Key Insights

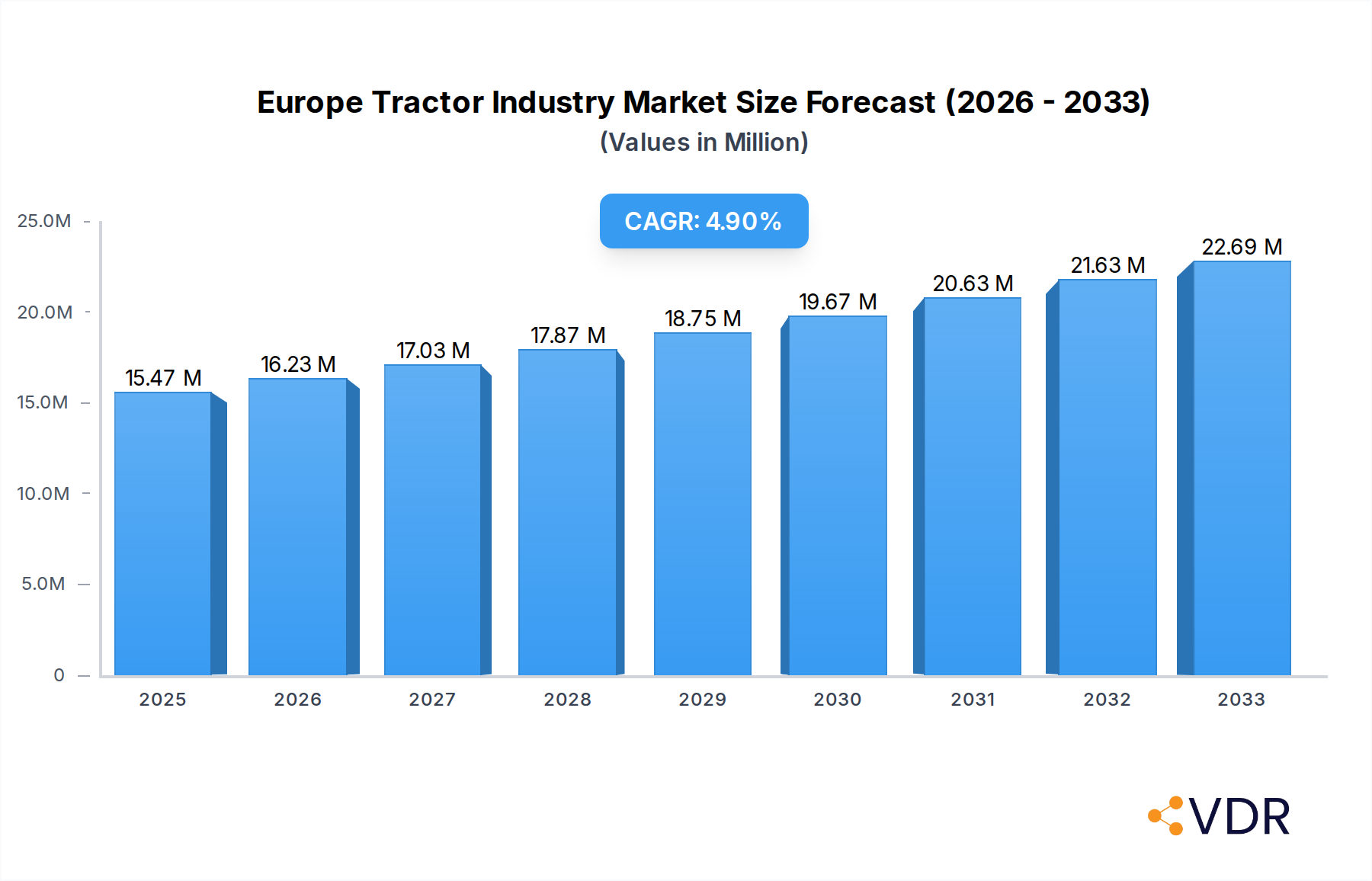

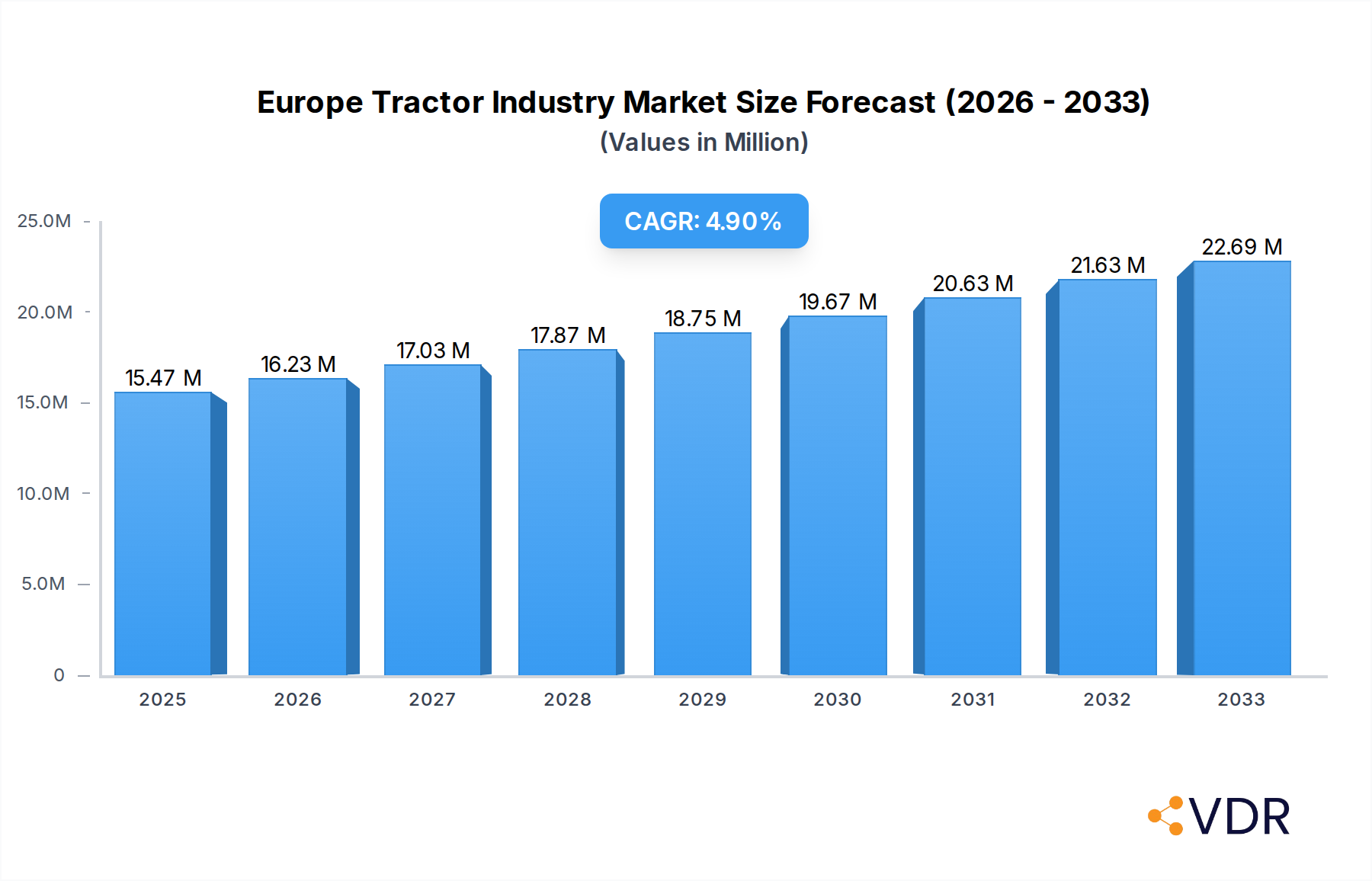

The European tractor market is poised for steady growth, exhibiting a projected Compound Annual Growth Rate (CAGR) of 4.90% from 2025 to 2033. The market size in 2025 is estimated at 15.47 Million units. This expansion is driven by several key factors. Firstly, the increasing adoption of advanced agricultural technologies, including precision farming, automation, and smart farming solutions, is significantly boosting demand for modern tractors equipped with these capabilities. Secondly, there's a growing emphasis on sustainable agriculture and reducing the environmental impact of farming practices, leading to a preference for fuel-efficient and emission-compliant tractor models. Furthermore, government initiatives and subsidies supporting agricultural modernization and mechanization across European nations are acting as strong catalysts for market growth. The need to improve operational efficiency, reduce labor costs, and enhance crop yields in the face of evolving agricultural landscapes is also contributing to the sustained demand for tractors.

Europe Tractor Industry Market Size (In Million)

Despite the positive outlook, certain challenges temper the market's trajectory. The high initial investment cost of advanced tractors can be a deterrent for smaller farms and emerging agricultural enterprises. Fluctuations in agricultural commodity prices can also impact farmers' purchasing power and their willingness to invest in new machinery. Additionally, stringent environmental regulations, while driving demand for greener technologies, also necessitate continuous innovation and investment from manufacturers, which can affect pricing. However, ongoing technological advancements, such as the development of electric and hybrid tractors, alongside the increasing availability of financing options and rental services, are expected to mitigate these restraints. The market is characterized by a dynamic competitive landscape, with key players actively investing in research and development to introduce innovative products and expand their market presence across diverse European agricultural regions.

Europe Tractor Industry Company Market Share

This in-depth report provides a definitive analysis of the Europe tractor industry, covering production, consumption, import/export dynamics, and price trends from 2019 to 2033, with a base and estimated year of 2025. Uncover critical insights into agricultural machinery market trends, farm equipment sales Europe, and the evolving landscape of off-highway vehicles and construction equipment. We delve into parent and child market segments, offering a granular view of opportunities within tractor manufacturing Europe, specialty tractors, and the burgeoning autonomous tractor technology.

This report is an indispensable resource for stakeholders seeking to understand and capitalize on the dynamic European agricultural equipment market. It offers strategic intelligence on tractor market share Europe, farm mechanization Europe, and the future of precision agriculture technology.

Europe Tractor Industry Market Dynamics & Structure

The Europe tractor industry is characterized by a moderate market concentration, with leading players like Deere & Company, CNH Industrial NV, and AGCO Corporation holding significant market share. Technological innovation remains a key driver, fueled by the increasing demand for precision farming solutions, electrified tractors, and autonomous farming equipment. Regulatory frameworks, particularly concerning emissions standards and agricultural subsidies, play a crucial role in shaping production and consumption patterns. Competitive product substitutes, such as advanced robotics and drones for certain farming tasks, are emerging but have not yet significantly impacted the core tractor market. End-user demographics are shifting, with a growing segment of younger, tech-savvy farmers adopting advanced machinery. Mergers and acquisitions (M&A) activity, while not at peak levels, is a consistent feature, aimed at expanding product portfolios and market reach.

- Market Concentration: Dominated by a few key global manufacturers, with a significant presence of European-based companies.

- Technological Innovation: Driven by automation, electrification, smart farming, and data analytics in agriculture.

- Regulatory Frameworks: EU regulations on emissions and environmental impact influence engine technology and tractor design.

- Competitive Substitutes: Growing interest in drones and robotic solutions for specific farm operations.

- End-User Demographics: Increasing adoption by younger farmers and a focus on ROI and efficiency.

- M&A Trends: Strategic partnerships and acquisitions to enhance technology offerings and market access.

Europe Tractor Industry Growth Trends & Insights

The Europe tractor industry is poised for steady growth, driven by an increasing focus on agricultural productivity and sustainability across the continent. Market size evolution is projected to show a consistent upward trajectory, propelled by the adoption of modern farming practices and the need to optimize land utilization. Adoption rates of advanced tractors, including those equipped with GPS guidance systems, telematics, and variable rate technology, are steadily increasing as farmers recognize their potential for improved efficiency and reduced resource wastage. Technological disruptions, such as the development of electric tractors and hydrogen-powered agricultural machinery, are beginning to influence the market, promising a greener future for farm mechanization. Consumer behavior shifts are evident, with a growing demand for tractors that offer enhanced operator comfort, reduced emissions, and integrated digital solutions for farm management. The CAGR for the forecast period is estimated to be around xx%, reflecting a healthy expansion driven by innovation and evolving agricultural needs.

- Market Size Evolution: Consistent growth driven by modernization of agricultural practices and demand for efficient machinery.

- Adoption Rates: Increasing uptake of tractors with advanced technologies like GPS, telematics, and automated features.

- Technological Disruptions: Emergence and growing interest in electrified, autonomous, and alternative fuel tractors.

- Consumer Behavior Shifts: Farmers prioritizing fuel efficiency, operator comfort, digital integration, and sustainability.

- Market Penetration: Deepening penetration of advanced tractor technologies in both large-scale and small-to-medium farms.

Dominant Regions, Countries, or Segments in Europe Tractor Industry

Within the Europe tractor industry, Western Europe, particularly Germany, France, and the UK, consistently emerges as a dominant force in both production analysis and consumption analysis. This dominance is attributed to their highly mechanized agricultural sectors, strong government support for farming, and the presence of advanced farming technologies. The production analysis is heavily influenced by established manufacturers with robust R&D capabilities, leading to a high volume of both standard and specialized tractors.

In terms of consumption analysis, these regions exhibit a strong demand for high-horsepower tractors, sophisticated implements, and machinery equipped with cutting-edge precision agriculture technology. The import market analysis (value & volume) for these dominant countries reflects a substantial inflow of specialized agricultural machinery, often complementing domestic production. Conversely, their export market analysis (value & volume) showcases their role as key suppliers of advanced tractors and related technologies to other European nations and global markets. The price trend analysis in these regions is often influenced by technological advancements, regulatory compliance costs, and competitive pressures.

- Dominant Regions: Western Europe (Germany, France, UK)

- Production Analysis: High volume, advanced technology, and specialized tractor manufacturing.

- Consumption Analysis: Strong demand for high-horsepower, technologically advanced, and efficient tractors.

- Import Market Analysis: Significant import of specialized farm equipment and components.

- Export Market Analysis: Leading exporters of tractors and agricultural machinery globally.

- Price Trend Analysis: Influenced by innovation, compliance, and market demand for premium features.

- Key Drivers of Dominance:

- Highly mechanized and efficient agricultural sectors.

- Strong government support and subsidies for modern farming.

- High adoption rate of advanced agricultural technologies.

- Presence of leading global tractor manufacturers and R&D centers.

- Robust infrastructure supporting agricultural operations.

Eastern European countries are also showing significant growth potential, driven by agricultural modernization efforts and increasing investment in farm mechanization, creating opportunities in the utility tractor market and compact tractor sales Europe.

Europe Tractor Industry Product Landscape

The Europe tractor industry's product landscape is characterized by continuous innovation focused on enhancing efficiency, sustainability, and operator experience. Leading manufacturers are introducing tractors with advanced engine technologies that meet stringent emission standards, alongside improved fuel efficiency. The integration of digital solutions, such as GPS navigation, telematics for real-time data monitoring, and precision application systems, is becoming standard. Furthermore, there is a growing emphasis on developing electric tractors and those powered by alternative fuels to meet environmental regulations and farmer demand for greener solutions. The product range spans from robust heavy-duty tractors for large-scale farming to versatile compact tractors for smaller operations and specialized agricultural tasks.

Key Drivers, Barriers & Challenges in Europe Tractor Industry

Key Drivers:

- Technological Advancements: The relentless pursuit of innovation in precision farming, automation, and electrified tractors drives market demand.

- Increasing Demand for Food Security: Growing global population necessitates enhanced agricultural output, requiring efficient mechanization.

- Government Support and Subsidies: Agricultural policies and financial incentives encourage the adoption of modern farm equipment.

- Mechanization of Agriculture: Ongoing efforts to mechanize farming practices, especially in emerging markets within Europe.

Barriers & Challenges:

- High Initial Investment: The cost of advanced tractors and associated technologies can be a significant barrier for some farmers.

- Skilled Labor Shortage: The lack of trained operators and maintenance personnel for complex machinery poses a challenge.

- Regulatory Hurdles: Evolving emission standards and other environmental regulations require continuous investment in R&D and compliance.

- Supply Chain Disruptions: Global events can impact the availability of components and raw materials, affecting production timelines.

- Economic Volatility: Fluctuations in commodity prices and agricultural incomes can influence farmer purchasing decisions.

Emerging Opportunities in Europe Tractor Industry

Emerging opportunities in the Europe tractor industry lie in the accelerating adoption of autonomous tractors and the expansion of the electric tractor market. The demand for specialized tractors designed for niche agricultural applications, such as vineyards and orchards, continues to grow. Furthermore, the integration of IoT and AI in farm machinery presents opportunities for predictive maintenance, optimized fleet management, and data-driven farming decisions. The focus on sustainable agriculture is also opening avenues for tractors that utilize alternative fuels and offer reduced environmental impact.

Growth Accelerators in the Europe Tractor Industry Industry

Several catalysts are accelerating growth in the Europe tractor industry. The increasing adoption of digital farming technologies, including telematics and AI-powered analytics, is enhancing operational efficiency and driving demand for smart tractors. Strategic partnerships and collaborations between tractor manufacturers, technology providers, and agricultural cooperatives are fostering innovation and market expansion. Furthermore, government initiatives promoting sustainable agriculture and farm modernization are providing a significant impetus for the adoption of advanced machinery. The ongoing evolution of autonomous farming solutions represents a major growth accelerator, promising to revolutionize farm operations.

Key Players Shaping the Europe Tractor Industry Market

- Deere & Company

- CNH Industrial NV

- MTZ Servis

- Kubota Corporation

- Mahindra & Mahindra Ltd

- Argo Tractors SpA

- Claas KGaA mbH

- Tractors and Farm Equipment Limited

- SDF SpA

- AGCO Corporation

Notable Milestones in Europe Tractor Industry Sector

- December 2021: SDF and DEUTZ expanded their strategic partnership, agreeing to a long-term supply agreement for various engine ranges, including the DEUTZ TCD 4.1, 6.1, and 7.8 engines.

- December 2020: AGCO introduced the Challenger MT800 Series track tractors, featuring new engine/transmission combinations, an enhanced track and chassis system, improved hydraulic and hitch options, and a redesigned cab.

- September 2020: Fendt (AGCO Corporation) launched the Fendt 900 Vario MT Series track tractors, delivering superior performance, ride comfort, and operational efficiency.

- July 2020: Deere & Company released rugged, heavy-duty compact utility tractors, the 3D Series, offering a powerful, affordable, and user-friendly solution for agriculture.

In-Depth Europe Tractor Industry Market Outlook

The Europe tractor industry is set for robust growth, driven by technological innovation and the increasing global demand for sustainable food production. The expansion of precision agriculture technologies and the growing interest in autonomous tractors will be key growth accelerators. Strategic investments in R&D for electric and alternative fuel tractors are expected to shape the future market. Opportunities abound in catering to the evolving needs of farmers seeking efficiency, environmental responsibility, and data-driven farm management solutions, ensuring a dynamic and promising outlook for the sector.

Europe Tractor Industry Segmentation

- 1. Production Analysis

- 2. Consumption Analysis

- 3. Import Market Analysis (Value & Volume)

- 4. Export Market Analysis (Value & Volume)

- 5. Price Trend Analysis

Europe Tractor Industry Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

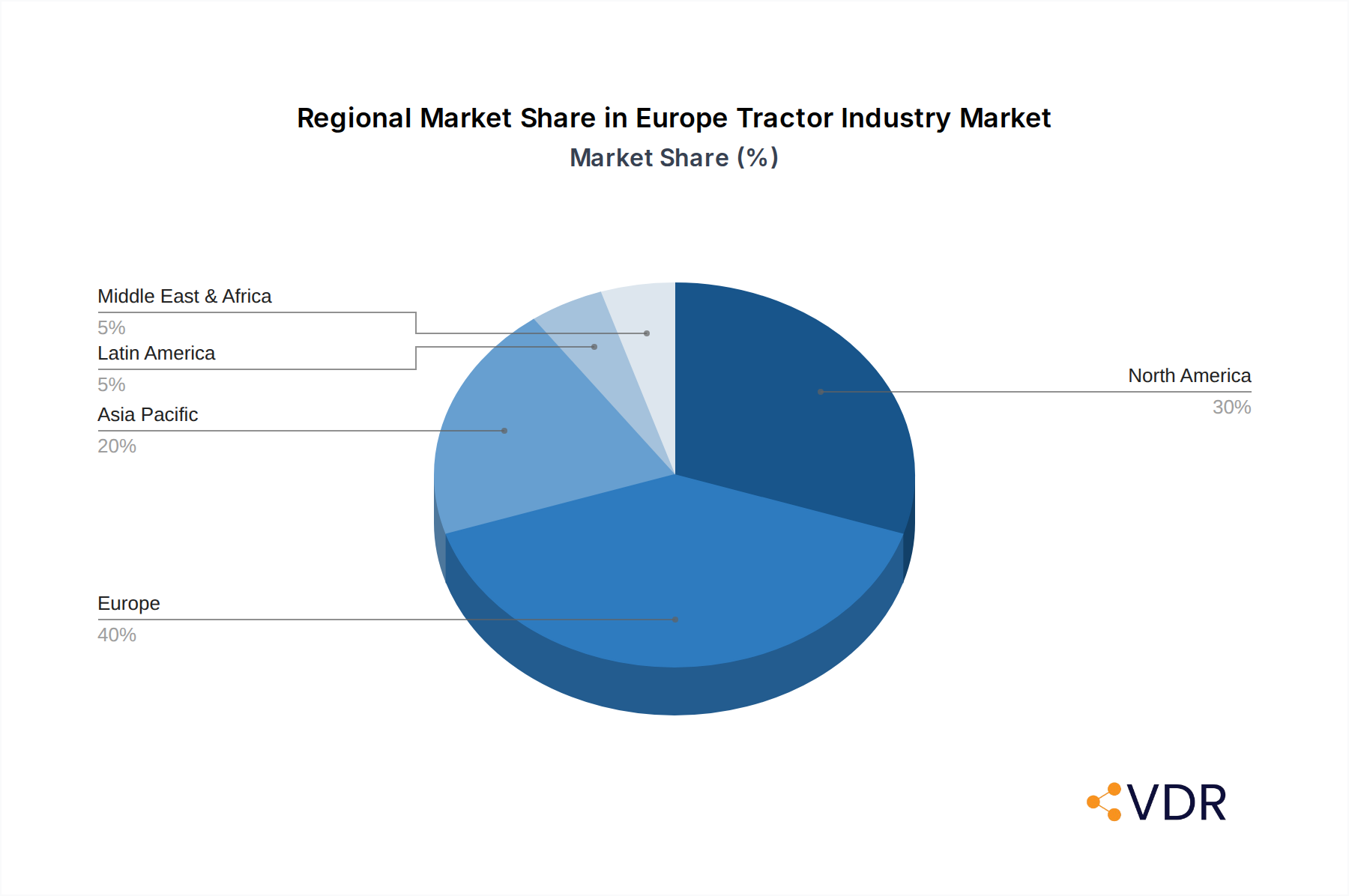

Europe Tractor Industry Regional Market Share

Geographic Coverage of Europe Tractor Industry

Europe Tractor Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.90% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Production Analysis

- 5.2. Market Analysis, Insights and Forecast - by Consumption Analysis

- 5.3. Market Analysis, Insights and Forecast - by Import Market Analysis (Value & Volume)

- 5.4. Market Analysis, Insights and Forecast - by Export Market Analysis (Value & Volume)

- 5.5. Market Analysis, Insights and Forecast - by Price Trend Analysis

- 5.6. Market Analysis, Insights and Forecast - by Region

- 5.6.1. Europe

- 6. Europe Tractor Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Production Analysis

- 6.2. Market Analysis, Insights and Forecast - by Consumption Analysis

- 6.3. Market Analysis, Insights and Forecast - by Import Market Analysis (Value & Volume)

- 6.4. Market Analysis, Insights and Forecast - by Export Market Analysis (Value & Volume)

- 6.5. Market Analysis, Insights and Forecast - by Price Trend Analysis

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Deere & Company

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 CNH Industrial NV

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 MTZ Servis

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Kubota Corporation

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Mahindra & Mahindra Ltd

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Argo Tractors SpA

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Claas KGaA mbH

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Tractors and Farm Equipment Limited

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 SDF SpA

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 AGCO Corporation

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Deere & Company

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Europe Tractor Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Europe Tractor Industry Share (%) by Company 2025

List of Tables

- Table 1: Europe Tractor Industry Revenue Million Forecast, by Production Analysis 2020 & 2033

- Table 2: Europe Tractor Industry Revenue Million Forecast, by Consumption Analysis 2020 & 2033

- Table 3: Europe Tractor Industry Revenue Million Forecast, by Import Market Analysis (Value & Volume) 2020 & 2033

- Table 4: Europe Tractor Industry Revenue Million Forecast, by Export Market Analysis (Value & Volume) 2020 & 2033

- Table 5: Europe Tractor Industry Revenue Million Forecast, by Price Trend Analysis 2020 & 2033

- Table 6: Europe Tractor Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 7: Europe Tractor Industry Revenue Million Forecast, by Production Analysis 2020 & 2033

- Table 8: Europe Tractor Industry Revenue Million Forecast, by Consumption Analysis 2020 & 2033

- Table 9: Europe Tractor Industry Revenue Million Forecast, by Import Market Analysis (Value & Volume) 2020 & 2033

- Table 10: Europe Tractor Industry Revenue Million Forecast, by Export Market Analysis (Value & Volume) 2020 & 2033

- Table 11: Europe Tractor Industry Revenue Million Forecast, by Price Trend Analysis 2020 & 2033

- Table 12: Europe Tractor Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 13: United Kingdom Europe Tractor Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: Germany Europe Tractor Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: France Europe Tractor Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Italy Europe Tractor Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: Spain Europe Tractor Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Netherlands Europe Tractor Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 19: Belgium Europe Tractor Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Sweden Europe Tractor Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 21: Norway Europe Tractor Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Poland Europe Tractor Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 23: Denmark Europe Tractor Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Tractor Industry?

The projected CAGR is approximately 4.90%.

2. Which companies are prominent players in the Europe Tractor Industry?

Key companies in the market include Deere & Company, CNH Industrial NV, MTZ Servis, Kubota Corporation, Mahindra & Mahindra Ltd, Argo Tractors SpA, Claas KGaA mbH, Tractors and Farm Equipment Limited, SDF SpA, AGCO Corporation.

3. What are the main segments of the Europe Tractor Industry?

The market segments include Production Analysis, Consumption Analysis, Import Market Analysis (Value & Volume), Export Market Analysis (Value & Volume), Price Trend Analysis.

4. Can you provide details about the market size?

The market size is estimated to be USD 15.47 Million as of 2022.

5. What are some drivers contributing to market growth?

Shortage of Skilled Labor; Government Support to Enhance Farm Mechanization.

6. What are the notable trends driving market growth?

Rising Farm Labor Cost is Driving the Market for Tractors.

7. Are there any restraints impacting market growth?

Heavy Initial Procurement Cost and High Expenditure on Maintenance.

8. Can you provide examples of recent developments in the market?

December 2021: A strategic partnership between SDF and DEUTZ was expanded. Both companies have a successful business partnership that began in the 1980s. The companies have reached an agreement for a long-term supply agreement to provide both the sub-4 and above-4 liter range engines and the DEUTZ TCD 4.1, 6.1, and 7.8 engines.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Tractor Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Tractor Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Tractor Industry?

To stay informed about further developments, trends, and reports in the Europe Tractor Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence