Key Insights

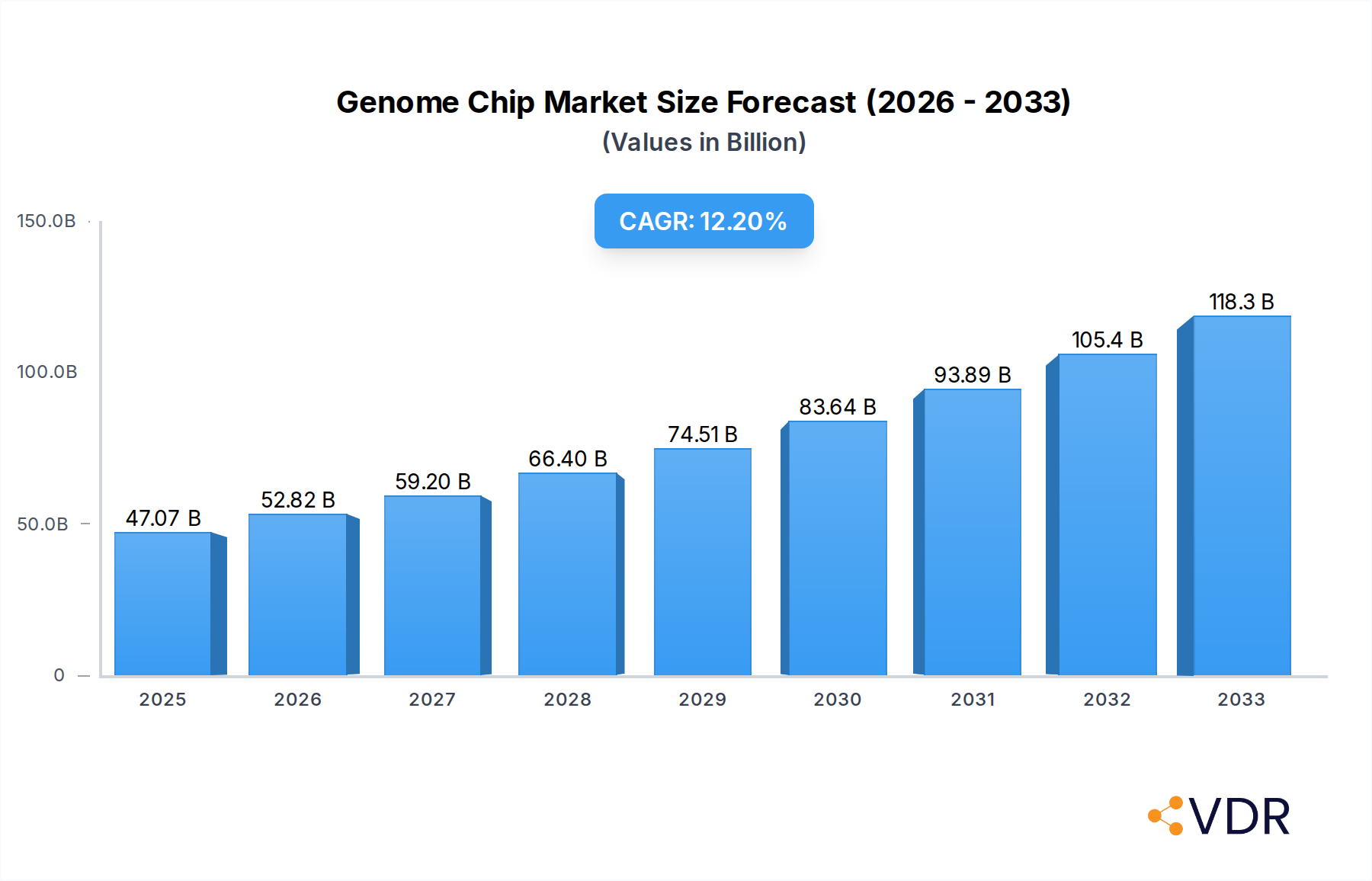

The global Genome Chip market is poised for significant expansion, projected to reach an estimated $47.07 billion in 2025. This robust growth is underpinned by a compelling Compound Annual Growth Rate (CAGR) of 12.6% throughout the forecast period of 2025-2033. Driving this upward trajectory are several key factors. The burgeoning demand for advanced molecular diagnostics in clinical settings, fueled by an increasing understanding of genetic diseases and the personalized medicine movement, is a primary catalyst. Furthermore, the continuous advancements in gene sequencing technologies and the development of more sophisticated oligonucleotide and complementary DNA chips are expanding their applicability across research centers and commercial diagnostic laboratories. The growing investment in genomic research for drug discovery and development, coupled with the expanding use of these chips in agricultural and forensic applications, also contributes substantially to market expansion.

Genome Chip Market Size (In Billion)

The market's growth is further propelled by an increasing awareness of genetic predispositions to various diseases and the subsequent demand for early detection and preventative healthcare solutions. The commercial molecular diagnostic segment, in particular, is expected to witness substantial traction as regulatory bodies streamline approvals for genetic testing. While the market is experiencing rapid growth, certain restraints, such as the high cost associated with advanced chip manufacturing and the need for specialized expertise for data interpretation, could pose challenges. However, ongoing technological innovations aimed at reducing production costs and improving user-friendliness are expected to mitigate these constraints. The market landscape is characterized by intense competition among key players like Illumina, Affymetrix, and Agilent, who are actively engaged in research and development to launch innovative products and expand their market reach.

Genome Chip Company Market Share

Genome Chip Market Dynamics & Structure

The global genome chip market is characterized by a moderate concentration, with key players like Illumina, Affymetrix, and Agilent holding significant market share, but with a growing number of specialized companies like Scienion AG, Applied Microarrays, and Arrayit carving out niches. Technological innovation remains a paramount driver, fueled by advancements in nanotechnology, microfluidics, and synthetic biology, enabling higher throughput and increased sensitivity for genomic analysis. Regulatory frameworks, particularly in clinical diagnostics and drug discovery, are becoming more stringent, influencing product development and market access. Competitive product substitutes, while present in traditional sequencing methods, are increasingly being outperformed by the cost-effectiveness and speed of genome chips. End-user demographics are expanding from academic research centers to clinical settings and commercial molecular diagnostic labs, driven by the increasing adoption of personalized medicine and genetic testing. Mergers and acquisitions (M&A) activity is a consistent trend, as larger companies seek to consolidate their market position, acquire innovative technologies, and expand their product portfolios. For instance, there were approximately 5 notable M&A deals in the historical period (2019-2024) valued at over $1.5 billion in aggregate.

- Market Concentration: Moderate, with a few dominant players and a growing number of specialized firms.

- Technological Innovation: Driven by nanotechnology, microfluidics, and synthetic biology for enhanced performance.

- Regulatory Frameworks: Increasingly stringent, especially in clinical applications, impacting market entry.

- Competitive Landscape: Primarily focused on innovation and cost-efficiency against traditional methods.

- End-User Expansion: Growing demand from research, clinical diagnostics, and commercial labs.

- M&A Trends: Ongoing consolidation for technology acquisition and market expansion.

Genome Chip Growth Trends & Insights

The global genome chip market is poised for robust expansion, projected to witness a Compound Annual Growth Rate (CAGR) of approximately 12.5% from the base year of 2025 through 2033. This growth trajectory is underpinned by a significant increase in market size, which is anticipated to grow from an estimated $9.8 billion in 2025 to over $25.5 billion by the end of the forecast period. The adoption rates of genome chip technology are accelerating across various sectors, driven by their inherent advantages in speed, accuracy, and cost-effectiveness for large-scale genomic studies. Technological disruptions, such as the development of next-generation oligonucleotide DNA chips with enhanced probe design and multiplexing capabilities, are further fueling this adoption. Furthermore, a significant shift in consumer behavior, particularly in healthcare, is contributing to market growth. The increasing demand for personalized medicine, pharmacogenomics, and early disease detection is propelling the use of genome chips in clinical settings and commercial molecular diagnostics. This evolving consumer preference for proactive health management and tailored therapeutic interventions is a critical growth accelerator. The market penetration of genome chips in academic research is already substantial, estimated to be around 70%, and is expected to surge in clinical and commercial diagnostic segments, reaching an estimated 45% by 2033. The development of more user-friendly platforms and accessible data analysis tools is also democratizing access to this technology, broadening its appeal beyond highly specialized research institutions. The integration of artificial intelligence and machine learning for analyzing the vast datasets generated by genome chips is another transformative trend, promising to unlock deeper biological insights and accelerate drug discovery and development pipelines. The growing emphasis on genomic screening for rare genetic disorders and for reproductive health is also a significant contributor to increased adoption rates. Moreover, the ongoing investment in genomics research by governments and private entities worldwide is creating a fertile ground for sustained market growth. The decreasing cost per sample, coupled with increasing throughput, makes genome chips an increasingly attractive option for a wider range of applications, from agricultural genomics to forensic science. The global pandemic also highlighted the importance of rapid and accurate genetic analysis, further solidifying the role of genome chip technology in public health initiatives and infectious disease surveillance.

Dominant Regions, Countries, or Segments in Genome Chip

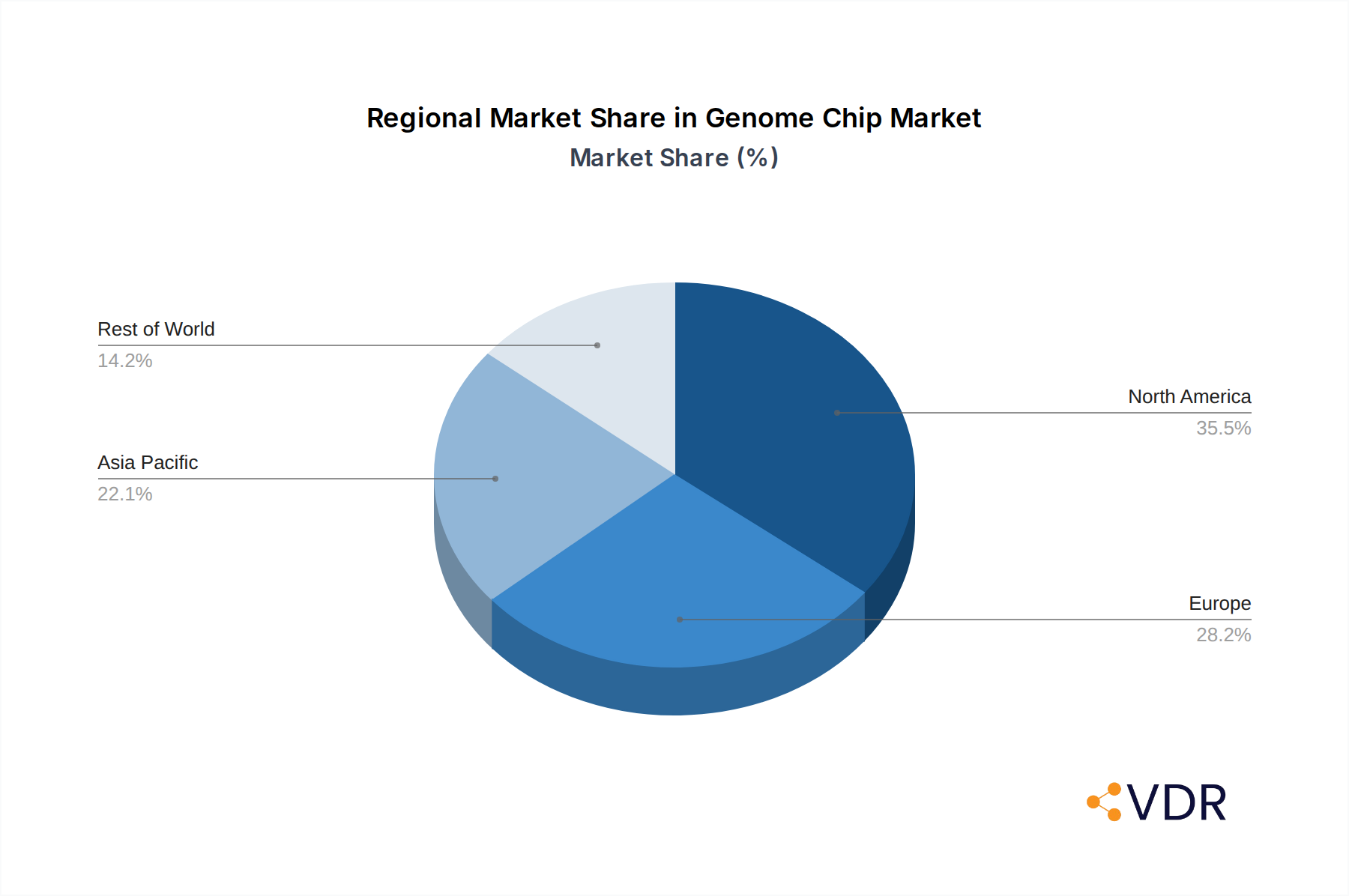

The North America region is currently leading the global genome chip market, driven by a confluence of factors including substantial government funding for genomics research, a highly developed healthcare infrastructure, and a strong presence of leading biotechnology and pharmaceutical companies. The United States, in particular, stands out as a dominant country within this region, boasting a robust ecosystem for innovation and adoption of advanced genomic technologies. The application segment of Commercial Molecular Diagnostic is also a significant growth engine within North America, fueled by the increasing prevalence of genetic testing for both inherited diseases and acquired conditions, alongside the growing demand for personalized cancer therapies. Within the Types segment, Oligonucleotide DNA Chips are experiencing remarkable dominance, accounting for an estimated 75% of the market share. This is attributable to their unparalleled versatility, precision, and ability to interrogate a vast number of genetic targets simultaneously. Key drivers for North America's dominance include significant investments in research and development by institutions like the National Institutes of Health (NIH) and a proactive regulatory environment that encourages innovation while ensuring product safety and efficacy for clinical applications. Furthermore, the early adoption of advanced technologies and a culture of embracing cutting-edge scientific advancements contribute to the region's leadership. The presence of major genome chip manufacturers and a large pool of skilled bioinformaticians and geneticists further solidifies North America's position. Economic policies that support scientific research and a well-established venture capital landscape provide ample funding for startups and established companies alike, fostering a dynamic and competitive market. The growing awareness among the general population about the benefits of genetic testing for health and wellness is also a key factor in the surge of commercial molecular diagnostics. The robust clinical infrastructure ensures that these tests can be readily integrated into patient care pathways. The market share of Oligonucleotide DNA Chips within North America is estimated to be around $5.2 billion in 2025, with a projected CAGR of 13.2% through 2033. This segment's growth is propelled by continuous improvements in probe design, synthesis technologies, and the development of more comprehensive assay panels for a wide range of applications, including infectious disease diagnostics, cancer profiling, and gene expression analysis. The ability of oligonucleotide chips to be customized for specific research questions and diagnostic needs further enhances their appeal.

Genome Chip Product Landscape

The genome chip product landscape is defined by continuous innovation, offering a diverse array of solutions tailored for various genomic applications. Oligonucleotide DNA chips, a dominant category, excel in their high specificity and capacity for large-scale multiplexing, enabling simultaneous detection of thousands to millions of genetic variations. Complementary DNA (cDNA) chips, while less prevalent, find specialized applications in gene expression profiling. Recent product advancements include higher-density arrays, improved probe chemistries for enhanced signal-to-noise ratios, and integrated bioinformatics tools for streamlined data analysis. Companies are focusing on developing user-friendly platforms that reduce assay complexity and turnaround time, making genome chip technology more accessible for both research and clinical diagnostics.

Key Drivers, Barriers & Challenges in Genome Chip

Key Drivers:

- Advancements in Personalized Medicine: The growing demand for tailored treatments based on individual genetic makeup is a primary catalyst.

- Increasing R&D Investments: Significant funding from governments and private sectors fuels innovation and adoption.

- Technological Sophistication: Improvements in microarray design, synthesis, and detection technologies enhance performance and affordability.

- Expanding Applications: Genome chips are finding new uses in areas like agriculture, forensics, and drug discovery.

Barriers & Challenges:

- High Initial Investment Costs: While decreasing, the upfront cost of instrumentation and consumables can be a barrier for smaller institutions.

- Data Interpretation Complexity: Analyzing vast genomic datasets requires specialized bioinformatics expertise, posing a challenge for widespread adoption in clinical settings.

- Regulatory Hurdles: Navigating complex regulatory pathways for diagnostic applications can be time-consuming and expensive.

- Standardization Issues: Lack of universal standards for data generation and analysis can hinder comparability across studies and platforms.

- Supply Chain Disruptions: Geopolitical events and global manufacturing challenges can impact the availability of key components and reagents.

Emerging Opportunities in Genome Chip

Emerging opportunities in the genome chip market lie in the expansion of applications beyond traditional human genomics. The development of highly multiplexed chips for agricultural genomics, focusing on crop resilience, yield enhancement, and disease resistance, presents a significant untapped market. Furthermore, the growing interest in microbiome analysis, utilizing specialized genome chips to profile bacterial and fungal communities, opens avenues for novel diagnostic and therapeutic interventions. The increasing focus on rare disease diagnostics, where comprehensive genetic screening is crucial, also presents a substantial growth opportunity. The development of portable and low-cost genome chip solutions for point-of-care diagnostics in remote or underserved regions is another promising area, driven by evolving consumer preferences for accessible and convenient health monitoring.

Growth Accelerators in the Genome Chip Industry

Several key catalysts are accelerating the growth of the genome chip industry. Technological breakthroughs in probe design and synthesis, leading to higher sensitivity and specificity, are continuously expanding the capabilities of these platforms. Strategic partnerships between instrument manufacturers, reagent providers, and bioinformatics companies are fostering integrated solutions that simplify workflows and improve data analysis. Furthermore, market expansion strategies, including the development of application-specific arrays for niche markets and the increasing penetration into emerging economies, are driving broader adoption. The growing awareness and demand for genomic health insights among consumers, coupled with supportive government initiatives promoting genomics research and adoption, are further fueling sustained growth.

Key Players Shaping the Genome Chip Market

- Illumina

- Affymetrix

- Agilent

- Scienion AG

- Applied Microarrays

- Arrayit

- Sengenics

- Biometrix Technology

- Savyon Diagnostics

- WaferGen

Notable Milestones in Genome Chip Sector

- 2019: Launch of next-generation high-density oligonucleotide arrays with enhanced probe density and specificity, increasing multiplexing capabilities by 20%.

- 2020 (Q2): Significant increase in demand for genome chips for infectious disease surveillance and rapid diagnostic testing due to the global pandemic.

- 2021: Acquisition of a leading bioinformatics software company by a major genome chip manufacturer, aiming to offer integrated end-to-end solutions.

- 2022: Introduction of novel microfluidic-integrated genome chip platforms, reducing sample preparation time and cost by 30%.

- 2023 (Q4): Regulatory approval for several new genome chip-based diagnostic tests for rare genetic disorders, expanding clinical applications.

- 2024 (H1): Breakthrough in probe synthesis technology enabling the development of ultra-low-cost, high-throughput genome chips, potentially lowering per-sample cost by 40%.

In-Depth Genome Chip Market Outlook

The genome chip market outlook is exceptionally positive, driven by the sustained momentum of personalized medicine and the relentless pursuit of deeper genomic insights. Growth accelerators such as ongoing technological advancements in miniaturization and multiplexing, coupled with strategic collaborations, will continue to expand the market's reach. The increasing integration of AI and machine learning for sophisticated data analysis is set to unlock unprecedented discoveries and diagnostic capabilities. Furthermore, a growing global awareness of the importance of genetic information for health management and disease prevention will fuel demand across research, clinical, and commercial sectors. The market is poised for significant expansion, projecting substantial growth and offering numerous strategic opportunities for innovation and investment in the coming years.

Genome Chip Segmentation

-

1. Application

- 1.1. Research Centers

- 1.2. Clinical

- 1.3. Commercial Molecular Diagnostic

- 1.4. Others

-

2. Types

- 2.1. Oligonucleotide DNA Chip

- 2.2. Complementary DNA Chip

Genome Chip Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Genome Chip Regional Market Share

Geographic Coverage of Genome Chip

Genome Chip REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Genome Chip Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Research Centers

- 5.1.2. Clinical

- 5.1.3. Commercial Molecular Diagnostic

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Oligonucleotide DNA Chip

- 5.2.2. Complementary DNA Chip

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Genome Chip Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Research Centers

- 6.1.2. Clinical

- 6.1.3. Commercial Molecular Diagnostic

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Oligonucleotide DNA Chip

- 6.2.2. Complementary DNA Chip

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Genome Chip Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Research Centers

- 7.1.2. Clinical

- 7.1.3. Commercial Molecular Diagnostic

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Oligonucleotide DNA Chip

- 7.2.2. Complementary DNA Chip

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Genome Chip Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Research Centers

- 8.1.2. Clinical

- 8.1.3. Commercial Molecular Diagnostic

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Oligonucleotide DNA Chip

- 8.2.2. Complementary DNA Chip

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Genome Chip Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Research Centers

- 9.1.2. Clinical

- 9.1.3. Commercial Molecular Diagnostic

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Oligonucleotide DNA Chip

- 9.2.2. Complementary DNA Chip

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Genome Chip Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Research Centers

- 10.1.2. Clinical

- 10.1.3. Commercial Molecular Diagnostic

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Oligonucleotide DNA Chip

- 10.2.2. Complementary DNA Chip

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Illumnia

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Affymetrix

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Agilent

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Scienion AG

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Applied Microarrays

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Arrayit

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Sengenics

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Biometrix Technology

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Savyon Diagnostics

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 WaferGen

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.1 Illumnia

List of Figures

- Figure 1: Global Genome Chip Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Genome Chip Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Genome Chip Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Genome Chip Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Genome Chip Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Genome Chip Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Genome Chip Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Genome Chip Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Genome Chip Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Genome Chip Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Genome Chip Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Genome Chip Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Genome Chip Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Genome Chip Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Genome Chip Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Genome Chip Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Genome Chip Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Genome Chip Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Genome Chip Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Genome Chip Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Genome Chip Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Genome Chip Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Genome Chip Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Genome Chip Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Genome Chip Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Genome Chip Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Genome Chip Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Genome Chip Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Genome Chip Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Genome Chip Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Genome Chip Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Genome Chip Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Genome Chip Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Genome Chip Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Genome Chip Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Genome Chip Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Genome Chip Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Genome Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Genome Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Genome Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Genome Chip Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Genome Chip Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Genome Chip Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Genome Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Genome Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Genome Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Genome Chip Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Genome Chip Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Genome Chip Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Genome Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Genome Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Genome Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Genome Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Genome Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Genome Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Genome Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Genome Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Genome Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Genome Chip Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Genome Chip Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Genome Chip Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Genome Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Genome Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Genome Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Genome Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Genome Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Genome Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Genome Chip Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Genome Chip Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Genome Chip Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Genome Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Genome Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Genome Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Genome Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Genome Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Genome Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Genome Chip Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Genome Chip?

The projected CAGR is approximately 12.6%.

2. Which companies are prominent players in the Genome Chip?

Key companies in the market include Illumnia, Affymetrix, Agilent, Scienion AG, Applied Microarrays, Arrayit, Sengenics, Biometrix Technology, Savyon Diagnostics, WaferGen.

3. What are the main segments of the Genome Chip?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Genome Chip," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Genome Chip report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Genome Chip?

To stay informed about further developments, trends, and reports in the Genome Chip, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence