Key Insights

The European Military Aviation Market is poised for steady growth, projected to reach USD 67.81 billion by 2025, with a Compound Annual Growth Rate (CAGR) of 2.98% during the forecast period of 2025-2033. This expansion is primarily driven by the increasing demand for advanced multi-role aircraft and sophisticated rotorcraft to enhance national defense capabilities and respond to evolving geopolitical landscapes. European nations are heavily investing in modernizing their air forces, focusing on platforms that offer versatility, superior performance, and enhanced operational effectiveness. Key investment areas include the procurement of next-generation fighter jets, transport aircraft for logistical support and troop deployment, and multi-mission helicopters for surveillance, attack, and rescue operations. The emphasis on technological superiority and the need to replace aging fleets are significant catalysts for this market's sustained upward trajectory.

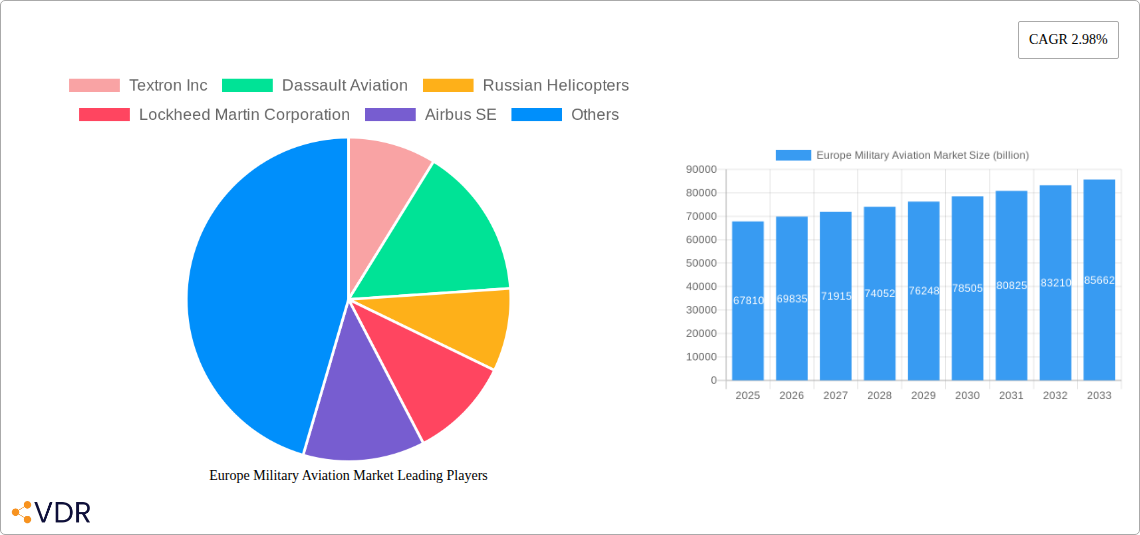

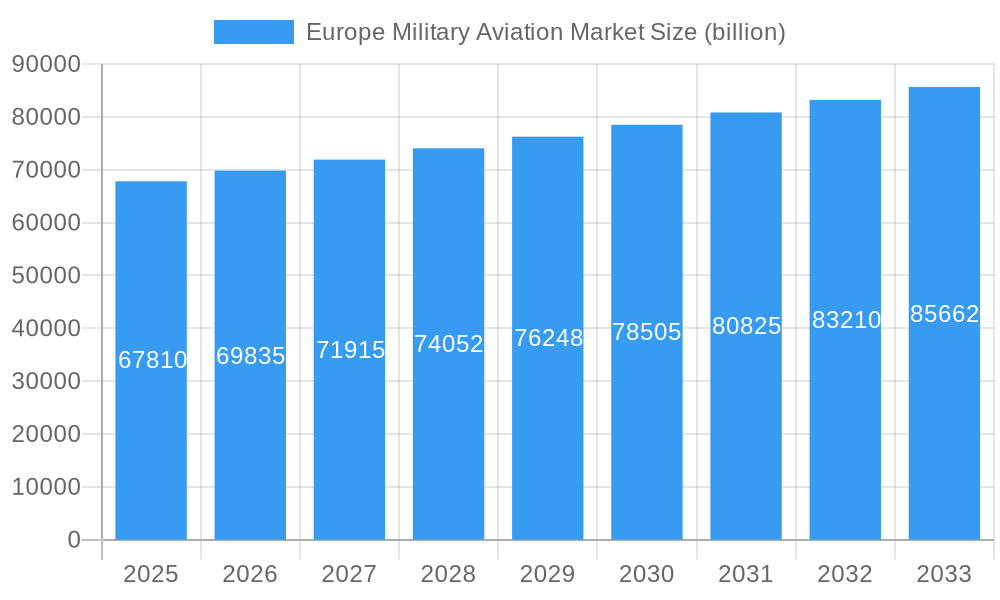

Europe Military Aviation Market Market Size (In Billion)

Further bolstering market expansion are key trends such as the growing adoption of unmanned aerial vehicles (UAVs) and the integration of artificial intelligence (AI) in military aviation systems, enhancing situational awareness and operational efficiency. The focus on joint military exercises and interoperability among NATO allies also stimulates demand for standardized and advanced aviation platforms. However, the market faces certain restraints, including stringent budgetary allocations for defense in some European countries and the high cost associated with research, development, and procurement of cutting-edge military aircraft. Despite these challenges, the unwavering commitment to national security, coupled with ongoing technological advancements and strategic alliances, ensures a robust and dynamic future for the European Military Aviation Market. Key players like Airbus SE, Dassault Aviation, and Leonardo S.p.A. are at the forefront, investing in innovation and strategic partnerships to secure a significant market share.

Europe Military Aviation Market Company Market Share

Here's the SEO-optimized report description for the Europe Military Aviation Market, incorporating your specified keywords, structure, and data.

Europe Military Aviation Market: Comprehensive Analysis, Growth Forecasts (2024-2033) & Industry Trends

This in-depth report provides a definitive outlook on the Europe Military Aviation Market, offering critical insights into its dynamics, growth trajectories, and competitive landscape. Spanning the study period of 2019–2033, with a base year of 2025, this analysis delves into the intricacies of fixed-wing aircraft and rotorcraft segments, forecasting market evolution with precision. We uncover key drivers, barriers, and emerging opportunities shaping the future of military aviation in Europe, essential for strategic decision-making by defense procurement agencies, manufacturers like Airbus SE, Dassault Aviation, and The Boeing Company, and defense technology providers. The report leverages comprehensive data to pinpoint dominant regions, countries, and specific aircraft types like Multi-Role Aircraft and Multi-Mission Helicopters that are fueling market expansion. Understand the impact of significant industry developments, such as the US State Department's approval of a USD 8.5 billion CH-47 Chinook helicopter sale to Germany and Boeing's contract for 184 AH-64E Apache attack helicopters. Gain an edge with our detailed product landscape, market trends, and exclusive insights into the strategies of key players including Lockheed Martin Corporation, Textron Inc., and Russian Helicopters.

Europe Military Aviation Market Market Dynamics & Structure

The Europe Military Aviation Market is characterized by a moderate level of concentration, with major global players like Airbus SE, The Boeing Company, and Lockheed Martin Corporation holding significant market shares. However, the presence of specialized regional manufacturers and the increasing demand for advanced indigenous capabilities create a dynamic competitive environment. Technological innovation serves as a primary driver, with ongoing advancements in areas such as unmanned aerial systems (UAS), artificial intelligence (AI) for combat systems, and next-generation propulsion technologies pushing the boundaries of military aviation capabilities. Regulatory frameworks, primarily driven by NATO standards and national defense policies, are crucial in dictating procurement cycles and technological specifications. Competitive product substitutes are emerging, particularly in the drone and electronic warfare sectors, challenging traditional manned aircraft dominance. End-user demographics are shifting towards a greater emphasis on multi-role platforms and advanced training solutions to meet evolving geopolitical threats. Mergers and acquisitions (M&A) trends, while not as aggressive as in other sectors, are strategic, focusing on acquiring specialized capabilities or consolidating market positions. For instance, past M&A activities have aimed at bolstering capabilities in areas like rotorcraft or advanced avionics.

- Market Concentration: Moderate, with a mix of global giants and specialized regional players.

- Technological Innovation Drivers: AI integration, UAS development, advanced sensor technology, and stealth capabilities.

- Regulatory Frameworks: NATO standards, national defense procurement policies, export controls.

- Competitive Product Substitutes: Advanced drones, cyber warfare capabilities, electronic intelligence platforms.

- End-User Demographics: Focus on modernization, interoperability, and cost-effectiveness.

- M&A Trends: Strategic acquisitions for technology enhancement and market consolidation.

Europe Military Aviation Market Growth Trends & Insights

The Europe Military Aviation Market is poised for robust growth, driven by escalating geopolitical tensions, modernization imperatives, and the increasing adoption of advanced technologies. The market size is projected to witness a compound annual growth rate (CAGR) of approximately 4.5% from 2025 to 2033. This expansion is fueled by significant defense budget allocations across key European nations aiming to upgrade aging fleets and enhance operational readiness. The adoption rates of advanced fixed-wing aircraft, particularly multi-role fighters and transport aircraft, are accelerating as countries seek greater flexibility and expeditionary capabilities. Similarly, the rotorcraft segment, encompassing multi-mission helicopters and transport helicopters, is experiencing strong demand for versatile platforms capable of a wide array of operations, from troop transport and combat search and rescue to intelligence, surveillance, and reconnaissance (ISR). Technological disruptions, such as the integration of AI in avionics, advanced stealth technologies, and the development of unmanned combat aerial vehicles (UCAVs), are not only enhancing existing platforms but also paving the way for entirely new operational concepts. Consumer behavior shifts, or rather, end-user (military) procurement strategies, are increasingly prioritizing life-cycle cost, interoperability, and the ability to integrate with coalition forces. The market penetration of highly sophisticated electronic warfare suites and advanced situational awareness systems is also on the rise, reflecting a broader trend towards information dominance. The European market is also witnessing a growing interest in sustainable aviation solutions, though military applications are still in nascent stages.

XXX, a leading market research firm, projects that the overall market value for Europe's military aviation sector will reach an estimated USD 85.7 billion by 2033, up from approximately USD 60.1 billion in 2025. This sustained growth is underpinned by a combination of planned fleet upgrades, new platform development programs, and substantial investments in defense R&D across the continent. The increasing emphasis on multi-domain operations further necessitates the acquisition of integrated air and missile defense systems, alongside advanced aerospace platforms that can operate seamlessly across land, sea, and air.

Dominant Regions, Countries, or Segments in Europe Military Aviation Market

Within the Europe Military Aviation Market, Western Europe stands out as the dominant region, largely driven by the substantial defense expenditures and modernization programs of key nations like France, Germany, the United Kingdom, and Italy. These countries, with their robust industrial bases and advanced technological capabilities, consistently lead in the adoption of cutting-edge military aviation solutions. The dominance is further amplified by their active participation in multinational defense initiatives and their role as significant contributors to NATO's collective security.

- France: A powerhouse in military aviation, with companies like Dassault Aviation at the forefront of developing advanced fighter jets (e.g., Rafale) and transport aircraft. France's commitment to indigenous defense production and technological sovereignty significantly boosts its market share.

- Germany: Undergoing a significant military modernization effort, Germany's defense budget increases are directly translating into substantial procurement of both fixed-wing aircraft and rotorcraft. The potential sale of CH-47 Chinook helicopters signifies this renewed focus.

- United Kingdom: With a strong heritage in aerospace and defense, the UK continues to invest heavily in its air force, focusing on next-generation fighter programs and advanced helicopter capabilities, supported by companies like BAE Systems.

- Italy: Home to Leonardo S.p.A., Italy plays a crucial role in the rotorcraft segment and is a key partner in several multinational fixed-wing aircraft programs, contributing significantly to the European market.

Analyzing by Sub Aircraft Type, Fixed-Wing Aircraft represents the largest and most influential segment. Within this, Multi-Role Aircraft are the primary growth engine. These versatile platforms, capable of air-to-air combat, air-to-ground attack, ISR, and electronic warfare, are crucial for modern military operations. Nations are investing in platforms like the Eurofighter Typhoon, Rafale, and the upcoming FCAS (Future Combat Air System) to maintain air superiority and execute complex missions. The Transport Aircraft sub-segment also holds considerable importance, with ongoing requirements for strategic and tactical airlift capabilities to support expeditionary operations, humanitarian aid, and troop deployment. The demand for larger, more capable transport aircraft, such as the Airbus A400M, underscores this trend.

While Rotorcraft also plays a vital role, particularly the Multi-Mission Helicopter category for its adaptability in reconnaissance, attack, and special operations, the sheer scale of investment and the strategic imperative for air superiority place Fixed-Wing Aircraft, especially Multi-Role variants, at the forefront of market dominance. The market share within these segments is continuously influenced by ongoing defense reviews, international collaborations, and the development of new combat aircraft technologies.

Europe Military Aviation Market Product Landscape

The Europe Military Aviation Market is defined by continuous product innovation and the development of highly sophisticated platforms designed for multi-domain operations. Key product innovations include the integration of advanced sensor suites, improved stealth technologies, and enhanced electronic warfare capabilities across both fixed-wing aircraft and rotorcraft. For instance, newer variants of multi-role aircraft are equipped with state-of-the-art radar systems and data links that improve situational awareness and interoperability. Rotorcraft are increasingly featuring advanced avionic systems, improved survivability measures, and modular mission equipment to adapt to diverse operational requirements. Performance metrics are being pushed by advancements in engine efficiency, aerodynamic design, and payload capacity. Unique selling propositions often revolve around modularity, adaptability, and the ability to be integrated into networked warfare environments. Technological advancements are also focusing on reducing the operational footprint and enhancing the survivability of platforms in contested airspace.

Key Drivers, Barriers & Challenges in Europe Military Aviation Market

Key Drivers: The primary forces propelling the Europe Military Aviation Market include escalating geopolitical tensions and the perceived need for enhanced national security. Nations are increasingly prioritizing defense modernization to counter evolving threats, leading to substantial investments in upgrading and expanding their air fleets. Technological advancements, particularly in areas like AI-driven avionics, unmanned systems, and advanced sensor technology, are significant drivers, offering enhanced capabilities and operational efficiency. Furthermore, a strong emphasis on interoperability within NATO and other alliances necessitates the procurement of standardized and technologically advanced platforms. The development of indigenous defense industries and the drive for technological sovereignty also contribute to market growth, encouraging national R&D and procurement of locally manufactured systems.

Barriers & Challenges: Despite the growth, the market faces several significant challenges. High acquisition and lifecycle costs of advanced military aircraft present a substantial financial barrier for many nations. Stringent regulatory frameworks and lengthy procurement processes can delay the deployment of new technologies. Supply chain disruptions, exacerbated by global events, pose risks to production timelines and the availability of critical components. Furthermore, the competitive pressure from global defense manufacturers and the increasing reliance on complex technological systems require significant investment in skilled personnel and maintenance infrastructure, which can be a constraint for some European nations. Cybersecurity threats targeting military aviation systems are also a growing concern, requiring continuous investment in defense mechanisms.

Emerging Opportunities in Europe Military Aviation Market

Emerging opportunities within the Europe Military Aviation Market lie in the increasing demand for unmanned aerial systems (UAS) and their integration with manned platforms. The development of advanced drone swarming capabilities, AI-powered autonomous flight systems, and sophisticated electronic warfare payloads for drones present a significant growth avenue. There is also a growing interest in the modernization and life-extension of existing platforms, offering opportunities for upgrade packages and mid-life enhancements. The evolving threat landscape is driving demand for specialized aircraft, such as advanced ISR platforms and dedicated electronic attack aircraft. Furthermore, the focus on sustainable aviation, while nascent in the military sector, could open opportunities for research and development into alternative fuels and more energy-efficient designs in the long term. The growing emphasis on resilient and distributed operations also creates demand for smaller, more agile, and networked platforms.

Growth Accelerators in the Europe Military Aviation Market Industry

Several catalysts are driving long-term growth in the Europe Military Aviation Market. Technological breakthroughs in areas like advanced materials, hypersonic propulsion, and directed energy weapons are set to revolutionize future combat air capabilities, spurring significant R&D investment. Strategic partnerships and collaborations between European defense companies, such as those involved in the Future Combat Air System (FCAS) program, are accelerating the development and adoption of next-generation platforms. Market expansion strategies, including increased defense spending by Eastern European nations and a renewed focus on collective security within NATO, are creating sustained demand for new aircraft and associated defense systems. The ongoing evolution of warfare towards multi-domain operations is also a key accelerator, pushing for the integration of air assets with land, sea, and cyber capabilities, thereby driving demand for versatile and networked military aircraft.

Key Players Shaping the Europe Military Aviation Market Market

- Textron Inc.

- Dassault Aviation

- Russian Helicopters

- Lockheed Martin Corporation

- Airbus SE

- MD Helicopters LLC

- United Aircraft Corporation

- Pilatus Aircraft Ltd

- Leonardo S.p.A.

- ATR

- Hughes Helicopters

- The Boeing Company

Notable Milestones in Europe Military Aviation Market Sector

- June 2023: Airbus Flight Academy Europe, a subsidiary of Airbus that supplies training services for the pilots and civilian cadets of the French Armed Forces, signed a memorandum of understanding (MoU) with AURA AERO, indicating a potential for future collaboration in pilot training and advanced aerospace solutions.

- May 2023: The US State Department approved a potential sale of CH-47 Chinook helicopters, engines, and associated equipment worth USD 8.5 billion to Germany, highlighting significant modernization efforts and a growing demand for heavy-lift rotorcraft in Europe.

- March 2023: Boeing was awarded a contract by the US government to manufacture 184 AH-64E Apache attack helicopters for the US military and international customers. The US government announced USD 1.95 million for these helicopters, slated for delivery to the US military, Australia, and Egypt by the end of 2027 as part of the Foreign Military Sales (FMS) program, showcasing continued demand for advanced attack rotorcraft globally.

In-Depth Europe Military Aviation Market Market Outlook

The Europe Military Aviation Market is poised for sustained expansion, driven by a confluence of geopolitical imperatives and technological advancements. Growth accelerators include the ongoing commitment to defense modernization across the continent, the development of sophisticated, multi-role platforms, and the increasing integration of artificial intelligence and unmanned systems. Strategic partnerships and collaborative defense programs will further bolster innovation and market penetration. The evolving security landscape necessitates enhanced air power, creating substantial opportunities for both fixed-wing aircraft and rotorcraft manufacturers. This outlook signifies a dynamic period of investment and development, with a focus on enhancing operational capabilities, interoperability, and strategic resilience for European armed forces.

Europe Military Aviation Market Segmentation

-

1. Sub Aircraft Type

-

1.1. Fixed-Wing Aircraft

- 1.1.1. Multi-Role Aircraft

- 1.1.2. Training Aircraft

- 1.1.3. Transport Aircraft

- 1.1.4. Others

-

1.2. Rotorcraft

- 1.2.1. Multi-Mission Helicopter

- 1.2.2. Transport Helicopter

-

1.1. Fixed-Wing Aircraft

Europe Military Aviation Market Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

Europe Military Aviation Market Regional Market Share

Geographic Coverage of Europe Military Aviation Market

Europe Military Aviation Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 2.98% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Sub Aircraft Type

- 5.1.1. Fixed-Wing Aircraft

- 5.1.1.1. Multi-Role Aircraft

- 5.1.1.2. Training Aircraft

- 5.1.1.3. Transport Aircraft

- 5.1.1.4. Others

- 5.1.2. Rotorcraft

- 5.1.2.1. Multi-Mission Helicopter

- 5.1.2.2. Transport Helicopter

- 5.1.1. Fixed-Wing Aircraft

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Sub Aircraft Type

- 6. Europe Military Aviation Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Sub Aircraft Type

- 6.1.1. Fixed-Wing Aircraft

- 6.1.1.1. Multi-Role Aircraft

- 6.1.1.2. Training Aircraft

- 6.1.1.3. Transport Aircraft

- 6.1.1.4. Others

- 6.1.2. Rotorcraft

- 6.1.2.1. Multi-Mission Helicopter

- 6.1.2.2. Transport Helicopter

- 6.1.1. Fixed-Wing Aircraft

- 6.1. Market Analysis, Insights and Forecast - by Sub Aircraft Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Textron Inc

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Dassault Aviation

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Russian Helicopters

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Lockheed Martin Corporation

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Airbus SE

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 MD Helicopters LLC

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 United Aircraft Corporatio

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Pilatus Aircraft Ltd

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Leonardo S p A

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 ATR

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Hughes Helicopters

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 The Boeing Company

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.1 Textron Inc

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Europe Military Aviation Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Europe Military Aviation Market Share (%) by Company 2025

List of Tables

- Table 1: Europe Military Aviation Market Revenue billion Forecast, by Sub Aircraft Type 2020 & 2033

- Table 2: Europe Military Aviation Market Revenue billion Forecast, by Region 2020 & 2033

- Table 3: Europe Military Aviation Market Revenue billion Forecast, by Sub Aircraft Type 2020 & 2033

- Table 4: Europe Military Aviation Market Revenue billion Forecast, by Country 2020 & 2033

- Table 5: United Kingdom Europe Military Aviation Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 6: Germany Europe Military Aviation Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 7: France Europe Military Aviation Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Italy Europe Military Aviation Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Spain Europe Military Aviation Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Netherlands Europe Military Aviation Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Belgium Europe Military Aviation Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Sweden Europe Military Aviation Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Norway Europe Military Aviation Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Poland Europe Military Aviation Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Denmark Europe Military Aviation Market Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Military Aviation Market?

The projected CAGR is approximately 2.98%.

2. Which companies are prominent players in the Europe Military Aviation Market?

Key companies in the market include Textron Inc, Dassault Aviation, Russian Helicopters, Lockheed Martin Corporation, Airbus SE, MD Helicopters LLC, United Aircraft Corporatio, Pilatus Aircraft Ltd, Leonardo S p A, ATR, Hughes Helicopters, The Boeing Company.

3. What are the main segments of the Europe Military Aviation Market?

The market segments include Sub Aircraft Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 67.81 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

June 2023: Airbus Flight Academy Europe, a subsidiary of Airbus that supplies training services for the pilots and civilian cadets of the French Armed Forces, signed a memorandum of understanding (MoU) with AURA AERO.May 2023: The US State Department approved a potential sale of CH-47 Chinook helicopters, engines, and equipment worth USD 8.5 billion to Germany.March 2023: Boeing has been awarded a contract by the US government to manufacture 184 AH-64E Apache attack helicopters for the US military and international customers. The US government announced USD 1.95 million, indicating that the helicopter will be delivered to the US military and overseas buyers - specifically Australia and Egypt - as a part of the paramilitary process to the Foreign Service (FMS) from the US government. Contract completion is expected by the end of 2027.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Military Aviation Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Military Aviation Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Military Aviation Market?

To stay informed about further developments, trends, and reports in the Europe Military Aviation Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence