Key Insights

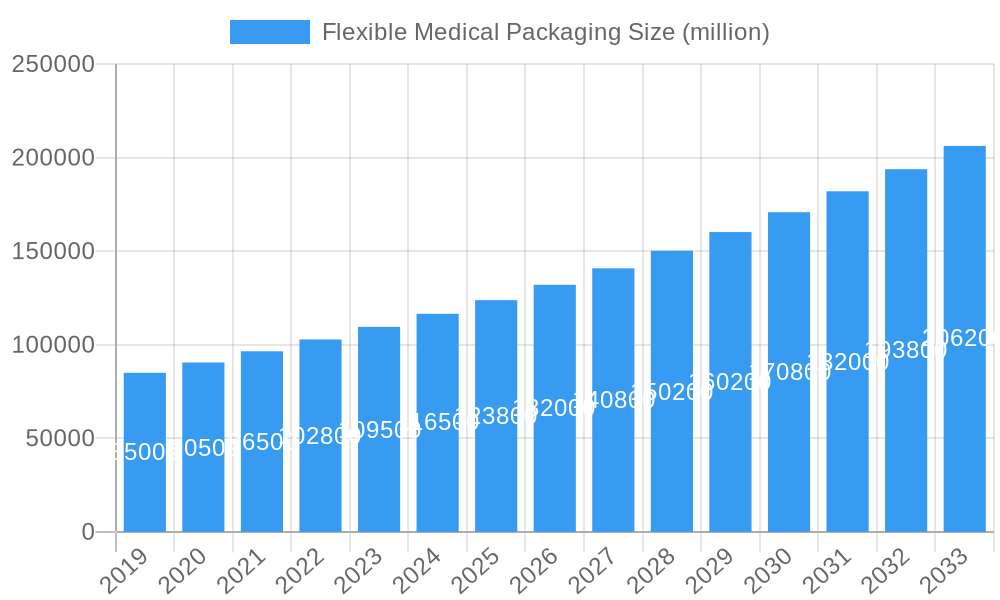

The global Flexible Medical Packaging market is projected to experience significant growth, reaching an estimated 52.85 billion by 2025. This market is anticipated to expand at a Compound Annual Growth Rate (CAGR) of 5.7% from 2025 to 2033. The surge in demand for sterile, safe, and convenient packaging solutions across pharmaceutical, medical device, and implant manufacturing sectors is a key growth driver. Factors such as the increasing prevalence of chronic diseases, an aging global population, and continuous healthcare innovation necessitate advanced packaging to ensure product integrity and patient safety.

Flexible Medical Packaging Market Size (In Billion)

The rise of minimally invasive procedures and home healthcare solutions is also fueling the demand for flexible packaging that offers enhanced portability and ease of use. Evolving regulatory landscapes and a growing emphasis on sustainable packaging materials are influencing manufacturers to invest in eco-friendly alternatives like advanced plastics and specialized papers. Key market trends include the development of advanced barrier properties to protect sensitive medical products and innovations in sterilization-compatible materials.

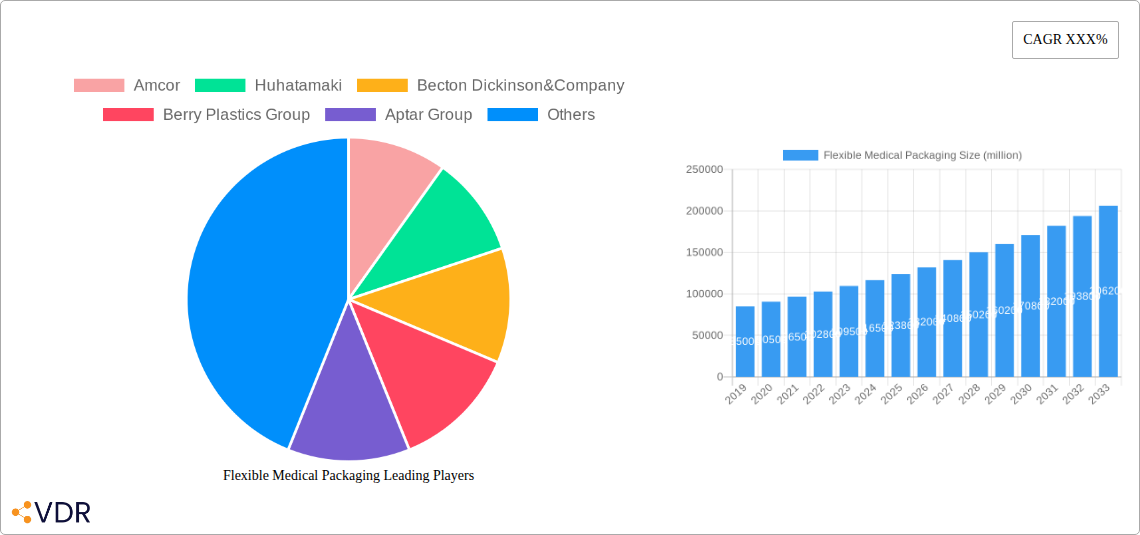

Flexible Medical Packaging Company Market Share

While the market benefits from strong demand, challenges such as rising raw material costs and the complexity of recycling multi-layered flexible packaging need to be addressed. However, the adoption of lightweight, space-efficient designs and advancements in printing and labeling for improved traceability are expected to mitigate these challenges. The pharmaceutical manufacturing segment holds a dominant share, followed by medical device manufacturing. Plastic-based flexible packaging leads in terms of type due to its versatility, durability, and cost-effectiveness. North America and Europe are mature markets, while the Asia Pacific region is expected to witness the fastest growth due to expanding healthcare infrastructure and increasing disposable incomes.

This report offers an in-depth analysis of the global Flexible Medical Packaging market, focusing on market dynamics, growth trends, regional insights, product landscape, key drivers, barriers, opportunities, and emerging players. The study covers the period from 2019 to 2033, with 2025 as the base year and a forecast period from 2025 to 2033, building on historical data from 2019–2024.

Flexible Medical Packaging Market Dynamics & Structure

The flexible medical packaging market exhibits a dynamic and moderately consolidated structure. Leading companies like Amcor, Huhatamaki, and Becton Dickinson & Company command significant market shares, driven by extensive R&D investments and broad product portfolios. Technological innovation is a primary driver, with advancements in material science leading to enhanced barrier properties, sterilization compatibility, and user-friendliness for pharmaceutical and medical device packaging. Regulatory frameworks, particularly those from the FDA and EMA, play a crucial role in shaping product development and market entry, demanding stringent adherence to safety and efficacy standards. Competitive product substitutes, while present in some niche applications, are largely outpaced by the superior flexibility, light-weighting, and cost-effectiveness of flexible packaging solutions. End-user demographics, characterized by an aging global population and rising prevalence of chronic diseases, fuel the demand for advanced medical packaging to ensure drug and device integrity. Mergers and acquisitions are a notable trend, with companies consolidating to expand their geographical reach, technological capabilities, and product offerings. For instance, recent M&A activity has seen market players acquiring specialized printing and lamination companies to vertically integrate their supply chains.

- Market Concentration: Moderately consolidated with key global players.

- Technological Innovation Drivers: Enhanced barrier properties, sterilization compatibility, smart packaging solutions.

- Regulatory Frameworks: Strict adherence to FDA, EMA, and other regional health authority guidelines.

- Competitive Product Substitutes: Limited, but include rigid packaging in certain high-barrier applications.

- End-User Demographics: Aging population, increasing chronic disease rates, growing demand for home healthcare.

- M&A Trends: Strategic acquisitions for market expansion and capability enhancement.

Flexible Medical Packaging Growth Trends & Insights

The Flexible Medical Packaging Market is projected to experience robust growth, driven by an expanding global healthcare expenditure and an increasing demand for advanced pharmaceutical and medical device solutions. Market size is expected to witness a significant evolution, with a projected Compound Annual Growth Rate (CAGR) of approximately 6.5% during the forecast period (2025–2033). This growth is underpinned by escalating adoption rates of innovative drug delivery systems and minimally invasive medical devices, both of which rely heavily on sophisticated flexible packaging to maintain sterility, protect sensitive components, and ensure optimal shelf life. Technological disruptions, such as the development of advanced polymers offering superior chemical resistance and puncture strength, are reshaping product offerings and creating new market opportunities. Furthermore, shifting consumer behavior towards convenient, pre-packaged, and single-use medical products, amplified by recent global health events, is accelerating the demand for sterile, easy-to-open flexible packaging formats. The penetration of advanced sterile barrier systems for complex medical devices is also a key growth indicator, reflecting the industry's commitment to patient safety and product integrity. The market for child-resistant flexible packaging solutions for pharmaceuticals is also seeing substantial growth, responding to regulatory demands and public safety concerns.

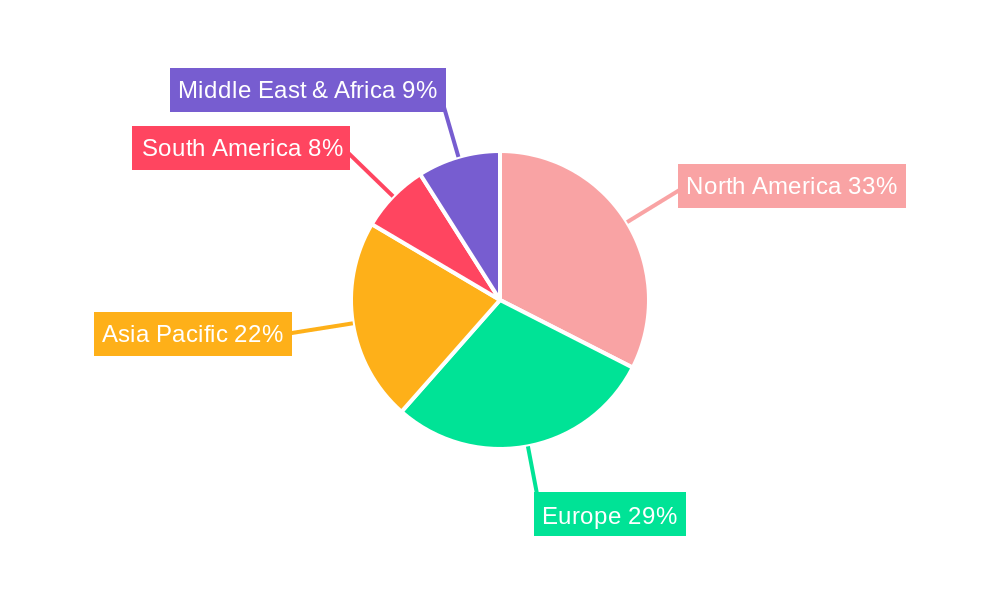

Dominant Regions, Countries, or Segments in Flexible Medical Packaging

The North America region, particularly the United States, is a dominant force in the Flexible Medical Packaging Market, primarily driven by its advanced healthcare infrastructure, high per capita healthcare spending, and a strong presence of leading pharmaceutical and medical device manufacturers. The Pharmaceutical Manufacturing segment within this region is a key growth engine, accounting for an estimated 45% of the total market share. This dominance is further fueled by substantial investments in research and development for novel therapeutics and biopharmaceuticals, all requiring high-performance, sterile flexible packaging solutions. Government initiatives promoting domestic manufacturing and supply chain resilience also contribute to the region's leadership.

In terms of Type, Plastic flexible packaging, encompassing materials like polyethylene (PE), polypropylene (PP), and specialized co-extrusions, holds the largest market share, estimated at 70%. This is attributed to its versatility, excellent barrier properties against moisture and oxygen, and cost-effectiveness in high-volume production. The growing demand for advanced sterilization techniques, such as gamma irradiation and ethylene oxide (EtO) sterilization, further solidifies the position of plastics that are compatible with these processes.

Key drivers for this regional and segmental dominance include:

- Economic Policies: Favorable regulatory environments and government support for healthcare innovation.

- Infrastructure: World-class manufacturing facilities and advanced logistics networks.

- Research & Development: Significant investments in pharmaceutical and medical device R&D, driving demand for specialized packaging.

- End-User Demand: High patient population and prevalence of chronic diseases necessitating advanced medical treatments and devices.

- Technological Advancements: Early adoption of cutting-edge packaging materials and technologies.

The Medical Device Manufacturing segment also exhibits significant growth, driven by the increasing demand for implantable devices and diagnostic kits, which require sterile, high-barrier flexible packaging to maintain product integrity and ensure patient safety. The Implant Manufacturing sub-segment, in particular, shows promising growth due to advancements in biomaterials and surgical techniques.

Flexible Medical Packaging Product Landscape

The flexible medical packaging product landscape is characterized by innovation focused on enhanced barrier protection, improved sterilization compatibility, and patient-centric design. Key product innovations include advanced multi-layer films with superior oxygen and moisture barriers, tamper-evident sealing technologies, and specialized pouches for lyophilized drugs and sensitive biologics. Applications span a wide range, from sterile pouches for surgical instruments and single-use medical devices to pharmaceutical blister packs and intravenous fluid bags. Performance metrics are paramount, with a focus on tensile strength, tear resistance, seal integrity, and resistance to chemical degradation during sterilization and transport. Unique selling propositions often lie in the ability to customize packaging for specific product requirements, such as extended shelf life for complex biologics or the integration of features like easy-peel openings and resealable closures for patient convenience. Technological advancements are also pushing towards smart packaging solutions that can indicate temperature excursions or product integrity.

Key Drivers, Barriers & Challenges in Flexible Medical Packaging

Key Drivers:

- Technological Advancements: Development of novel materials with superior barrier properties, enhanced sterilization compatibility, and antimicrobial features.

- Rising Healthcare Expenditure: Increased global spending on pharmaceuticals and medical devices fuels demand for advanced packaging.

- Growing Demand for Sterile Products: The necessity for sterile packaging for drugs, devices, and implants to prevent infections and ensure patient safety.

- Convenience and Patient-Centric Design: Demand for easy-to-open, single-use, and child-resistant packaging solutions.

Barriers & Challenges:

- Stringent Regulatory Compliance: Navigating complex and evolving regulations from bodies like the FDA and EMA, impacting product development timelines and costs.

- Supply Chain Disruptions: Volatility in raw material prices and availability, coupled with logistical challenges, can impact production and costs.

- Environmental Concerns: Growing pressure for sustainable packaging solutions, requiring innovation in recyclable or biodegradable materials without compromising performance.

- High R&D Costs: Significant investment is required for the development and validation of new medical packaging materials and technologies.

- Counterfeiting Concerns: The need for robust anti-counterfeiting measures integrated into packaging solutions.

Emerging Opportunities in Flexible Medical Packaging

Emerging opportunities in the flexible medical packaging market lie in the development of intelligent and sustainable packaging solutions. The integration of RFID tags and IoT capabilities for real-time tracking and condition monitoring of pharmaceuticals and medical devices presents a significant growth avenue. Furthermore, the increasing demand for personalized medicine necessitates the development of specialized, small-batch flexible packaging tailored to individual patient needs. Untapped markets in emerging economies with growing healthcare access offer substantial expansion potential. The drive towards a circular economy is also creating opportunities for innovative biodegradable and compostable flexible packaging materials that meet stringent medical requirements.

Growth Accelerators in the Flexible Medical Packaging Industry

Growth in the flexible medical packaging industry is being significantly accelerated by several key factors. Technological breakthroughs in advanced polymer science are enabling the creation of thinner, stronger, and more sustainable packaging materials with superior barrier properties. Strategic partnerships between packaging manufacturers and pharmaceutical/medical device companies are fostering co-development of customized solutions, leading to faster market entry and greater product innovation. Furthermore, market expansion strategies, including focusing on emerging economies with rapidly developing healthcare sectors, are unlocking new revenue streams and driving demand. The increasing adoption of contract manufacturing organizations (CMOs) also indirectly boosts demand for flexible packaging as these organizations scale their operations to meet global pharmaceutical needs.

Key Players Shaping the Flexible Medical Packaging Market

- Amcor

- Huhatamaki

- Becton Dickinson & Company

- Berry Plastics Group

- Aptar Group

- Datwyler Holdings

- Westrock Company

- Mondi Group

- Winpak

- Glenroy

Notable Milestones in Flexible Medical Packaging Sector

- 2019: Introduction of advanced recyclable barrier films by major manufacturers, addressing growing environmental concerns.

- 2020: Increased demand for sterile barrier packaging for critical medical supplies and personal protective equipment (PPE) during the global pandemic.

- 2021: Launch of smart packaging solutions with integrated temperature monitoring for sensitive biologics.

- 2022: Significant investment in sustainable materials research and development by leading packaging companies.

- 2023: Advancements in child-resistant flexible packaging designs meeting new regulatory standards.

- 2024: Expansion of flexible packaging manufacturing capabilities in emerging markets to cater to growing healthcare demand.

In-Depth Flexible Medical Packaging Market Outlook

The future outlook for the flexible medical packaging market is exceptionally promising, driven by persistent global healthcare demands and continuous technological innovation. Growth accelerators such as the development of advanced material science, enabling lighter yet more protective packaging, and the increasing integration of digital technologies for supply chain transparency and product authentication, will be pivotal. Strategic partnerships between packaging converters and healthcare giants will continue to drive the development of bespoke solutions for complex pharmaceutical and medical device needs, accelerating market penetration. Furthermore, the burgeoning demand for personalized medicine and the expanding reach of home healthcare will create significant opportunities for specialized, user-friendly flexible packaging formats. The industry is poised for sustained expansion as it adapts to evolving regulatory landscapes and embraces sustainability, ensuring its critical role in safeguarding global health.

Flexible Medical Packaging Segmentation

-

1. Application

- 1.1. Pharmaceutical Manufacturing

- 1.2. Medical Device Manufacturing

- 1.3. Implant Manufacturing

- 1.4. Others

-

2. Type

- 2.1. Plastic

- 2.2. Paper

- 2.3. Aluminum

- 2.4. Others

Flexible Medical Packaging Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Flexible Medical Packaging Regional Market Share

Geographic Coverage of Flexible Medical Packaging

Flexible Medical Packaging REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Pharmaceutical Manufacturing

- 5.1.2. Medical Device Manufacturing

- 5.1.3. Implant Manufacturing

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Plastic

- 5.2.2. Paper

- 5.2.3. Aluminum

- 5.2.4. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Flexible Medical Packaging Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Pharmaceutical Manufacturing

- 6.1.2. Medical Device Manufacturing

- 6.1.3. Implant Manufacturing

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Plastic

- 6.2.2. Paper

- 6.2.3. Aluminum

- 6.2.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Flexible Medical Packaging Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Pharmaceutical Manufacturing

- 7.1.2. Medical Device Manufacturing

- 7.1.3. Implant Manufacturing

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Plastic

- 7.2.2. Paper

- 7.2.3. Aluminum

- 7.2.4. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Flexible Medical Packaging Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Pharmaceutical Manufacturing

- 8.1.2. Medical Device Manufacturing

- 8.1.3. Implant Manufacturing

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Plastic

- 8.2.2. Paper

- 8.2.3. Aluminum

- 8.2.4. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Flexible Medical Packaging Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Pharmaceutical Manufacturing

- 9.1.2. Medical Device Manufacturing

- 9.1.3. Implant Manufacturing

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Plastic

- 9.2.2. Paper

- 9.2.3. Aluminum

- 9.2.4. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Flexible Medical Packaging Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Pharmaceutical Manufacturing

- 10.1.2. Medical Device Manufacturing

- 10.1.3. Implant Manufacturing

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Plastic

- 10.2.2. Paper

- 10.2.3. Aluminum

- 10.2.4. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Flexible Medical Packaging Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Pharmaceutical Manufacturing

- 11.1.2. Medical Device Manufacturing

- 11.1.3. Implant Manufacturing

- 11.1.4. Others

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. Plastic

- 11.2.2. Paper

- 11.2.3. Aluminum

- 11.2.4. Others

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Amcor

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Huhatamaki

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Becton Dickinson&Company

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Berry Plastics Group

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Aptar Group

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Datwyler Holdings

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Westrock Company

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Mondi Group

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Winpak

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Glenroy

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Amcor

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Flexible Medical Packaging Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Flexible Medical Packaging Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Flexible Medical Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Flexible Medical Packaging Revenue (billion), by Type 2025 & 2033

- Figure 5: North America Flexible Medical Packaging Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Flexible Medical Packaging Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Flexible Medical Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Flexible Medical Packaging Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Flexible Medical Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Flexible Medical Packaging Revenue (billion), by Type 2025 & 2033

- Figure 11: South America Flexible Medical Packaging Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Flexible Medical Packaging Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Flexible Medical Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Flexible Medical Packaging Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Flexible Medical Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Flexible Medical Packaging Revenue (billion), by Type 2025 & 2033

- Figure 17: Europe Flexible Medical Packaging Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Flexible Medical Packaging Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Flexible Medical Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Flexible Medical Packaging Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Flexible Medical Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Flexible Medical Packaging Revenue (billion), by Type 2025 & 2033

- Figure 23: Middle East & Africa Flexible Medical Packaging Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Flexible Medical Packaging Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Flexible Medical Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Flexible Medical Packaging Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Flexible Medical Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Flexible Medical Packaging Revenue (billion), by Type 2025 & 2033

- Figure 29: Asia Pacific Flexible Medical Packaging Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Flexible Medical Packaging Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Flexible Medical Packaging Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Flexible Medical Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Flexible Medical Packaging Revenue billion Forecast, by Type 2020 & 2033

- Table 3: Global Flexible Medical Packaging Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Flexible Medical Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Flexible Medical Packaging Revenue billion Forecast, by Type 2020 & 2033

- Table 6: Global Flexible Medical Packaging Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Flexible Medical Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Flexible Medical Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Flexible Medical Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Flexible Medical Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Flexible Medical Packaging Revenue billion Forecast, by Type 2020 & 2033

- Table 12: Global Flexible Medical Packaging Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Flexible Medical Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Flexible Medical Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Flexible Medical Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Flexible Medical Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Flexible Medical Packaging Revenue billion Forecast, by Type 2020 & 2033

- Table 18: Global Flexible Medical Packaging Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Flexible Medical Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Flexible Medical Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Flexible Medical Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Flexible Medical Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Flexible Medical Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Flexible Medical Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Flexible Medical Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Flexible Medical Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Flexible Medical Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Flexible Medical Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Flexible Medical Packaging Revenue billion Forecast, by Type 2020 & 2033

- Table 30: Global Flexible Medical Packaging Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Flexible Medical Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Flexible Medical Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Flexible Medical Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Flexible Medical Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Flexible Medical Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Flexible Medical Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Flexible Medical Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Flexible Medical Packaging Revenue billion Forecast, by Type 2020 & 2033

- Table 39: Global Flexible Medical Packaging Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Flexible Medical Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Flexible Medical Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Flexible Medical Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Flexible Medical Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Flexible Medical Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Flexible Medical Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Flexible Medical Packaging Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Flexible Medical Packaging?

The projected CAGR is approximately 5.7%.

2. Which companies are prominent players in the Flexible Medical Packaging?

Key companies in the market include Amcor, Huhatamaki, Becton Dickinson&Company, Berry Plastics Group, Aptar Group, Datwyler Holdings, Westrock Company, Mondi Group, Winpak, Glenroy.

3. What are the main segments of the Flexible Medical Packaging?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 52.85 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Flexible Medical Packaging," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Flexible Medical Packaging report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Flexible Medical Packaging?

To stay informed about further developments, trends, and reports in the Flexible Medical Packaging, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence