Key Insights

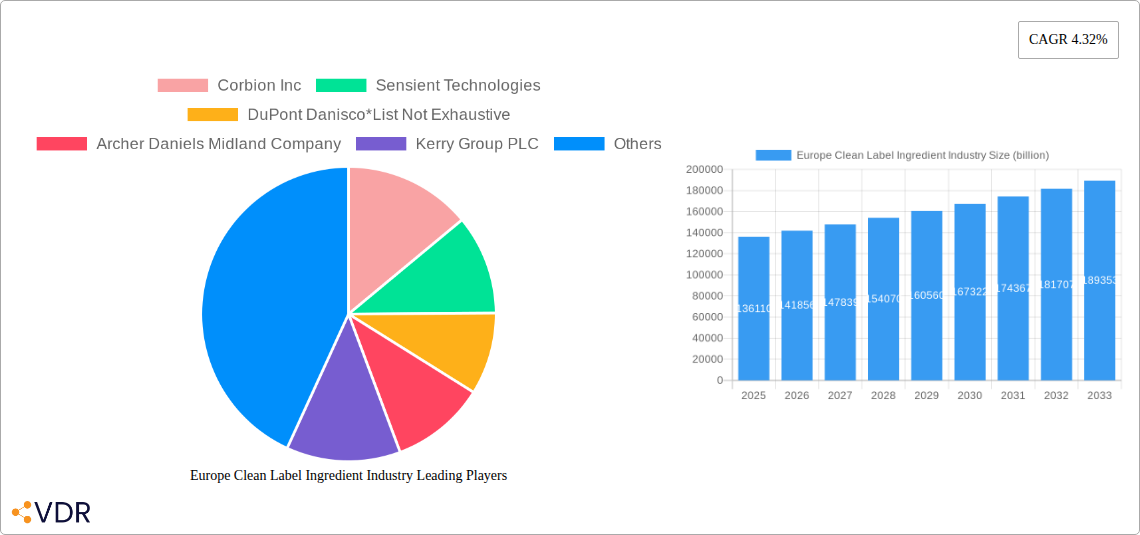

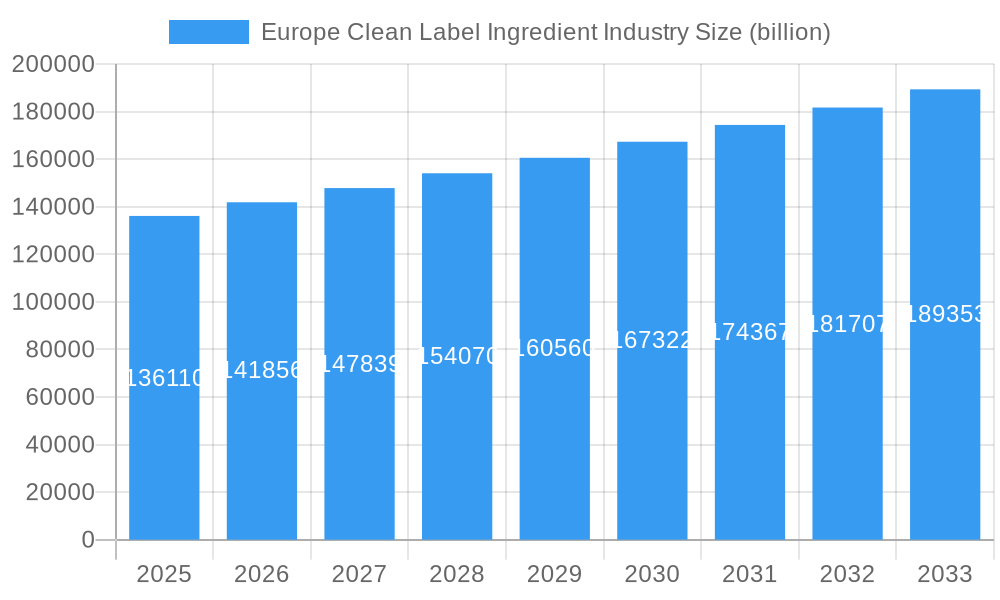

The Europe Clean Label Ingredient market is poised for significant expansion, projecting a market size of USD 136.11 billion in 2025. This growth is underpinned by a robust CAGR of 4.32% throughout the forecast period, indicating a consistent upward trajectory. Consumer demand for transparency and healthier food options is a primary driver, pushing manufacturers to reformulate products with recognizable, minimally processed ingredients. Key ingredient types fueling this trend include natural colorants and flavors, which are seeing accelerated adoption as consumers actively seek to avoid synthetic additives. Furthermore, the demand for natural sweeteners and preservatives is on the rise, driven by concerns over sugar intake and the desire for extended shelf life without artificial chemicals. These factors collectively shape a dynamic market where innovation in ingredient sourcing and processing is paramount for success.

Europe Clean Label Ingredient Industry Market Size (In Billion)

The beverage sector, followed closely by bakery and confectionery, are the dominant application segments within the European clean label market. Consumers are increasingly scrutinizing beverage labels for natural ingredients, while the allure of healthier, yet indulgent, baked goods and sweets is driving demand for clean label alternatives. Emerging trends also point towards a growing preference for clean label solutions in dairy and frozen desserts, as well as other processed food categories. Despite this positive outlook, certain restraints could influence the market's pace. These may include the higher cost of naturally sourced ingredients compared to their synthetic counterparts, potential challenges in achieving desired product functionalities with limited ingredient palettes, and evolving regulatory landscapes across different European nations. Key players like Corbion Inc., Sensient Technologies, and DuPont Danisco are actively investing in R&D to address these challenges and capitalize on the burgeoning opportunities in this evolving market.

Europe Clean Label Ingredient Industry Company Market Share

Europe Clean Label Ingredient Industry: Market Analysis, Growth Trends, and Future Outlook (2019-2033)

Report Description:

Dive into the dynamic Europe Clean Label Ingredient Industry with this comprehensive market report, offering an in-depth analysis from 2019 to 2033. This report is meticulously crafted for industry professionals seeking to understand market concentration, growth drivers, regional dominance, and key player strategies within the burgeoning clean label segment. With a base year of 2025 and a forecast period extending to 2033, this study leverages extensive historical data (2019-2024) and estimated figures to provide actionable insights. We meticulously examine parent and child market segments, crucial for understanding the intricate value chain and identifying lucrative niches within the European food and beverage landscape. This report is your definitive guide to navigating the evolving demands for natural, transparent, and minimally processed ingredients across various applications.

Europe Clean Label Ingredient Industry Market Dynamics & Structure

The Europe Clean Label Ingredient Industry is characterized by a moderate market concentration, with a few key players holding significant market share while a growing number of smaller, innovative companies are emerging. Technological innovation remains a primary driver, fueled by consumer demand for recognizable ingredients and enhanced nutritional profiles. Regulatory frameworks, such as those promoting natural sourcing and simplified ingredient lists, are increasingly shaping product development and market entry strategies. Competitive product substitutes are abundant, ranging from traditional synthetic additives to novel natural alternatives, intensifying the need for differentiation. End-user demographics are shifting towards younger, health-conscious consumers actively seeking transparency in food production. Mergers and acquisitions (M&A) are a notable trend, with larger corporations acquiring innovative startups to expand their clean label portfolios and gain market access. For instance, the recent acquisition of [Specific Company Name] by [Acquiring Company Name] for an estimated $1.2 billion underscores this consolidation. Barriers to innovation include the high cost of research and development for novel ingredients, scalability challenges, and the need for rigorous scientific validation to meet regulatory and consumer acceptance standards.

- Market Concentration: Moderate, with key players and a growing number of SMEs.

- Technological Innovation Drivers: Consumer demand for natural and recognizable ingredients, demand for enhanced nutritional profiles.

- Regulatory Frameworks: Increasingly supportive of natural sourcing and simplified ingredient lists.

- Competitive Product Substitutes: Abundant, including synthetic additives and novel natural alternatives.

- End-User Demographics: Growing segment of health-conscious consumers prioritizing transparency.

- M&A Trends: Significant consolidation driven by the pursuit of clean label portfolios.

- Innovation Barriers: High R&D costs, scalability issues, stringent scientific validation requirements.

Europe Clean Label Ingredient Industry Growth Trends & Insights

The Europe Clean Label Ingredient Industry is poised for robust growth, projected to reach an estimated market size of $XX billion by 2033. This expansion is driven by a confluence of factors including evolving consumer preferences, stringent regulatory landscapes, and continuous technological advancements. The adoption rates for clean label ingredients have accelerated significantly over the historical period (2019-2024), with consumers demonstrating a clear preference for products with fewer, recognizable ingredients. This shift is particularly evident in the Bakery and Confectionery and Beverage application segments, which are anticipated to lead market penetration. Technological disruptions, such as advancements in fermentation techniques and plant-based protein extraction, are enabling the development of novel clean label solutions that offer comparable or superior functionality to traditional ingredients. Consumer behavior is undergoing a profound transformation; transparency is no longer a niche concern but a mainstream expectation, compelling manufacturers to reformulate products and prioritize ingredient sourcing. The CAGR for the clean label ingredient market in Europe is estimated at XX% during the forecast period (2025-2033). This growth is further substantiated by an increasing awareness of the health benefits associated with natural ingredients and a growing concern about the potential long-term effects of artificial additives. The industry is witnessing a surge in demand for specific ingredient categories like natural colorants derived from fruits and vegetables, and natural preservatives that extend shelf life without compromising on health perceptions.

The market size is expected to grow from an estimated $XX billion in the base year 2025 to $XX billion by 2033. This represents a substantial increase, highlighting the significant opportunities within this sector. Adoption rates are projected to climb as more food and beverage manufacturers respond to consumer demand and regulatory pressures. Technological advancements, including enzymatic modification of starches and the development of advanced extraction methods for natural flavors, will continue to democratize the availability and affordability of clean label solutions. Consumer behavior shifts are deeply ingrained, with an emphasis on "free-from" claims and a preference for ingredients that consumers can understand and pronounce. This trend is expected to sustain and amplify the demand for clean label ingredients across all food categories. The increasing availability of plant-based alternatives also contributes to the clean label movement, aligning with consumer preferences for sustainable and ethical sourcing.

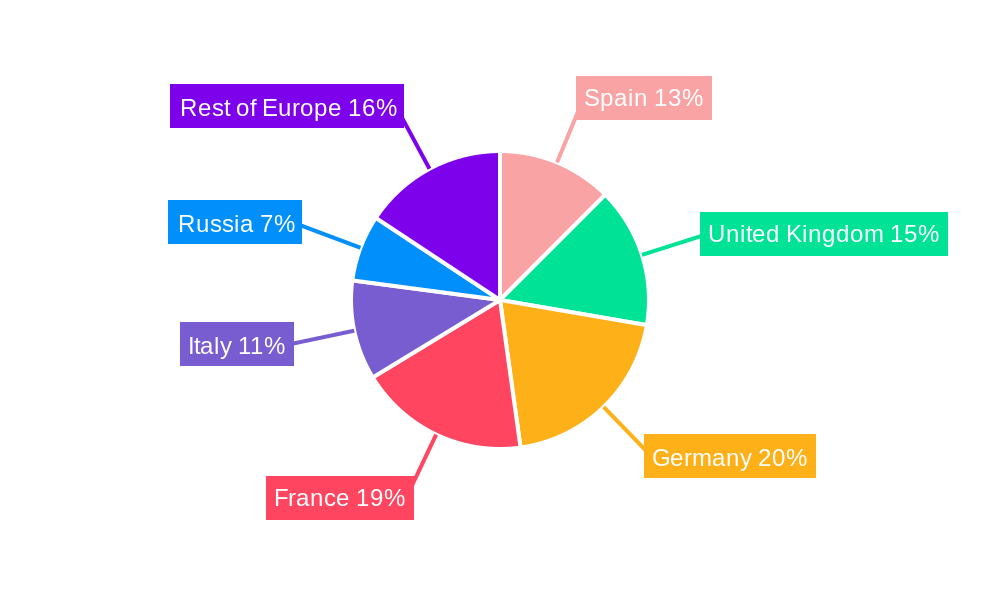

Dominant Regions, Countries, or Segments in Europe Clean Label Ingredient Industry

Germany and the United Kingdom are emerging as dominant countries within the Europe Clean Label Ingredient Industry, driven by strong consumer demand for transparency and a mature food and beverage sector. The Beverage and Bakery and Confectionery application segments are currently leading market growth, propelled by high consumer awareness and manufacturers' proactive reformulation efforts. In the Ingredient Type segment, Flavors and Flavor Enhancers are experiencing substantial demand, as consumers seek natural alternatives to artificial flavorings.

- Dominant Country: Germany, with an estimated market share of XX% in 2025, due to its robust regulatory environment and strong consumer advocacy for natural products.

- Dominant Application: Beverage, estimated at $XX billion market size in 2025, driven by demand for natural sweeteners, colors, and flavors in juices, carbonated drinks, and functional beverages.

- Dominant Ingredient Type: Flavors and Flavor Enhancers, expected to reach $XX billion in 2025, fueled by the desire for authentic and natural taste profiles.

- Key Drivers in Germany: High disposable income, strong environmental consciousness, and stringent food safety regulations promoting natural ingredients.

- Key Drivers in the UK: Growing health and wellness trend, significant influence of social media on consumer choices, and a proactive approach by retailers to stock clean label products.

- Growth Potential in Beverage Segment: Driven by innovation in plant-based milk alternatives and the increasing popularity of functional beverages with natural ingredients.

- Growth Potential in Bakery and Confectionery: Fueled by demand for natural colors, preservatives, and sweeteners in cakes, biscuits, and sweets.

- Market Share of Flavors and Flavor Enhancers: Anticipated to hold a XX% share of the total clean label ingredient market in 2025, with significant growth potential.

- Economic Policies: Favorable government initiatives promoting sustainable agriculture and food production contribute to the growth of natural ingredient sourcing.

- Infrastructure: Well-established supply chains for sourcing natural raw materials and advanced manufacturing capabilities enable efficient production of clean label ingredients.

- Consumer Awareness: High levels of consumer education regarding the benefits of clean label ingredients are a critical factor in regional dominance.

Europe Clean Label Ingredient Industry Product Landscape

The product landscape in the Europe Clean Label Ingredient Industry is characterized by continuous innovation focused on replicating the functionality of conventional ingredients using natural sources. Key product developments include natural colorants derived from fruits, vegetables, and algae, offering vibrant hues without artificial dyes. Natural preservatives, such as cultured dairy products and plant extracts, are gaining traction for their effectiveness in extending shelf life. Furthermore, the market is seeing a rise in plant-based sweeteners, derived from stevia, monk fruit, and erythritol, meeting the growing demand for sugar reduction. Companies are also developing clean label flavors and flavor enhancers that mimic traditional tastes, utilizing fermentation and extraction technologies. These innovations aim to provide solutions for applications in beverages, bakery, confectionery, dairy, and processed foods, emphasizing improved performance metrics like heat stability, pH tolerance, and shelf-life extension, thereby offering unique selling propositions for manufacturers seeking to meet consumer demand for healthier and more transparent food options.

Key Drivers, Barriers & Challenges in Europe Clean Label Ingredient Industry

The Europe Clean Label Ingredient Industry is primarily propelled by the escalating consumer demand for natural, minimally processed, and transparently sourced ingredients. This is reinforced by evolving regulatory landscapes that increasingly favor simpler ingredient lists and fewer artificial additives. Technological advancements in extraction, fermentation, and plant-based ingredient processing are crucial enablers, making cleaner alternatives more accessible and functional.

Conversely, the industry faces significant challenges. The high cost of research and development for novel natural ingredients, coupled with the complexities of scaling up production while maintaining quality and consistency, presents a major barrier. Regulatory hurdles, particularly in ensuring the safety and efficacy of new natural ingredients, can be time-consuming and expensive. Supply chain issues, including the seasonal availability and price volatility of natural raw materials, also pose a significant constraint. Competitive pressures from established conventional ingredient suppliers and the constant need for consumer education regarding the benefits and efficacy of clean label alternatives add to the complexity of this market.

Emerging Opportunities in Europe Clean Label Ingredient Industry

Emerging opportunities within the Europe Clean Label Ingredient Industry lie in the untapped potential of lesser-known natural extracts with potent antioxidant and antimicrobial properties. The growing demand for sustainable and ethically sourced ingredients presents a significant avenue for innovation, particularly for plant-based proteins and alternative sweeteners derived from waste streams. Furthermore, the expansion of clean label solutions into niche applications such as infant nutrition and specialized dietary products offers substantial growth prospects. Evolving consumer preferences for functional foods that offer health benefits beyond basic nutrition are also creating a demand for ingredients that deliver specific health outcomes.

Growth Accelerators in the Europe Clean Label Ingredient Industry Industry

Several catalysts are accelerating the growth of the Europe Clean Label Ingredient Industry. Technological breakthroughs in biotechnology and precision fermentation are enabling the development of cost-effective and highly functional clean label ingredients at scale. Strategic partnerships between ingredient manufacturers and major food and beverage companies are crucial for faster market penetration and product innovation. Furthermore, market expansion strategies targeting emerging European economies with growing middle classes and increasing awareness of health and wellness trends are vital for sustained growth. The increasing focus on sustainable sourcing and the circular economy within the food industry also acts as a significant growth accelerator, aligning with broader societal and environmental concerns.

Key Players Shaping the Europe Clean Label Ingredient Market

- Corbion Inc

- Sensient Technologies

- DuPont Danisco

- Archer Daniels Midland Company

- Kerry Group PLC

- Koninklijke DSM NV

- Cargill Inc

- Ingredion Incorporated

- Tate & Lyle

Notable Milestones in Europe Clean Label Ingredient Industry Sector

- 2023 Q2: Corbion Inc. launched a new range of natural emulsifiers for bakery applications, enhancing texture and shelf-life.

- 2023 Q4: Sensient Technologies expanded its natural colorant portfolio with the introduction of vibrant shades derived from microalgae.

- 2024 Q1: DuPont Danisco announced a strategic partnership to develop novel fermentation-based clean label preservatives.

- 2024 Q3: Archer Daniels Midland Company acquired a specialty plant-based protein producer, bolstering its clean label ingredient offerings.

- 2024 Q4: Kerry Group PLC invested in a new R&D center focused on clean label flavor solutions.

In-Depth Europe Clean Label Ingredient Industry Market Outlook

The future market potential of the Europe Clean Label Ingredient Industry is exceptionally bright, driven by sustained consumer demand for transparency and health-conscious products. Growth accelerators, including continuous technological innovation in areas like enzyme technology and plant-based ingredient processing, will empower manufacturers to offer increasingly sophisticated and functional clean label solutions. Strategic partnerships between ingredient suppliers and food brands are expected to become more prevalent, fostering co-creation and accelerating market adoption. Expanding into underserved segments and emerging markets within Europe will be a key strategy for companies looking to capitalize on this growth trajectory. The industry's commitment to sustainability and ethical sourcing will further solidify its position as a cornerstone of the future food landscape.

Europe Clean Label Ingredient Industry Segmentation

-

1. Ingredient Type

- 1.1. Colorants

- 1.2. Flavors and Flavor Enhancers

- 1.3. Food Sweeteners

- 1.4. Preservatives

- 1.5. Others

-

2. Application

- 2.1. Beverage

- 2.2. Bakery and Confectionery

- 2.3. Sauce and Condiment

- 2.4. Dairy and Frozen Dessert

- 2.5. Other Processed Foods

Europe Clean Label Ingredient Industry Segmentation By Geography

- 1. Spain

- 2. United Kingdom

- 3. Germany

- 4. France

- 5. Italy

- 6. Russia

- 7. Rest of Europe

Europe Clean Label Ingredient Industry Regional Market Share

Geographic Coverage of Europe Clean Label Ingredient Industry

Europe Clean Label Ingredient Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.32% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Ingredient Type

- 5.1.1. Colorants

- 5.1.2. Flavors and Flavor Enhancers

- 5.1.3. Food Sweeteners

- 5.1.4. Preservatives

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Beverage

- 5.2.2. Bakery and Confectionery

- 5.2.3. Sauce and Condiment

- 5.2.4. Dairy and Frozen Dessert

- 5.2.5. Other Processed Foods

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Spain

- 5.3.2. United Kingdom

- 5.3.3. Germany

- 5.3.4. France

- 5.3.5. Italy

- 5.3.6. Russia

- 5.3.7. Rest of Europe

- 5.1. Market Analysis, Insights and Forecast - by Ingredient Type

- 6. Europe Clean Label Ingredient Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Ingredient Type

- 6.1.1. Colorants

- 6.1.2. Flavors and Flavor Enhancers

- 6.1.3. Food Sweeteners

- 6.1.4. Preservatives

- 6.1.5. Others

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Beverage

- 6.2.2. Bakery and Confectionery

- 6.2.3. Sauce and Condiment

- 6.2.4. Dairy and Frozen Dessert

- 6.2.5. Other Processed Foods

- 6.1. Market Analysis, Insights and Forecast - by Ingredient Type

- 7. Spain Europe Clean Label Ingredient Industry Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Ingredient Type

- 7.1.1. Colorants

- 7.1.2. Flavors and Flavor Enhancers

- 7.1.3. Food Sweeteners

- 7.1.4. Preservatives

- 7.1.5. Others

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Beverage

- 7.2.2. Bakery and Confectionery

- 7.2.3. Sauce and Condiment

- 7.2.4. Dairy and Frozen Dessert

- 7.2.5. Other Processed Foods

- 7.1. Market Analysis, Insights and Forecast - by Ingredient Type

- 8. United Kingdom Europe Clean Label Ingredient Industry Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Ingredient Type

- 8.1.1. Colorants

- 8.1.2. Flavors and Flavor Enhancers

- 8.1.3. Food Sweeteners

- 8.1.4. Preservatives

- 8.1.5. Others

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Beverage

- 8.2.2. Bakery and Confectionery

- 8.2.3. Sauce and Condiment

- 8.2.4. Dairy and Frozen Dessert

- 8.2.5. Other Processed Foods

- 8.1. Market Analysis, Insights and Forecast - by Ingredient Type

- 9. Germany Europe Clean Label Ingredient Industry Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Ingredient Type

- 9.1.1. Colorants

- 9.1.2. Flavors and Flavor Enhancers

- 9.1.3. Food Sweeteners

- 9.1.4. Preservatives

- 9.1.5. Others

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Beverage

- 9.2.2. Bakery and Confectionery

- 9.2.3. Sauce and Condiment

- 9.2.4. Dairy and Frozen Dessert

- 9.2.5. Other Processed Foods

- 9.1. Market Analysis, Insights and Forecast - by Ingredient Type

- 10. France Europe Clean Label Ingredient Industry Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Ingredient Type

- 10.1.1. Colorants

- 10.1.2. Flavors and Flavor Enhancers

- 10.1.3. Food Sweeteners

- 10.1.4. Preservatives

- 10.1.5. Others

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Beverage

- 10.2.2. Bakery and Confectionery

- 10.2.3. Sauce and Condiment

- 10.2.4. Dairy and Frozen Dessert

- 10.2.5. Other Processed Foods

- 10.1. Market Analysis, Insights and Forecast - by Ingredient Type

- 11. Italy Europe Clean Label Ingredient Industry Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Ingredient Type

- 11.1.1. Colorants

- 11.1.2. Flavors and Flavor Enhancers

- 11.1.3. Food Sweeteners

- 11.1.4. Preservatives

- 11.1.5. Others

- 11.2. Market Analysis, Insights and Forecast - by Application

- 11.2.1. Beverage

- 11.2.2. Bakery and Confectionery

- 11.2.3. Sauce and Condiment

- 11.2.4. Dairy and Frozen Dessert

- 11.2.5. Other Processed Foods

- 11.1. Market Analysis, Insights and Forecast - by Ingredient Type

- 12. Russia Europe Clean Label Ingredient Industry Analysis, Insights and Forecast, 2021-2033

- 12.1. Market Analysis, Insights and Forecast - by Ingredient Type

- 12.1.1. Colorants

- 12.1.2. Flavors and Flavor Enhancers

- 12.1.3. Food Sweeteners

- 12.1.4. Preservatives

- 12.1.5. Others

- 12.2. Market Analysis, Insights and Forecast - by Application

- 12.2.1. Beverage

- 12.2.2. Bakery and Confectionery

- 12.2.3. Sauce and Condiment

- 12.2.4. Dairy and Frozen Dessert

- 12.2.5. Other Processed Foods

- 12.1. Market Analysis, Insights and Forecast - by Ingredient Type

- 13. Rest of Europe Europe Clean Label Ingredient Industry Analysis, Insights and Forecast, 2021-2033

- 13.1. Market Analysis, Insights and Forecast - by Ingredient Type

- 13.1.1. Colorants

- 13.1.2. Flavors and Flavor Enhancers

- 13.1.3. Food Sweeteners

- 13.1.4. Preservatives

- 13.1.5. Others

- 13.2. Market Analysis, Insights and Forecast - by Application

- 13.2.1. Beverage

- 13.2.2. Bakery and Confectionery

- 13.2.3. Sauce and Condiment

- 13.2.4. Dairy and Frozen Dessert

- 13.2.5. Other Processed Foods

- 13.1. Market Analysis, Insights and Forecast - by Ingredient Type

- 14. Competitive Analysis

- 14.1. Company Profiles

- 14.1.1 Corbion Inc

- 14.1.1.1. Company Overview

- 14.1.1.2. Products

- 14.1.1.3. Company Financials

- 14.1.1.4. SWOT Analysis

- 14.1.2 Sensient Technologies

- 14.1.2.1. Company Overview

- 14.1.2.2. Products

- 14.1.2.3. Company Financials

- 14.1.2.4. SWOT Analysis

- 14.1.3 DuPont Danisco*List Not Exhaustive

- 14.1.3.1. Company Overview

- 14.1.3.2. Products

- 14.1.3.3. Company Financials

- 14.1.3.4. SWOT Analysis

- 14.1.4 Archer Daniels Midland Company

- 14.1.4.1. Company Overview

- 14.1.4.2. Products

- 14.1.4.3. Company Financials

- 14.1.4.4. SWOT Analysis

- 14.1.5 Kerry Group PLC

- 14.1.5.1. Company Overview

- 14.1.5.2. Products

- 14.1.5.3. Company Financials

- 14.1.5.4. SWOT Analysis

- 14.1.6 Koninklijke DSM NV

- 14.1.6.1. Company Overview

- 14.1.6.2. Products

- 14.1.6.3. Company Financials

- 14.1.6.4. SWOT Analysis

- 14.1.7 Cargill Inc

- 14.1.7.1. Company Overview

- 14.1.7.2. Products

- 14.1.7.3. Company Financials

- 14.1.7.4. SWOT Analysis

- 14.1.8 Ingredion Incorporated

- 14.1.8.1. Company Overview

- 14.1.8.2. Products

- 14.1.8.3. Company Financials

- 14.1.8.4. SWOT Analysis

- 14.1.9 Tate & Lyle

- 14.1.9.1. Company Overview

- 14.1.9.2. Products

- 14.1.9.3. Company Financials

- 14.1.9.4. SWOT Analysis

- 14.1.1 Corbion Inc

- 14.2. Market Entropy

- 14.2.1 Company's Key Areas Served

- 14.2.2 Recent Developments

- 14.3. Company Market Share Analysis 2025

- 14.3.1 Top 5 Companies Market Share Analysis

- 14.3.2 Top 3 Companies Market Share Analysis

- 14.4. List of Potential Customers

- 15. Research Methodology

List of Figures

- Figure 1: Europe Clean Label Ingredient Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Europe Clean Label Ingredient Industry Share (%) by Company 2025

List of Tables

- Table 1: Europe Clean Label Ingredient Industry Revenue billion Forecast, by Ingredient Type 2020 & 2033

- Table 2: Europe Clean Label Ingredient Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 3: Europe Clean Label Ingredient Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Europe Clean Label Ingredient Industry Revenue billion Forecast, by Ingredient Type 2020 & 2033

- Table 5: Europe Clean Label Ingredient Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 6: Europe Clean Label Ingredient Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: Europe Clean Label Ingredient Industry Revenue billion Forecast, by Ingredient Type 2020 & 2033

- Table 8: Europe Clean Label Ingredient Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 9: Europe Clean Label Ingredient Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 10: Europe Clean Label Ingredient Industry Revenue billion Forecast, by Ingredient Type 2020 & 2033

- Table 11: Europe Clean Label Ingredient Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 12: Europe Clean Label Ingredient Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Europe Clean Label Ingredient Industry Revenue billion Forecast, by Ingredient Type 2020 & 2033

- Table 14: Europe Clean Label Ingredient Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 15: Europe Clean Label Ingredient Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 16: Europe Clean Label Ingredient Industry Revenue billion Forecast, by Ingredient Type 2020 & 2033

- Table 17: Europe Clean Label Ingredient Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 18: Europe Clean Label Ingredient Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 19: Europe Clean Label Ingredient Industry Revenue billion Forecast, by Ingredient Type 2020 & 2033

- Table 20: Europe Clean Label Ingredient Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 21: Europe Clean Label Ingredient Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 22: Europe Clean Label Ingredient Industry Revenue billion Forecast, by Ingredient Type 2020 & 2033

- Table 23: Europe Clean Label Ingredient Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 24: Europe Clean Label Ingredient Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Clean Label Ingredient Industry?

The projected CAGR is approximately 4.32%.

2. Which companies are prominent players in the Europe Clean Label Ingredient Industry?

Key companies in the market include Corbion Inc, Sensient Technologies, DuPont Danisco*List Not Exhaustive, Archer Daniels Midland Company, Kerry Group PLC, Koninklijke DSM NV, Cargill Inc, Ingredion Incorporated, Tate & Lyle.

3. What are the main segments of the Europe Clean Label Ingredient Industry?

The market segments include Ingredient Type, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 136.11 billion as of 2022.

5. What are some drivers contributing to market growth?

Rising Demand for Processed Foods; Strategic Initiatives by Companies Uplifting Market Growth.

6. What are the notable trends driving market growth?

Growing Awareness Regarding the Consumption of Artificial Food Additives.

7. Are there any restraints impacting market growth?

Availability of Substitute Products.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Clean Label Ingredient Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Clean Label Ingredient Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Clean Label Ingredient Industry?

To stay informed about further developments, trends, and reports in the Europe Clean Label Ingredient Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence