Key Insights

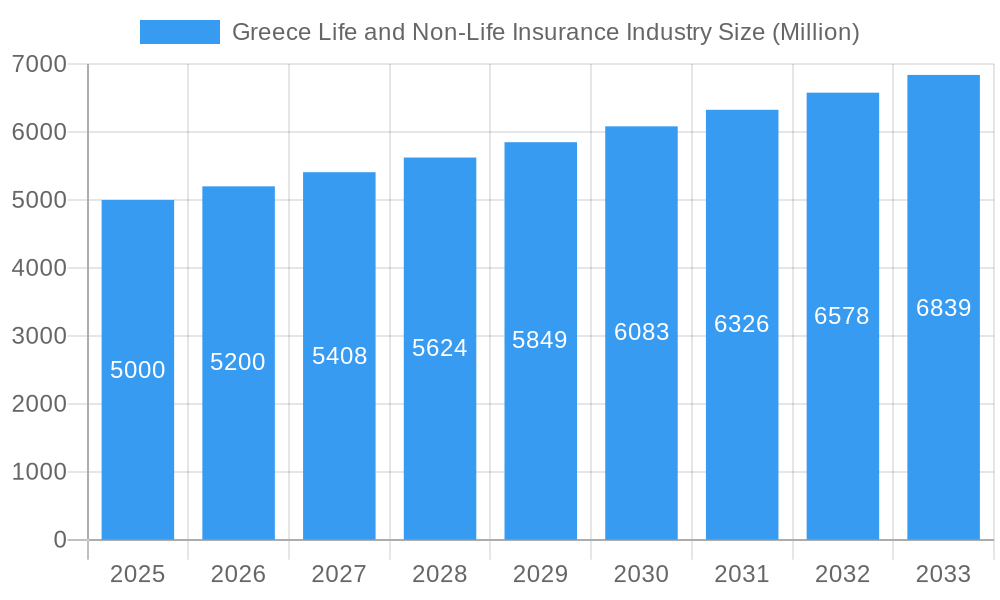

The Greek life and non-life insurance market, though smaller than many Western European counterparts, demonstrates resilience and evolution. Between 2019 and 2024, the sector experienced consolidation and cautious expansion, shaped by the Eurozone crisis aftermath and economic recovery. Key growth drivers include an aging demographic, heightened risk management awareness, and the progressive digitalization of insurance services. While specific market figures are unavailable, estimations based on comparable European markets and an assumed CAGR of **34.51%** project a market size of **6.66 billion** in **2025**. This encompasses both life and non-life insurance. The life insurance segment, more mature, anticipates steady growth driven by demand for retirement and savings solutions. The non-life sector, however, shows potential for more significant expansion due to increasing awareness of property and casualty risks, complemented by innovative products like cyber and parametric insurance addressing climate-specific risks prevalent in Greece. Regulatory shifts and intensified competition from domestic and international entities will critically influence the industry's path through the forecast period (2025-2033).

Greece Life and Non-Life Insurance Industry Market Size (In Billion)

The forecast period (2025-2033) presents significant opportunities and challenges. A projected CAGR of **34.51%** indicates robust expansion, influenced by macroeconomic indicators like GDP growth, inflation, and interest rates. Technological advancements, particularly in Insurtech, possess the potential to disrupt established business models and enhance operational efficiency. Prioritizing customer experience, personalized offerings, and proactive risk management will be crucial for market leadership. Increased insurance product penetration, especially in under-served demographics, represents substantial untapped growth potential. The growing integration of digital technologies promises streamlined claims processing and superior customer service, fostering enhanced customer satisfaction and loyalty.

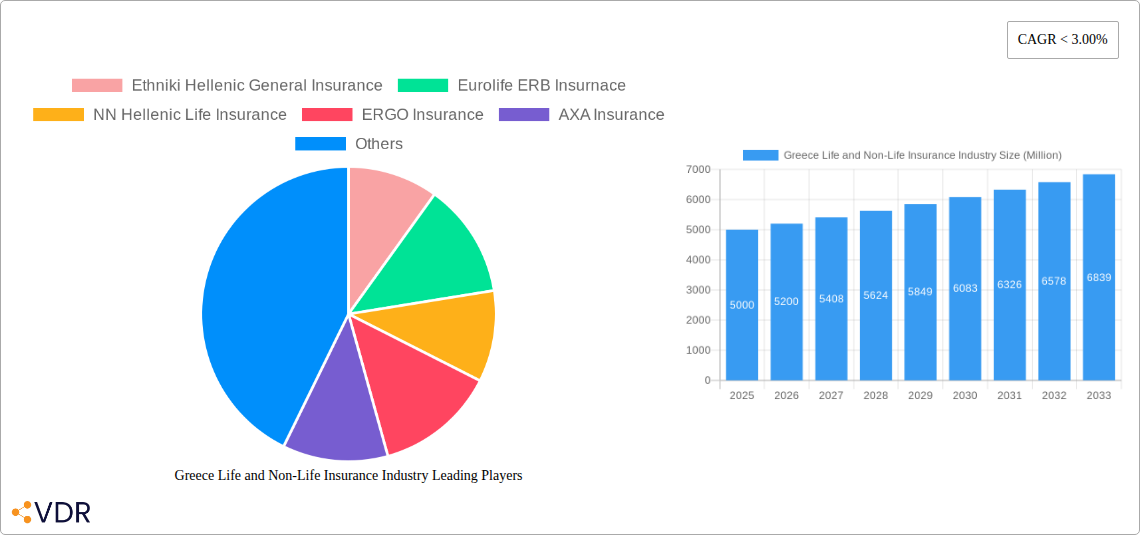

Greece Life and Non-Life Insurance Industry Company Market Share

Greece Life and Non-Life Insurance Industry Market Report: 2019-2033

This comprehensive report provides an in-depth analysis of the Greek life and non-life insurance industry, covering market dynamics, growth trends, competitive landscape, and future outlook. The study period spans from 2019 to 2033, with 2025 serving as the base and estimated year. The report offers invaluable insights for industry professionals, investors, and strategic decision-makers seeking to navigate this dynamic market.

Keywords: Greece insurance market, life insurance Greece, non-life insurance Greece, Greek insurance industry analysis, insurance market size Greece, insurance sector Greece, Ethniki Insurance, AXA Insurance Greece, Generali Greece, insurance market trends Greece, insurance regulations Greece, mergers and acquisitions Greece insurance.

Greece Life and Non-Life Insurance Industry Market Dynamics & Structure

The Greek insurance market, segmented into life and non-life, exhibits a moderately concentrated structure. Major players like Ethniki Hellenic General Insurance, Eurolife ERB Insurance, NN Hellenic Life Insurance, ERGO Insurance, AXA Insurance, European Reliance General, MetLife, General Hellas, Allianz Hellas, and Griupama Phoenix Hellenic Insurance (list not exhaustive) compete for market share. Technological innovation, while present, faces barriers including legacy systems and data security concerns. The regulatory framework, influenced by EU directives, is undergoing continuous evolution, impacting operational efficiency and compliance costs. Market dynamics are shaped by competitive product substitutes (e.g., microinsurance), shifting end-user demographics (aging population), and a growing appetite for M&A activity, as exemplified by recent high-profile transactions.

- Market Concentration: Moderately concentrated, with top 5 players holding xx% market share (2024).

- Technological Innovation: Adoption of Insurtech solutions is gradual, hindered by legacy IT infrastructure and data privacy regulations.

- Regulatory Framework: Evolving regulatory landscape, aligned with EU standards, impacting solvency and compliance requirements.

- Competitive Substitutes: Emergence of microinsurance and alternative risk management solutions creates competitive pressure.

- End-User Demographics: Aging population presents both opportunities and challenges for life insurers.

- M&A Trends: Significant M&A activity observed recently, driven by consolidation and foreign investment. Deal volume in 2024 estimated at xx million EUR.

Greece Life and Non-Life Insurance Industry Growth Trends & Insights

The Greek insurance market demonstrated a fluctuating growth trajectory during the historical period (2019-2024), influenced by macroeconomic factors and regulatory changes. The market size in 2024 is estimated at xx million EUR. The CAGR for the historical period is xx%. The adoption rate of new insurance products varies across segments, with digital channels gaining traction. Technological disruptions, such as AI-powered underwriting and claims processing, are gradually impacting operational efficiency. Consumer behavior is evolving, with increased demand for personalized products and digital interactions. The forecast period (2025-2033) projects a CAGR of xx%, driven by increasing insurance awareness and economic recovery. Market penetration is expected to reach xx% by 2033.

Dominant Regions, Countries, or Segments in Greece Life and Non-Life Insurance Industry

The Attica region (including Athens) dominates the Greek insurance market due to its high population density and economic activity. Other significant regions include Thessaloniki and other major urban centers. The non-life insurance segment exhibits higher growth potential compared to the life insurance segment, driven by rising demand for motor and property insurance.

- Key Drivers:

- High population density in urban areas.

- Developed infrastructure in major cities.

- Relatively higher disposable incomes.

- Government initiatives promoting insurance penetration.

Greece Life and Non-Life Insurance Industry Product Landscape

Product innovation focuses on bundled offerings, tailored insurance packages, and the increasing use of digital platforms for distribution and customer service. Telematics-based motor insurance and health insurance products incorporating wellness features exemplify technological advancements leading to enhanced product offerings and customer engagement. Unique selling propositions hinge on competitive pricing, personalized services, and digital convenience.

Key Drivers, Barriers & Challenges in Greece Life and Non-Life Insurance Industry

Key Drivers: Increasing disposable income, rising awareness of insurance benefits, and government initiatives supporting insurance penetration.

Key Challenges: Economic instability, high levels of non-performing loans (NPLs), and regulatory hurdles create constraints on industry growth. Increased competition from international players and pressure on pricing margins poses further challenges.

Emerging Opportunities in Greece Life and Non-Life Insurance Industry

Untapped markets in rural areas, demand for specialized insurance products, and the potential for partnerships with fintech companies represent significant opportunities. Microinsurance solutions could target underserved segments of the population, while data analytics can drive more personalized and efficient service delivery.

Growth Accelerators in the Greece Life and Non-Life Insurance Industry Industry

Technological advancements, such as AI and blockchain, are poised to enhance efficiency and customer experience. Strategic partnerships with fintech companies, expanding into untapped markets (e.g., rural areas), and developing innovative product offerings will accelerate industry growth.

Key Players Shaping the Greece Life and Non-Life Insurance Market

- Ethniki Hellenic General Insurance

- Eurolife ERB Insurance

- NN Hellenic Life Insurance

- ERGO Insurance

- AXA Insurance

- European Reliance General

- MetLife

- General Hellas

- Allianz Hellas

- Griupama Phoenix Hellenic Insurance

Notable Milestones in Greece Life and Non-Life Insurance Industry Sector

- 2020: Generali acquires AXA's Greek operations.

- 2021: CVC Capital acquires 90.01% of Ethniki Insurance from NBG.

In-Depth Greece Life and Non-Life Insurance Industry Market Outlook

The Greek insurance market is projected to experience steady growth over the forecast period, driven by economic recovery, increased insurance awareness, and technological advancements. Strategic opportunities exist for companies to capitalize on evolving consumer preferences and expand into underserved market segments. The focus on digital transformation and innovative product offerings will be crucial for maintaining competitiveness and achieving long-term growth.

Greece Life and Non-Life Insurance Industry Segmentation

-

1. Type

-

1.1. Life Insurances

- 1.1.1. Individual

- 1.1.2. Group

-

1.2. Non-Life Insurances

- 1.2.1. Home

- 1.2.2. Motor

- 1.2.3. Other Non-Life Insurances

-

1.1. Life Insurances

-

2. Distribution Channel

- 2.1. Direct

- 2.2. Agency

- 2.3. Banks

- 2.4. Other Distribution Channels

Greece Life and Non-Life Insurance Industry Segmentation By Geography

- 1. Greece

Greece Life and Non-Life Insurance Industry Regional Market Share

Geographic Coverage of Greece Life and Non-Life Insurance Industry

Greece Life and Non-Life Insurance Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 34.51% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Life Insurances

- 5.1.1.1. Individual

- 5.1.1.2. Group

- 5.1.2. Non-Life Insurances

- 5.1.2.1. Home

- 5.1.2.2. Motor

- 5.1.2.3. Other Non-Life Insurances

- 5.1.1. Life Insurances

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Direct

- 5.2.2. Agency

- 5.2.3. Banks

- 5.2.4. Other Distribution Channels

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Greece

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Greece Life and Non-Life Insurance Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Life Insurances

- 6.1.1.1. Individual

- 6.1.1.2. Group

- 6.1.2. Non-Life Insurances

- 6.1.2.1. Home

- 6.1.2.2. Motor

- 6.1.2.3. Other Non-Life Insurances

- 6.1.1. Life Insurances

- 6.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.2.1. Direct

- 6.2.2. Agency

- 6.2.3. Banks

- 6.2.4. Other Distribution Channels

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Ethniki Hellenic General Insurance

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Eurolife ERB Insurnace

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 NN Hellenic Life Insurance

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 ERGO Insurance

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 AXA Insurance

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 European Relaince General

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 MetLife

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 General Hellas

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Allianz Hellas

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Griupama Phoenix Hellenic Insurance*List Not Exhaustive

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Ethniki Hellenic General Insurance

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Greece Life and Non-Life Insurance Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Greece Life and Non-Life Insurance Industry Share (%) by Company 2025

List of Tables

- Table 1: Greece Life and Non-Life Insurance Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 2: Greece Life and Non-Life Insurance Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 3: Greece Life and Non-Life Insurance Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Greece Life and Non-Life Insurance Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 5: Greece Life and Non-Life Insurance Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 6: Greece Life and Non-Life Insurance Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Greece Life and Non-Life Insurance Industry?

The projected CAGR is approximately 34.51%.

2. Which companies are prominent players in the Greece Life and Non-Life Insurance Industry?

Key companies in the market include Ethniki Hellenic General Insurance, Eurolife ERB Insurnace, NN Hellenic Life Insurance, ERGO Insurance, AXA Insurance, European Relaince General, MetLife, General Hellas, Allianz Hellas, Griupama Phoenix Hellenic Insurance*List Not Exhaustive.

3. What are the main segments of the Greece Life and Non-Life Insurance Industry?

The market segments include Type, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 6.66 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

Penetration Ratio of Insurance Premium and their Investments to GDP Increased Greece Life & Non-Life Insurance Industry Size.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

In 2021, Greek Insurance Conglomerate Ethniki Sold to Private Fund. Through its subsidiaries Garanta and Ethniki Asfalistiki Cyprus, it has a significant and dynamic presence in Romania and Cyprus, respectively. Its growth has attracted the interest of several foreign funds recently. In a statement, CVC Capital announced that it has entered into a definitive agreement to acquire 90.01% of Ethniki Insurance from NBG.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Greece Life and Non-Life Insurance Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Greece Life and Non-Life Insurance Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Greece Life and Non-Life Insurance Industry?

To stay informed about further developments, trends, and reports in the Greece Life and Non-Life Insurance Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence