Key Insights

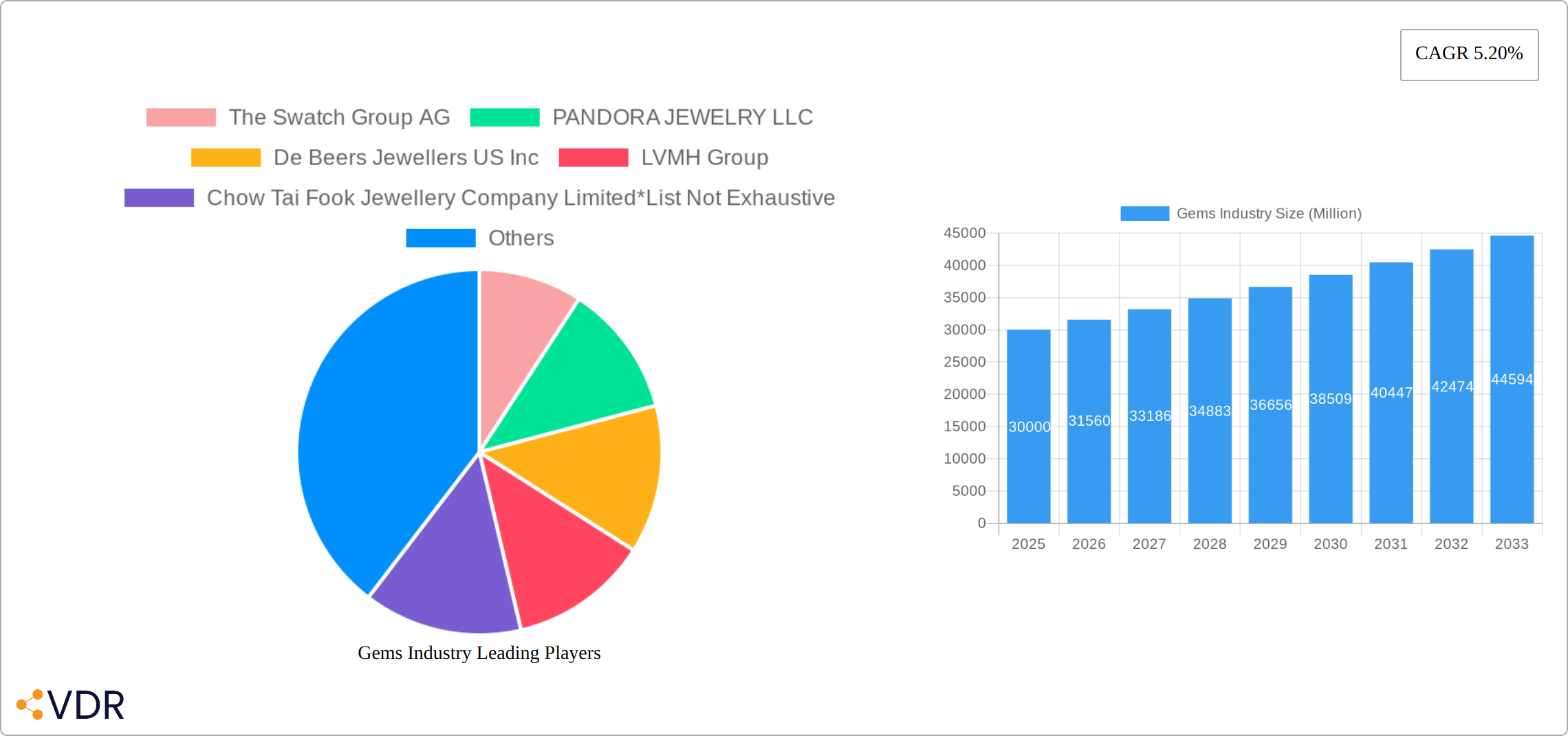

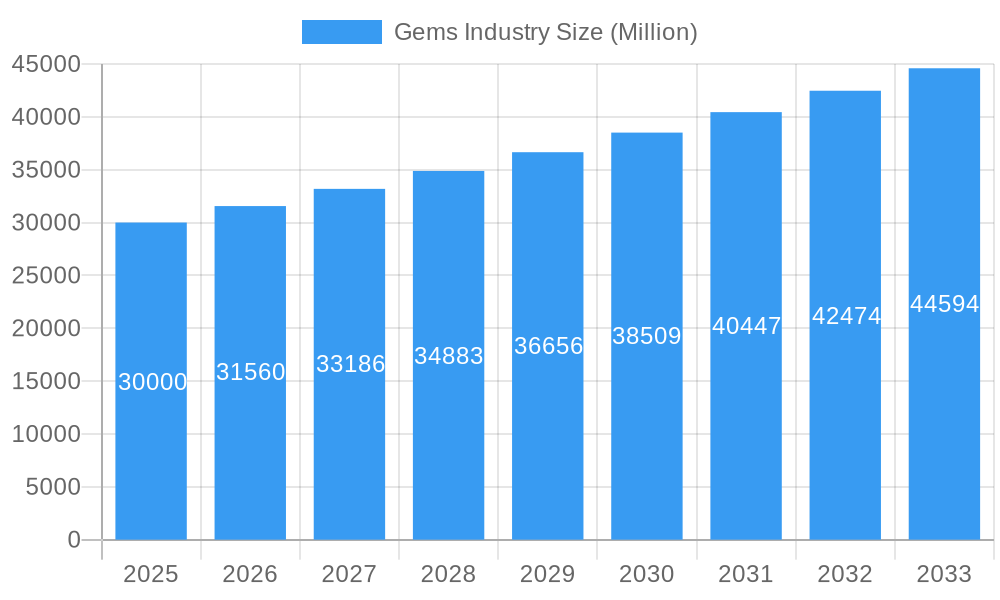

The global gemstone market, valued at approximately $12.7 billion in 2025, is projected for significant expansion, driven by a Compound Annual Growth Rate (CAGR) of 6.3% from 2025 to 2033. Key growth drivers include rising disposable incomes in emerging economies, particularly in the Asia-Pacific region, fueling demand for luxury items. Evolving consumer preferences for personalized and unique jewelry also stimulate design innovation and sales. The burgeoning e-commerce landscape enhances accessibility and choice, further boosting market growth. While supply chain volatility and price fluctuations present challenges, the industry outlook remains robust. Market segmentation by product (rings, necklaces, earrings, bracelets) and distribution channel (online, offline retail) reveals diverse opportunities, with online retail exhibiting substantial expansion due to its convenience and broad reach. Leading players, including The Swatch Group AG, PANDORA, De Beers, LVMH, and Chow Tai Fook, are strategically leveraging brand equity and established networks.

Gems Industry Market Size (In Billion)

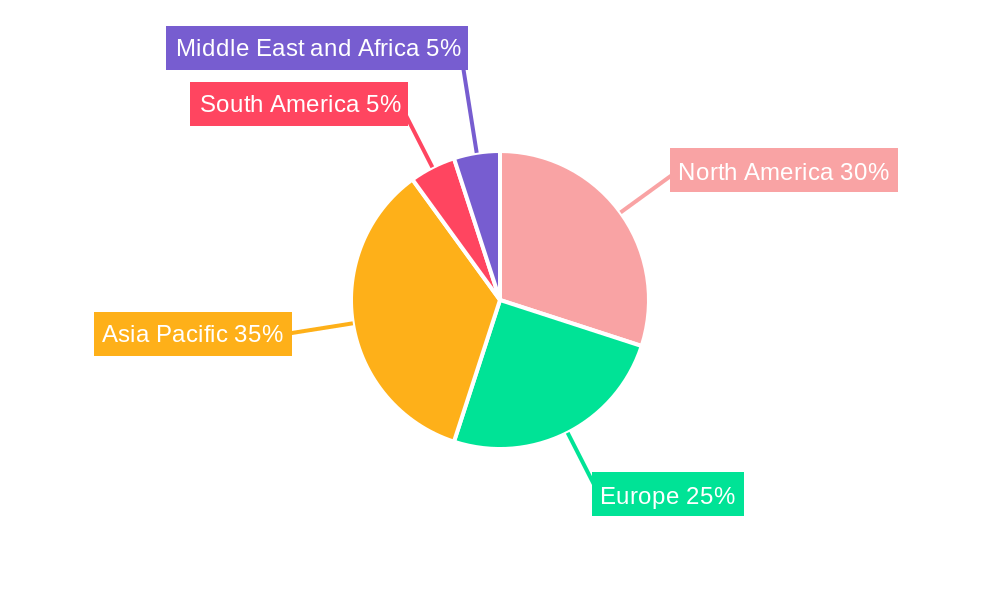

Regional analysis highlights strong growth prospects across diverse markets. North America and Europe will continue to be significant contributors, while the Asia-Pacific region, propelled by a growing middle class and increased consumer spending, is anticipated to experience the most rapid expansion. The increasing adoption of lab-grown diamonds and other gemstones presents both opportunities for innovation in sustainable and affordable jewelry and potential competition for natural gemstones. Strategic alliances, mergers, acquisitions, and product diversification are essential for competitive advantage in this dynamic market. The forecast period of 2025-2033 indicates substantial market value growth, positioning the sector as an attractive investment and expansion opportunity.

Gems Industry Company Market Share

This comprehensive report offers a detailed analysis of the global gemstone market, covering market dynamics, growth trajectories, regional leadership, product segmentation, key stakeholders, and future projections. The study period spans 2019-2033, with a base year of 2025. This report is an essential resource for industry professionals, investors, and stakeholders seeking in-depth insights into this lucrative market. Granular analysis of parent and child markets provides detailed segment-specific information. Market valuations are presented in billions of U.S. dollars.

Gems Industry Market Dynamics & Structure

The global gems industry presents a moderately concentrated market structure, dominated by several key players commanding significant market share. Leading companies such as Swatch Group AG, PANDORA JEWELRY LLC, De Beers Jewellers US Inc, LVMH Group, Chow Tai Fook Jewellery Company Limited, Richemont SA, Swarovski Crystal Online AG, and Signet Jewelers represent a substantial portion of the market. However, a diverse landscape of smaller players and independent jewelers also contribute significantly. Market growth is significantly influenced by technological advancements, particularly in gemstone creation and manufacturing processes. Furthermore, evolving regulatory frameworks emphasizing ethical sourcing and environmental sustainability are increasingly shaping industry practices. The competitive landscape includes the rising challenge of substitute products like lab-grown diamonds and imitation jewelry. The industry caters to a broad spectrum of end-users, ranging from mass-market consumers to high-net-worth individuals seeking luxury items. Mergers and acquisitions (M&A) remain a frequent occurrence, with larger corporations actively pursuing market share expansion and diversification of their product portfolios. The increasing demand for traceability and transparency across the supply chain is also driving significant changes.

- Market Concentration: The top 5 players are estimated to control approximately [Insert Percentage]% of the global market in 2025. This concentration is expected to [Increase/Decrease/Remain Stable] in the coming years.

- Technological Innovation: Substantial investments are being channeled into 3D printing, laser cutting, advanced material science, and other cutting-edge manufacturing techniques, leading to greater efficiency and design possibilities.

- Regulatory Framework: A growing emphasis on ethical sourcing, including conflict-free diamonds and responsible mining practices, exerts considerable influence on supply chains and pricing strategies.

- Competitive Substitutes: Lab-grown diamonds are experiencing robust market share growth, creating both competitive pressure and opportunities for innovation within the natural diamond sector.

- M&A Activity: An average of [Insert Number] M&A deals per year were recorded during the historical period (2019-2024), indicating a dynamic and consolidating market.

- Innovation Barriers: High R&D costs and the requirement for specialized skills present considerable hurdles for smaller players seeking to compete effectively.

- Supply Chain Transparency: Increased consumer demand for transparency and traceability is forcing companies to implement robust tracking and verification systems.

Gems Industry Growth Trends & Insights

The gems industry exhibited a Compound Annual Growth Rate (CAGR) of [Insert Percentage]% during the historical period (2019-2024). This growth trajectory is attributed to several key factors: rising disposable incomes in emerging markets, escalating demand for luxury goods, and evolving consumer preferences towards personalized and sustainable products. Disruptive technological advancements, such as the proliferation of e-commerce and the integration of 3D printing, are reshaping distribution channels and product offerings. A notable shift in consumer behavior towards ethically sourced jewelry is impacting the demand for specific products and brands. The increasing market penetration of lab-grown diamonds presents both opportunities and challenges. The forecast period (2025-2033) anticipates continued growth, driven by increasing consumer demand across both developed and developing economies. By 2033, the global market is projected to reach [Insert Value] million units, with a CAGR of [Insert Percentage]% during the forecast period. The adoption rate of online retail channels is poised for significant expansion, particularly amongst younger demographics. The influence of social media and influencer marketing is also becoming increasingly important.

Dominant Regions, Countries, or Segments in Gems Industry

The Asia-Pacific region, specifically China and India, holds a dominant position in the gems industry, accounting for approximately xx% of the global market in 2025. Strong economic growth, a large consumer base, and cultural significance of jewelry contribute to this dominance. Within the product types, rings and necklaces dominate the market, followed by earrings and bracelets. Offline retail stores continue to be the primary distribution channel, although online sales are rapidly growing.

- Key Drivers in Asia-Pacific: Rising disposable incomes, increasing urbanization, and strong cultural affinity for gold and gemstones.

- Offline Retail Dominance: Established brick-and-mortar stores benefit from the trust and in-person experience they offer.

- Online Retail Growth: E-commerce platforms offer convenience and accessibility, driving increased sales.

- Product Type Dominance: Rings and Necklaces hold the largest market share due to their popularity across various occasions and demographics.

Gems Industry Product Landscape

The gems industry encompasses a diverse range of products, including rings, necklaces, earrings, bracelets, chains, pendants, and numerous other specialized items. Innovation within the sector focuses on enhancing the aesthetic appeal, durability, and ethical credentials of gemstones. Technological progress in gemstone cutting, setting, and manufacturing processes has resulted in improved precision, efficiency, and design flexibility. Unique selling propositions increasingly emphasize ethical sourcing, sustainable practices, and bespoke designs tailored to individual customer preferences. Lab-grown diamonds represent a substantial and rapidly growing segment, providing a compelling alternative to mined diamonds. The rise of personalized jewelry and customized settings is also a noteworthy trend.

Key Drivers, Barriers & Challenges in Gems Industry

Key Drivers:

- Increasing disposable incomes in emerging markets

- Growing demand for luxury goods and personalized jewelry

- Technological advancements in gemstone creation and manufacturing

- Rise of e-commerce and online retail channels

Key Challenges:

- Fluctuations in gemstone prices due to supply chain disruptions

- Ethical sourcing and conflict-free diamond concerns

- Competition from lab-grown diamonds and imitation jewelry

- Regulatory hurdles and compliance costs

The impact of these challenges is estimated to result in a xx% reduction in market growth in 2027.

Emerging Opportunities in Gems Industry

- Expansion into untapped markets in Africa and Latin America

- Growing demand for sustainable and ethically sourced gemstones

- Increasing popularity of personalized and bespoke jewelry

- Integration of technology, such as augmented reality, in the retail experience.

Growth Accelerators in the Gems Industry Industry

Technological advancements, particularly in gemstone creation and personalized design, are accelerating market growth. Strategic partnerships between mining companies, manufacturers, and retailers create efficient supply chains. Market expansion into emerging economies with a high growth potential further fuels industry growth. The focus on sustainable and ethical practices attracts environmentally and socially conscious consumers, positively impacting market demand.

Key Players Shaping the Gems Industry Market

- The Swatch Group AG

- PANDORA JEWELRY LLC

- De Beers Jewellers US Inc

- LVMH Group

- Chow Tai Fook Jewellery Company Limited

- Richemont SA

- Swarovski Crystal Online AG

- Chow Tai Fook Jewelry Company Limited

- Tata Sons Private Ltd

- Signet Jewelers

Notable Milestones in Gems Industry Sector

- September 2022: Tanishq launches "The Chola" collection, inspired by the Chola Dynasty.

- August 2022: Louis Vuitton launches the Empreinte Fine Jewelry collection.

- August 2022: Pandora launches the "Pandora Brilliance" line featuring lab-grown diamonds.

These launches showcase innovation and expanding market segments.

In-Depth Gems Industry Market Outlook

The gems industry is poised for sustained growth, propelled by escalating consumer demand, continuous technological advancements, and expansion into new and emerging markets. Strategic opportunities abound in embracing sustainable practices, catering to the demand for personalized designs, and effectively leveraging digital technologies to enhance the customer experience. The industry's future is defined by innovation, ethical considerations, and a steadfast commitment to meeting the ever-evolving preferences of consumers. The forecast projects robust growth throughout the projected period, with the market size exceeding [Insert Value] million units by 2033. Factors like the growing middle class in developing nations and increasing online sales will continue to drive growth.

Gems Industry Segmentation

-

1. Product Type

- 1.1. Rings

- 1.2. Necklaces

- 1.3. Earrings

- 1.4. Bracelets

- 1.5. Chains and Pendants

- 1.6. Other Product Types

-

2. Distribution Channel

- 2.1. Offline Retail Stores

- 2.2. Online Retail Stores

Gems Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

- 1.4. Rest of North America

-

2. Europe

- 2.1. Spain

- 2.2. United Kingdom

- 2.3. France

- 2.4. Germany

- 2.5. Russia

- 2.6. Italy

- 2.7. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. Rest of Asia Pacific

-

4. South America

- 4.1. Brazil

- 4.2. Argentina

- 4.3. Rest of South America

-

5. Middle East and Africa

- 5.1. South Africa

- 5.2. United Arab Emirates

- 5.3. Rest of Middle East and Africa

Gems Industry Regional Market Share

Geographic Coverage of Gems Industry

Gems Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Rings

- 5.1.2. Necklaces

- 5.1.3. Earrings

- 5.1.4. Bracelets

- 5.1.5. Chains and Pendants

- 5.1.6. Other Product Types

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Offline Retail Stores

- 5.2.2. Online Retail Stores

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. South America

- 5.3.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. Global Gems Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Rings

- 6.1.2. Necklaces

- 6.1.3. Earrings

- 6.1.4. Bracelets

- 6.1.5. Chains and Pendants

- 6.1.6. Other Product Types

- 6.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.2.1. Offline Retail Stores

- 6.2.2. Online Retail Stores

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. North America Gems Industry Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 7.1.1. Rings

- 7.1.2. Necklaces

- 7.1.3. Earrings

- 7.1.4. Bracelets

- 7.1.5. Chains and Pendants

- 7.1.6. Other Product Types

- 7.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 7.2.1. Offline Retail Stores

- 7.2.2. Online Retail Stores

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 8. Europe Gems Industry Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 8.1.1. Rings

- 8.1.2. Necklaces

- 8.1.3. Earrings

- 8.1.4. Bracelets

- 8.1.5. Chains and Pendants

- 8.1.6. Other Product Types

- 8.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 8.2.1. Offline Retail Stores

- 8.2.2. Online Retail Stores

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 9. Asia Pacific Gems Industry Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 9.1.1. Rings

- 9.1.2. Necklaces

- 9.1.3. Earrings

- 9.1.4. Bracelets

- 9.1.5. Chains and Pendants

- 9.1.6. Other Product Types

- 9.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 9.2.1. Offline Retail Stores

- 9.2.2. Online Retail Stores

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 10. South America Gems Industry Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 10.1.1. Rings

- 10.1.2. Necklaces

- 10.1.3. Earrings

- 10.1.4. Bracelets

- 10.1.5. Chains and Pendants

- 10.1.6. Other Product Types

- 10.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 10.2.1. Offline Retail Stores

- 10.2.2. Online Retail Stores

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 11. Middle East and Africa Gems Industry Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 11.1.1. Rings

- 11.1.2. Necklaces

- 11.1.3. Earrings

- 11.1.4. Bracelets

- 11.1.5. Chains and Pendants

- 11.1.6. Other Product Types

- 11.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 11.2.1. Offline Retail Stores

- 11.2.2. Online Retail Stores

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 The Swatch Group AG

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 PANDORA JEWELRY LLC

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 De Beers Jewellers US Inc

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 LVMH Group

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Chow Tai Fook Jewellery Company Limited*List Not Exhaustive

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Richemont SA

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Swarovski Crystal Online AG

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Chow Tai Fook Jewelry Company Limited

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Tata Sons Private Ltd

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Signet Jewelers

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 The Swatch Group AG

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Gems Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Gems Industry Revenue (billion), by Product Type 2025 & 2033

- Figure 3: North America Gems Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 4: North America Gems Industry Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 5: North America Gems Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 6: North America Gems Industry Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Gems Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Gems Industry Revenue (billion), by Product Type 2025 & 2033

- Figure 9: Europe Gems Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 10: Europe Gems Industry Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 11: Europe Gems Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 12: Europe Gems Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: Europe Gems Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Gems Industry Revenue (billion), by Product Type 2025 & 2033

- Figure 15: Asia Pacific Gems Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 16: Asia Pacific Gems Industry Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 17: Asia Pacific Gems Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 18: Asia Pacific Gems Industry Revenue (billion), by Country 2025 & 2033

- Figure 19: Asia Pacific Gems Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: South America Gems Industry Revenue (billion), by Product Type 2025 & 2033

- Figure 21: South America Gems Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 22: South America Gems Industry Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 23: South America Gems Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 24: South America Gems Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: South America Gems Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East and Africa Gems Industry Revenue (billion), by Product Type 2025 & 2033

- Figure 27: Middle East and Africa Gems Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 28: Middle East and Africa Gems Industry Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 29: Middle East and Africa Gems Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 30: Middle East and Africa Gems Industry Revenue (billion), by Country 2025 & 2033

- Figure 31: Middle East and Africa Gems Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Gems Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 2: Global Gems Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 3: Global Gems Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Gems Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 5: Global Gems Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 6: Global Gems Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Gems Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Gems Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Gems Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Rest of North America Gems Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Global Gems Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 12: Global Gems Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 13: Global Gems Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 14: Spain Gems Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: United Kingdom Gems Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: France Gems Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: Germany Gems Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Russia Gems Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 19: Italy Gems Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Rest of Europe Gems Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: Global Gems Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 22: Global Gems Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 23: Global Gems Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 24: China Gems Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Japan Gems Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: India Gems Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Australia Gems Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Rest of Asia Pacific Gems Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 29: Global Gems Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 30: Global Gems Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 31: Global Gems Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 32: Brazil Gems Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: Argentina Gems Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: Rest of South America Gems Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: Global Gems Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 36: Global Gems Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 37: Global Gems Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 38: South Africa Gems Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 39: United Arab Emirates Gems Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 40: Rest of Middle East and Africa Gems Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Gems Industry?

The projected CAGR is approximately 6.3%.

2. Which companies are prominent players in the Gems Industry?

Key companies in the market include The Swatch Group AG, PANDORA JEWELRY LLC, De Beers Jewellers US Inc, LVMH Group, Chow Tai Fook Jewellery Company Limited*List Not Exhaustive, Richemont SA, Swarovski Crystal Online AG, Chow Tai Fook Jewelry Company Limited, Tata Sons Private Ltd, Signet Jewelers.

3. What are the main segments of the Gems Industry?

The market segments include Product Type, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 12.7 billion as of 2022.

5. What are some drivers contributing to market growth?

Product Innovations to Drive Demand for Watches; Rising Demand for Premium Fashion Items.

6. What are the notable trends driving market growth?

Rising Demand for Gems & Jewellery Owing to the Emerging Middle Class.

7. Are there any restraints impacting market growth?

Presence of Counterfeit Products.

8. Can you provide examples of recent developments in the market?

September 2022: As an ode to the Chola Dynasty, which is considered a golden age of Indian history, Tanishq launched its new exclusive collection The Chola, which is an ode to the dynasty.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Gems Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Gems Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Gems Industry?

To stay informed about further developments, trends, and reports in the Gems Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence