Key Insights into the Fluoropolymer Bottle Market

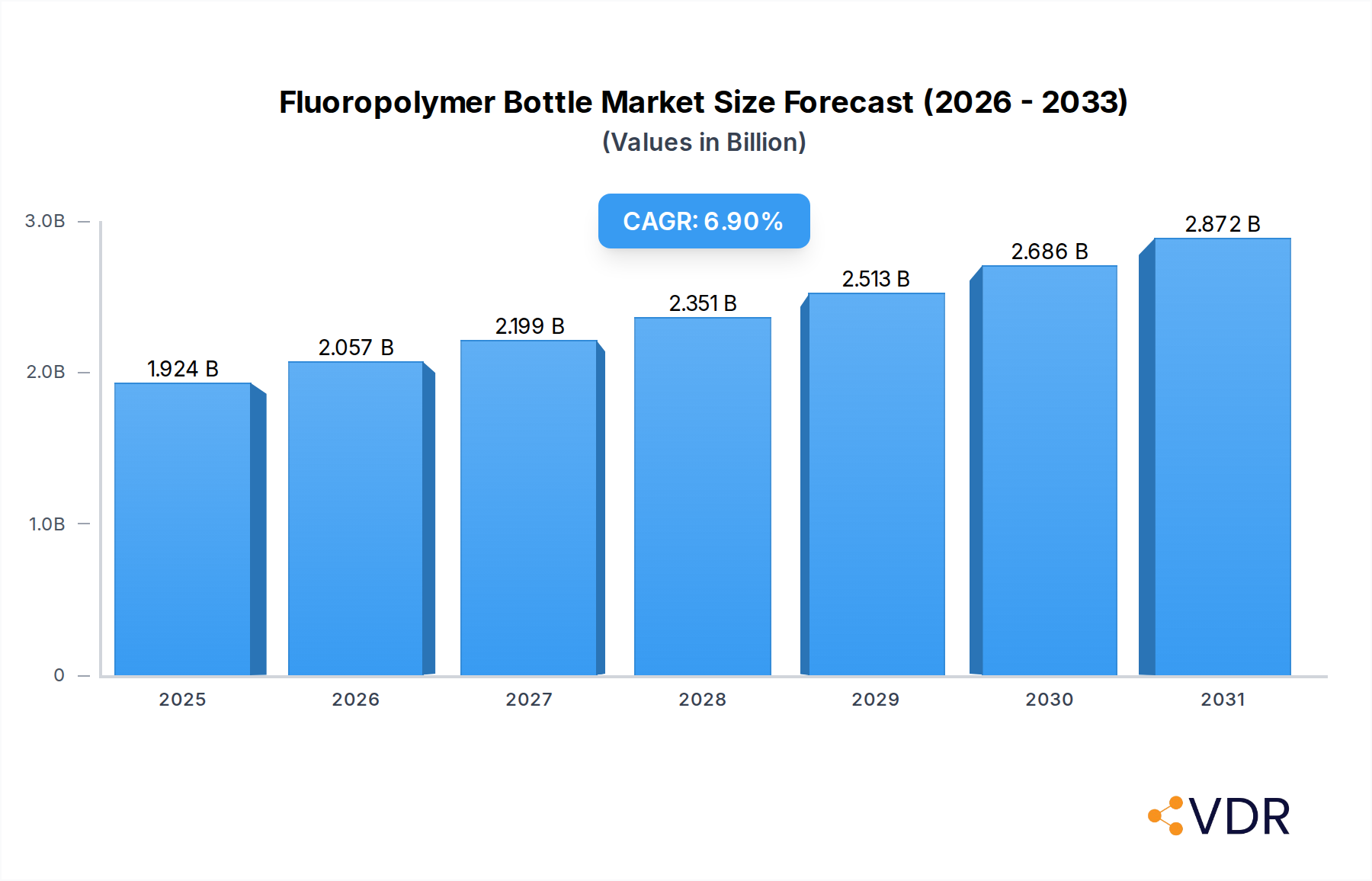

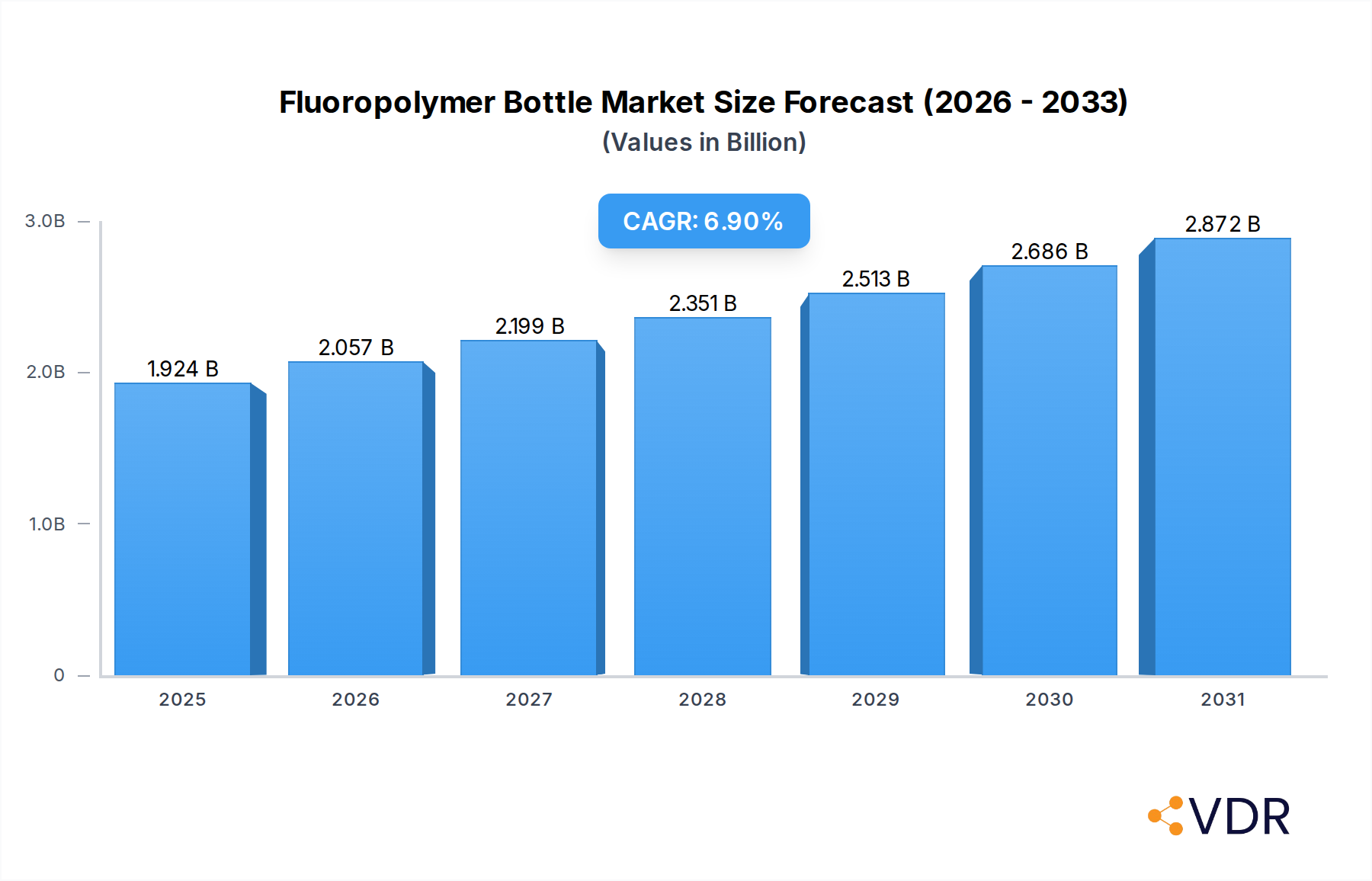

The Global Fluoropolymer Bottle Market is demonstrating robust expansion, valued at an estimated USD 1.8 billion in 2025. Projections indicate a substantial increase, driven by a compound annual growth rate (CAGR) of 6.9% from 2025 to 2034, culminating in an anticipated market valuation of approximately USD 3.28 billion by the end of the forecast period. This growth trajectory is underpinned by the intrinsic properties of fluoropolymers, namely their exceptional chemical inertness, high purity, broad temperature resistance, and unparalleled chemical compatibility. These attributes make fluoropolymer bottles indispensable for the safe and reliable storage, transport, and dispensing of aggressive chemicals, high-purity reagents, and sensitive biological samples across diverse industries.

Fluoropolymer Bottle Market Size (In Billion)

Key demand drivers include the escalating requirements from the chemical industry, particularly for specialty chemicals, where material integrity and prevention of contamination are paramount. The rapidly expanding pharmaceutical and biotechnology sectors also significantly contribute to market growth, necessitating ultra-clean and non-reactive packaging solutions for active pharmaceutical ingredients (APIs), diagnostic reagents, and cell culture media. Macroeconomic tailwinds such as increasing global investment in research and development (R&D), the proliferation of advanced manufacturing processes, and the tightening of regulatory standards for product purity and safety across various end-user industries further amplify market demand. Geopolitical stability and robust economic growth in emerging regions are fostering industrial expansion, subsequently boosting the adoption of high-performance packaging solutions like fluoropolymer bottles. The market is also benefiting from continuous innovation in fluoropolymer material science, leading to enhanced barrier properties, improved lifecycle performance, and the development of more sustainable production methods, all contributing to the sustained upward trend in the Fluoropolymer Bottle Market.

Fluoropolymer Bottle Company Market Share

Analysis of the Dominant Material Type Segment in the Fluoropolymer Bottle Market: PFA

Within the highly specialized Fluoropolymer Bottle Market, the 'Material Type' segment stands as a critical differentiator, with Perfluoroalkoxy (PFA) emerging as a dominant and rapidly expanding sub-segment. While Polytetrafluoroethylene (PTFE) initiated the fluoropolymer revolution with its superior chemical inertness, PFA has increasingly garnered market share due to its combination of PTFE's robust chemical resistance with enhanced mechanical properties, optical transparency, and excellent melt processability. The Perfluoroalkoxy Resin Market, in particular, underpins the production of these high-performance bottles.

PFA bottles are highly favored in applications demanding ultra-high purity, such as in the storage of corrosive and high-purity chemicals, pharmaceutical intermediates, and diagnostic reagents, largely due to their extremely low extractables profile and smooth, non-porous surface that minimizes adsorption and absorption. Their superior resistance to a wider range of chemicals and solvents, coupled with excellent high-temperature stability up to 260°C, positions PFA as an ideal material for handling aggressive media that would degrade other plastic or even glass containers. The transparency of PFA also offers a significant advantage, allowing for visual inspection of contents without compromising material integrity, a feature often lacking in opaque PTFE alternatives. Furthermore, PFA’s melt processability enables the fabrication of complex bottle geometries and tighter tolerances, facilitating higher-quality and more consistent products compared to the more challenging processing of PTFE.

Leading players in the Fluoropolymer Bottle Market, including Savillex Corporation, Saint-Gobain Performance Plastics, and Nalgene (Thermo Fisher Scientific), heavily emphasize PFA products in their portfolios, recognizing its critical role in advanced scientific and industrial applications. The increasing stringency of regulatory requirements in industries such as semiconductors, pharmaceuticals, and biotechnology for materials that ensure minimal contamination has further propelled the adoption of PFA. As industries continue to innovate and demand higher purity and performance from their containment solutions, the PFA segment is expected to continue its growth trajectory, potentially consolidating its dominant position over other fluoropolymer types in the broader High-Performance Plastics Market, despite the enduring relevance of materials from the Polytetrafluoroethylene Market and Fluorinated Ethylene Propylene Market for specific applications. Continuous advancements in PFA formulation and processing technologies are anticipated to further enhance its attributes and broaden its applicability, reinforcing its leading position within the Fluoropolymer Bottle Market.

Key Market Drivers & Constraints in the Fluoropolymer Bottle Market

The Fluoropolymer Bottle Market's expansion is fundamentally shaped by a confluence of potent demand drivers and specific limiting factors. A primary driver is the escalating global demand for high-purity and chemically inert packaging solutions. Industries such as pharmaceuticals and biotechnology, for instance, mandate containers that prevent leachables and extractables to maintain product integrity, directly fueling the growth of the Pharmaceutical Packaging Market. This is particularly critical for sensitive APIs and diagnostic reagents where even trace contamination can compromise efficacy or lead to regulatory non-compliance, thus amplifying the necessity for fluoropolymer bottles.

Another significant impetus stems from the robust growth within the Specialty Chemicals Market. Manufacturers of aggressive acids, bases, solvents, and other highly reactive chemical compounds rely on fluoropolymer bottles due to their exceptional chemical resistance, which prevents corrosion and degradation of the container material. This ensures safe handling, extended shelf life, and integrity of valuable chemical formulations, underpinning the demand for specialized Chemical Storage Market solutions. Furthermore, the continuous expansion of research and development activities across academic institutions and industrial laboratories globally contributes substantially. These facilities, integral to the broader Laboratory Consumables Market, require reliable, non-reactive containers for sample storage, media preparation, and reagent dispensing, making fluoropolymer bottles an essential component of modern scientific research.

However, the Fluoropolymer Bottle Market faces inherent constraints. The foremost challenge is the relatively high manufacturing cost associated with fluoropolymers compared to conventional plastic packaging materials. This elevated cost can be a barrier to adoption in price-sensitive applications or industries where less stringent purity requirements allow for more economical alternatives within the broader Plastic Packaging Market. Additionally, the complex recycling and disposal processes for fluoropolymers pose environmental concerns and regulatory hurdles. The inert nature that makes them so valuable also makes them difficult to break down or repurpose, contributing to environmental accumulation issues. Lastly, while offering superior performance, fluoropolymer bottles encounter competition from alternative materials like high-grade glass, stainless steel, or even advanced engineering plastics in specific niche applications where the extreme properties of fluoropolymers might be over-engineered or economically prohibitive.

Competitive Ecosystem of the Fluoropolymer Bottle Market

The Fluoropolymer Bottle Market is characterized by the presence of several specialized manufacturers offering high-performance solutions. These companies differentiate themselves through material science expertise, product innovation, and established distribution networks, catering to stringent industry demands.

- Savillex Corporation: A prominent manufacturer known for its high-purity fluoropolymer products, specializing in PFA and FEP labware and custom components for critical applications requiring ultra-low contamination.

- Saint-Gobain Performance Plastics: A global leader providing a wide array of high-performance polymer solutions, including fluoropolymer bottles and containers, focusing on life sciences, chemical processing, and industrial markets.

- Thermo Fisher Scientific: A major player in scientific instrumentation, consumables, and reagents, offering a comprehensive range of fluoropolymer bottles, primarily under its Nalgene brand, catering to research and laboratory needs.

- DWK Life Sciences: Known for its specialized laboratory glassware and plasticware, including fluoropolymer bottles, serving pharmaceutical, diagnostic, and research sectors with an emphasis on quality and precision.

- Nalgene (Thermo Fisher Scientific): A widely recognized brand within the laboratory consumables sector, offering a diverse portfolio of plasticware, with fluoropolymer bottles being a key offering for chemical resistance and purity.

- AMETEK Fluoropolymer Products: Specializes in high-purity fluoropolymer products, including custom-designed containers and components, focusing on industries requiring exceptional chemical resistance and cleanliness.

- Entegris, Inc.: A global provider of materials and solutions for advanced manufacturing, offering high-purity fluoropolymer containers and fluid handling systems, particularly for the semiconductor and life sciences industries.

- NICHIAS Corporation: A Japanese industrial conglomerate with a strong presence in advanced materials, including fluoropolymer products and fluid handling systems for various industrial and chemical applications.

- Zeus Industrial Products, Inc.: A leading polymer extrusion manufacturer, providing precision fluoropolymer tubing, and increasingly, components for high-purity container solutions, leveraging its material expertise.

- Fluorotherm Polymers, Inc.: Focuses on fluoropolymer solutions, offering specialty tubing, heat exchangers, and containers, emphasizing chemical resistance and high-temperature performance for industrial clients.

- Chang Zhou Feng Di Plastic Technology: A manufacturer specializing in plastic packaging and containers, including fluoropolymer bottles, catering to industrial and chemical sectors with a focus on customizable solutions.

- AGC Chemicals Americas: A major global chemical company producing a wide range of fluorochemicals and fluoropolymers, supplying raw materials and finished products that support the fluoropolymer bottle manufacturing sector.

- Daikin Industries Ltd.: A diversified global manufacturer with a significant fluorochemicals division, producing advanced fluoropolymers that are critical raw materials for high-performance fluoropolymer bottles.

Recent Developments & Milestones in the Fluoropolymer Bottle Market

Recent advancements and strategic movements within the Fluoropolymer Bottle Market underscore a commitment to enhancing product utility, sustainability, and market reach:

- January 2024: Savillex Corporation introduced a new line of PFA narrow-mouth bottles, optimized for ultra-high purity applications in trace metal analysis and semiconductor manufacturing, expanding their volume range from 30 mL to 2 L, addressing specific laboratory and industrial needs.

- November 2023: Saint-Gobain Performance Plastics announced an investment in sustainable fluoropolymer production technologies, aiming to reduce the environmental footprint of their FEP and PFA bottle manufacturing processes, aligning with global green initiatives.

- September 2023: Nalgene (Thermo Fisher Scientific) launched a series of certified pre-cleaned fluoropolymer bottles specifically designed for low-particulate applications in the pharmaceutical and biotechnology industries, ensuring compliance with stringent regulatory standards for the Biopharmaceutical Market.

- July 2023: Entegris, Inc. entered into a strategic partnership with a leading analytical instrumentation provider to develop integrated fluid handling systems that leverage their high-purity PFA bottles for enhanced sample integrity in advanced chemical processes.

- May 2023: Zeus Industrial Products, Inc. unveiled advancements in their fluoropolymer extrusion technology, enabling the production of thinner-walled yet equally robust fluoropolymer bottles, potentially leading to material savings and reduced manufacturing costs across the market.

- March 2023: A significant trend of increased capacity expansion was observed among key Asian manufacturers, including Chang Zhou Feng Di Plastic Technology, to meet the escalating demand from the rapidly growing chemical and pharmaceutical sectors in the Asia Pacific region.

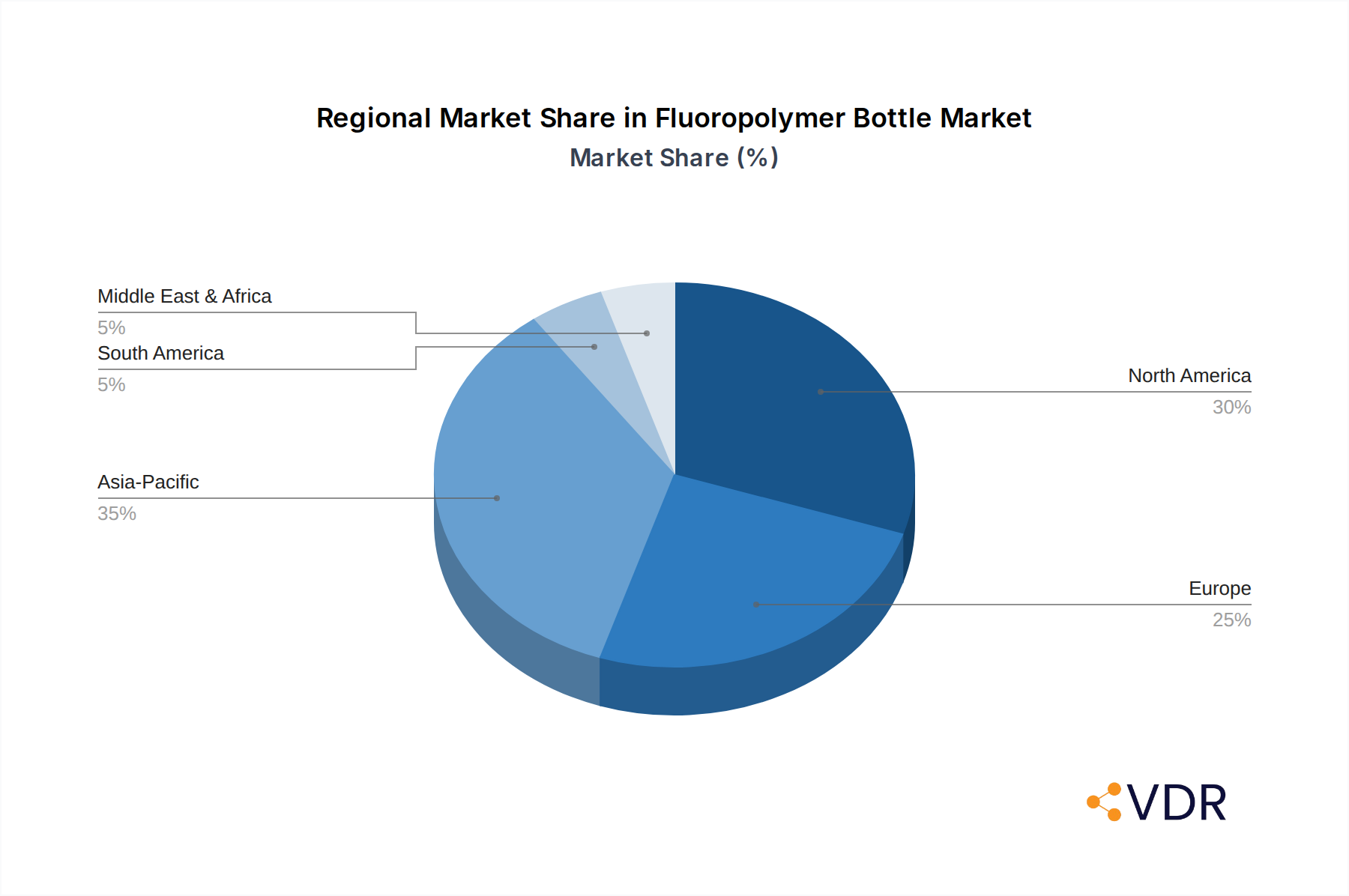

Regional Market Breakdown for the Fluoropolymer Bottle Market

The Global Fluoropolymer Bottle Market exhibits distinct regional dynamics, influenced by industrialization levels, regulatory frameworks, and technological adoption rates. North America and Europe currently represent the most mature markets, holding significant revenue shares due to robust pharmaceutical, biotechnology, and chemical industries, coupled with stringent regulatory environments demanding high-purity packaging solutions.

North America holds a substantial share, driven by extensive R&D investments, a thriving Biopharmaceutical Market, and a strong presence of advanced manufacturing facilities. The region's focus on high-tech industries and sophisticated laboratory research ensures a consistent demand for specialized fluoropolymer bottles. While exhibiting a solid, stable growth, its CAGR is estimated at around 6.2%, reflecting its maturity but sustained innovation.

Europe also commands a significant market share, fueled by a well-established chemical industry, leading pharmaceutical companies, and rigorous environmental and safety regulations that necessitate inert containment solutions. Countries like Germany, France, and the UK are major contributors. The regional CAGR is projected at approximately 6.5%, underpinned by ongoing scientific research and industrial expansion, particularly in the Pharmaceutical Packaging Market.

Asia Pacific is identified as the fastest-growing region in the Fluoropolymer Bottle Market, with an anticipated CAGR of over 8.0%. This rapid expansion is primarily driven by accelerating industrialization, increasing foreign direct investment, and a burgeoning pharmaceutical, biotechnology, and electronics manufacturing base, especially in China, India, and Japan. The region's expanding chemical industry and growing research infrastructure are creating immense demand for high-performance fluoropolymer containers, particularly for the Specialty Chemicals Market.

The Middle East & Africa and South America regions, while currently holding smaller market shares, are poised for considerable growth. Investments in infrastructure, chemical processing, and healthcare sectors across these regions are gradually increasing the demand for advanced packaging. These emerging markets are expected to demonstrate CAGRs in the range of 7.0% to 7.5%, as industrial development and the adoption of international quality standards gather pace.

Fluoropolymer Bottle Regional Market Share

Customer Segmentation & Buying Behavior in the Fluoropolymer Bottle Market

Customer segmentation within the Fluoropolymer Bottle Market is primarily dictated by the end-user industry, each with unique purchasing criteria and behavioral patterns. The major segments include the Chemical Industry, Pharmaceutical Industry, Biotechnology Companies, and Research & Academic Laboratories. Each segment's buying behavior is heavily influenced by the specific requirements for chemical resistance, purity, temperature stability, and regulatory compliance.

For the Chemical Industry, especially those dealing with corrosive or high-purity reagents, the primary purchasing criteria revolve around maximum chemical compatibility, temperature range tolerance, and long-term material integrity to prevent degradation or contamination. Price sensitivity tends to be moderate to high for bulk applications, but extremely low for critical, high-value chemicals where material failure is unacceptable. Procurement often occurs through direct sales channels for custom solutions or via specialized distributors stocking a broad range of Chemical Storage Market containers.

Pharmaceutical Industry and Biotechnology Companies exhibit the most stringent buying behaviors. Their purchasing decisions are critically driven by extractables and leachables profiles, USP Class VI compliance, sterility, and traceability. Purity certifications (e.g., Certificates of Analysis) are mandatory. Price sensitivity is relatively low for critical process components or API storage where product integrity and patient safety are paramount. Procurement typically involves direct relationships with manufacturers for validated products or through highly specialized distributors, often with long-term supply agreements.

Research & Academic Laboratories, representing a significant portion of the Laboratory Consumables Market, prioritize broad chemical compatibility, ease of use, reusability, and availability in various sizes. While purity is important, the level of stringency can vary from basic research to highly sensitive analytical work. Price sensitivity is moderate, as budget constraints are often present, but quality is rarely compromised for essential tasks. Procurement is commonly done through online scientific supply platforms and regional distributors for off-the-shelf solutions.

Notable shifts in buyer preference include an increasing demand for pre-cleaned and certified bottles to save laboratory time and ensure consistency, a growing interest in sustainable fluoropolymer options, and a move towards digital procurement platforms for standard product lines. The ongoing drive for higher analytical precision and process control continues to push end-users towards bottles with superior material properties and validated performance.

Investment & Funding Activity in the Fluoropolymer Bottle Market

The Fluoropolymer Bottle Market, while niche, experiences a steady stream of investment and funding activity, largely driven by the evolving needs of its high-value end-user industries and the continuous push for material innovation. Over the past two to three years, activity has concentrated on strategic acquisitions, research and development funding, and partnerships aimed at enhancing product capabilities and addressing sustainability concerns.

Mergers and Acquisitions (M&A) within the market are typically characterized by larger chemical or plastics conglomerates acquiring smaller, specialized fluoropolymer manufacturers to expand their product portfolios, gain access to proprietary material technologies, or consolidate market share. For instance, integration efforts by large players in the High-Performance Plastics Market seek to offer more comprehensive solutions to their industrial clients. While specific public M&A data directly targeting fluoropolymer bottle manufacturers is often confidential, the general trend indicates a move towards vertical integration or consolidation to optimize supply chains and achieve economies of scale.

Venture funding and private equity investments tend to gravitate towards companies developing novel fluoropolymer formulations, advanced manufacturing processes that reduce costs or enhance performance, and sustainable fluoropolymer solutions. There's a particular interest in innovations that address the recyclability challenges of traditional fluoropolymers or develop bio-based alternatives that can meet the stringent demands of existing applications. Sub-segments attracting the most capital include those focused on ultra-high purity applications for the Biopharmaceutical Market and semiconductor industry, as well as companies pioneering green fluoropolymer technologies.

Strategic partnerships are also prevalent, often involving collaborations between fluoropolymer manufacturers and end-user industry leaders. These partnerships are crucial for developing custom-engineered bottle solutions that meet highly specific performance criteria, such as enhanced barrier properties for new chemical compounds or specialized aseptic packaging for sensitive biologicals. Research collaborations with academic institutions are common for fundamental material science advancements, while partnerships with equipment manufacturers focus on developing more efficient filling and sealing technologies compatible with fluoropolymer materials. This investment landscape reflects a market that values material science excellence, application-specific innovation, and a growing commitment to environmental responsibility.

Fluoropolymer Bottle Segmentation

-

1. Material Type

- 1.1. PTFE (Polytetrafluoroethylene)

- 1.2. PFA (Perfluoroalkoxy)

- 1.3. FEP (Fluorinated Ethylene Propylene)

- 1.4. ETFE (Ethylene Tetrafluoroethylene)

- 1.5. PVDF (Polyvinylidene Fluoride)

- 1.6. PCTFE (Polychlorotrifluoroethylene)

- 1.7. ECTFE (Ethylene Chlorotrifluoroethylene)

-

2. Size

- 2.1. 100 ml

- 2.2. 250 ml

- 2.3. 500 ml

- 2.4. 1L

- 2.5. 2L

- 2.6. Others

-

3. End User Industry

- 3.1. Chemical Industry

- 3.2. Pharmaceutical Industry

- 3.3. Biotechnology Companies

- 3.4. Research & Academic Laboratories

- 3.5. Others

-

4. Distribution Channel

- 4.1. Direct Sales

- 4.2. Distributors & Wholesalers

- 4.3. Online

Fluoropolymer Bottle Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Fluoropolymer Bottle Regional Market Share

Geographic Coverage of Fluoropolymer Bottle

Fluoropolymer Bottle REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Material Type

- 5.1.1. PTFE (Polytetrafluoroethylene)

- 5.1.2. PFA (Perfluoroalkoxy)

- 5.1.3. FEP (Fluorinated Ethylene Propylene)

- 5.1.4. ETFE (Ethylene Tetrafluoroethylene)

- 5.1.5. PVDF (Polyvinylidene Fluoride)

- 5.1.6. PCTFE (Polychlorotrifluoroethylene)

- 5.1.7. ECTFE (Ethylene Chlorotrifluoroethylene)

- 5.2. Market Analysis, Insights and Forecast - by Size

- 5.2.1. 100 ml

- 5.2.2. 250 ml

- 5.2.3. 500 ml

- 5.2.4. 1L

- 5.2.5. 2L

- 5.2.6. Others

- 5.3. Market Analysis, Insights and Forecast - by End User Industry

- 5.3.1. Chemical Industry

- 5.3.2. Pharmaceutical Industry

- 5.3.3. Biotechnology Companies

- 5.3.4. Research & Academic Laboratories

- 5.3.5. Others

- 5.4. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.4.1. Direct Sales

- 5.4.2. Distributors & Wholesalers

- 5.4.3. Online

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. North America

- 5.5.2. South America

- 5.5.3. Europe

- 5.5.4. Middle East & Africa

- 5.5.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Material Type

- 6. Global Fluoropolymer Bottle Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Material Type

- 6.1.1. PTFE (Polytetrafluoroethylene)

- 6.1.2. PFA (Perfluoroalkoxy)

- 6.1.3. FEP (Fluorinated Ethylene Propylene)

- 6.1.4. ETFE (Ethylene Tetrafluoroethylene)

- 6.1.5. PVDF (Polyvinylidene Fluoride)

- 6.1.6. PCTFE (Polychlorotrifluoroethylene)

- 6.1.7. ECTFE (Ethylene Chlorotrifluoroethylene)

- 6.2. Market Analysis, Insights and Forecast - by Size

- 6.2.1. 100 ml

- 6.2.2. 250 ml

- 6.2.3. 500 ml

- 6.2.4. 1L

- 6.2.5. 2L

- 6.2.6. Others

- 6.3. Market Analysis, Insights and Forecast - by End User Industry

- 6.3.1. Chemical Industry

- 6.3.2. Pharmaceutical Industry

- 6.3.3. Biotechnology Companies

- 6.3.4. Research & Academic Laboratories

- 6.3.5. Others

- 6.4. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.4.1. Direct Sales

- 6.4.2. Distributors & Wholesalers

- 6.4.3. Online

- 6.1. Market Analysis, Insights and Forecast - by Material Type

- 7. North America Fluoropolymer Bottle Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Material Type

- 7.1.1. PTFE (Polytetrafluoroethylene)

- 7.1.2. PFA (Perfluoroalkoxy)

- 7.1.3. FEP (Fluorinated Ethylene Propylene)

- 7.1.4. ETFE (Ethylene Tetrafluoroethylene)

- 7.1.5. PVDF (Polyvinylidene Fluoride)

- 7.1.6. PCTFE (Polychlorotrifluoroethylene)

- 7.1.7. ECTFE (Ethylene Chlorotrifluoroethylene)

- 7.2. Market Analysis, Insights and Forecast - by Size

- 7.2.1. 100 ml

- 7.2.2. 250 ml

- 7.2.3. 500 ml

- 7.2.4. 1L

- 7.2.5. 2L

- 7.2.6. Others

- 7.3. Market Analysis, Insights and Forecast - by End User Industry

- 7.3.1. Chemical Industry

- 7.3.2. Pharmaceutical Industry

- 7.3.3. Biotechnology Companies

- 7.3.4. Research & Academic Laboratories

- 7.3.5. Others

- 7.4. Market Analysis, Insights and Forecast - by Distribution Channel

- 7.4.1. Direct Sales

- 7.4.2. Distributors & Wholesalers

- 7.4.3. Online

- 7.1. Market Analysis, Insights and Forecast - by Material Type

- 8. South America Fluoropolymer Bottle Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Material Type

- 8.1.1. PTFE (Polytetrafluoroethylene)

- 8.1.2. PFA (Perfluoroalkoxy)

- 8.1.3. FEP (Fluorinated Ethylene Propylene)

- 8.1.4. ETFE (Ethylene Tetrafluoroethylene)

- 8.1.5. PVDF (Polyvinylidene Fluoride)

- 8.1.6. PCTFE (Polychlorotrifluoroethylene)

- 8.1.7. ECTFE (Ethylene Chlorotrifluoroethylene)

- 8.2. Market Analysis, Insights and Forecast - by Size

- 8.2.1. 100 ml

- 8.2.2. 250 ml

- 8.2.3. 500 ml

- 8.2.4. 1L

- 8.2.5. 2L

- 8.2.6. Others

- 8.3. Market Analysis, Insights and Forecast - by End User Industry

- 8.3.1. Chemical Industry

- 8.3.2. Pharmaceutical Industry

- 8.3.3. Biotechnology Companies

- 8.3.4. Research & Academic Laboratories

- 8.3.5. Others

- 8.4. Market Analysis, Insights and Forecast - by Distribution Channel

- 8.4.1. Direct Sales

- 8.4.2. Distributors & Wholesalers

- 8.4.3. Online

- 8.1. Market Analysis, Insights and Forecast - by Material Type

- 9. Europe Fluoropolymer Bottle Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Material Type

- 9.1.1. PTFE (Polytetrafluoroethylene)

- 9.1.2. PFA (Perfluoroalkoxy)

- 9.1.3. FEP (Fluorinated Ethylene Propylene)

- 9.1.4. ETFE (Ethylene Tetrafluoroethylene)

- 9.1.5. PVDF (Polyvinylidene Fluoride)

- 9.1.6. PCTFE (Polychlorotrifluoroethylene)

- 9.1.7. ECTFE (Ethylene Chlorotrifluoroethylene)

- 9.2. Market Analysis, Insights and Forecast - by Size

- 9.2.1. 100 ml

- 9.2.2. 250 ml

- 9.2.3. 500 ml

- 9.2.4. 1L

- 9.2.5. 2L

- 9.2.6. Others

- 9.3. Market Analysis, Insights and Forecast - by End User Industry

- 9.3.1. Chemical Industry

- 9.3.2. Pharmaceutical Industry

- 9.3.3. Biotechnology Companies

- 9.3.4. Research & Academic Laboratories

- 9.3.5. Others

- 9.4. Market Analysis, Insights and Forecast - by Distribution Channel

- 9.4.1. Direct Sales

- 9.4.2. Distributors & Wholesalers

- 9.4.3. Online

- 9.1. Market Analysis, Insights and Forecast - by Material Type

- 10. Middle East & Africa Fluoropolymer Bottle Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Material Type

- 10.1.1. PTFE (Polytetrafluoroethylene)

- 10.1.2. PFA (Perfluoroalkoxy)

- 10.1.3. FEP (Fluorinated Ethylene Propylene)

- 10.1.4. ETFE (Ethylene Tetrafluoroethylene)

- 10.1.5. PVDF (Polyvinylidene Fluoride)

- 10.1.6. PCTFE (Polychlorotrifluoroethylene)

- 10.1.7. ECTFE (Ethylene Chlorotrifluoroethylene)

- 10.2. Market Analysis, Insights and Forecast - by Size

- 10.2.1. 100 ml

- 10.2.2. 250 ml

- 10.2.3. 500 ml

- 10.2.4. 1L

- 10.2.5. 2L

- 10.2.6. Others

- 10.3. Market Analysis, Insights and Forecast - by End User Industry

- 10.3.1. Chemical Industry

- 10.3.2. Pharmaceutical Industry

- 10.3.3. Biotechnology Companies

- 10.3.4. Research & Academic Laboratories

- 10.3.5. Others

- 10.4. Market Analysis, Insights and Forecast - by Distribution Channel

- 10.4.1. Direct Sales

- 10.4.2. Distributors & Wholesalers

- 10.4.3. Online

- 10.1. Market Analysis, Insights and Forecast - by Material Type

- 11. Asia Pacific Fluoropolymer Bottle Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Material Type

- 11.1.1. PTFE (Polytetrafluoroethylene)

- 11.1.2. PFA (Perfluoroalkoxy)

- 11.1.3. FEP (Fluorinated Ethylene Propylene)

- 11.1.4. ETFE (Ethylene Tetrafluoroethylene)

- 11.1.5. PVDF (Polyvinylidene Fluoride)

- 11.1.6. PCTFE (Polychlorotrifluoroethylene)

- 11.1.7. ECTFE (Ethylene Chlorotrifluoroethylene)

- 11.2. Market Analysis, Insights and Forecast - by Size

- 11.2.1. 100 ml

- 11.2.2. 250 ml

- 11.2.3. 500 ml

- 11.2.4. 1L

- 11.2.5. 2L

- 11.2.6. Others

- 11.3. Market Analysis, Insights and Forecast - by End User Industry

- 11.3.1. Chemical Industry

- 11.3.2. Pharmaceutical Industry

- 11.3.3. Biotechnology Companies

- 11.3.4. Research & Academic Laboratories

- 11.3.5. Others

- 11.4. Market Analysis, Insights and Forecast - by Distribution Channel

- 11.4.1. Direct Sales

- 11.4.2. Distributors & Wholesalers

- 11.4.3. Online

- 11.1. Market Analysis, Insights and Forecast - by Material Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Savillex Corporation

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Saint-Gobain Performance Plastics

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Thermo Fisher Scientific

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 DWK Life Sciences

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Nalgene (Thermo Fisher Scientific)

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 AMETEK Fluoropolymer Products

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Entegris Inc.

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 NICHIAS Corporation

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Zeus Industrial Products Inc.

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Fluorotherm Polymers Inc.

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Chang Zhou Feng Di Plastic Technology

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 AGC Chemicals Americas

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Daikin Industries Ltd.

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Others

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.1 Savillex Corporation

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Fluoropolymer Bottle Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Global Fluoropolymer Bottle Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: North America Fluoropolymer Bottle Revenue (billion), by Material Type 2025 & 2033

- Figure 4: North America Fluoropolymer Bottle Volume (K), by Material Type 2025 & 2033

- Figure 5: North America Fluoropolymer Bottle Revenue Share (%), by Material Type 2025 & 2033

- Figure 6: North America Fluoropolymer Bottle Volume Share (%), by Material Type 2025 & 2033

- Figure 7: North America Fluoropolymer Bottle Revenue (billion), by Size 2025 & 2033

- Figure 8: North America Fluoropolymer Bottle Volume (K), by Size 2025 & 2033

- Figure 9: North America Fluoropolymer Bottle Revenue Share (%), by Size 2025 & 2033

- Figure 10: North America Fluoropolymer Bottle Volume Share (%), by Size 2025 & 2033

- Figure 11: North America Fluoropolymer Bottle Revenue (billion), by End User Industry 2025 & 2033

- Figure 12: North America Fluoropolymer Bottle Volume (K), by End User Industry 2025 & 2033

- Figure 13: North America Fluoropolymer Bottle Revenue Share (%), by End User Industry 2025 & 2033

- Figure 14: North America Fluoropolymer Bottle Volume Share (%), by End User Industry 2025 & 2033

- Figure 15: North America Fluoropolymer Bottle Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 16: North America Fluoropolymer Bottle Volume (K), by Distribution Channel 2025 & 2033

- Figure 17: North America Fluoropolymer Bottle Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 18: North America Fluoropolymer Bottle Volume Share (%), by Distribution Channel 2025 & 2033

- Figure 19: North America Fluoropolymer Bottle Revenue (billion), by Country 2025 & 2033

- Figure 20: North America Fluoropolymer Bottle Volume (K), by Country 2025 & 2033

- Figure 21: North America Fluoropolymer Bottle Revenue Share (%), by Country 2025 & 2033

- Figure 22: North America Fluoropolymer Bottle Volume Share (%), by Country 2025 & 2033

- Figure 23: South America Fluoropolymer Bottle Revenue (billion), by Material Type 2025 & 2033

- Figure 24: South America Fluoropolymer Bottle Volume (K), by Material Type 2025 & 2033

- Figure 25: South America Fluoropolymer Bottle Revenue Share (%), by Material Type 2025 & 2033

- Figure 26: South America Fluoropolymer Bottle Volume Share (%), by Material Type 2025 & 2033

- Figure 27: South America Fluoropolymer Bottle Revenue (billion), by Size 2025 & 2033

- Figure 28: South America Fluoropolymer Bottle Volume (K), by Size 2025 & 2033

- Figure 29: South America Fluoropolymer Bottle Revenue Share (%), by Size 2025 & 2033

- Figure 30: South America Fluoropolymer Bottle Volume Share (%), by Size 2025 & 2033

- Figure 31: South America Fluoropolymer Bottle Revenue (billion), by End User Industry 2025 & 2033

- Figure 32: South America Fluoropolymer Bottle Volume (K), by End User Industry 2025 & 2033

- Figure 33: South America Fluoropolymer Bottle Revenue Share (%), by End User Industry 2025 & 2033

- Figure 34: South America Fluoropolymer Bottle Volume Share (%), by End User Industry 2025 & 2033

- Figure 35: South America Fluoropolymer Bottle Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 36: South America Fluoropolymer Bottle Volume (K), by Distribution Channel 2025 & 2033

- Figure 37: South America Fluoropolymer Bottle Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 38: South America Fluoropolymer Bottle Volume Share (%), by Distribution Channel 2025 & 2033

- Figure 39: South America Fluoropolymer Bottle Revenue (billion), by Country 2025 & 2033

- Figure 40: South America Fluoropolymer Bottle Volume (K), by Country 2025 & 2033

- Figure 41: South America Fluoropolymer Bottle Revenue Share (%), by Country 2025 & 2033

- Figure 42: South America Fluoropolymer Bottle Volume Share (%), by Country 2025 & 2033

- Figure 43: Europe Fluoropolymer Bottle Revenue (billion), by Material Type 2025 & 2033

- Figure 44: Europe Fluoropolymer Bottle Volume (K), by Material Type 2025 & 2033

- Figure 45: Europe Fluoropolymer Bottle Revenue Share (%), by Material Type 2025 & 2033

- Figure 46: Europe Fluoropolymer Bottle Volume Share (%), by Material Type 2025 & 2033

- Figure 47: Europe Fluoropolymer Bottle Revenue (billion), by Size 2025 & 2033

- Figure 48: Europe Fluoropolymer Bottle Volume (K), by Size 2025 & 2033

- Figure 49: Europe Fluoropolymer Bottle Revenue Share (%), by Size 2025 & 2033

- Figure 50: Europe Fluoropolymer Bottle Volume Share (%), by Size 2025 & 2033

- Figure 51: Europe Fluoropolymer Bottle Revenue (billion), by End User Industry 2025 & 2033

- Figure 52: Europe Fluoropolymer Bottle Volume (K), by End User Industry 2025 & 2033

- Figure 53: Europe Fluoropolymer Bottle Revenue Share (%), by End User Industry 2025 & 2033

- Figure 54: Europe Fluoropolymer Bottle Volume Share (%), by End User Industry 2025 & 2033

- Figure 55: Europe Fluoropolymer Bottle Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 56: Europe Fluoropolymer Bottle Volume (K), by Distribution Channel 2025 & 2033

- Figure 57: Europe Fluoropolymer Bottle Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 58: Europe Fluoropolymer Bottle Volume Share (%), by Distribution Channel 2025 & 2033

- Figure 59: Europe Fluoropolymer Bottle Revenue (billion), by Country 2025 & 2033

- Figure 60: Europe Fluoropolymer Bottle Volume (K), by Country 2025 & 2033

- Figure 61: Europe Fluoropolymer Bottle Revenue Share (%), by Country 2025 & 2033

- Figure 62: Europe Fluoropolymer Bottle Volume Share (%), by Country 2025 & 2033

- Figure 63: Middle East & Africa Fluoropolymer Bottle Revenue (billion), by Material Type 2025 & 2033

- Figure 64: Middle East & Africa Fluoropolymer Bottle Volume (K), by Material Type 2025 & 2033

- Figure 65: Middle East & Africa Fluoropolymer Bottle Revenue Share (%), by Material Type 2025 & 2033

- Figure 66: Middle East & Africa Fluoropolymer Bottle Volume Share (%), by Material Type 2025 & 2033

- Figure 67: Middle East & Africa Fluoropolymer Bottle Revenue (billion), by Size 2025 & 2033

- Figure 68: Middle East & Africa Fluoropolymer Bottle Volume (K), by Size 2025 & 2033

- Figure 69: Middle East & Africa Fluoropolymer Bottle Revenue Share (%), by Size 2025 & 2033

- Figure 70: Middle East & Africa Fluoropolymer Bottle Volume Share (%), by Size 2025 & 2033

- Figure 71: Middle East & Africa Fluoropolymer Bottle Revenue (billion), by End User Industry 2025 & 2033

- Figure 72: Middle East & Africa Fluoropolymer Bottle Volume (K), by End User Industry 2025 & 2033

- Figure 73: Middle East & Africa Fluoropolymer Bottle Revenue Share (%), by End User Industry 2025 & 2033

- Figure 74: Middle East & Africa Fluoropolymer Bottle Volume Share (%), by End User Industry 2025 & 2033

- Figure 75: Middle East & Africa Fluoropolymer Bottle Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 76: Middle East & Africa Fluoropolymer Bottle Volume (K), by Distribution Channel 2025 & 2033

- Figure 77: Middle East & Africa Fluoropolymer Bottle Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 78: Middle East & Africa Fluoropolymer Bottle Volume Share (%), by Distribution Channel 2025 & 2033

- Figure 79: Middle East & Africa Fluoropolymer Bottle Revenue (billion), by Country 2025 & 2033

- Figure 80: Middle East & Africa Fluoropolymer Bottle Volume (K), by Country 2025 & 2033

- Figure 81: Middle East & Africa Fluoropolymer Bottle Revenue Share (%), by Country 2025 & 2033

- Figure 82: Middle East & Africa Fluoropolymer Bottle Volume Share (%), by Country 2025 & 2033

- Figure 83: Asia Pacific Fluoropolymer Bottle Revenue (billion), by Material Type 2025 & 2033

- Figure 84: Asia Pacific Fluoropolymer Bottle Volume (K), by Material Type 2025 & 2033

- Figure 85: Asia Pacific Fluoropolymer Bottle Revenue Share (%), by Material Type 2025 & 2033

- Figure 86: Asia Pacific Fluoropolymer Bottle Volume Share (%), by Material Type 2025 & 2033

- Figure 87: Asia Pacific Fluoropolymer Bottle Revenue (billion), by Size 2025 & 2033

- Figure 88: Asia Pacific Fluoropolymer Bottle Volume (K), by Size 2025 & 2033

- Figure 89: Asia Pacific Fluoropolymer Bottle Revenue Share (%), by Size 2025 & 2033

- Figure 90: Asia Pacific Fluoropolymer Bottle Volume Share (%), by Size 2025 & 2033

- Figure 91: Asia Pacific Fluoropolymer Bottle Revenue (billion), by End User Industry 2025 & 2033

- Figure 92: Asia Pacific Fluoropolymer Bottle Volume (K), by End User Industry 2025 & 2033

- Figure 93: Asia Pacific Fluoropolymer Bottle Revenue Share (%), by End User Industry 2025 & 2033

- Figure 94: Asia Pacific Fluoropolymer Bottle Volume Share (%), by End User Industry 2025 & 2033

- Figure 95: Asia Pacific Fluoropolymer Bottle Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 96: Asia Pacific Fluoropolymer Bottle Volume (K), by Distribution Channel 2025 & 2033

- Figure 97: Asia Pacific Fluoropolymer Bottle Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 98: Asia Pacific Fluoropolymer Bottle Volume Share (%), by Distribution Channel 2025 & 2033

- Figure 99: Asia Pacific Fluoropolymer Bottle Revenue (billion), by Country 2025 & 2033

- Figure 100: Asia Pacific Fluoropolymer Bottle Volume (K), by Country 2025 & 2033

- Figure 101: Asia Pacific Fluoropolymer Bottle Revenue Share (%), by Country 2025 & 2033

- Figure 102: Asia Pacific Fluoropolymer Bottle Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Fluoropolymer Bottle Revenue billion Forecast, by Material Type 2020 & 2033

- Table 2: Global Fluoropolymer Bottle Volume K Forecast, by Material Type 2020 & 2033

- Table 3: Global Fluoropolymer Bottle Revenue billion Forecast, by Size 2020 & 2033

- Table 4: Global Fluoropolymer Bottle Volume K Forecast, by Size 2020 & 2033

- Table 5: Global Fluoropolymer Bottle Revenue billion Forecast, by End User Industry 2020 & 2033

- Table 6: Global Fluoropolymer Bottle Volume K Forecast, by End User Industry 2020 & 2033

- Table 7: Global Fluoropolymer Bottle Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 8: Global Fluoropolymer Bottle Volume K Forecast, by Distribution Channel 2020 & 2033

- Table 9: Global Fluoropolymer Bottle Revenue billion Forecast, by Region 2020 & 2033

- Table 10: Global Fluoropolymer Bottle Volume K Forecast, by Region 2020 & 2033

- Table 11: Global Fluoropolymer Bottle Revenue billion Forecast, by Material Type 2020 & 2033

- Table 12: Global Fluoropolymer Bottle Volume K Forecast, by Material Type 2020 & 2033

- Table 13: Global Fluoropolymer Bottle Revenue billion Forecast, by Size 2020 & 2033

- Table 14: Global Fluoropolymer Bottle Volume K Forecast, by Size 2020 & 2033

- Table 15: Global Fluoropolymer Bottle Revenue billion Forecast, by End User Industry 2020 & 2033

- Table 16: Global Fluoropolymer Bottle Volume K Forecast, by End User Industry 2020 & 2033

- Table 17: Global Fluoropolymer Bottle Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 18: Global Fluoropolymer Bottle Volume K Forecast, by Distribution Channel 2020 & 2033

- Table 19: Global Fluoropolymer Bottle Revenue billion Forecast, by Country 2020 & 2033

- Table 20: Global Fluoropolymer Bottle Volume K Forecast, by Country 2020 & 2033

- Table 21: United States Fluoropolymer Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: United States Fluoropolymer Bottle Volume (K) Forecast, by Application 2020 & 2033

- Table 23: Canada Fluoropolymer Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Canada Fluoropolymer Bottle Volume (K) Forecast, by Application 2020 & 2033

- Table 25: Mexico Fluoropolymer Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Mexico Fluoropolymer Bottle Volume (K) Forecast, by Application 2020 & 2033

- Table 27: Global Fluoropolymer Bottle Revenue billion Forecast, by Material Type 2020 & 2033

- Table 28: Global Fluoropolymer Bottle Volume K Forecast, by Material Type 2020 & 2033

- Table 29: Global Fluoropolymer Bottle Revenue billion Forecast, by Size 2020 & 2033

- Table 30: Global Fluoropolymer Bottle Volume K Forecast, by Size 2020 & 2033

- Table 31: Global Fluoropolymer Bottle Revenue billion Forecast, by End User Industry 2020 & 2033

- Table 32: Global Fluoropolymer Bottle Volume K Forecast, by End User Industry 2020 & 2033

- Table 33: Global Fluoropolymer Bottle Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 34: Global Fluoropolymer Bottle Volume K Forecast, by Distribution Channel 2020 & 2033

- Table 35: Global Fluoropolymer Bottle Revenue billion Forecast, by Country 2020 & 2033

- Table 36: Global Fluoropolymer Bottle Volume K Forecast, by Country 2020 & 2033

- Table 37: Brazil Fluoropolymer Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: Brazil Fluoropolymer Bottle Volume (K) Forecast, by Application 2020 & 2033

- Table 39: Argentina Fluoropolymer Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 40: Argentina Fluoropolymer Bottle Volume (K) Forecast, by Application 2020 & 2033

- Table 41: Rest of South America Fluoropolymer Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Rest of South America Fluoropolymer Bottle Volume (K) Forecast, by Application 2020 & 2033

- Table 43: Global Fluoropolymer Bottle Revenue billion Forecast, by Material Type 2020 & 2033

- Table 44: Global Fluoropolymer Bottle Volume K Forecast, by Material Type 2020 & 2033

- Table 45: Global Fluoropolymer Bottle Revenue billion Forecast, by Size 2020 & 2033

- Table 46: Global Fluoropolymer Bottle Volume K Forecast, by Size 2020 & 2033

- Table 47: Global Fluoropolymer Bottle Revenue billion Forecast, by End User Industry 2020 & 2033

- Table 48: Global Fluoropolymer Bottle Volume K Forecast, by End User Industry 2020 & 2033

- Table 49: Global Fluoropolymer Bottle Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 50: Global Fluoropolymer Bottle Volume K Forecast, by Distribution Channel 2020 & 2033

- Table 51: Global Fluoropolymer Bottle Revenue billion Forecast, by Country 2020 & 2033

- Table 52: Global Fluoropolymer Bottle Volume K Forecast, by Country 2020 & 2033

- Table 53: United Kingdom Fluoropolymer Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 54: United Kingdom Fluoropolymer Bottle Volume (K) Forecast, by Application 2020 & 2033

- Table 55: Germany Fluoropolymer Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 56: Germany Fluoropolymer Bottle Volume (K) Forecast, by Application 2020 & 2033

- Table 57: France Fluoropolymer Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 58: France Fluoropolymer Bottle Volume (K) Forecast, by Application 2020 & 2033

- Table 59: Italy Fluoropolymer Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 60: Italy Fluoropolymer Bottle Volume (K) Forecast, by Application 2020 & 2033

- Table 61: Spain Fluoropolymer Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 62: Spain Fluoropolymer Bottle Volume (K) Forecast, by Application 2020 & 2033

- Table 63: Russia Fluoropolymer Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 64: Russia Fluoropolymer Bottle Volume (K) Forecast, by Application 2020 & 2033

- Table 65: Benelux Fluoropolymer Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 66: Benelux Fluoropolymer Bottle Volume (K) Forecast, by Application 2020 & 2033

- Table 67: Nordics Fluoropolymer Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 68: Nordics Fluoropolymer Bottle Volume (K) Forecast, by Application 2020 & 2033

- Table 69: Rest of Europe Fluoropolymer Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 70: Rest of Europe Fluoropolymer Bottle Volume (K) Forecast, by Application 2020 & 2033

- Table 71: Global Fluoropolymer Bottle Revenue billion Forecast, by Material Type 2020 & 2033

- Table 72: Global Fluoropolymer Bottle Volume K Forecast, by Material Type 2020 & 2033

- Table 73: Global Fluoropolymer Bottle Revenue billion Forecast, by Size 2020 & 2033

- Table 74: Global Fluoropolymer Bottle Volume K Forecast, by Size 2020 & 2033

- Table 75: Global Fluoropolymer Bottle Revenue billion Forecast, by End User Industry 2020 & 2033

- Table 76: Global Fluoropolymer Bottle Volume K Forecast, by End User Industry 2020 & 2033

- Table 77: Global Fluoropolymer Bottle Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 78: Global Fluoropolymer Bottle Volume K Forecast, by Distribution Channel 2020 & 2033

- Table 79: Global Fluoropolymer Bottle Revenue billion Forecast, by Country 2020 & 2033

- Table 80: Global Fluoropolymer Bottle Volume K Forecast, by Country 2020 & 2033

- Table 81: Turkey Fluoropolymer Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 82: Turkey Fluoropolymer Bottle Volume (K) Forecast, by Application 2020 & 2033

- Table 83: Israel Fluoropolymer Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 84: Israel Fluoropolymer Bottle Volume (K) Forecast, by Application 2020 & 2033

- Table 85: GCC Fluoropolymer Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 86: GCC Fluoropolymer Bottle Volume (K) Forecast, by Application 2020 & 2033

- Table 87: North Africa Fluoropolymer Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 88: North Africa Fluoropolymer Bottle Volume (K) Forecast, by Application 2020 & 2033

- Table 89: South Africa Fluoropolymer Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 90: South Africa Fluoropolymer Bottle Volume (K) Forecast, by Application 2020 & 2033

- Table 91: Rest of Middle East & Africa Fluoropolymer Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 92: Rest of Middle East & Africa Fluoropolymer Bottle Volume (K) Forecast, by Application 2020 & 2033

- Table 93: Global Fluoropolymer Bottle Revenue billion Forecast, by Material Type 2020 & 2033

- Table 94: Global Fluoropolymer Bottle Volume K Forecast, by Material Type 2020 & 2033

- Table 95: Global Fluoropolymer Bottle Revenue billion Forecast, by Size 2020 & 2033

- Table 96: Global Fluoropolymer Bottle Volume K Forecast, by Size 2020 & 2033

- Table 97: Global Fluoropolymer Bottle Revenue billion Forecast, by End User Industry 2020 & 2033

- Table 98: Global Fluoropolymer Bottle Volume K Forecast, by End User Industry 2020 & 2033

- Table 99: Global Fluoropolymer Bottle Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 100: Global Fluoropolymer Bottle Volume K Forecast, by Distribution Channel 2020 & 2033

- Table 101: Global Fluoropolymer Bottle Revenue billion Forecast, by Country 2020 & 2033

- Table 102: Global Fluoropolymer Bottle Volume K Forecast, by Country 2020 & 2033

- Table 103: China Fluoropolymer Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 104: China Fluoropolymer Bottle Volume (K) Forecast, by Application 2020 & 2033

- Table 105: India Fluoropolymer Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 106: India Fluoropolymer Bottle Volume (K) Forecast, by Application 2020 & 2033

- Table 107: Japan Fluoropolymer Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 108: Japan Fluoropolymer Bottle Volume (K) Forecast, by Application 2020 & 2033

- Table 109: South Korea Fluoropolymer Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 110: South Korea Fluoropolymer Bottle Volume (K) Forecast, by Application 2020 & 2033

- Table 111: ASEAN Fluoropolymer Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 112: ASEAN Fluoropolymer Bottle Volume (K) Forecast, by Application 2020 & 2033

- Table 113: Oceania Fluoropolymer Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 114: Oceania Fluoropolymer Bottle Volume (K) Forecast, by Application 2020 & 2033

- Table 115: Rest of Asia Pacific Fluoropolymer Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 116: Rest of Asia Pacific Fluoropolymer Bottle Volume (K) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Fluoropolymer Bottle?

The projected CAGR is approximately 6.9%.

2. Which companies are prominent players in the Fluoropolymer Bottle?

Key companies in the market include Savillex Corporation, Saint-Gobain Performance Plastics, Thermo Fisher Scientific, DWK Life Sciences, Nalgene (Thermo Fisher Scientific), AMETEK Fluoropolymer Products, Entegris, Inc., NICHIAS Corporation, Zeus Industrial Products, Inc., Fluorotherm Polymers, Inc., Chang Zhou Feng Di Plastic Technology, AGC Chemicals Americas, Daikin Industries Ltd., Others.

3. What are the main segments of the Fluoropolymer Bottle?

The market segments include Material Type, Size, End User Industry, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.8 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Fluoropolymer Bottle," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Fluoropolymer Bottle report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Fluoropolymer Bottle?

To stay informed about further developments, trends, and reports in the Fluoropolymer Bottle, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence