Key Insights

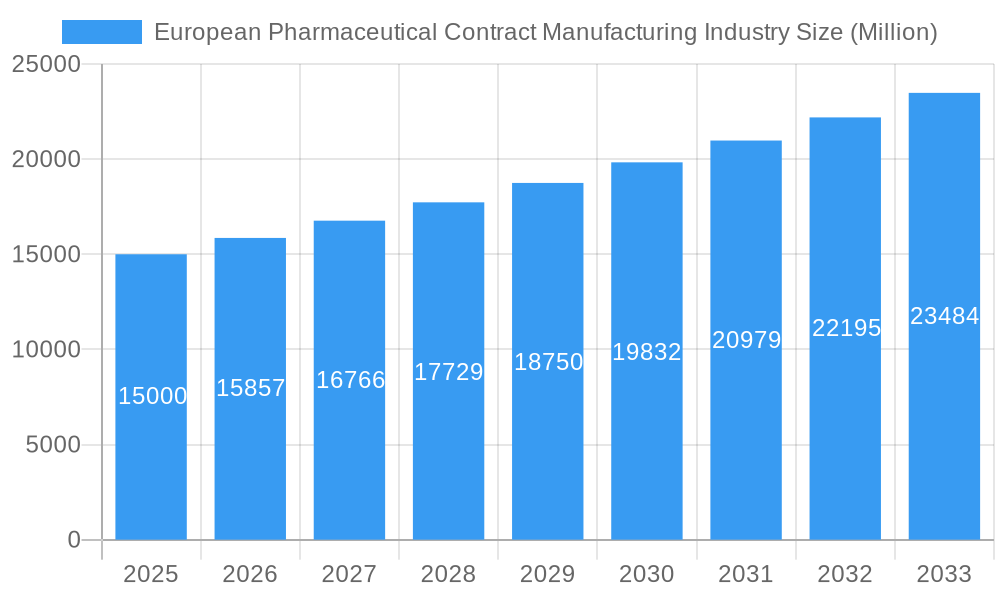

The European pharmaceutical contract manufacturing (PCM) market, valued at approximately €15 billion in 2025, is experiencing robust growth, projected to reach €25 billion by 2033, driven by a 5.71% compound annual growth rate (CAGR). This expansion is fueled by several key factors. Firstly, increasing R&D expenditure by pharmaceutical companies necessitates outsourcing non-core activities like manufacturing to specialized contract manufacturers, allowing them to focus on innovation and core competencies. Secondly, the growing demand for complex drug formulations, particularly injectables and specialized dosage forms, is driving the need for experienced and technologically advanced contract manufacturers. This is further amplified by the rising prevalence of chronic diseases across Europe, leading to a higher demand for medications. Finally, stringent regulatory requirements and the need for high-quality manufacturing standards are prompting pharmaceutical companies to partner with established PCM providers who can ensure compliance and efficiency.

European Pharmaceutical Contract Manufacturing Industry Market Size (In Billion)

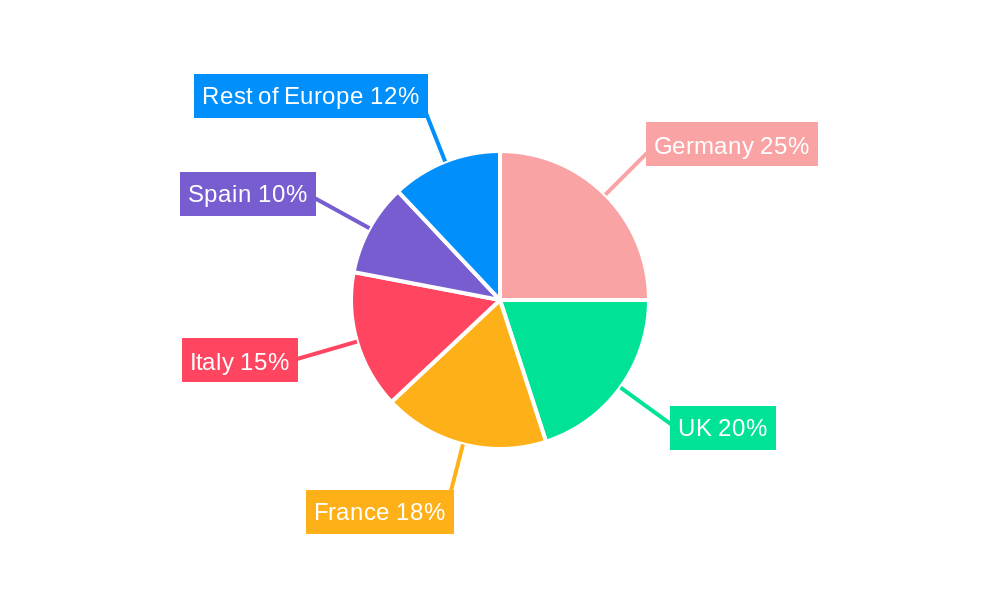

Geographical distribution of the market showcases Germany, the UK, France, and Italy as major contributors, reflecting established pharmaceutical hubs. However, growth opportunities exist in other European nations like Spain and the Netherlands as their pharmaceutical sectors mature and embrace outsourcing. The market is segmented by service type, with active pharmaceutical ingredient (API) manufacturing, finished dosage formulation (FDF) development and manufacturing, and injectable dose formulation secondary packaging representing key service offerings. Competition is fierce, with established players like Lonza Group, Recipharm AB, and Boehringer Ingelheim Group vying for market share alongside smaller, specialized contract manufacturers. While potential restraints include fluctuating raw material prices and potential supply chain disruptions, the overall market outlook remains positive, driven by the enduring need for efficient and high-quality pharmaceutical manufacturing across Europe.

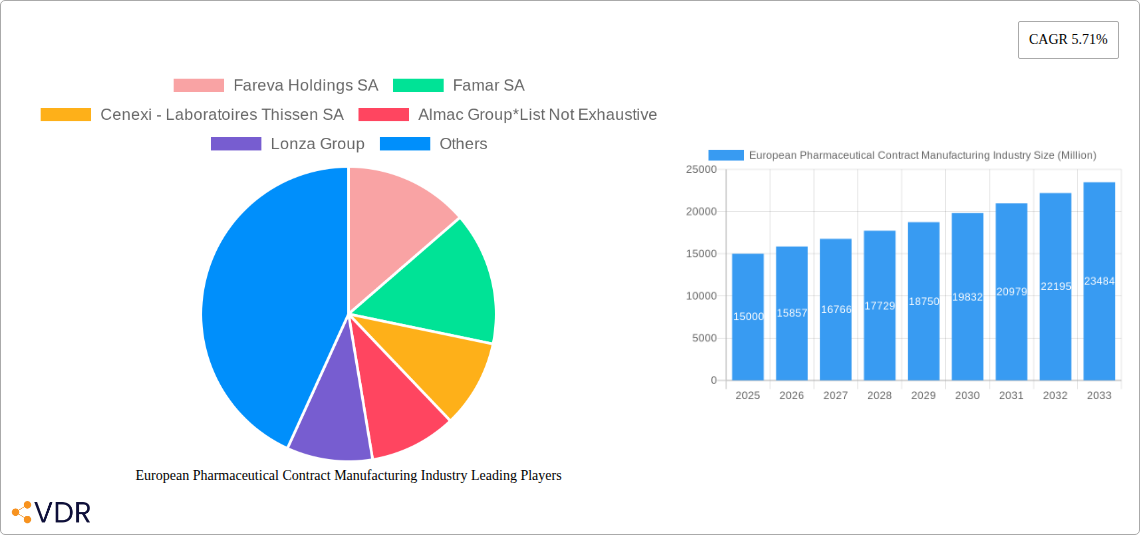

European Pharmaceutical Contract Manufacturing Industry Company Market Share

European Pharmaceutical Contract Manufacturing Industry Market Report: 2019-2033

This comprehensive report provides a detailed analysis of the European pharmaceutical contract manufacturing industry, covering market dynamics, growth trends, key players, and future outlook. With a study period spanning 2019-2033 (base year 2025, forecast period 2025-2033), this report is an invaluable resource for industry professionals, investors, and strategic decision-makers. The report analyzes the parent market of pharmaceutical manufacturing and its child market, contract manufacturing services, delivering granular insights across various segments.

European Pharmaceutical Contract Manufacturing Industry Market Dynamics & Structure

The European pharmaceutical contract manufacturing market is characterized by a moderately concentrated structure, featuring a blend of large, established players and a dynamic ecosystem of smaller, specialized firms. This dynamic landscape is propelled by continuous technological innovation, particularly in cutting-edge areas such as advanced drug delivery systems, complex biologics manufacturing, and sophisticated analytical services. Adherence to stringent regulatory frameworks, exemplified by the rigorous standards set by the European Medicines Agency (EMA), profoundly shapes manufacturing processes, quality control protocols, and overall product development strategies. The market also navigates evolving competitive pressures from contract manufacturers operating outside of Europe, alongside the emergence of specialized alternative service providers. Strategic consolidation through mergers and acquisitions (M&A) remains a significant and ongoing trend, contributing to market evolution and capability enhancement.

- Market Concentration: Currently moderately concentrated, with the top 5 players projected to hold approximately 40-45% of the market share in 2024.

- Technological Drivers: Key advancements in high-potency API synthesis, novel formulation technologies for complex molecules, digitalization of manufacturing processes, and the implementation of automation and AI are significant growth enablers.

- Regulatory Landscape: The stringent and evolving EMA guidelines are pivotal in defining manufacturing practices, ensuring unwavering quality control, and facilitating the approval of innovative therapies.

- Competitive Substitutes: Increased competition is observed from contract manufacturers in emerging markets offering cost-effective solutions, alongside the growing in-house manufacturing capabilities of some pharmaceutical giants and the rise of specialized niche service providers.

- M&A Activity: A notable trend of consolidation has been observed in recent years, with an estimated 15-20 major strategic deals finalized between 2019 and 2024. Deal volume is anticipated to remain steady, with approximately 5-7 significant M&A transactions expected annually between 2025 and 2033, driven by the pursuit of expanded capabilities and market reach.

- End-User Demographics: The primary demand is driven by large, established pharmaceutical companies, innovative biotechnology firms, and manufacturers of generic and biosimilar drugs seeking specialized expertise and flexible manufacturing solutions.

European Pharmaceutical Contract Manufacturing Industry Growth Trends & Insights

The European pharmaceutical contract manufacturing market exhibited strong growth between 2019 and 2024, driven by increasing R&D expenditure in the pharmaceutical sector, outsourcing trends, and the growing demand for specialized manufacturing services. The market size reached xx million units in 2024 and is projected to expand at a CAGR of xx% from 2025 to 2033, reaching xx million units by 2033. This growth is fuelled by technological advancements such as continuous manufacturing and personalized medicine, increasing adoption of CDMO services, and shifts in consumer behavior toward more specialized and targeted therapies. The market penetration of advanced technologies like continuous manufacturing is expected to increase from xx% in 2024 to xx% by 2033.

Dominant Regions, Countries, or Segments in European Pharmaceutical Contract Manufacturing Industry

Germany, the United Kingdom, and France stand as the preeminent markets within Europe for pharmaceutical contract manufacturing. This leadership is underpinned by their robust domestic pharmaceutical industries, highly developed industrial infrastructure, and a highly skilled and specialized workforce. Within the service type segments, Finished Dosage Formulation (FDF) Development and Manufacturing commands the largest market share, reflecting the escalating demand for increasingly complex and patient-centric drug formulations, including advanced oral solids, sterile injectables, and topical preparations.

- By Country:

- Germany: Benefits from a strong domestic pharmaceutical industry, proactive government support for R&D and manufacturing, and a robust network of specialized CDMOs. Projected market share of approximately 25-30% in 2024.

- United Kingdom: Boasts an established R&D infrastructure, a significant presence of major global pharmaceutical companies, and a supportive regulatory environment for innovation. Projected market share of approximately 20-25% in 2024.

- France: Features a substantial ecosystem of both large-scale contract manufacturers and agile small and medium-sized enterprises (SMEs) catering to diverse needs. Projected market share of approximately 15-20% in 2024.

- By Service Type:

- Finished Dosage Formulation (FDF) Development and Manufacturing: Represents the largest segment due to the increasing complexity of drug delivery systems, including modified-release formulations, combination products, and novel dosage forms.

- Active Pharmaceutical Ingredient (API) Manufacturing: Shows significant growth potential, driven by the global demand for cost-effective generics, the rise of biosimilars, and the increasing outsourcing of complex small molecule and peptide API production.

- Injectable Dose Formulation & Secondary Packaging: Experiences steady growth, propelled by the sustained demand for sterile injectables, pre-filled syringes, and vials, alongside the increasing requirement for specialized and compliant secondary packaging solutions.

European Pharmaceutical Contract Manufacturing Industry Product Landscape

Product innovations focus on improving efficiency, reducing costs, and enhancing product quality. This includes advanced analytical techniques for quality control, automation of manufacturing processes, and the development of innovative drug delivery systems. Key selling propositions emphasize speed, flexibility, and adherence to stringent regulatory standards. Technological advancements include the integration of AI and machine learning for process optimization.

Key Drivers, Barriers & Challenges in European Pharmaceutical Contract Manufacturing Industry

Key Drivers:

- Increased outsourcing by pharmaceutical companies.

- Growing demand for specialized manufacturing services.

- Technological advancements in drug delivery and manufacturing processes.

- Stringent regulatory requirements pushing for higher quality and safety standards.

Key Challenges:

- Intense competition, particularly from low-cost manufacturers in emerging markets. This leads to price pressure, impacting profit margins by an estimated xx% in 2024.

- Regulatory hurdles and compliance costs. The average cost of regulatory compliance per manufacturing facility increased by xx% in 2022.

- Supply chain disruptions, particularly concerning raw materials and specialized components. Supply chain disruptions cost the industry an estimated xx million units in lost revenue in 2022.

Emerging Opportunities in European Pharmaceutical Contract Manufacturing Industry

The horizon for pharmaceutical contract manufacturing in Europe is illuminated by significant emerging opportunities. The burgeoning field of personalized medicine, with its demand for highly customized and often low-volume production, presents a substantial growth avenue. Similarly, the rapid advancement and increasing clinical application of cell and gene therapies necessitate specialized manufacturing expertise and infrastructure that many CDMOs are actively developing. Furthermore, there is a growing demand for advanced drug delivery systems that enhance therapeutic efficacy and patient compliance. Untapped markets include expanding service offerings within emerging economies across Europe and a heightened demand for specialized contract manufacturing services in niche areas such as high-potency biologics, viral vector production, and complex therapeutic modalities.

Growth Accelerators in the European Pharmaceutical Contract Manufacturing Industry Industry

Key growth accelerators are revolutionizing the European pharmaceutical contract manufacturing industry. Technological breakthroughs in continuous manufacturing and sophisticated process automation are driving substantial efficiency gains, leading to significant cost reductions and improved product consistency. Strategic partnerships and collaborations forged between contract manufacturers and pharmaceutical companies are proving instrumental in accelerating innovation, fostering the development of novel therapies, and enhancing supply chain resilience and agility. The proactive expansion into new and complex therapeutic areas, particularly cell and gene therapy, alongside the development of specialized capabilities for biologics and highly potent compounds, are creating significant new market opportunities and driving industry growth.

Key Players Shaping the European Pharmaceutical Contract Manufacturing Industry Market

- Fareva Holdings SA

- Famar SA

- Cenexi - Laboratoires Thissen SA

- Almac Group

- Lonza Group

- Aenova Group

- Boehringer Ingelheim Group

- Recipharm AB

Notable Milestones in European Pharmaceutical Contract Manufacturing Industry Sector

- Feb 2022: Merck, Germany, strategically restructured its business units to bolster its Contract Development and Manufacturing Organization (CDMO) capabilities, establishing the dedicated Life Science Services (LSS) division to cater to a broader range of client needs.

- March 2022: MorphoSys incurred significant charges amounting to USD 254 million following a strategic consolidation of its research and development operations within Germany, leading to the discontinuation of its U.S. R&D efforts and early-stage pipeline projects.

- Q4 2023: Lonza announced a significant expansion of its biologics manufacturing capacity in Switzerland, investing in state-of-the-art facilities to meet the escalating demand for monoclonal antibodies and other complex biopharmaceuticals.

- Early 2024: Catalent completed the acquisition of a specialized fill-finish facility in Italy, enhancing its capabilities in sterile injectables and pre-filled syringe manufacturing, addressing a critical market need.

In-Depth European Pharmaceutical Contract Manufacturing Industry Market Outlook

The European pharmaceutical contract manufacturing market is poised for sustained growth over the next decade. The increasing complexity of drug development, the growing adoption of outsourcing strategies, and continuous technological innovations will drive market expansion. Strategic partnerships and investment in advanced manufacturing technologies will further enhance the competitiveness of European contract manufacturers, solidifying their position in the global market.

European Pharmaceutical Contract Manufacturing Industry Segmentation

-

1. Service Type

- 1.1. Active P

-

1.2. Finished

- 1.2.1. Solid Dose Formulation

- 1.2.2. Liquid Dose Formulation

- 1.2.3. Injectable Dose Formulation

- 1.3. Secondary Packaging

European Pharmaceutical Contract Manufacturing Industry Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

European Pharmaceutical Contract Manufacturing Industry Regional Market Share

Geographic Coverage of European Pharmaceutical Contract Manufacturing Industry

European Pharmaceutical Contract Manufacturing Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Service Type

- 5.1.1. Active P

- 5.1.2. Finished

- 5.1.2.1. Solid Dose Formulation

- 5.1.2.2. Liquid Dose Formulation

- 5.1.2.3. Injectable Dose Formulation

- 5.1.3. Secondary Packaging

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Service Type

- 6. European Pharmaceutical Contract Manufacturing Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Service Type

- 6.1.1. Active P

- 6.1.2. Finished

- 6.1.2.1. Solid Dose Formulation

- 6.1.2.2. Liquid Dose Formulation

- 6.1.2.3. Injectable Dose Formulation

- 6.1.3. Secondary Packaging

- 6.1. Market Analysis, Insights and Forecast - by Service Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Fareva Holdings SA

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Famar SA

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Cenexi - Laboratoires Thissen SA

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Almac Group*List Not Exhaustive

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Lonza Group

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Aenova Group

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Boehringer Ingelheim Group

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Recipharm AB

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.1 Fareva Holdings SA

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: European Pharmaceutical Contract Manufacturing Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: European Pharmaceutical Contract Manufacturing Industry Share (%) by Company 2025

List of Tables

- Table 1: European Pharmaceutical Contract Manufacturing Industry Revenue billion Forecast, by Service Type 2020 & 2033

- Table 2: European Pharmaceutical Contract Manufacturing Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 3: European Pharmaceutical Contract Manufacturing Industry Revenue billion Forecast, by Service Type 2020 & 2033

- Table 4: European Pharmaceutical Contract Manufacturing Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 5: United Kingdom European Pharmaceutical Contract Manufacturing Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 6: Germany European Pharmaceutical Contract Manufacturing Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 7: France European Pharmaceutical Contract Manufacturing Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Italy European Pharmaceutical Contract Manufacturing Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Spain European Pharmaceutical Contract Manufacturing Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Netherlands European Pharmaceutical Contract Manufacturing Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Belgium European Pharmaceutical Contract Manufacturing Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Sweden European Pharmaceutical Contract Manufacturing Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Norway European Pharmaceutical Contract Manufacturing Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Poland European Pharmaceutical Contract Manufacturing Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Denmark European Pharmaceutical Contract Manufacturing Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the European Pharmaceutical Contract Manufacturing Industry?

The projected CAGR is approximately 8.2%.

2. Which companies are prominent players in the European Pharmaceutical Contract Manufacturing Industry?

Key companies in the market include Fareva Holdings SA, Famar SA, Cenexi - Laboratoires Thissen SA, Almac Group*List Not Exhaustive, Lonza Group, Aenova Group, Boehringer Ingelheim Group, Recipharm AB.

3. What are the main segments of the European Pharmaceutical Contract Manufacturing Industry?

The market segments include Service Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 209.9 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Outsourcing Volume by Pharmaceutical Companies; Increasing Investment in R&D.

6. What are the notable trends driving market growth?

Rising Investment in R&D will Drive The Market Growth.

7. Are there any restraints impacting market growth?

Increasing Lead Time and Logistics Costs; Stringent Regulatory Requirements; Capacity Utilization Issues Affecting the Profitability of CMOs.

8. Can you provide examples of recent developments in the market?

March 2022: MorphoSys sacked US R&D to consolidate work in Germany, taking USD 254 million in charges. MorphoSys axed its early pipeline and U.S. R&D work that came with the USD 1.7 billion purchase of Constellation Pharmaceuticals, meaning a more than USD 250 million impairment charge as the German pharma shifted the focus home.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "European Pharmaceutical Contract Manufacturing Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the European Pharmaceutical Contract Manufacturing Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the European Pharmaceutical Contract Manufacturing Industry?

To stay informed about further developments, trends, and reports in the European Pharmaceutical Contract Manufacturing Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence