Key Insights

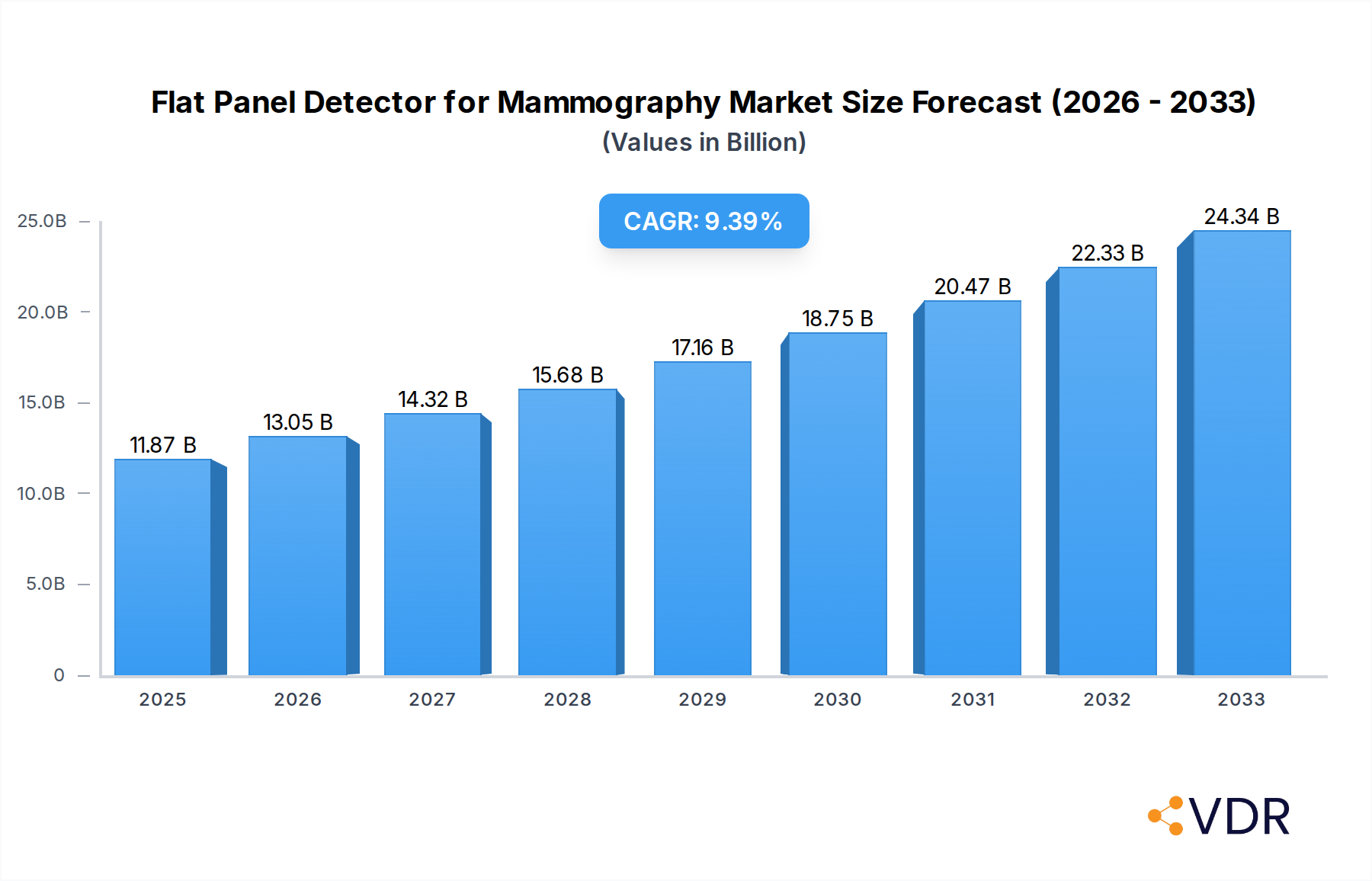

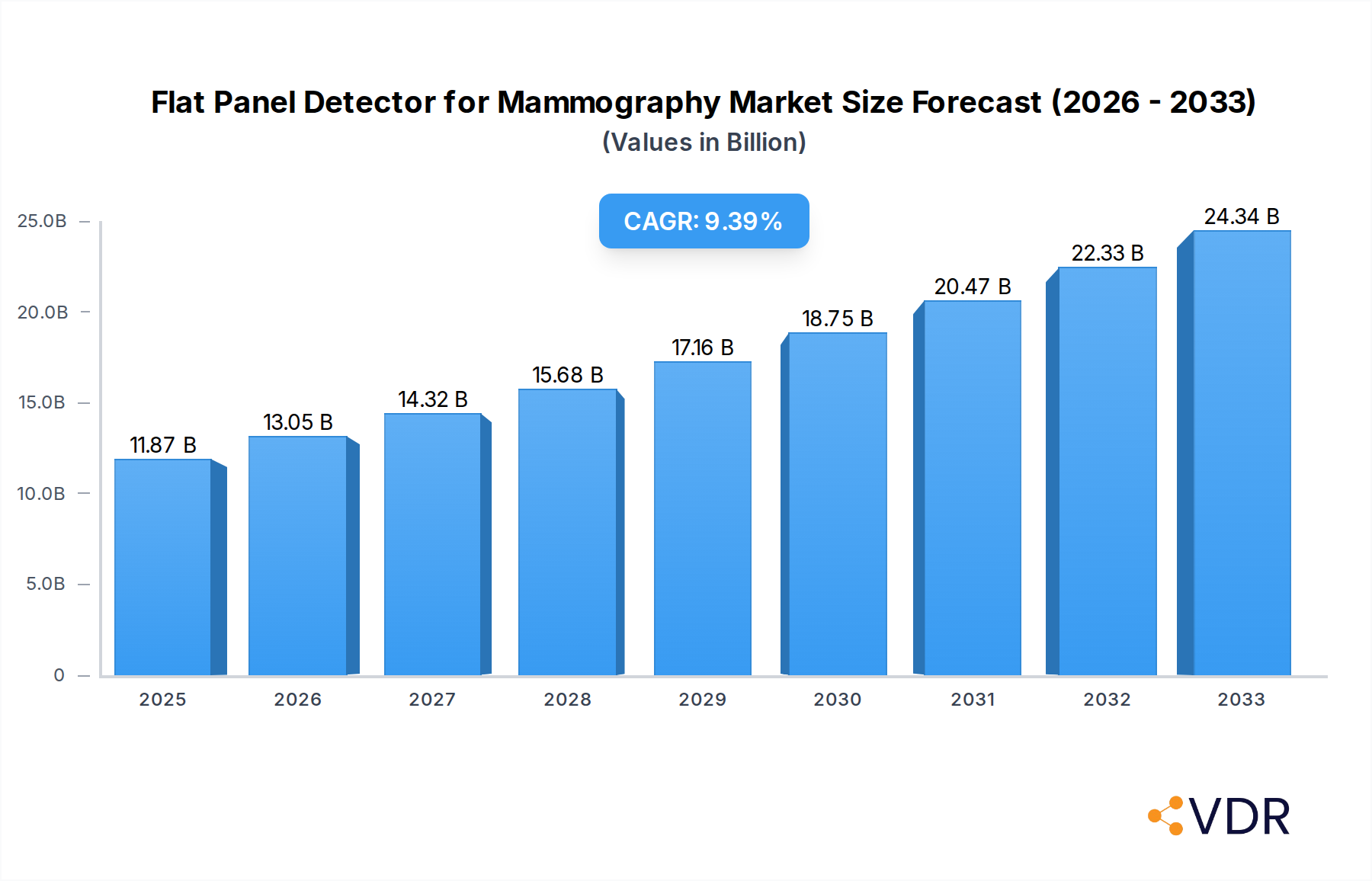

The global Flat Panel Detector (FPD) for Mammography market is poised for robust expansion, with an estimated market size of USD 11.87 billion in 2025. This significant growth is fueled by a compelling compound annual growth rate (CAGR) of 9.93%, projecting a dynamic trajectory through 2033. The increasing adoption of digital mammography, driven by its superior image quality and reduced radiation exposure compared to traditional film-based systems, stands as a primary market driver. Furthermore, the escalating prevalence of breast cancer globally, coupled with proactive government initiatives aimed at early detection and screening programs, significantly bolsters demand for advanced mammography solutions, including FPDs. Advancements in FPD technology, such as enhanced resolution, faster imaging speeds, and improved dose efficiency, are critical in meeting the evolving needs of diagnostic imaging centers and hospitals, further propelling market growth.

Flat Panel Detector for Mammography Market Size (In Billion)

The market is segmented into key applications, notably Full-Field Digital Mammography (FFDM) and Digital Breast Tomosynthesis (DBT). DBT, in particular, is gaining substantial traction due to its ability to provide three-dimensional images, significantly improving the detection of subtle abnormalities and reducing recall rates. Within detector types, both Direct Conversion and Indirect Conversion technologies are witnessing advancements, each offering distinct advantages in terms of image quality and cost-effectiveness. Key industry players like Teledyne DALSA, Varex Imaging, Analogic, and GE Healthcare are at the forefront of innovation, investing heavily in research and development to introduce next-generation FPDs. Restraints such as the high initial cost of advanced FPD systems and the need for specialized training for radiographers are being addressed through technological refinements and increasing market maturity, ensuring continued positive market momentum.

Flat Panel Detector for Mammography Company Market Share

This comprehensive report offers an in-depth analysis of the global Flat Panel Detector for Mammography market, a critical component in advanced breast cancer screening and diagnosis. With an estimated market size reaching $5.2 billion in 2025 and projected to grow at a robust CAGR of 12.5% during the 2025-2033 forecast period, this market is poised for significant expansion. The study encompasses the historical period of 2019-2024 and a detailed forecast period of 2025-2033, with 2025 serving as the base and estimated year. We delve into the nuances of Full-Field Digital Mammography (FFDM) and Digital Breast Tomosynthesis (DBT) applications, analyzing both Direct Conversion and Indirect Conversion detector types. This report is essential for understanding the evolving landscape, technological advancements, and strategic opportunities within this vital segment of the medical imaging industry.

Flat Panel Detector for Mammography Market Dynamics & Structure

The flat panel detector for mammography market is characterized by a moderately concentrated structure, with key players like Teledyne DALSA, Varex Imaging, Analogic, and GE Healthcare holding significant market shares. Technological innovation is the primary driver, fueled by the relentless pursuit of higher resolution, reduced radiation dose, and improved image quality. Regulatory frameworks, particularly those emphasizing patient safety and diagnostic accuracy, play a crucial role in shaping product development and market access. Competitive product substitutes, though limited in direct mammography applications, include advancements in ultrasound and MRI technologies that complement or, in specific scenarios, offer alternative diagnostic pathways. End-user demographics, including an aging global population and increased awareness campaigns, are steadily driving demand for advanced mammography solutions. Mergers and acquisitions (M&A) activity, though not at an extremely high volume, has been strategic, aimed at consolidating expertise, expanding product portfolios, and gaining market access. For instance, the 2022 acquisition of a smaller detector technology firm by a major player aimed to bolster their R&D capabilities in next-generation amorphous selenium detectors. Innovation barriers include the high cost of R&D, stringent regulatory approval processes, and the need for extensive clinical validation.

Flat Panel Detector for Mammography Growth Trends & Insights

The flat panel detector for mammography market is experiencing a transformative growth trajectory, driven by increasing global incidence of breast cancer and a growing emphasis on early detection. The market size, estimated at $5.2 billion in 2025, is projected to reach $13.8 billion by 2033, exhibiting a compound annual growth rate (CAGR) of 12.5% throughout the 2025-2033 forecast period. This robust growth is underpinned by several key trends. Firstly, the adoption rate of digital mammography systems, particularly those incorporating Digital Breast Tomosynthesis (DBT), is accelerating. DBT, offering a 3D view of breast tissue, significantly enhances diagnostic accuracy by reducing overlapping structures, leading to fewer false positives and improved cancer detection rates. Market penetration for DBT systems, which stood at approximately 45% in 2025, is anticipated to surpass 70% by 2033.

Technological disruptions are primarily focused on enhancing detector performance. Direct conversion detectors, utilizing materials like amorphous selenium, are gaining traction due to their superior spatial resolution and lower noise characteristics, leading to reduced radiation dose for patients. Their market share is expected to grow from 30% in 2025 to 55% by 2033. Conversely, indirect conversion detectors, employing scintillators like cesium iodide, continue to evolve with improved quantum efficiency and faster readout speeds. Consumer behavior shifts are also influencing market dynamics. Patients are increasingly aware of the benefits of advanced imaging technologies and actively seek out healthcare facilities equipped with the latest mammography equipment. This growing demand for higher quality imaging and improved patient experience is compelling healthcare providers to invest in cutting-edge flat panel detectors. Furthermore, government initiatives and reimbursement policies supporting breast cancer screening programs are acting as significant catalysts for market expansion. The increasing integration of artificial intelligence (AI) in mammography analysis, which relies on high-quality imaging data from flat panel detectors, further amplifies the demand for advanced detector technologies.

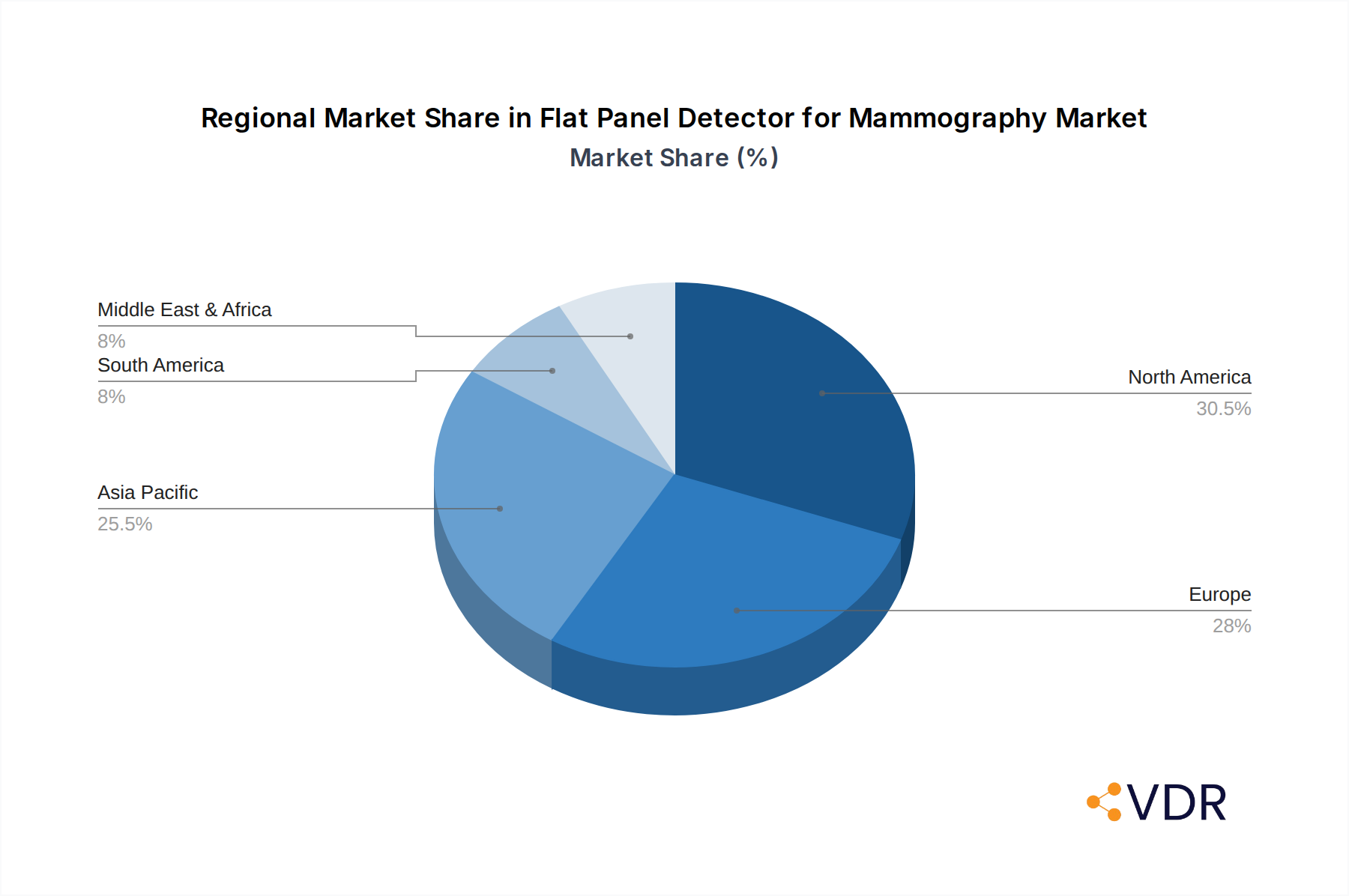

Dominant Regions, Countries, or Segments in Flat Panel Detector for Mammography

The North America region stands as the dominant force in the flat panel detector for mammography market, driven by a confluence of factors including high healthcare spending, advanced technological infrastructure, and a proactive approach to cancer screening. The United States, in particular, represents a significant portion of the regional market share, estimated at 60% of the global market in 2025. This dominance is further amplified by stringent regulatory standards and reimbursement policies that favor the adoption of advanced medical imaging technologies. The prevalence of Digital Breast Tomosynthesis (DBT) applications within North America is a key growth driver. With an estimated 65% of mammography procedures in the US utilizing DBT in 2025, this segment is projected to expand its market share to 80% by 2033. The increasing incidence of breast cancer in this demographic, coupled with a proactive screening culture, fuels the demand for high-resolution and advanced imaging capabilities.

In terms of detector types, Direct Conversion technology is progressively gaining prominence in North America due to its inherent advantages in spatial resolution and dose reduction. Its market share is projected to grow from 40% in 2025 to 65% by 2033 in this region. Key drivers contributing to North America's leadership include:

- High Healthcare Expenditure: Significant investment in healthcare infrastructure and advanced medical devices.

- Early Adoption of Technology: A willingness to embrace and integrate new diagnostic technologies for improved patient outcomes.

- Robust Screening Programs: Comprehensive national and state-level breast cancer screening initiatives.

- Favorable Regulatory Environment: Clear pathways for new technology approval and adoption.

- Presence of Key Market Players: Home to major manufacturers and research institutions driving innovation.

While North America leads, the Asia-Pacific region is emerging as a significant growth area, driven by increasing healthcare investments, a growing middle class, and rising awareness of breast cancer. Countries like China and India are witnessing rapid expansion in their healthcare sectors, leading to a surge in demand for digital mammography systems. The Full-Field Digital Mammography (FFDM) segment, while maturing in developed regions, still holds substantial market share in emerging economies due to its cost-effectiveness and established infrastructure.

Flat Panel Detector for Mammography Product Landscape

The product landscape for flat panel detectors for mammography is characterized by continuous innovation focused on enhancing image quality, reducing patient radiation dose, and improving diagnostic accuracy. Leading manufacturers are developing detectors with higher spatial resolution, improved detective quantum efficiency (DQE), and faster acquisition speeds. Innovations in amorphous selenium (a-Se) and advanced scintillator materials for indirect conversion are leading to superior contrast and detail visualization. Unique selling propositions often revolve around ultra-low dose imaging capabilities, facilitating more frequent screening without compromising image fidelity. Emerging technologies include detectors with integrated AI processing capabilities, enabling real-time image analysis and workflow optimization. The performance metrics of these detectors, such as pixel pitch, DQE at relevant spatial frequencies, and modulation transfer function (MTF), are critical differentiators in this competitive market.

Key Drivers, Barriers & Challenges in Flat Panel Detector for Mammography

Key Drivers: The flat panel detector for mammography market is propelled by the escalating global burden of breast cancer, demanding more accurate and efficient early detection methods. Technological advancements, particularly the superior image quality and dose reduction offered by Direct Conversion detectors and the diagnostic benefits of Digital Breast Tomosynthesis (DBT), are significant growth catalysts. Growing government initiatives and healthcare policies supporting cancer screening programs worldwide further bolster market expansion.

Key Barriers & Challenges: The high capital investment required for upgrading to digital mammography systems, especially for smaller clinics and in developing economies, presents a substantial barrier. Stringent regulatory approval processes, while ensuring safety, can also extend time-to-market for new technologies. Supply chain disruptions, as experienced in recent years, can impact the availability and cost of critical components. Intense competition among established players and the emergence of new entrants also exert pressure on pricing and profit margins. The $2.1 billion estimated cost of comprehensive mammography unit replacements globally in 2025 underscores this challenge.

Emerging Opportunities in Flat Panel Detector for Mammography

Emerging opportunities in the flat panel detector for mammography market lie in the untapped potential of developing nations where digital mammography penetration is still low. The integration of artificial intelligence (AI) with advanced detector technologies presents a significant avenue for growth, enabling enhanced image analysis, automated lesion detection, and risk stratification. The development of more portable and cost-effective mammography solutions could also open new markets, particularly in remote or underserved areas. Furthermore, the growing demand for personalized medicine and tailored screening protocols will drive the need for detectors capable of providing highly detailed and quantitative imaging data. The $0.8 billion projected market for AI-enabled mammography solutions by 2028 highlights this burgeoning opportunity.

Growth Accelerators in the Flat Panel Detector for Mammography Industry

Long-term growth in the flat panel detector for mammography industry is being accelerated by continuous technological breakthroughs in detector materials and design, leading to enhanced image resolution and reduced radiation exposure. Strategic partnerships between detector manufacturers, original equipment manufacturers (OEMs), and AI developers are fostering the creation of integrated imaging solutions. Market expansion strategies, focusing on emerging economies with growing healthcare expenditures and increasing breast cancer awareness, are also critical growth accelerators. The increasing adoption of Digital Breast Tomosynthesis (DBT) as a standard of care globally, driven by its proven diagnostic efficacy, is a major catalyst for the demand of advanced flat panel detectors.

Key Players Shaping the Flat Panel Detector for Mammography Market

- Teledyne DALSA

- Varex Imaging

- Analogic

- GE Healthcare

- Detection Technology

- Iray Technology

- Vieworks

- CareRay

Notable Milestones in Flat Panel Detector for Mammography Sector

- 2019: Introduction of next-generation amorphous selenium detectors offering improved DQE and lower noise.

- 2020: Increased adoption of DBT systems globally, driving demand for compatible FPDs.

- 2021: Advancements in indirect conversion scintillators leading to faster readout times and higher throughput.

- 2022: Strategic partnerships formed between FPD manufacturers and AI companies to integrate advanced image analysis capabilities.

- 2023: Regulatory approvals for new ultra-low dose mammography systems utilizing cutting-edge FPD technology.

- 2024: Enhanced manufacturing capabilities and supply chain resilience to meet growing global demand.

In-Depth Flat Panel Detector for Mammography Market Outlook

The future outlook for the flat panel detector for mammography market is exceptionally bright, underpinned by sustained growth accelerators. The ongoing evolution of detector technologies, promising unprecedented image clarity and dose optimization, will continue to drive upgrades and new installations. The synergistic integration of AI with these advanced detectors is poised to revolutionize breast cancer screening, offering greater accuracy and efficiency. Strategic market expansion into regions with developing healthcare infrastructures presents a significant opportunity for market players. The anticipated market value is expected to reach $13.8 billion by 2033, indicating robust long-term potential and a sustained demand for innovative flat panel detector solutions in safeguarding global breast health.

Flat Panel Detector for Mammography Segmentation

-

1. Application

- 1.1. Full-Field Digital Mammography

- 1.2. Digital Breast Tomosynthesis

-

2. Types

- 2.1. Direct Conversion

- 2.2. Indirect Conversion

Flat Panel Detector for Mammography Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Flat Panel Detector for Mammography Regional Market Share

Geographic Coverage of Flat Panel Detector for Mammography

Flat Panel Detector for Mammography REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.93% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Flat Panel Detector for Mammography Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Full-Field Digital Mammography

- 5.1.2. Digital Breast Tomosynthesis

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Direct Conversion

- 5.2.2. Indirect Conversion

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Flat Panel Detector for Mammography Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Full-Field Digital Mammography

- 6.1.2. Digital Breast Tomosynthesis

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Direct Conversion

- 6.2.2. Indirect Conversion

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Flat Panel Detector for Mammography Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Full-Field Digital Mammography

- 7.1.2. Digital Breast Tomosynthesis

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Direct Conversion

- 7.2.2. Indirect Conversion

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Flat Panel Detector for Mammography Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Full-Field Digital Mammography

- 8.1.2. Digital Breast Tomosynthesis

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Direct Conversion

- 8.2.2. Indirect Conversion

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Flat Panel Detector for Mammography Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Full-Field Digital Mammography

- 9.1.2. Digital Breast Tomosynthesis

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Direct Conversion

- 9.2.2. Indirect Conversion

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Flat Panel Detector for Mammography Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Full-Field Digital Mammography

- 10.1.2. Digital Breast Tomosynthesis

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Direct Conversion

- 10.2.2. Indirect Conversion

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Teledyne DALSA

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Varex Imaging

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Analogic

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 GE Healthcare

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Detection Technology

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Iray Technology

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Vieworks

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 CareRay

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.1 Teledyne DALSA

List of Figures

- Figure 1: Global Flat Panel Detector for Mammography Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Flat Panel Detector for Mammography Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Flat Panel Detector for Mammography Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Flat Panel Detector for Mammography Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Flat Panel Detector for Mammography Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Flat Panel Detector for Mammography Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Flat Panel Detector for Mammography Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Flat Panel Detector for Mammography Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Flat Panel Detector for Mammography Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Flat Panel Detector for Mammography Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Flat Panel Detector for Mammography Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Flat Panel Detector for Mammography Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Flat Panel Detector for Mammography Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Flat Panel Detector for Mammography Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Flat Panel Detector for Mammography Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Flat Panel Detector for Mammography Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Flat Panel Detector for Mammography Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Flat Panel Detector for Mammography Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Flat Panel Detector for Mammography Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Flat Panel Detector for Mammography Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Flat Panel Detector for Mammography Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Flat Panel Detector for Mammography Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Flat Panel Detector for Mammography Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Flat Panel Detector for Mammography Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Flat Panel Detector for Mammography Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Flat Panel Detector for Mammography Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Flat Panel Detector for Mammography Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Flat Panel Detector for Mammography Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Flat Panel Detector for Mammography Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Flat Panel Detector for Mammography Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Flat Panel Detector for Mammography Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Flat Panel Detector for Mammography Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Flat Panel Detector for Mammography Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Flat Panel Detector for Mammography Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Flat Panel Detector for Mammography Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Flat Panel Detector for Mammography Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Flat Panel Detector for Mammography Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Flat Panel Detector for Mammography Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Flat Panel Detector for Mammography Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Flat Panel Detector for Mammography Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Flat Panel Detector for Mammography Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Flat Panel Detector for Mammography Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Flat Panel Detector for Mammography Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Flat Panel Detector for Mammography Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Flat Panel Detector for Mammography Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Flat Panel Detector for Mammography Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Flat Panel Detector for Mammography Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Flat Panel Detector for Mammography Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Flat Panel Detector for Mammography Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Flat Panel Detector for Mammography Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Flat Panel Detector for Mammography Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Flat Panel Detector for Mammography Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Flat Panel Detector for Mammography Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Flat Panel Detector for Mammography Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Flat Panel Detector for Mammography Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Flat Panel Detector for Mammography Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Flat Panel Detector for Mammography Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Flat Panel Detector for Mammography Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Flat Panel Detector for Mammography Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Flat Panel Detector for Mammography Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Flat Panel Detector for Mammography Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Flat Panel Detector for Mammography Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Flat Panel Detector for Mammography Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Flat Panel Detector for Mammography Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Flat Panel Detector for Mammography Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Flat Panel Detector for Mammography Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Flat Panel Detector for Mammography Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Flat Panel Detector for Mammography Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Flat Panel Detector for Mammography Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Flat Panel Detector for Mammography Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Flat Panel Detector for Mammography Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Flat Panel Detector for Mammography Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Flat Panel Detector for Mammography Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Flat Panel Detector for Mammography Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Flat Panel Detector for Mammography Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Flat Panel Detector for Mammography Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Flat Panel Detector for Mammography Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Flat Panel Detector for Mammography?

The projected CAGR is approximately 9.93%.

2. Which companies are prominent players in the Flat Panel Detector for Mammography?

Key companies in the market include Teledyne DALSA, Varex Imaging, Analogic, GE Healthcare, Detection Technology, Iray Technology, Vieworks, CareRay.

3. What are the main segments of the Flat Panel Detector for Mammography?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 11.87 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Flat Panel Detector for Mammography," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Flat Panel Detector for Mammography report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Flat Panel Detector for Mammography?

To stay informed about further developments, trends, and reports in the Flat Panel Detector for Mammography, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence