Key Insights

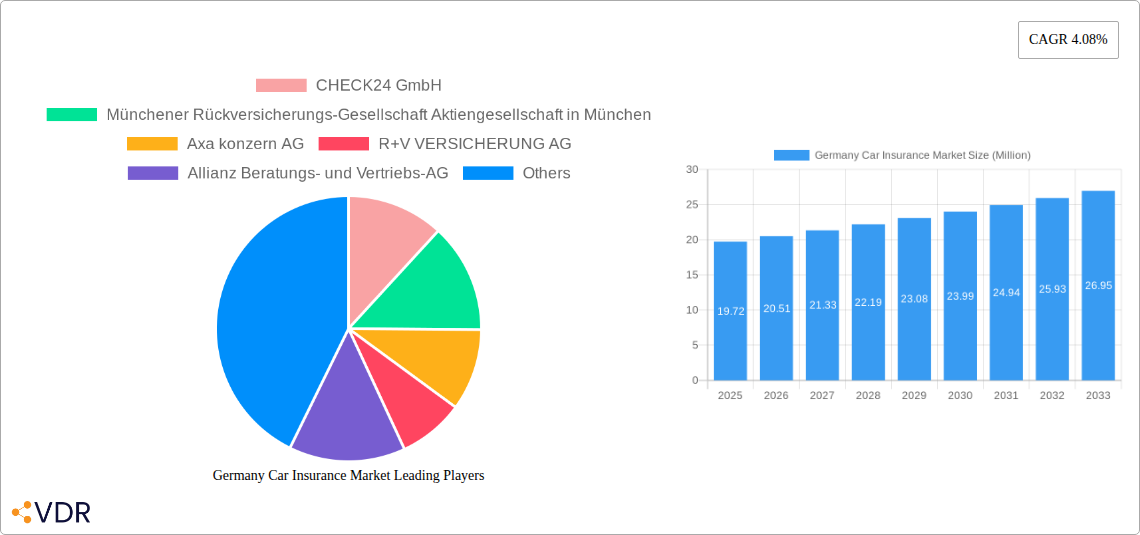

The German car insurance market is projected to reach a substantial size, estimated at €19.72 million in its base year of 2025, reflecting its maturity and ongoing significance within the broader European automotive and insurance sectors. With a projected Compound Annual Growth Rate (CAGR) of 4.08% from 2025 to 2033, the market demonstrates robust expansion driven by several key factors. The increasing adoption of electric vehicles (EVs) and advanced driver-assistance systems (ADAS) are significant growth catalysts, necessitating specialized coverage and potentially higher premiums. Furthermore, evolving consumer preferences towards personalized and digital insurance solutions, facilitated by online distribution channels, are reshaping how policies are purchased and managed. Economic stability, coupled with a high car ownership rate in Germany, underpins sustained demand for mandatory third-party liability coverage, while optional comprehensive and collision packages see uptake driven by a desire for greater protection for increasingly sophisticated and valuable vehicles.

Germany Car Insurance Market Market Size (In Million)

Despite its strong growth trajectory, the German car insurance market faces certain restraints. Intense competition among established players and the emergence of InsurTech startups are creating pricing pressures and demanding greater innovation in product offerings and customer service. Regulatory changes, particularly those concerning data privacy and consumer protection, can also influence operational costs and strategic approaches. The market is characterized by diverse distribution channels, including direct sales, individual agents, brokers, banks, and a rapidly growing online segment, each catering to different customer segments and preferences. Leading companies such as Allianz, Münchener Rück, and AXA are actively navigating these dynamics, investing in digital transformation and exploring new product lines to maintain their market positions. The focus on customer retention and acquisition through tailored policies and competitive pricing will be crucial for success in this evolving landscape.

Germany Car Insurance Market Company Market Share

Germany Car Insurance Market Report: Comprehensive Analysis and Future Outlook (2019-2033)

This in-depth report provides a strategic overview of the Germany Car Insurance Market, offering critical insights into its current dynamics, growth trajectories, and future potential. With a focus on both parent and child markets, this analysis is indispensable for insurers, reinsurers, brokers, technology providers, and financial institutions seeking to navigate the evolving landscape of automotive insurance in Europe's largest economy. Utilizing high-traffic keywords and a structured format, this report is optimized for maximum search engine visibility and delivers actionable intelligence for industry professionals. The study covers the historical period from 2019 to 2024, with the base and estimated year set at 2025 and a comprehensive forecast period extending from 2025 to 2033. All monetary values are presented in Million units.

Germany Car Insurance Market Market Dynamics & Structure

The Germany Car Insurance Market exhibits a moderately consolidated structure, with a few dominant players holding significant market share, yet offering ample room for niche players and digital disruptors. Technological innovation is a key driver, with advancements in telematics, AI-powered claims processing, and online comparison platforms reshaping customer interactions and operational efficiencies. Regulatory frameworks, largely influenced by the European Union's Solvency II directive and national consumer protection laws, ensure a stable yet competitive environment. Competitive product substitutes are emerging, including usage-based insurance (UBI) and subscription-based car ownership models that bundle insurance. End-user demographics reveal a growing demand for personalized, flexible, and digitally accessible insurance solutions, particularly among younger, tech-savvy consumers. Mergers and acquisitions (M&A) trends are observed, albeit at a measured pace, as larger entities seek to consolidate market presence or acquire innovative technologies.

- Market Concentration: Dominated by established insurers, with a growing presence of InsurTech startups.

- Technological Innovation Drivers: Telematics, AI, IoT, and Big Data analytics are transforming underwriting, claims, and customer experience.

- Regulatory Frameworks: Strict compliance with EU directives and national consumer protection laws ensures market stability.

- Competitive Product Substitutes: Usage-Based Insurance (UBI), pay-per-mile models, and integrated mobility solutions.

- End-User Demographics: Increasing demand for digital channels, personalized coverage, and transparent pricing, particularly from millennials and Gen Z.

- M&A Trends: Strategic acquisitions for technology integration and market expansion.

Germany Car Insurance Market Growth Trends & Insights

The Germany Car Insurance Market is poised for robust growth, driven by increasing vehicle parc, evolving consumer preferences, and technological advancements. The market size is projected to expand significantly from its current valuation, with a projected Compound Annual Growth Rate (CAGR) of approximately 3.5% between 2025 and 2033. Adoption rates for digital insurance solutions are rapidly increasing, as consumers seek greater convenience and transparency in policy selection and management. Technological disruptions, such as the integration of advanced driver-assistance systems (ADAS) and the growing prevalence of electric vehicles (EVs), are creating new underwriting challenges and opportunities, demanding innovative risk assessment and pricing models. Consumer behavior shifts are evident, with a move away from traditional, rigid insurance products towards more flexible, modular, and needs-based coverage options. The market penetration of comprehensive and collision coverage is expected to rise as consumer awareness of the benefits of broader protection increases, especially for newer and higher-value vehicles. The increasing use of telematics devices, both factory-installed and aftermarket, is facilitating the growth of UBI policies, allowing for personalized premiums based on actual driving behavior. This trend is further fueled by a growing consumer demand for fair pricing and the opportunity to reduce insurance costs through safe driving practices. Furthermore, the digitalization of the sales process, including online comparison portals and direct-to-consumer offerings, is enhancing accessibility and driving competitive pricing. The expansion of car-sharing services and flexible car subscription models also presents a new paradigm for insurance, with a greater emphasis on short-term, adaptable policies. The ongoing focus on data analytics and AI by leading insurers allows for more precise risk segmentation, leading to more accurate pricing and tailored product development. This data-driven approach is crucial for anticipating future market trends and responding proactively to changing customer needs. The market is also witnessing a trend towards bundled insurance offerings, often in collaboration with automotive manufacturers and mobility service providers, providing a holistic solution for vehicle ownership. The increasing affordability of comprehensive insurance policies, coupled with a rising disposable income in certain segments of the German population, is also contributing to higher adoption rates.

Dominant Regions, Countries, or Segments in Germany Car Insurance Market

The Germany Car Insurance Market is characterized by regional variations in demand and penetration, with several key segments driving overall growth. Personal Vehicles represent the largest application segment, accounting for a substantial portion of the total market share, reflecting the high rate of private car ownership in Germany. Within this segment, Collision/Comprehensive/Other Optional Coverage is experiencing accelerated growth as consumers, particularly those with newer or higher-value vehicles, increasingly opt for broader protection beyond mandatory third-party liability. This surge is attributed to rising awareness of repair costs and the desire for financial security against a wider range of risks, including theft and vandalism. The Online distribution channel is rapidly gaining prominence, outpacing traditional methods like individual agents and brokers in terms of new policy acquisition growth. This dominance is fueled by the convenience, transparency, and competitive pricing offered by online comparison platforms and direct insurer websites. Consumers are increasingly comfortable researching, comparing, and purchasing insurance policies digitally, leveraging readily available information and user reviews.

- Dominant Application Segment: Personal Vehicles, driven by high private car ownership and increasing demand for comprehensive protection.

- Growth Segment within Coverage: Collision/Comprehensive/Other Optional Coverage, as consumers prioritize broader financial security for their vehicles.

- Leading Distribution Channel: Online, due to its convenience, transparency, competitive pricing, and ease of comparison.

- Key Drivers for Online Dominance: Digital savviness of consumers, accessibility of comparison portals, and direct-to-consumer models.

- Regional Influence: Major urban centers and densely populated areas tend to exhibit higher adoption rates for comprehensive and online insurance solutions due to greater vehicle density and consumer demand for efficient services.

- Economic Policies: Favorable economic conditions and consumer purchasing power in Germany directly correlate with higher demand for optional insurance coverages.

- Infrastructure: A well-developed road network and high vehicle utilization in Germany naturally support a robust car insurance market.

Germany Car Insurance Market Product Landscape

The Germany Car Insurance Market is witnessing significant product innovation focused on customization and digital integration. Insurers are moving beyond standardized policies to offer modular coverage options that allow consumers to tailor their policies to specific needs, such as adding roadside assistance, breakdown cover, or protection for electronic components in electric vehicles. The performance metrics are increasingly being evaluated by customer satisfaction scores, claims processing times, and the adoption rate of digital self-service tools. Unique selling propositions are emerging around flexible payment plans, pay-as-you-drive options, and integrated telematics features that reward safe driving. Technological advancements are enabling real-time risk assessment and personalized premium adjustments, making policies more dynamic and reflective of actual usage and driving behavior.

Key Drivers, Barriers & Challenges in Germany Car Insurance Market

Key Drivers:

- Rising Vehicle Parc: Continued growth in the number of registered vehicles, particularly electric and hybrid models, fuels demand for insurance.

- Technological Advancements: Telematics, AI, and data analytics enable personalized pricing, improved risk assessment, and efficient claims handling, driving innovation.

- Consumer Demand for Digitalization: Growing preference for online comparison, purchasing, and self-service policy management enhances accessibility and competition.

- Evolving Mobility Concepts: Car sharing, subscription services, and autonomous driving technologies necessitate new insurance solutions.

Barriers & Challenges:

- Intense Competition: The market is highly competitive, with price wars and increasing pressure on profit margins.

- Regulatory Compliance: Navigating complex and evolving regulatory landscapes, including data privacy laws (GDPR), adds operational burden and cost.

- Customer Acquisition Costs: High marketing expenses and customer acquisition costs for digital channels present a significant challenge.

- Economic Uncertainty: Fluctuations in the German and global economies can impact consumer spending on discretionary insurance products.

Emerging Opportunities in Germany Car Insurance Market

Emerging opportunities in the Germany Car Insurance Market lie in leveraging data analytics for hyper-personalized products, especially for the burgeoning electric vehicle (EV) segment. The increasing adoption of autonomous driving features presents a complex yet lucrative area for specialized coverage. Furthermore, partnerships with mobility service providers and manufacturers for integrated insurance offerings within broader vehicle ecosystems represent significant untapped potential. The demand for usage-based insurance (UBI) is expected to grow, offering consumers cost savings through safe driving, and providing insurers with richer data for risk management.

Growth Accelerators in the Germany Car Insurance Market Industry

Several catalysts are propelling long-term growth in the Germany Car Insurance Market. Technological breakthroughs in telematics and AI are enabling more sophisticated underwriting and claims processing, leading to increased efficiency and customer satisfaction. Strategic partnerships between insurers, technology providers, and automotive manufacturers are creating innovative bundled offerings and expanding market reach. The ongoing expansion of online distribution channels and the development of user-friendly digital platforms are making insurance more accessible and appealing to a wider demographic.

Key Players Shaping the Germany Car Insurance Market Market

- CHECK24 GmbH

- Münchener Rückversicherungs-Gesellschaft Aktiengesellschaft in München

- Axa konzern AG

- R+V VERSICHERUNG AG

- Allianz Beratungs- und Vertriebs-AG

- VHV Vereinigte Hannoversche Versicherung a G

- Debeka Lebensversicherungsverein auf Gegenseitigkeit Sitz Koblenz am Rhein

- GOTHAER Versicherungsbank VVaG

- Versicherungskammer Bayern Versicherungsanstalt des öffentlichen Rechts

- SIGNAL IDUNA Lebensversicherung a G

Notable Milestones in Germany Car Insurance Market Sector

- July 2023: Wrisk, an intermediary insurance provider, entered into a partnership with Mobilize Financial Services, offering customers a fully flexible car insurance experience with a genuine monthly rolling subscription policy aligned to car subscription contract terms.

- January 2023: Signal Iduna, Germany's leading car insurance company, partnered with Google Cloud to accelerate the development of cloud-based, customer-oriented insurance products and services.

In-Depth Germany Car Insurance Market Market Outlook

The Germany Car Insurance Market outlook is characterized by sustained growth and transformative innovation. Key accelerators include the continued digitalization of services, the integration of advanced telematics for usage-based insurance, and the development of tailored solutions for electric and connected vehicles. Strategic alliances and a focus on customer-centric product development will be crucial for market players to capture future opportunities. The market's trajectory points towards greater personalization, seamless digital experiences, and a more dynamic approach to risk management, ensuring a robust and evolving landscape for years to come.

Germany Car Insurance Market Segmentation

-

1. Coverage

- 1.1. Third-Party Liability Coverage

- 1.2. Collision/Comprehensive/Other Optional Coverage

-

2. Application

- 2.1. Personal Vehicles

- 2.2. Commercial Vehicles

-

3. Distribution Channel

- 3.1. Direct Sales

- 3.2. Individual Agents

- 3.3. Brokers

- 3.4. Banks

- 3.5. Online

- 3.6. Other Distribution Channels

Germany Car Insurance Market Segmentation By Geography

- 1. Germany

Germany Car Insurance Market Regional Market Share

Geographic Coverage of Germany Car Insurance Market

Germany Car Insurance Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.08% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Coverage

- 5.1.1. Third-Party Liability Coverage

- 5.1.2. Collision/Comprehensive/Other Optional Coverage

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Personal Vehicles

- 5.2.2. Commercial Vehicles

- 5.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.3.1. Direct Sales

- 5.3.2. Individual Agents

- 5.3.3. Brokers

- 5.3.4. Banks

- 5.3.5. Online

- 5.3.6. Other Distribution Channels

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Germany

- 5.1. Market Analysis, Insights and Forecast - by Coverage

- 6. Germany Car Insurance Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Coverage

- 6.1.1. Third-Party Liability Coverage

- 6.1.2. Collision/Comprehensive/Other Optional Coverage

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Personal Vehicles

- 6.2.2. Commercial Vehicles

- 6.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.3.1. Direct Sales

- 6.3.2. Individual Agents

- 6.3.3. Brokers

- 6.3.4. Banks

- 6.3.5. Online

- 6.3.6. Other Distribution Channels

- 6.1. Market Analysis, Insights and Forecast - by Coverage

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 CHECK24 GmbH

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Münchener Rückversicherungs-Gesellschaft Aktiengesellschaft in München

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Axa konzern AG

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 R+V VERSICHERUNG AG

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Allianz Beratungs- und Vertriebs-AG

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 VHV Vereinigte Hannoversche Versicherung a G

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Debeka Lebensversicherungsverein auf Gegenseitigkeit Sitz Koblenz am Rhein

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 GOTHAER Versicherungsbank VVaG* *List Not Exhaustive

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Versicherungskammer Bayern Versicherungsanstalt des öffentlichen Rechts

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 SIGNAL IDUNA Lebensversicherung a G

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 CHECK24 GmbH

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Germany Car Insurance Market Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Germany Car Insurance Market Share (%) by Company 2025

List of Tables

- Table 1: Germany Car Insurance Market Revenue Million Forecast, by Coverage 2020 & 2033

- Table 2: Germany Car Insurance Market Revenue Million Forecast, by Application 2020 & 2033

- Table 3: Germany Car Insurance Market Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 4: Germany Car Insurance Market Revenue Million Forecast, by Region 2020 & 2033

- Table 5: Germany Car Insurance Market Revenue Million Forecast, by Coverage 2020 & 2033

- Table 6: Germany Car Insurance Market Revenue Million Forecast, by Application 2020 & 2033

- Table 7: Germany Car Insurance Market Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 8: Germany Car Insurance Market Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Germany Car Insurance Market?

The projected CAGR is approximately 4.08%.

2. Which companies are prominent players in the Germany Car Insurance Market?

Key companies in the market include CHECK24 GmbH, Münchener Rückversicherungs-Gesellschaft Aktiengesellschaft in München, Axa konzern AG, R+V VERSICHERUNG AG, Allianz Beratungs- und Vertriebs-AG, VHV Vereinigte Hannoversche Versicherung a G, Debeka Lebensversicherungsverein auf Gegenseitigkeit Sitz Koblenz am Rhein, GOTHAER Versicherungsbank VVaG* *List Not Exhaustive, Versicherungskammer Bayern Versicherungsanstalt des öffentlichen Rechts, SIGNAL IDUNA Lebensversicherung a G.

3. What are the main segments of the Germany Car Insurance Market?

The market segments include Coverage , Application , Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 19.72 Million as of 2022.

5. What are some drivers contributing to market growth?

Rising Sales of Cars in Germany Drives The Market; Increase in Road Traffic Accidents Drives The Market.

6. What are the notable trends driving market growth?

Increasing Focus Towards Digitalization In Car Insurance.

7. Are there any restraints impacting market growth?

Increase in Cost of Claims Made; Increase in False Claims and Scams.

8. Can you provide examples of recent developments in the market?

July 2023: Wrisk, an intermediary insurance provider, entered into a partnership with Mobilize Financial Services, which provides customers with a fully flexible car insurance experience, offering a genuine monthly rolling subscription policy that is aligned to the car subscription contract term.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Germany Car Insurance Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Germany Car Insurance Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Germany Car Insurance Market?

To stay informed about further developments, trends, and reports in the Germany Car Insurance Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence