Key Insights

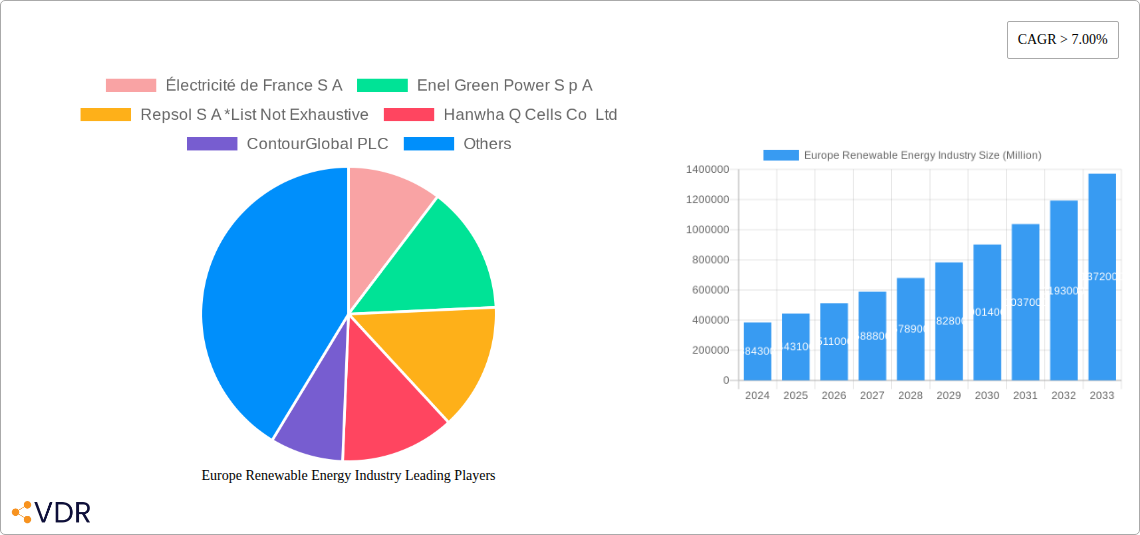

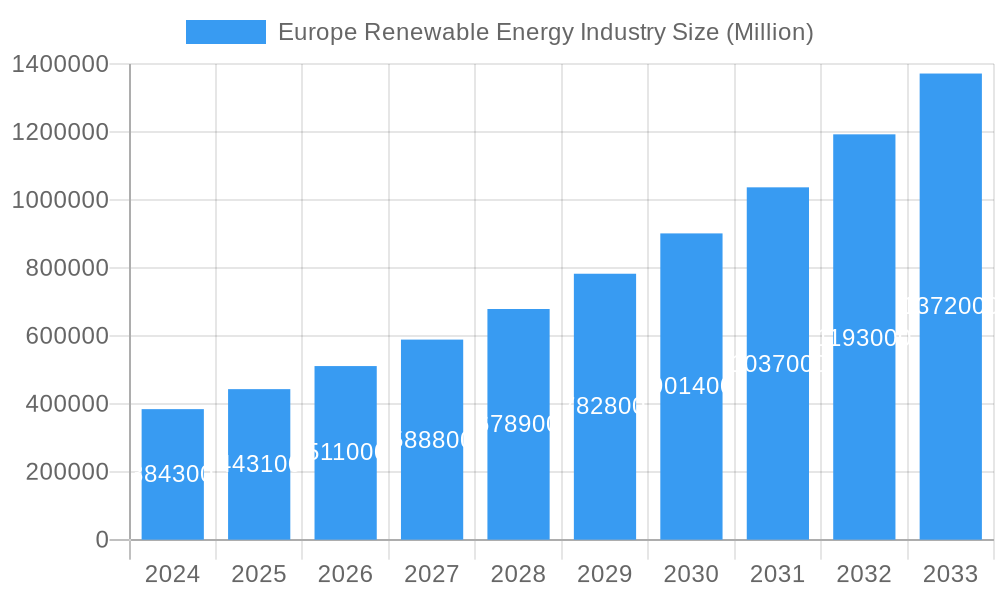

The Europe Renewable Energy Industry is poised for significant expansion, driven by a strong commitment to decarbonization and energy independence. The market size was an estimated $384.3 billion in 2024, and is projected to witness a robust CAGR of 15.3% over the forecast period of 2025-2033. This remarkable growth is fueled by increasing government incentives, favorable policy frameworks, and a growing awareness of the environmental and economic benefits of renewable energy sources. Key drivers include the urgent need to reduce greenhouse gas emissions, achieve climate targets, and diversify energy portfolios away from volatile fossil fuel markets. Investments in solar photovoltaic (PV) and wind power, both onshore and offshore, are expected to lead the charge, owing to technological advancements and declining costs. The "Others" segment, encompassing emerging technologies like green hydrogen and advanced geothermal, is also anticipated to gain traction, contributing to the overall dynamism of the sector.

Europe Renewable Energy Industry Market Size (In Billion)

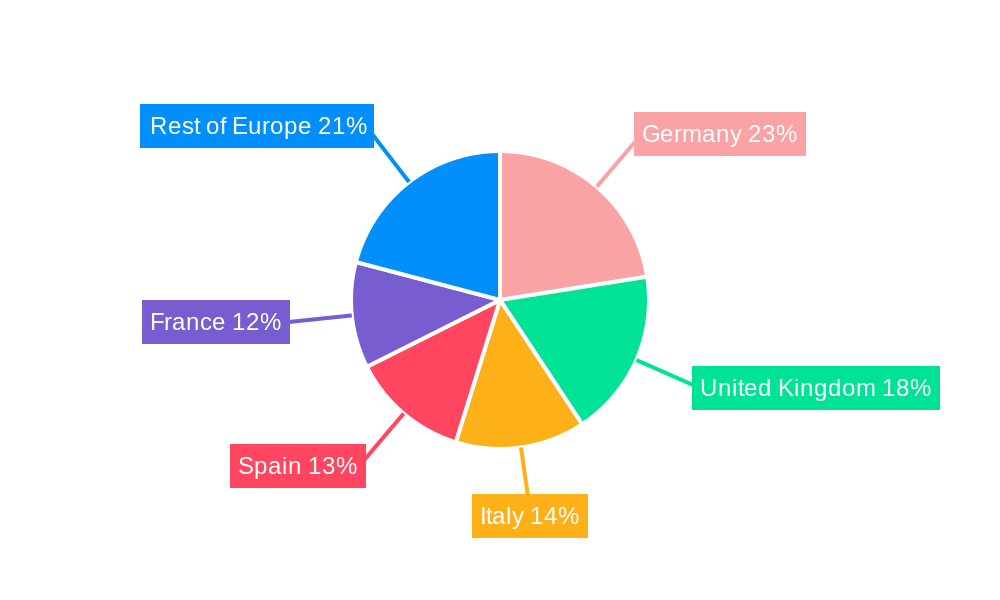

Despite the overwhelmingly positive outlook, certain restraints could temper the pace of growth. These include potential challenges in grid infrastructure modernization to accommodate the intermittent nature of solar and wind power, land acquisition complexities for large-scale projects, and the need for continuous innovation to improve energy storage solutions. However, the established players in the market, such as Électricité de France S.A., Enel Green Power S.p.A., and Vestas Wind Systems A/S, alongside emerging companies, are actively investing in research and development to overcome these hurdles. The European market is characterized by significant regional variations, with countries like Germany, the United Kingdom, Italy, Spain, and France leading in renewable energy adoption and investment, while the "Rest of Europe" also shows considerable potential for growth.

Europe Renewable Energy Industry Company Market Share

Europe Renewable Energy Industry Report: Driving Sustainable Growth and Innovation

This comprehensive report offers an in-depth analysis of the Europe Renewable Energy Industry, a rapidly expanding sector vital for the continent's sustainable future. We delve into market dynamics, growth trends, regional dominance, and the evolving product landscape, providing actionable insights for stakeholders. Covering the study period 2019–2033, with a base year of 2025 and forecast period 2025–2033, this report analyzes historical data from 2019–2024 to project future trajectories. Explore the immense potential of hydropower, solar, wind, and other renewable energy sources across Europe, identifying key drivers and emerging opportunities.

Europe Renewable Energy Industry Market Dynamics & Structure

The Europe Renewable Energy Industry is characterized by a fragmented yet increasingly consolidated market structure. Technological innovation, particularly in solar PV efficiency and wind turbine technology, remains a primary driver. Robust regulatory frameworks, including EU directives and national incentives, are crucial in accelerating adoption. Competitive product substitutes, such as fossil fuels, are gradually being displaced by the superior environmental and economic benefits of renewables. End-user demographics are shifting, with a growing demand for clean energy solutions from residential, commercial, and industrial sectors. Mergers and acquisitions (M&A) are on the rise as companies seek to expand their portfolios and gain market share. The market concentration is influenced by regional resource availability and government support.

- Technological Innovation: Continuous advancements in battery storage, smart grid technology, and offshore wind installations are key differentiators.

- Regulatory Frameworks: Ambitious climate targets and supportive policies for renewable energy deployment are critical for market growth.

- End-User Demand: Increasing corporate sustainability goals and consumer awareness of climate change are fueling demand.

- M&A Trends: Strategic acquisitions are consolidating the market, leading to larger, more integrated renewable energy players. The volume of M&A deals is expected to grow significantly, driven by the need for scale and diversification.

Europe Renewable Energy Industry Growth Trends & Insights

The Europe Renewable Energy Industry is poised for substantial growth, driven by a confluence of factors including ambitious decarbonization targets, declining technology costs, and increasing investor confidence. The market size is projected to experience significant expansion, with adoption rates for renewable energy sources accelerating across all segments. Technological disruptions, such as advancements in green hydrogen production and advanced energy storage systems, are set to redefine the energy landscape. Consumer behavior shifts towards sustainable consumption patterns are further bolstering the demand for renewable energy solutions. The integration of digitalization and AI in managing renewable energy assets promises enhanced efficiency and grid stability.

The market is anticipated to grow at a robust CAGR, reflecting a strong commitment to transitioning away from fossil fuels. The European Green Deal and its subsequent initiatives are foundational to this growth, providing a clear policy direction and financial incentives for renewable energy development. Countries across the continent are actively investing in expanding their renewable energy capacity, driven by energy security concerns and the imperative to combat climate change. The increasing affordability of solar panels and wind turbines has democratized access to renewable energy, making it a viable and often preferred option for both large-scale utility projects and distributed generation.

Furthermore, the evolving landscape of electric mobility and the increasing electrification of industrial processes are creating new demand centers for renewable electricity. This symbiotic relationship between renewable energy generation and energy consumption sectors is a key growth accelerator. Offshore wind farms, in particular, are emerging as a significant growth area, benefiting from technological advancements that allow for larger turbines and deployment in deeper waters. The development of interconnectors between national grids is also crucial for optimizing the utilization of renewable energy resources across Europe. The overall outlook for the Europe Renewable Energy Industry is exceptionally positive, characterized by sustained investment, policy support, and technological innovation. The market is expected to witness a substantial increase in its overall valuation, projected to reach multi-billion Euro figures by the end of the forecast period.

Dominant Regions, Countries, or Segments in Europe Renewable Energy Industry

The wind energy segment is a dominant force driving growth within the Europe Renewable Energy Industry. This dominance is fueled by a combination of favorable geographical conditions, supportive government policies, and continuous technological advancements in turbine efficiency and offshore deployment capabilities. Countries like Germany, Denmark, and the United Kingdom are leading the charge in wind power development, capitalizing on their extensive coastlines and robust industrial infrastructure. The increasing scale and sophistication of offshore wind farms have made them a cornerstone of Europe's renewable energy strategy.

Germany stands out as a leading country in renewable energy adoption, with a significant installed capacity in both solar PV and wind power. The country's "Energiewende" (energy transition) policy has been instrumental in driving this growth, supported by feed-in tariffs and other incentives that have fostered a mature and competitive market. The Nordic countries, particularly Norway and Sweden, are major contributors through their extensive hydropower resources, which provide a stable and consistent source of clean electricity. The United Kingdom, with its vast offshore wind potential, is also a key player, consistently breaking records in new capacity installations.

The solar energy segment is experiencing rapid expansion across Southern Europe, with countries like Spain and Italy leveraging their high solar irradiation levels. Government initiatives aimed at promoting rooftop solar installations and large-scale solar farms are accelerating adoption. The declining cost of solar panels has made solar energy increasingly competitive, even without subsidies in some regions. The "Others" segment, which includes geothermal energy, biomass, and emerging technologies like green hydrogen, also plays a crucial role in diversifying Europe's renewable energy mix. While currently smaller in scale compared to wind and solar, these segments hold significant future growth potential, particularly in specific industrial applications and for grid balancing. The interplay of these segments, supported by robust grid infrastructure and storage solutions, is critical for achieving Europe's ambitious renewable energy targets.

Europe Renewable Energy Industry Product Landscape

The Europe Renewable Energy Industry is defined by continuous product innovation aimed at enhancing efficiency, reliability, and cost-effectiveness. In the solar energy segment, advancements in photovoltaic (PV) module technology, including higher conversion efficiencies and bifacial panels, are becoming standard. Floating solar installations are emerging as a novel application, optimizing land use. For wind energy, larger and more powerful wind turbines, particularly offshore, are key developments, alongside innovations in blade design and materials to capture more wind energy. The hydropower sector sees ongoing upgrades to existing infrastructure and the development of small-scale and pumped-storage hydropower systems for grid flexibility. The "Others" segment is witnessing rapid innovation in battery storage technologies, from lithium-ion to next-generation solid-state batteries, crucial for intermittent renewable sources. Green hydrogen production technologies, such as advanced electrolyzers, are also gaining prominence, offering a versatile energy carrier.

Key Drivers, Barriers & Challenges in Europe Renewable Energy Industry

Key Drivers:

- Ambitious Climate Targets: EU and national government commitments to achieve net-zero emissions by 2050 are the primary growth catalysts.

- Declining Technology Costs: Significant reductions in the cost of solar PV and wind power equipment have made renewables increasingly competitive with fossil fuels.

- Energy Security Concerns: Geopolitical events have underscored the importance of diversified and domestically sourced energy.

- Technological Advancements: Ongoing innovations in efficiency, storage, and grid integration are improving the viability and attractiveness of renewables.

- Public and Corporate Demand: Growing awareness of climate change and increasing corporate sustainability goals are driving demand for clean energy.

Barriers & Challenges:

- Grid Integration and Infrastructure: The intermittency of some renewable sources requires substantial investment in grid upgrades and energy storage solutions.

- Regulatory and Permitting Hurdles: Complex and lengthy permitting processes can delay project development and increase costs.

- Supply Chain Dependencies: Reliance on certain raw materials and manufacturing capabilities can create vulnerabilities.

- Public Acceptance and NIMBYism: Local opposition to renewable energy projects, particularly wind farms, can pose significant challenges.

- Financing and Investment Risks: While investment is growing, perceived risks associated with long-term policy stability and market volatility can deter some investors. The total cost of grid modernization is estimated to be in the hundreds of billions of Euros.

Emerging Opportunities in Europe Renewable Energy Industry

Emerging opportunities in the Europe Renewable Energy Industry are abundant, particularly in the realm of offshore wind expansion into deeper waters and new markets, leveraging floating wind technologies. The development of green hydrogen ecosystems, from production to storage and utilization in industrial processes and transportation, represents a significant growth frontier. Decentralized energy systems and virtual power plants (VPPs), enabled by smart grid technologies and AI, offer new models for energy management and grid services. Furthermore, the increasing focus on circular economy principles within the renewable energy sector presents opportunities for recycling and repurposing of components. The integration of renewables with sustainable aviation fuels (SAFs) and electric vehicle charging infrastructure are also poised for substantial growth.

Growth Accelerators in the Europe Renewable Energy Industry Industry

Several key accelerators are driving long-term growth in the Europe Renewable Energy Industry. Technological breakthroughs in energy storage, such as improved battery density and lifespan, are critical for enhancing the reliability of intermittent renewables. Strategic partnerships and collaborations between energy companies, technology providers, and industrial consumers are fostering innovation and accelerating market penetration. Market expansion strategies, including cross-border interconnections and the development of new renewable energy hubs, are crucial for optimizing resource utilization and achieving economies of scale. The continued supportive policy environment at both the EU and national levels, with clear long-term targets and financial incentives, provides the necessary certainty for sustained investment.

Key Players Shaping the Europe Renewable Energy Industry Market

- Électricité de France S A

- Enel Green Power S p A

- Repsol S A

- Hanwha Q Cells Co Ltd

- ContourGlobal PLC

- Acciona S A

- Abengoa SA

- Andritz AG

Notable Milestones in Europe Renewable Energy Industry Sector

- September 2022: Orsted AS entered into an agreement with Ostwind, a developer of wind and solar PV projects in Germany and France, to acquire a 100 per cent equity interest in OSTWIND Erneuerbare Energien GmbH, OSTWINDpark Rotmainquelle GmbH & Co. K.G., OSTWIND International S.A.S., and OSTWIND Engineering S.A.S., significantly expanding its renewable project pipeline and market presence in key European regions.

- September 2022: Mercedes-Benz, a German luxury and commercial vehicle automotive manufacturer, announced its plan to build a wind farm in the northwestern German state of Lower Saxony, by the year 2025, which will be able to produce one hundred megawatts of electricity, equivalent to over 15 per cent of the carmaker's annual demand in Germany, highlighting a growing trend of industrial self-sufficiency in renewable power generation.

In-Depth Europe Renewable Energy Industry Market Outlook

The Europe Renewable Energy Industry is set for a robust future, driven by an unwavering commitment to sustainability and energy independence. Growth accelerators include continued innovation in energy storage, enabling greater grid stability and the efficient integration of intermittent renewables. Strategic partnerships across the value chain will unlock new project opportunities and accelerate the deployment of cutting-edge technologies. Market expansion will be facilitated by enhanced cross-border electricity interconnections and the development of new renewable energy zones. Policy certainty and the ongoing decarbonization imperative will ensure sustained investment, creating a dynamic and rapidly evolving market landscape. The industry's outlook is exceptionally promising, with significant opportunities for economic growth, job creation, and a cleaner energy future for Europe. The projected market valuation is expected to surpass €500 billion by the end of the forecast period.

Europe Renewable Energy Industry Segmentation

-

1. Type

- 1.1. Hydropower

- 1.2. Solar

- 1.3. Wind

- 1.4. Others

Europe Renewable Energy Industry Segmentation By Geography

- 1. Germany

- 2. United Kingdom

- 3. Italy

- 4. Spain

- 5. France

- 6. Rest of Europe

Europe Renewable Energy Industry Regional Market Share

Geographic Coverage of Europe Renewable Energy Industry

Europe Renewable Energy Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 14.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Hydropower

- 5.1.2. Solar

- 5.1.3. Wind

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Germany

- 5.2.2. United Kingdom

- 5.2.3. Italy

- 5.2.4. Spain

- 5.2.5. France

- 5.2.6. Rest of Europe

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Europe Renewable Energy Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Hydropower

- 6.1.2. Solar

- 6.1.3. Wind

- 6.1.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Germany Europe Renewable Energy Industry Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Hydropower

- 7.1.2. Solar

- 7.1.3. Wind

- 7.1.4. Others

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. United Kingdom Europe Renewable Energy Industry Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Hydropower

- 8.1.2. Solar

- 8.1.3. Wind

- 8.1.4. Others

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Italy Europe Renewable Energy Industry Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Hydropower

- 9.1.2. Solar

- 9.1.3. Wind

- 9.1.4. Others

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Spain Europe Renewable Energy Industry Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Hydropower

- 10.1.2. Solar

- 10.1.3. Wind

- 10.1.4. Others

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. France Europe Renewable Energy Industry Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Hydropower

- 11.1.2. Solar

- 11.1.3. Wind

- 11.1.4. Others

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Rest of Europe Europe Renewable Energy Industry Analysis, Insights and Forecast, 2021-2033

- 12.1. Market Analysis, Insights and Forecast - by Type

- 12.1.1. Hydropower

- 12.1.2. Solar

- 12.1.3. Wind

- 12.1.4. Others

- 12.1. Market Analysis, Insights and Forecast - by Type

- 13. Competitive Analysis

- 13.1. Company Profiles

- 13.1.1 Électricité de France S A

- 13.1.1.1. Company Overview

- 13.1.1.2. Products

- 13.1.1.3. Company Financials

- 13.1.1.4. SWOT Analysis

- 13.1.2 Enel Green Power S p A

- 13.1.2.1. Company Overview

- 13.1.2.2. Products

- 13.1.2.3. Company Financials

- 13.1.2.4. SWOT Analysis

- 13.1.3 Repsol S A *List Not Exhaustive

- 13.1.3.1. Company Overview

- 13.1.3.2. Products

- 13.1.3.3. Company Financials

- 13.1.3.4. SWOT Analysis

- 13.1.4 Hanwha Q Cells Co Ltd

- 13.1.4.1. Company Overview

- 13.1.4.2. Products

- 13.1.4.3. Company Financials

- 13.1.4.4. SWOT Analysis

- 13.1.5 ContourGlobal PLC

- 13.1.5.1. Company Overview

- 13.1.5.2. Products

- 13.1.5.3. Company Financials

- 13.1.5.4. SWOT Analysis

- 13.1.6 Acciona S A

- 13.1.6.1. Company Overview

- 13.1.6.2. Products

- 13.1.6.3. Company Financials

- 13.1.6.4. SWOT Analysis

- 13.1.7 Abengoa SA

- 13.1.7.1. Company Overview

- 13.1.7.2. Products

- 13.1.7.3. Company Financials

- 13.1.7.4. SWOT Analysis

- 13.1.8 Andritz AG

- 13.1.8.1. Company Overview

- 13.1.8.2. Products

- 13.1.8.3. Company Financials

- 13.1.8.4. SWOT Analysis

- 13.1.1 Électricité de France S A

- 13.2. Market Entropy

- 13.2.1 Company's Key Areas Served

- 13.2.2 Recent Developments

- 13.3. Company Market Share Analysis 2025

- 13.3.1 Top 5 Companies Market Share Analysis

- 13.3.2 Top 3 Companies Market Share Analysis

- 13.4. List of Potential Customers

- 14. Research Methodology

List of Figures

- Figure 1: Europe Renewable Energy Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Europe Renewable Energy Industry Share (%) by Company 2025

List of Tables

- Table 1: Europe Renewable Energy Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 2: Europe Renewable Energy Industry Volume Gigawatt Forecast, by Type 2020 & 2033

- Table 3: Europe Renewable Energy Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Europe Renewable Energy Industry Volume Gigawatt Forecast, by Region 2020 & 2033

- Table 5: Europe Renewable Energy Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 6: Europe Renewable Energy Industry Volume Gigawatt Forecast, by Type 2020 & 2033

- Table 7: Europe Renewable Energy Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 8: Europe Renewable Energy Industry Volume Gigawatt Forecast, by Country 2020 & 2033

- Table 9: Europe Renewable Energy Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 10: Europe Renewable Energy Industry Volume Gigawatt Forecast, by Type 2020 & 2033

- Table 11: Europe Renewable Energy Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 12: Europe Renewable Energy Industry Volume Gigawatt Forecast, by Country 2020 & 2033

- Table 13: Europe Renewable Energy Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 14: Europe Renewable Energy Industry Volume Gigawatt Forecast, by Type 2020 & 2033

- Table 15: Europe Renewable Energy Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 16: Europe Renewable Energy Industry Volume Gigawatt Forecast, by Country 2020 & 2033

- Table 17: Europe Renewable Energy Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 18: Europe Renewable Energy Industry Volume Gigawatt Forecast, by Type 2020 & 2033

- Table 19: Europe Renewable Energy Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 20: Europe Renewable Energy Industry Volume Gigawatt Forecast, by Country 2020 & 2033

- Table 21: Europe Renewable Energy Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 22: Europe Renewable Energy Industry Volume Gigawatt Forecast, by Type 2020 & 2033

- Table 23: Europe Renewable Energy Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 24: Europe Renewable Energy Industry Volume Gigawatt Forecast, by Country 2020 & 2033

- Table 25: Europe Renewable Energy Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 26: Europe Renewable Energy Industry Volume Gigawatt Forecast, by Type 2020 & 2033

- Table 27: Europe Renewable Energy Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 28: Europe Renewable Energy Industry Volume Gigawatt Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Renewable Energy Industry?

The projected CAGR is approximately 14.6%.

2. Which companies are prominent players in the Europe Renewable Energy Industry?

Key companies in the market include Électricité de France S A, Enel Green Power S p A, Repsol S A *List Not Exhaustive, Hanwha Q Cells Co Ltd, ContourGlobal PLC, Acciona S A, Abengoa SA, Andritz AG.

3. What are the main segments of the Europe Renewable Energy Industry?

The market segments include Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 1711.51 billion as of 2022.

5. What are some drivers contributing to market growth?

Integration of Renewable Energy4.; Supportive Government Policies.

6. What are the notable trends driving market growth?

Wind Energy Segment is Expected to Dominate the Market.

7. Are there any restraints impacting market growth?

High infrastructure costs.

8. Can you provide examples of recent developments in the market?

In September 2022, Orsted AS entered into an agreement with Ostwind, a developer of wind and solar PV projects in Germany and France, to acquire a 100 per cent equity interest in OSTWIND Erneuerbare Energien GmbH, OSTWINDpark Rotmainquelle GmbH & Co. K.G., OSTWIND International S.A.S., and OSTWIND Engineering S.A.S.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in Gigawatt.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Renewable Energy Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Renewable Energy Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Renewable Energy Industry?

To stay informed about further developments, trends, and reports in the Europe Renewable Energy Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence