Key Insights

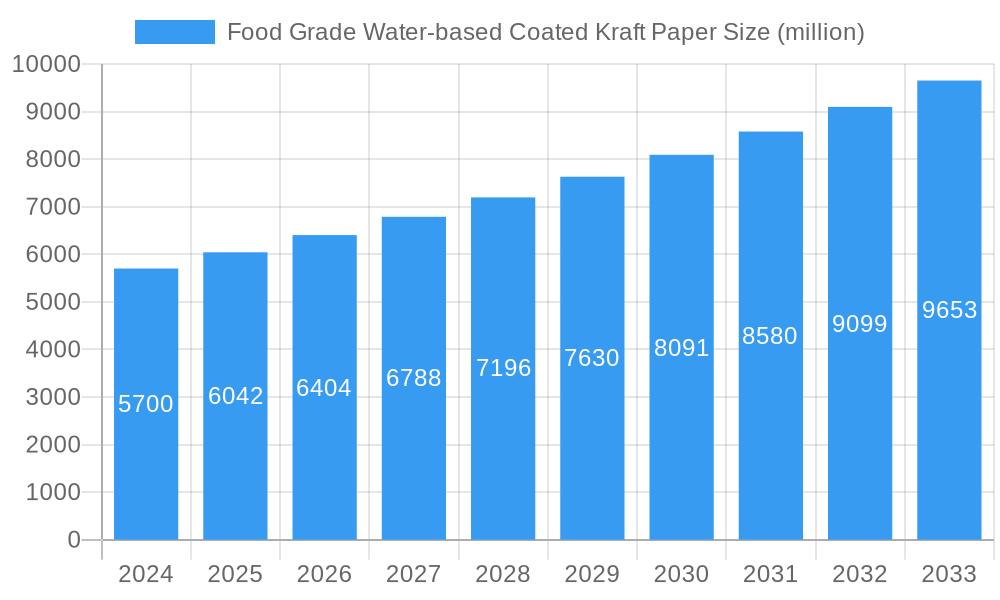

The global market for Food Grade Water-based Coated Kraft Paper is poised for significant expansion, driven by increasing consumer demand for sustainable and safe food packaging solutions. In 2024, the market is estimated to be valued at approximately $5.7 billion, exhibiting a robust Compound Annual Growth Rate (CAGR) of 6% from 2025 to 2033. This upward trajectory is primarily fueled by the stringent regulatory landscape favoring eco-friendly materials and a growing awareness of the health implications associated with traditional plastic packaging. The versatility of water-based coatings, offering excellent grease and moisture resistance while being environmentally benign, makes them an attractive alternative across various food applications. Key applications such as baked goods, beverage/dairy, and convenience foods are leading the charge, with manufacturers actively seeking innovative packaging that enhances product shelf-life and consumer appeal. The growing preference for lightweight, recyclable packaging materials further solidifies the market's positive outlook.

Food Grade Water-based Coated Kraft Paper Market Size (In Billion)

The market segmentation by quantitative coating weight reveals a strong demand for materials ranging from ≤50 g/㎡ to 50 g/㎡<Quantitative<120 g/㎡, catering to diverse packaging needs from primary wraps to secondary containers. Geographically, the Asia Pacific region, particularly China and India, is emerging as a dominant force due to its rapidly expanding food industry, burgeoning middle class, and increasing adoption of advanced packaging technologies. North America and Europe remain significant markets, driven by established food processing sectors and a strong emphasis on sustainability and food safety regulations. Despite the positive growth drivers, potential restraints such as the initial investment in new coating technologies and the fluctuating prices of raw materials could present challenges. However, the long-term outlook remains highly optimistic, with continuous innovation in coating formulations and paper production processes expected to overcome these hurdles and unlock further market potential.

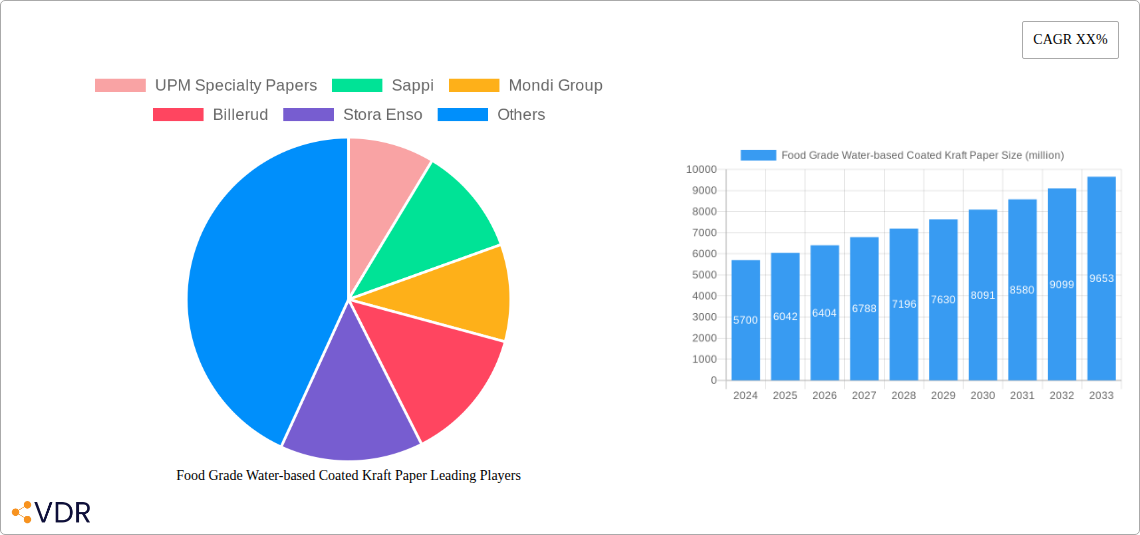

Food Grade Water-based Coated Kraft Paper Company Market Share

This comprehensive report offers an in-depth analysis of the Food Grade Water-based Coated Kraft Paper Market, a rapidly evolving sector driven by increasing demand for sustainable and safe food packaging solutions. With a study period spanning from 2019 to 2033 and a base year of 2025, this report provides critical insights into market dynamics, growth trends, regional dominance, and key player strategies. Leveraging high-traffic keywords such as "sustainable packaging," "eco-friendly food packaging," "kraft paper solutions," and "water-based coatings," this report is optimized for maximum search engine visibility, attracting industry professionals seeking detailed market intelligence.

The food grade water-based coated kraft paper market is projected to witness significant expansion, driven by stringent regulations favoring food safety and the escalating consumer preference for environmentally responsible packaging. This report delves into the intricate market structure, technological advancements, and competitive landscape, offering a forward-looking perspective crucial for strategic decision-making in both parent and child markets.

Food Grade Water-based Coated Kraft Paper Market Dynamics & Structure

The global food grade water-based coated kraft paper market exhibits a moderately consolidated structure, with leading players like UPM Specialty Papers, Sappi, Mondi Group, Billerud, and Stora Enso holding substantial market shares. Technological innovation remains a key driver, with continuous advancements in water-based coating formulations enhancing barrier properties, printability, and recyclability. Regulatory frameworks, particularly concerning food contact materials and environmental sustainability, are increasingly shaping market dynamics, pushing manufacturers towards compliant and eco-friendly alternatives. Competitive product substitutes include plastic films, waxed papers, and other coated papers, though water-based coated kraft paper gains traction due to its superior environmental profile. End-user demographics are shifting towards environmentally conscious consumers and businesses seeking to align with sustainability goals. Mergers and acquisitions (M&A) trends, while present, are largely focused on capacity expansion and technological integration, with approximately 5-7 major M&A deals anticipated within the forecast period. Innovation barriers primarily revolve around achieving cost-competitiveness with established plastic alternatives and scaling up production of advanced water-based coating technologies.

- Market Concentration: Moderately consolidated with a few key global players.

- Technological Innovation: Driven by improved barrier properties, printability, and recyclability of water-based coatings.

- Regulatory Impact: Strict food safety and environmental regulations are key market shapers.

- Competitive Landscape: Key competitors include plastic films, waxed papers, and other coated paper types.

- End-User Demand: Growing preference for sustainable and safe food packaging solutions.

- M&A Activity: Primarily focused on capacity expansion and technological integration, with an estimated 5-7 deals in the forecast period.

Food Grade Water-based Coated Kraft Paper Growth Trends & Insights

The global food grade water-based coated kraft paper market is poised for robust growth, propelled by an escalating demand for sustainable and safe food packaging solutions across diverse applications. The market size is estimated to have reached approximately $15.8 billion in 2024 and is projected to expand at a Compound Annual Growth Rate (CAGR) of 7.2% during the forecast period of 2025–2033, reaching an estimated value of $28.5 billion by 2033. This significant expansion is underpinned by shifting consumer preferences towards eco-friendly alternatives, coupled with stringent governmental regulations mandating safer and more sustainable packaging materials. The adoption rate of these papers is steadily increasing, particularly in developed economies, as brands increasingly integrate sustainability into their corporate social responsibility initiatives. Technological disruptions, such as the development of advanced water-based coatings with enhanced barrier properties against moisture, grease, and oxygen, are playing a pivotal role. These innovations not only meet regulatory requirements but also improve product shelf-life and integrity, making them a preferred choice over traditional plastic packaging. Consumer behavior shifts are evident, with a growing segment of consumers actively seeking products with minimal environmental impact, thereby influencing brand choices and driving demand for paper-based packaging. The penetration of food grade water-based coated kraft paper in emerging markets is also on an upward trajectory, fueled by growing disposable incomes and increased awareness of environmental issues. The market's evolution is also influenced by evolving food trends, such as the rise of convenience foods and ready-to-eat meals, which necessitate efficient and safe packaging solutions. The inherent recyclability and biodegradability of kraft paper, combined with the improved performance offered by water-based coatings, position it as a sustainable and high-performing alternative in the competitive food packaging landscape. The transition away from single-use plastics is further accelerating this growth.

Dominant Regions, Countries, or Segments in Food Grade Water-based Coated Kraft Paper

North America, particularly the United States, currently dominates the global food grade water-based coated kraft paper market, driven by a confluence of factors including stringent food safety regulations, a mature and environmentally conscious consumer base, and a well-established food processing industry. The Application segment of Convenience Foods is a significant growth driver within this region. The high adoption rate of ready-to-eat meals, snacks, and on-the-go food options necessitates packaging that is not only safe and hygienic but also convenient and visually appealing, areas where water-based coated kraft paper excels. The Type segment of 50g/㎡<Quantitative<120g/㎡ also plays a crucial role, offering a versatile range of grammages suitable for various convenience food packaging formats, from sandwich wrappers to meal trays.

Key drivers for North America's dominance include:

- Economic Policies: Government initiatives promoting sustainability and circular economy principles encourage the adoption of eco-friendly packaging.

- Infrastructure: Robust recycling infrastructure and advanced manufacturing capabilities support the widespread use and production of these papers.

- Consumer Awareness: A highly informed consumer base actively demands sustainable product options, influencing brand packaging choices.

- Food Industry Investments: Significant investments by major food manufacturers in sustainable packaging solutions further boost demand.

- Regulatory Compliance: Proactive adherence to FDA and other regulatory standards for food contact materials ensures market confidence.

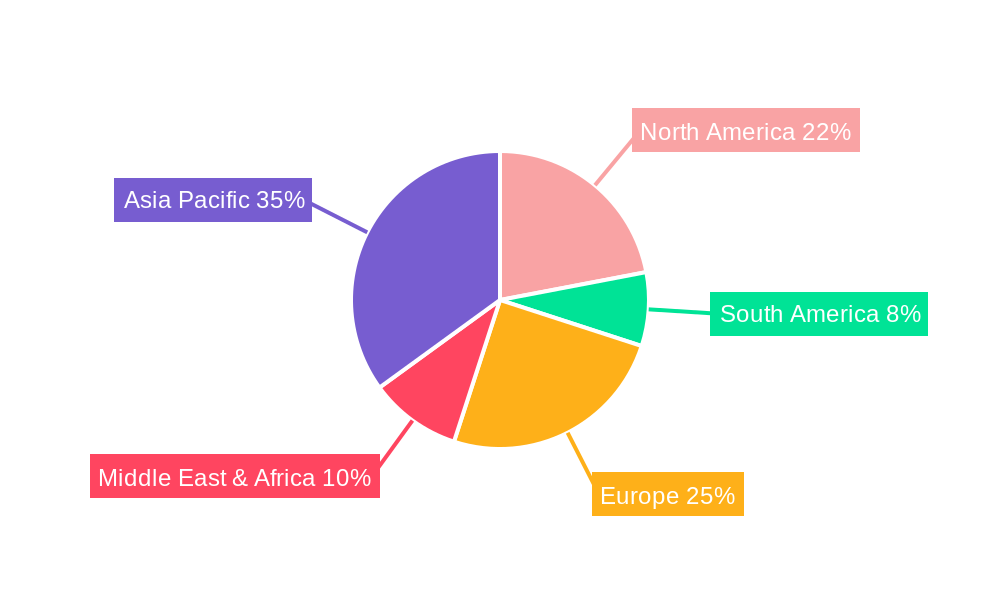

Within the Convenience Foods application, the demand for secondary packaging, such as paper bags and boxes for snacks and baked goods, is particularly strong. The 50g/㎡<Quantitative<120g/㎡ grammage is ideal for these applications, providing the necessary strength and printability for branding and product information. The Others application segment, encompassing items like coffee cups and food service ware, also contributes significantly to market growth, reflecting the broader shift towards sustainable disposables in the food service industry. The market share for this dominant region is estimated to be around 35% of the global market.

Europe, with its strong emphasis on environmental protection and the European Green Deal, is a close second and shows rapid growth potential. Asia Pacific is emerging as a high-growth region due to increasing disposable incomes, rapid urbanization, and a growing awareness of food safety and environmental concerns.

Food Grade Water-based Coated Kraft Paper Product Landscape

The product landscape of food grade water-based coated kraft paper is characterized by continuous innovation aimed at enhancing performance and sustainability. Manufacturers are developing specialized coatings that offer superior grease, moisture, and heat resistance, crucial for various food applications. These coatings are formulated using water-based polymers and additives, ensuring compliance with food safety regulations and minimizing environmental impact compared to solvent-based alternatives. Applications range from baked goods packaging, paper tableware, and beverage/dairy containers to convenience food wrappers and trays. Unique selling propositions often revolve around excellent printability for vibrant branding, recyclability, compostability, and a favorable safety profile for direct food contact. Technological advancements include the development of advanced barrier coatings for extended shelf life and compostable options catering to the growing demand for end-of-life solutions.

Key Drivers, Barriers & Challenges in Food Grade Water-based Coated Kraft Paper

The food grade water-based coated kraft paper market is propelled by several key drivers. The escalating global demand for sustainable and eco-friendly packaging solutions is paramount, fueled by consumer awareness and regulatory mandates. Advancements in water-based coating technology, offering improved barrier properties and printability, further enhance its appeal. The increasing restrictions on single-use plastics are a significant catalyst, pushing industries towards viable paper-based alternatives.

- Drivers:

- Growing consumer preference for sustainable packaging.

- Stringent environmental regulations and plastic bans.

- Technological advancements in water-based coatings (barrier properties, recyclability).

- Demand from the food service and convenience food sectors.

- Corporate sustainability initiatives.

Key challenges and restraints include the relatively higher cost of production compared to conventional plastic packaging, which can be a barrier to widespread adoption, especially in price-sensitive markets. Achieving comparable barrier properties to some specialized plastics for extremely sensitive products remains an ongoing challenge, although significant progress is being made. Supply chain disruptions and fluctuating raw material prices can also impact market stability.

- Challenges & Restraints:

- Higher production costs compared to some traditional packaging.

- Achieving parity with certain high-performance plastic barrier properties.

- Supply chain volatility and raw material price fluctuations.

- Consumer perception and awareness regarding the capabilities of paper-based packaging.

- Development of widespread industrial composting infrastructure.

Emerging Opportunities in Food Grade Water-based Coated Kraft Paper

Emerging opportunities lie in the development of advanced biodegradable and compostable water-based coatings that meet stringent performance requirements. Untapped markets in developing economies present significant growth potential as environmental awareness and disposable incomes rise. Innovative applications, such as direct food contact paper-based containers for hot and cold beverages and specialized packaging for frozen foods, offer promising avenues. The evolving consumer preference for transparency and traceability in food sourcing also creates opportunities for packaging that can effectively communicate such information.

Growth Accelerators in the Food Grade Water-based Coated Kraft Paper Industry

Growth accelerators in the food grade water-based coated kraft paper industry are primarily driven by continuous research and development in coating formulations that enhance sustainability and performance. Strategic partnerships between paper manufacturers, coating suppliers, and end-users are crucial for co-creating innovative packaging solutions tailored to specific needs. Market expansion strategies focusing on emerging economies, where the demand for safer and eco-friendly packaging is rapidly increasing, will also serve as significant growth accelerators. The development of localized production facilities and supply chains can further reduce costs and enhance accessibility.

Key Players Shaping the Food Grade Water-based Coated Kraft Paper Market

- UPM Specialty Papers

- Sappi

- Mondi Group

- Billerud

- Stora Enso

- Koehler Paper

- Sierra Coating Technologies

- Oji Paper

- Westrock

- Wuzhou Specialty Papers

- Sun Paper

- Hetrun

- Sinar Mas Group

- Ruize Arts

- Zhejiang Hengda New Materials

- Glory Paper

- Zhuhai Hongta Renheng Packaging

- Rosense

Notable Milestones in Food Grade Water-based Coated Kraft Paper Sector

- 2019: Increased focus on biodegradable coating formulations.

- 2020: Introduction of high-barrier water-based coatings for extended shelf-life applications.

- 2021: Growing adoption in the ready-to-eat meal sector due to convenience and sustainability.

- 2022: Stringent regulations on PFAS in food packaging drive shift towards water-based alternatives.

- 2023: Significant investments in R&D for compostable kraft paper solutions.

- 2024: Expansion of production capacities by major players to meet rising demand.

- 2025 (Est.): Anticipated widespread adoption for baked goods and paper tableware applications.

- 2026-2033: Expected continuous innovation in barrier technology and circular economy solutions.

In-Depth Food Grade Water-based Coated Kraft Paper Market Outlook

The outlook for the food grade water-based coated kraft paper market remains exceptionally strong, fueled by an unwavering global commitment to sustainability and enhanced food safety standards. Growth accelerators like ongoing technological breakthroughs in barrier coatings, strategic collaborations across the value chain, and targeted market expansion initiatives, especially in rapidly developing economies, will continue to propel the industry forward. The increasing adoption of circular economy principles and the demand for fully recyclable and compostable packaging solutions present significant strategic opportunities for market players. The long-term potential is further bolstered by a fundamental shift in consumer preferences and regulatory landscapes, solidifying the position of water-based coated kraft paper as a vital component of future food packaging.

Food Grade Water-based Coated Kraft Paper Segmentation

-

1. Application

- 1.1. Baked Goods

- 1.2. Paper Tableware

- 1.3. Beverage/Dairy

- 1.4. Convenience Foods

- 1.5. Others

-

2. Types

- 2.1. Quantitative ≤50g/㎡

- 2.2. 50g/㎡<Quantitative<120g/㎡

- 2.3. Quantitative ≥120g/㎡

Food Grade Water-based Coated Kraft Paper Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Food Grade Water-based Coated Kraft Paper Regional Market Share

Geographic Coverage of Food Grade Water-based Coated Kraft Paper

Food Grade Water-based Coated Kraft Paper REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Baked Goods

- 5.1.2. Paper Tableware

- 5.1.3. Beverage/Dairy

- 5.1.4. Convenience Foods

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Quantitative ≤50g/㎡

- 5.2.2. 50g/㎡<Quantitative<120g/㎡

- 5.2.3. Quantitative ≥120g/㎡

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Food Grade Water-based Coated Kraft Paper Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Baked Goods

- 6.1.2. Paper Tableware

- 6.1.3. Beverage/Dairy

- 6.1.4. Convenience Foods

- 6.1.5. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Quantitative ≤50g/㎡

- 6.2.2. 50g/㎡<Quantitative<120g/㎡

- 6.2.3. Quantitative ≥120g/㎡

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Food Grade Water-based Coated Kraft Paper Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Baked Goods

- 7.1.2. Paper Tableware

- 7.1.3. Beverage/Dairy

- 7.1.4. Convenience Foods

- 7.1.5. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Quantitative ≤50g/㎡

- 7.2.2. 50g/㎡<Quantitative<120g/㎡

- 7.2.3. Quantitative ≥120g/㎡

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Food Grade Water-based Coated Kraft Paper Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Baked Goods

- 8.1.2. Paper Tableware

- 8.1.3. Beverage/Dairy

- 8.1.4. Convenience Foods

- 8.1.5. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Quantitative ≤50g/㎡

- 8.2.2. 50g/㎡<Quantitative<120g/㎡

- 8.2.3. Quantitative ≥120g/㎡

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Food Grade Water-based Coated Kraft Paper Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Baked Goods

- 9.1.2. Paper Tableware

- 9.1.3. Beverage/Dairy

- 9.1.4. Convenience Foods

- 9.1.5. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Quantitative ≤50g/㎡

- 9.2.2. 50g/㎡<Quantitative<120g/㎡

- 9.2.3. Quantitative ≥120g/㎡

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Food Grade Water-based Coated Kraft Paper Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Baked Goods

- 10.1.2. Paper Tableware

- 10.1.3. Beverage/Dairy

- 10.1.4. Convenience Foods

- 10.1.5. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Quantitative ≤50g/㎡

- 10.2.2. 50g/㎡<Quantitative<120g/㎡

- 10.2.3. Quantitative ≥120g/㎡

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Food Grade Water-based Coated Kraft Paper Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Baked Goods

- 11.1.2. Paper Tableware

- 11.1.3. Beverage/Dairy

- 11.1.4. Convenience Foods

- 11.1.5. Others

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Quantitative ≤50g/㎡

- 11.2.2. 50g/㎡<Quantitative<120g/㎡

- 11.2.3. Quantitative ≥120g/㎡

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 UPM Specialty Papers

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Sappi

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Mondi Group

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Billerud

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Stora Enso

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Koehler Paper

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Sierra Coating Technologies

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Oji Paper

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Westrock

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Wuzhou Specialty Papers

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Sun Paper

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Hetrun

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Sinar Mas Group

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Ruize Arts

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Zhejiang Hengda New Materials

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 Glory Paper

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.17 Zhuhai Hongta Renheng Packaging

- 12.1.17.1. Company Overview

- 12.1.17.2. Products

- 12.1.17.3. Company Financials

- 12.1.17.4. SWOT Analysis

- 12.1.18 Rosense

- 12.1.18.1. Company Overview

- 12.1.18.2. Products

- 12.1.18.3. Company Financials

- 12.1.18.4. SWOT Analysis

- 12.1.1 UPM Specialty Papers

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Food Grade Water-based Coated Kraft Paper Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Food Grade Water-based Coated Kraft Paper Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Food Grade Water-based Coated Kraft Paper Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Food Grade Water-based Coated Kraft Paper Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Food Grade Water-based Coated Kraft Paper Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Food Grade Water-based Coated Kraft Paper Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Food Grade Water-based Coated Kraft Paper Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Food Grade Water-based Coated Kraft Paper Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Food Grade Water-based Coated Kraft Paper Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Food Grade Water-based Coated Kraft Paper Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Food Grade Water-based Coated Kraft Paper Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Food Grade Water-based Coated Kraft Paper Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Food Grade Water-based Coated Kraft Paper Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Food Grade Water-based Coated Kraft Paper Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Food Grade Water-based Coated Kraft Paper Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Food Grade Water-based Coated Kraft Paper Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Food Grade Water-based Coated Kraft Paper Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Food Grade Water-based Coated Kraft Paper Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Food Grade Water-based Coated Kraft Paper Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Food Grade Water-based Coated Kraft Paper Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Food Grade Water-based Coated Kraft Paper Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Food Grade Water-based Coated Kraft Paper Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Food Grade Water-based Coated Kraft Paper Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Food Grade Water-based Coated Kraft Paper Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Food Grade Water-based Coated Kraft Paper Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Food Grade Water-based Coated Kraft Paper Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Food Grade Water-based Coated Kraft Paper Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Food Grade Water-based Coated Kraft Paper Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Food Grade Water-based Coated Kraft Paper Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Food Grade Water-based Coated Kraft Paper Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Food Grade Water-based Coated Kraft Paper Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Food Grade Water-based Coated Kraft Paper Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Food Grade Water-based Coated Kraft Paper Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Food Grade Water-based Coated Kraft Paper Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Food Grade Water-based Coated Kraft Paper Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Food Grade Water-based Coated Kraft Paper Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Food Grade Water-based Coated Kraft Paper Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Food Grade Water-based Coated Kraft Paper Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Food Grade Water-based Coated Kraft Paper Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Food Grade Water-based Coated Kraft Paper Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Food Grade Water-based Coated Kraft Paper Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Food Grade Water-based Coated Kraft Paper Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Food Grade Water-based Coated Kraft Paper Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Food Grade Water-based Coated Kraft Paper Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Food Grade Water-based Coated Kraft Paper Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Food Grade Water-based Coated Kraft Paper Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Food Grade Water-based Coated Kraft Paper Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Food Grade Water-based Coated Kraft Paper Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Food Grade Water-based Coated Kraft Paper Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Food Grade Water-based Coated Kraft Paper Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Food Grade Water-based Coated Kraft Paper Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Food Grade Water-based Coated Kraft Paper Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Food Grade Water-based Coated Kraft Paper Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Food Grade Water-based Coated Kraft Paper Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Food Grade Water-based Coated Kraft Paper Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Food Grade Water-based Coated Kraft Paper Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Food Grade Water-based Coated Kraft Paper Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Food Grade Water-based Coated Kraft Paper Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Food Grade Water-based Coated Kraft Paper Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Food Grade Water-based Coated Kraft Paper Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Food Grade Water-based Coated Kraft Paper Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Food Grade Water-based Coated Kraft Paper Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Food Grade Water-based Coated Kraft Paper Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Food Grade Water-based Coated Kraft Paper Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Food Grade Water-based Coated Kraft Paper Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Food Grade Water-based Coated Kraft Paper Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Food Grade Water-based Coated Kraft Paper Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Food Grade Water-based Coated Kraft Paper Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Food Grade Water-based Coated Kraft Paper Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Food Grade Water-based Coated Kraft Paper Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Food Grade Water-based Coated Kraft Paper Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Food Grade Water-based Coated Kraft Paper Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Food Grade Water-based Coated Kraft Paper Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Food Grade Water-based Coated Kraft Paper Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Food Grade Water-based Coated Kraft Paper Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Food Grade Water-based Coated Kraft Paper Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Food Grade Water-based Coated Kraft Paper Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Food Grade Water-based Coated Kraft Paper?

The projected CAGR is approximately 6.8%.

2. Which companies are prominent players in the Food Grade Water-based Coated Kraft Paper?

Key companies in the market include UPM Specialty Papers, Sappi, Mondi Group, Billerud, Stora Enso, Koehler Paper, Sierra Coating Technologies, Oji Paper, Westrock, Wuzhou Specialty Papers, Sun Paper, Hetrun, Sinar Mas Group, Ruize Arts, Zhejiang Hengda New Materials, Glory Paper, Zhuhai Hongta Renheng Packaging, Rosense.

3. What are the main segments of the Food Grade Water-based Coated Kraft Paper?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 66.5 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Food Grade Water-based Coated Kraft Paper," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Food Grade Water-based Coated Kraft Paper report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Food Grade Water-based Coated Kraft Paper?

To stay informed about further developments, trends, and reports in the Food Grade Water-based Coated Kraft Paper, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence