high-growth IVD sector. Innovation barriers include the high cost of developing and validating new packaging materials that meet stringent IVD requirements and the lengthy regulatory approval processes.

- Market Concentration: Moderate to High, driven by consolidation and the presence of established global players.

- Technological Innovation: Focus on barrier properties, sterility, and smart packaging features.

- Regulatory Frameworks: FDA, EMA, ISO standards are crucial for market entry and compliance.

- Competitive Product Substitutes: Advancements in diagnostic technologies and alternative container materials.

- End-User Demographics: Hospitals (xx%), Laboratories (xx%), Academic Institutes (xx%) with specific needs.

- M&A Trends: Consolidation to expand product offerings and market penetration.

- Innovation Barriers: High R&D costs, lengthy regulatory approvals.

In Vitro Diagnostic Packaging Growth Trends & Insights

The global in vitro diagnostic packaging market is poised for robust growth, driven by an escalating demand for diagnostic testing and the continuous evolution of the healthcare landscape. The market size is projected to expand significantly, with an estimated CAGR of approximately 7.2% from 2025 to 2033. This growth is underpinned by increasing patient populations, a rising prevalence of chronic diseases, and a growing emphasis on early disease detection and personalized medicine. Adoption rates for advanced IVD packaging solutions are accelerating as manufacturers and diagnostic companies prioritize sample integrity, safety, and extended shelf-life to ensure accurate test results. Technological disruptions, such as the development of novel sterilization techniques, antimicrobial packaging materials, and smart packaging solutions incorporating track-and-trace capabilities, are revolutionizing the industry. These innovations address critical needs for preventing contamination, maintaining sample viability during transit and storage, and enhancing supply chain transparency. Consumer behavior shifts are also playing a vital role; healthcare providers are increasingly demanding packaging that offers convenience, ease of use, and reliable performance. This includes a preference for lightweight, durable, and environmentally sustainable packaging options where feasible, without compromising on critical safety and sterility requirements. The expansion of point-of-care diagnostics also necessitates specialized, often smaller-format packaging solutions that maintain sterility and protect sensitive reagents. Furthermore, the growing demand for liquid biopsy and companion diagnostics, which often require specialized collection tubes and vials, is a significant growth catalyst. The global market for IVD packaging is projected to reach an estimated value of over $25.3 billion units by 2033, up from approximately $14.5 billion units in 2025. This substantial expansion reflects the critical role of packaging in ensuring the accuracy, reliability, and accessibility of in vitro diagnostics worldwide.

Dominant Regions, Countries, or Segments in In Vitro Diagnostic Packaging

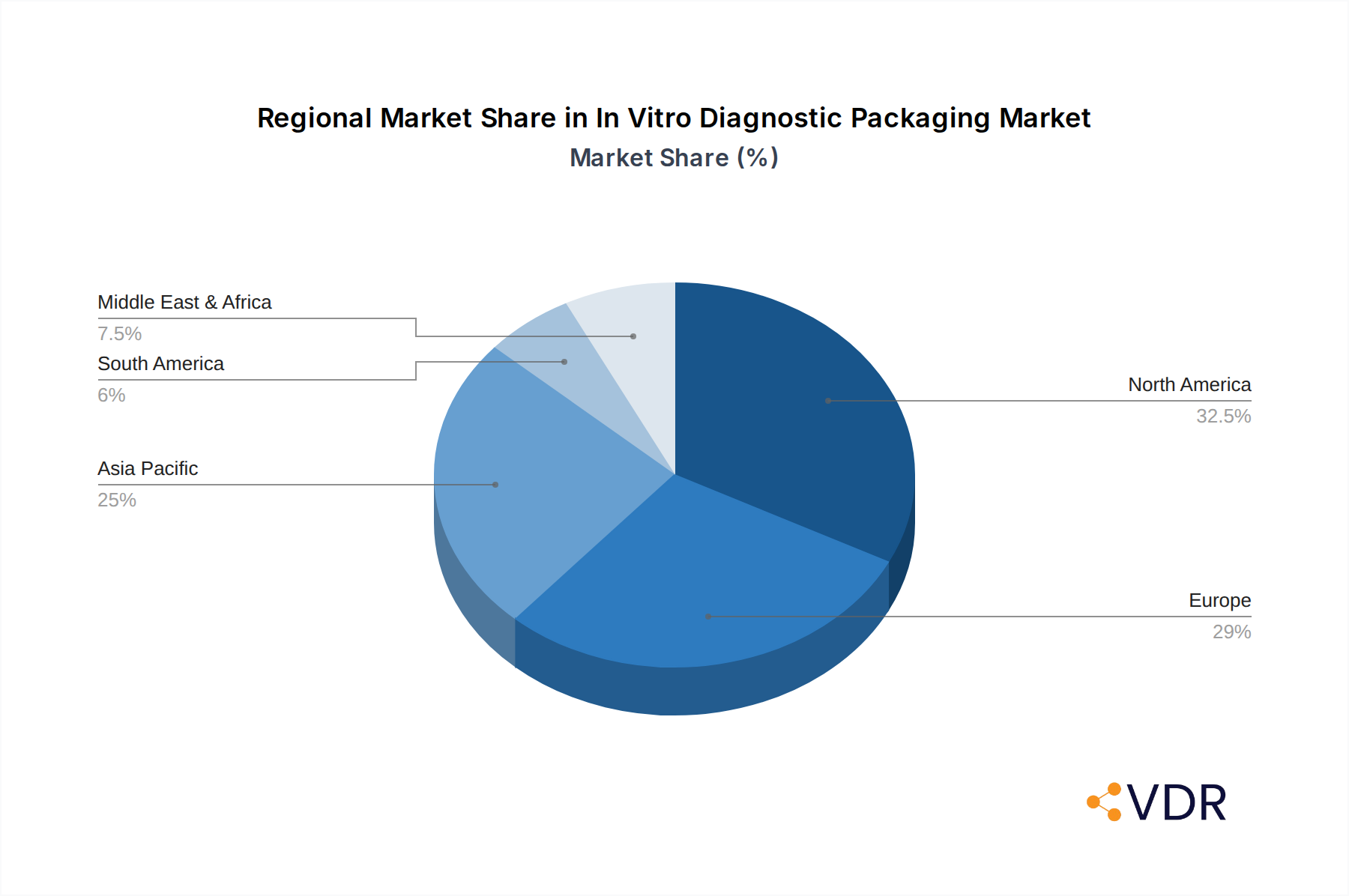

The in vitro diagnostic (IVD) packaging market exhibits distinct regional and segmental dominance, driven by a confluence of economic policies, healthcare infrastructure development, and technological adoption rates. North America, particularly the United States, currently holds a leading position in the IVD packaging market. This dominance is attributed to its highly developed healthcare system, substantial investment in research and development of diagnostic technologies, and a large patient pool undergoing diagnostic tests. The region benefits from a robust regulatory framework that, while stringent, fosters innovation and ensures high standards of quality and safety for IVD packaging. Furthermore, the presence of major IVD manufacturers and contract research organizations in North America stimulates the demand for sophisticated and specialized packaging solutions.

Examining the application segments, Laboratories emerge as the most dominant consumer of IVD packaging. Diagnostic laboratories, both standalone and hospital-affiliated, perform the vast majority of in vitro diagnostic tests. This segment's demand is characterized by a need for high-volume, reliable, and precisely engineered packaging for a wide array of sample types, including blood, urine, and tissue. The increasing sophistication of laboratory automation and the expansion of molecular diagnostics further amplify the demand for specialized tubes, vials, and collection devices. Hospitals also represent a significant, albeit secondary, application segment, with their demand driven by in-house laboratory testing and the critical need for sterile and secure packaging to ensure patient safety. Academic Institutes contribute to the demand, particularly for research-oriented IVD reagents and sample containment.

In terms of product type, Tubes constitute the largest and most dominant segment within IVD packaging. This is directly linked to the prevalence of blood collection and sample processing in diagnostic workflows. The market for blood collection tubes, ranging from simple vacuum tubes to advanced tubes with specific additives for various biochemical assays, is immense. The continuous evolution of these tubes to improve sample stability, reduce clotting times, and enhance diagnostic accuracy fuels their market dominance. Bottles and other specialized containers also play a crucial role, particularly for reagent packaging, sample storage, and the transport of bulk diagnostic materials.

Key drivers for this dominance include:

- Economic Policies: Favorable healthcare reimbursement policies in North America encourage widespread diagnostic testing, thereby boosting packaging demand.

- Infrastructure: Well-established logistics and supply chains in dominant regions ensure efficient distribution of IVD products and their packaging.

- Technological Advancement: Leading regions are at the forefront of developing and adopting new IVD technologies, which in turn require innovative and specialized packaging.

- Market Share & Growth Potential: North America commands a significant market share due to its advanced healthcare ecosystem, while Asia-Pacific is showing rapid growth potential driven by increasing healthcare expenditure and a burgeoning diagnostic market. The Laboratories segment, due to its sheer volume of testing, offers the most consistent and substantial market share for IVD packaging. The Tubes segment's dominance is intrinsically tied to fundamental diagnostic procedures like blood draws, ensuring sustained high demand.

In Vitro Diagnostic Packaging Product Landscape

The IVD packaging product landscape is characterized by a relentless pursuit of enhanced sample integrity, sterility assurance, and user convenience. Innovations span advanced polymer materials offering superior barrier properties against moisture, oxygen, and light, thereby extending product shelf-life and ensuring diagnostic accuracy. Sterile barrier systems, including specialized films, pouches, and rigid containers, are paramount, designed to maintain aseptic conditions from manufacturing to the point of use. Tamper-evident features and robust sealing mechanisms are critical for security and regulatory compliance. Product applications range from small collection tubes for blood and urine samples to larger bottles for reagents and diagnostic kits, with a growing emphasis on customizable solutions for specific IVD assays. Performance metrics focus on chemical inertness, leachables and extractables testing, and resistance to sterilization methods, ensuring no compromise to the diagnostic sample or reagent.

Key Drivers, Barriers & Challenges in In Vitro Diagnostic Packaging

The in vitro diagnostic packaging market is propelled by several key drivers. The escalating global demand for diagnostic testing, fueled by an aging population and the rising incidence of chronic and infectious diseases, is a primary growth catalyst. Advancements in diagnostic technologies, such as molecular diagnostics and companion diagnostics, necessitate specialized and high-performance packaging. Furthermore, increasing healthcare expenditure, particularly in emerging economies, expands market access and demand for IVD products and their associated packaging. Technological innovation in material science, leading to improved barrier properties, sterility, and shelf-life, also drives adoption.

However, significant barriers and challenges exist. Stringent and evolving regulatory requirements from bodies like the FDA and EMA impose high costs and lengthy approval timelines for new packaging materials and designs. The need for specialized materials that are biocompatible, chemically inert, and safe for diagnostic samples can lead to higher manufacturing costs. Supply chain disruptions, as seen in recent global events, can impact the availability and cost of raw materials. Intense competition among packaging manufacturers, coupled with price sensitivity from some end-users, also poses a challenge. The environmental impact and sustainability of packaging materials are becoming increasingly important considerations, requiring a balance between performance and eco-friendliness.

Emerging Opportunities in In Vitro Diagnostic Packaging

Emerging opportunities in the IVD packaging sector lie in the development of smart packaging solutions that can provide real-time data on sample integrity, temperature fluctuations, and even tamper detection. The growing field of personalized medicine and companion diagnostics creates a niche for highly specialized, low-volume packaging solutions tailored to specific genetic tests and targeted therapies. Furthermore, the expansion of point-of-care diagnostics requires innovative, user-friendly, and often integrated packaging designs that simplify sample collection and analysis outside traditional laboratory settings. Growing awareness and regulatory push towards sustainable packaging present opportunities for manufacturers developing biodegradable or recyclable IVD packaging materials that meet stringent performance and safety standards.

Growth Accelerators in the In Vitro Diagnostic Packaging Industry

The in vitro diagnostic packaging industry's long-term growth is significantly accelerated by continuous technological breakthroughs in material science and manufacturing processes. The development of novel polymers with enhanced barrier properties, improved chemical inertness, and increased resistance to extreme conditions directly supports the expanding range of sensitive diagnostic tests. Strategic partnerships between packaging manufacturers and IVD assay developers are crucial, fostering co-creation of packaging solutions that optimize sample handling, stability, and overall diagnostic accuracy. Market expansion strategies, particularly targeting the rapidly growing healthcare markets in Asia-Pacific and Latin America, will also serve as powerful growth accelerators. The increasing adoption of automation in diagnostic workflows also drives demand for packaging that is compatible with high-speed processing.

Key Players Shaping the In Vitro Diagnostic Packaging Market

- Amcor

- Bio-Rad Laboratories

- Corning

- Greiner

- Narang Medical

- Duran Group

- Wheaton Industries

- MCC Label

- Sarstedt

- Aptar

Notable Milestones in In Vitro Diagnostic Packaging Sector

- 2019: Launch of new antimicrobial-treated blood collection tubes by Sarstedt, enhancing sample safety and stability.

- 2020: Amcor's acquisition of a significant share in a specialized medical packaging company, bolstering its IVD offerings.

- 2021: Corning introduces advanced glass vial solutions for sensitive biologic samples, improving drug development and diagnostics.

- 2022: Aptar's development of innovative spray bottle technologies for diagnostic reagents, improving ease of use and accuracy.

- 2023: Greiner Bio-One expands its range of cryogenic storage tubes with enhanced sealing technology for long-term sample preservation.

- 2024: Wheaton Industries unveils new designs for diagnostic collection kits focusing on improved ergonomics and sterilization.

In-Depth In Vitro Diagnostic Packaging Market Outlook

The future outlook for the in vitro diagnostic packaging market is exceptionally promising, driven by an unwavering demand for accurate and reliable diagnostic solutions globally. Growth accelerators such as ongoing innovations in material science, the increasing prevalence of personalized medicine, and the expansion of point-of-care diagnostics will continue to shape the market. Strategic collaborations between packaging experts and IVD manufacturers are anticipated to yield next-generation packaging that enhances sample integrity, traceability, and user experience. Furthermore, the market is poised for significant expansion in emerging economies, presenting substantial opportunities for both established and new players. The emphasis on sustainable packaging solutions will also continue to grow, necessitating further research and development in eco-friendly alternatives that do not compromise on critical performance standards.

In Vitro Diagnostic Packaging Segmentation

-

1. Application

- 1.1. Hospitals

- 1.2. Laboratories

- 1.3. Academic Institutes

-

2. Type

- 2.1. Bottles

- 2.2. Tubes

- 2.3. Others

In Vitro Diagnostic Packaging Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

In Vitro Diagnostic Packaging Regional Market Share

Geographic Coverage of In Vitro Diagnostic Packaging

In Vitro Diagnostic Packaging REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Hospitals

- 5.1.2. Laboratories

- 5.1.3. Academic Institutes

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Bottles

- 5.2.2. Tubes

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global In Vitro Diagnostic Packaging Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Hospitals

- 6.1.2. Laboratories

- 6.1.3. Academic Institutes

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Bottles

- 6.2.2. Tubes

- 6.2.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America In Vitro Diagnostic Packaging Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Hospitals

- 7.1.2. Laboratories

- 7.1.3. Academic Institutes

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Bottles

- 7.2.2. Tubes

- 7.2.3. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America In Vitro Diagnostic Packaging Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Hospitals

- 8.1.2. Laboratories

- 8.1.3. Academic Institutes

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Bottles

- 8.2.2. Tubes

- 8.2.3. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe In Vitro Diagnostic Packaging Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Hospitals

- 9.1.2. Laboratories

- 9.1.3. Academic Institutes

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Bottles

- 9.2.2. Tubes

- 9.2.3. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa In Vitro Diagnostic Packaging Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Hospitals

- 10.1.2. Laboratories

- 10.1.3. Academic Institutes

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Bottles

- 10.2.2. Tubes

- 10.2.3. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific In Vitro Diagnostic Packaging Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Hospitals

- 11.1.2. Laboratories

- 11.1.3. Academic Institutes

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. Bottles

- 11.2.2. Tubes

- 11.2.3. Others

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Bio-Rad Laboratories

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Corning

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Greiner

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Narang Medical

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Amcor

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Duran Group

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Wheaton Industries

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 MCC Label

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Sarstedt

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Aptar

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Bio-Rad Laboratories

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global In Vitro Diagnostic Packaging Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America In Vitro Diagnostic Packaging Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America In Vitro Diagnostic Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America In Vitro Diagnostic Packaging Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America In Vitro Diagnostic Packaging Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America In Vitro Diagnostic Packaging Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America In Vitro Diagnostic Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America In Vitro Diagnostic Packaging Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America In Vitro Diagnostic Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America In Vitro Diagnostic Packaging Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America In Vitro Diagnostic Packaging Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America In Vitro Diagnostic Packaging Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America In Vitro Diagnostic Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe In Vitro Diagnostic Packaging Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe In Vitro Diagnostic Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe In Vitro Diagnostic Packaging Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe In Vitro Diagnostic Packaging Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe In Vitro Diagnostic Packaging Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe In Vitro Diagnostic Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa In Vitro Diagnostic Packaging Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa In Vitro Diagnostic Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa In Vitro Diagnostic Packaging Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa In Vitro Diagnostic Packaging Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa In Vitro Diagnostic Packaging Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa In Vitro Diagnostic Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific In Vitro Diagnostic Packaging Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific In Vitro Diagnostic Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific In Vitro Diagnostic Packaging Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific In Vitro Diagnostic Packaging Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific In Vitro Diagnostic Packaging Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific In Vitro Diagnostic Packaging Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global In Vitro Diagnostic Packaging Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global In Vitro Diagnostic Packaging Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global In Vitro Diagnostic Packaging Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global In Vitro Diagnostic Packaging Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global In Vitro Diagnostic Packaging Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global In Vitro Diagnostic Packaging Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States In Vitro Diagnostic Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada In Vitro Diagnostic Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico In Vitro Diagnostic Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global In Vitro Diagnostic Packaging Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global In Vitro Diagnostic Packaging Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global In Vitro Diagnostic Packaging Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil In Vitro Diagnostic Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina In Vitro Diagnostic Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America In Vitro Diagnostic Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global In Vitro Diagnostic Packaging Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global In Vitro Diagnostic Packaging Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global In Vitro Diagnostic Packaging Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom In Vitro Diagnostic Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany In Vitro Diagnostic Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France In Vitro Diagnostic Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy In Vitro Diagnostic Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain In Vitro Diagnostic Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia In Vitro Diagnostic Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux In Vitro Diagnostic Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics In Vitro Diagnostic Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe In Vitro Diagnostic Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global In Vitro Diagnostic Packaging Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global In Vitro Diagnostic Packaging Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global In Vitro Diagnostic Packaging Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey In Vitro Diagnostic Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel In Vitro Diagnostic Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC In Vitro Diagnostic Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa In Vitro Diagnostic Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa In Vitro Diagnostic Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa In Vitro Diagnostic Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global In Vitro Diagnostic Packaging Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global In Vitro Diagnostic Packaging Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global In Vitro Diagnostic Packaging Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China In Vitro Diagnostic Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India In Vitro Diagnostic Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan In Vitro Diagnostic Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea In Vitro Diagnostic Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN In Vitro Diagnostic Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania In Vitro Diagnostic Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific In Vitro Diagnostic Packaging Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the In Vitro Diagnostic Packaging?

The projected CAGR is approximately 5.1%.

2. Which companies are prominent players in the In Vitro Diagnostic Packaging?

Key companies in the market include Bio-Rad Laboratories, Corning, Greiner, Narang Medical, Amcor, Duran Group, Wheaton Industries, MCC Label, Sarstedt, Aptar.

3. What are the main segments of the In Vitro Diagnostic Packaging?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "In Vitro Diagnostic Packaging," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the In Vitro Diagnostic Packaging report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the In Vitro Diagnostic Packaging?

To stay informed about further developments, trends, and reports in the In Vitro Diagnostic Packaging, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence