Key Insights

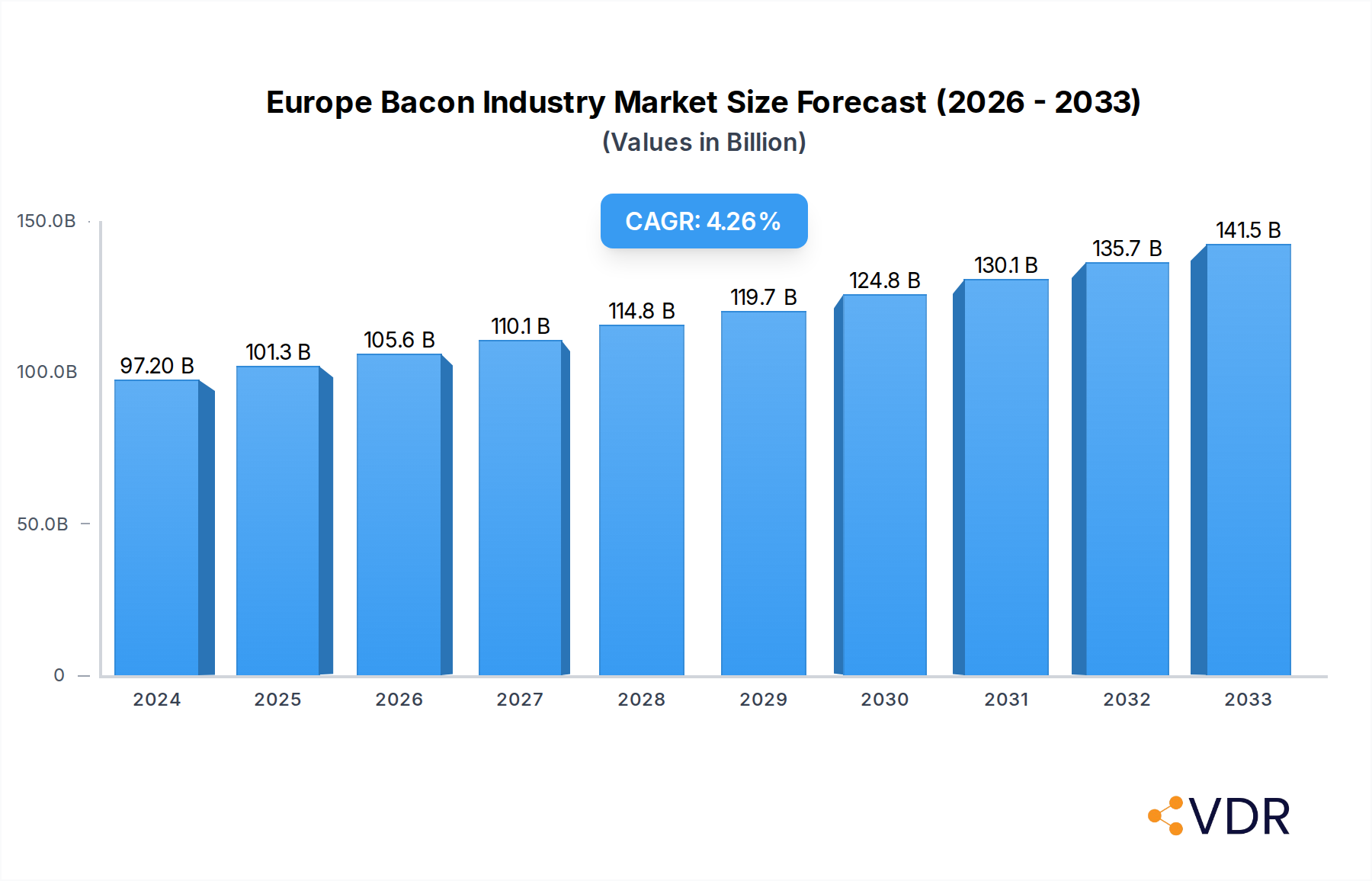

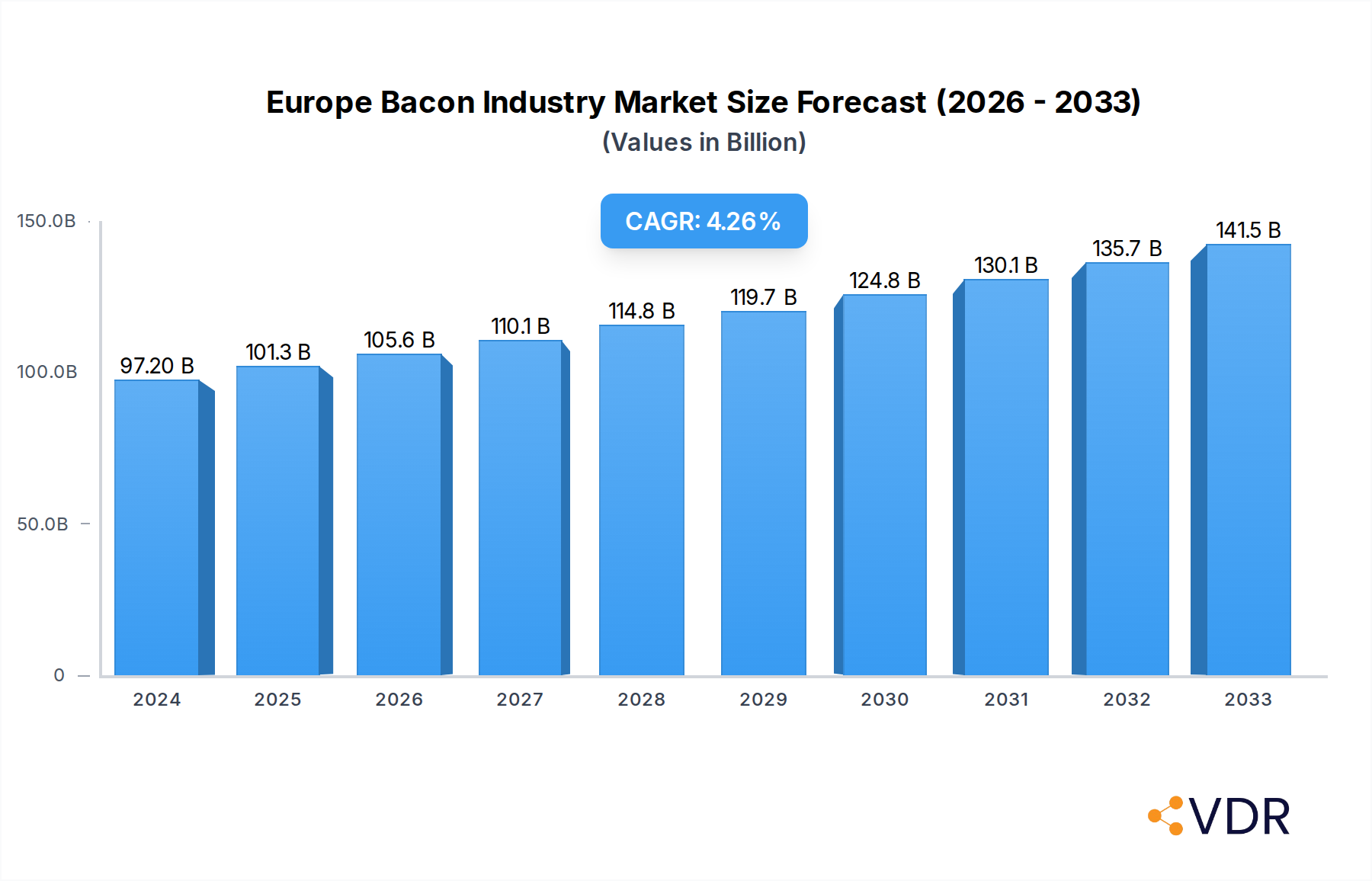

The European bacon market is poised for significant expansion, currently valued at an estimated 97.2 billion Euros in 2024. Projections indicate a CAGR of 4.2% over the forecast period of 2025-2033, suggesting sustained growth driven by evolving consumer preferences and robust market dynamics. The market is segmented into Standard Bacon and Ready-to-eat Bacon, with the latter likely experiencing faster growth due to increasing demand for convenience. Distribution channels are dominated by the Retail Channel, encompassing supermarkets, hypermarkets, specialty stores, and burgeoning online platforms. The Food Service Channel also plays a crucial role, catering to restaurants, cafes, and catering services. Key players such as WH Group Limited, JBS SA (TULIP Ltd), and OSI Group (Gelderland) are actively shaping the market landscape through innovation and strategic expansion. The drivers for this growth are multifaceted, including a rising disposable income across European nations, a growing appetite for protein-rich food items, and the increasing adoption of convenient food solutions.

Europe Bacon Industry Market Size (In Billion)

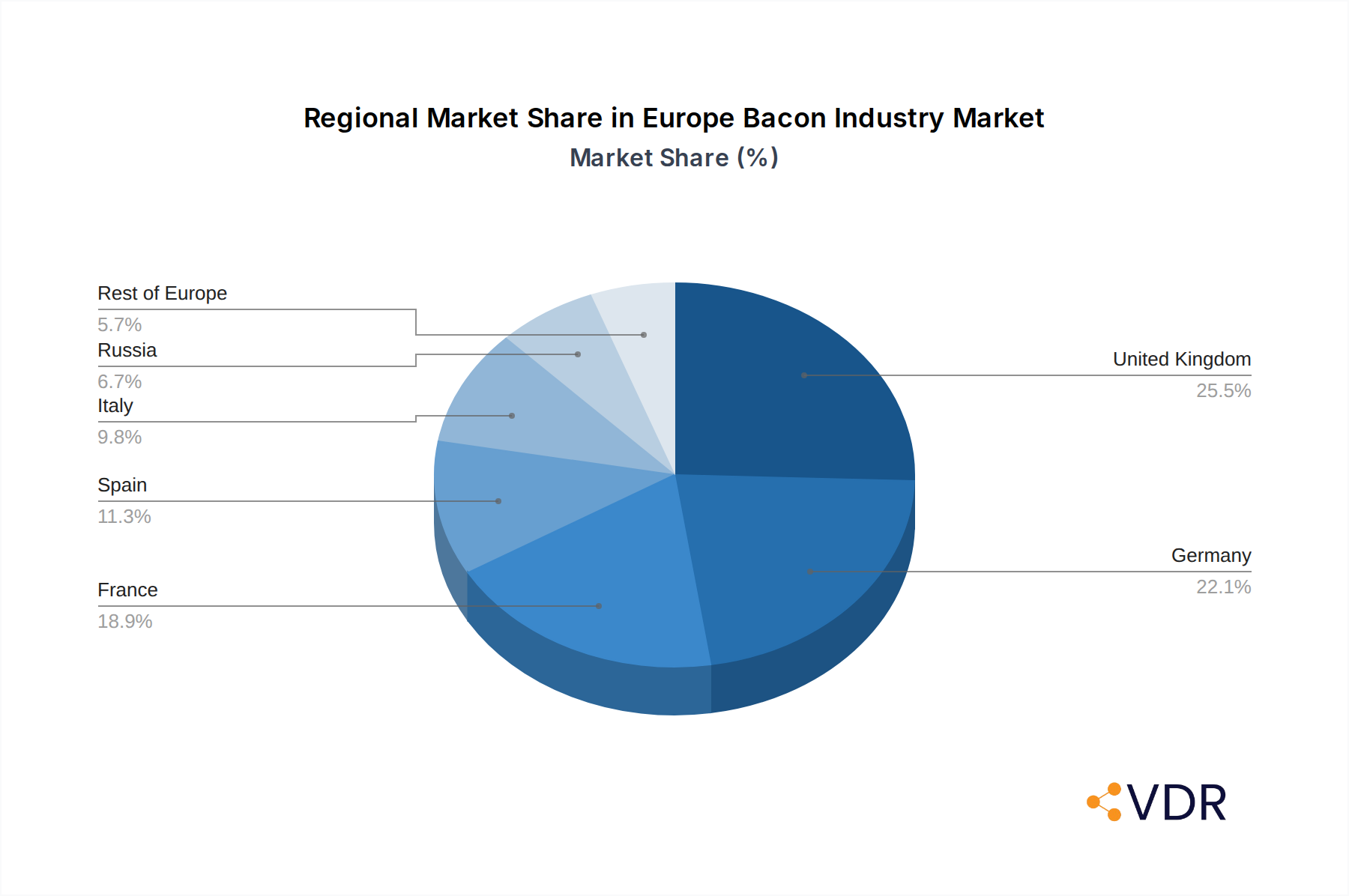

The competitive environment is characterized by a blend of established large corporations and agile artisanal producers. Trends indicate a strong push towards premiumization, with consumers increasingly seeking ethically sourced, high-quality bacon with unique flavor profiles. This is likely to fuel the growth of specialty stores and direct-to-consumer online sales. Conversely, restraints such as fluctuating raw material costs, particularly pork prices, and increasing health consciousness among a segment of the population, which may limit red meat consumption, could pose challenges. However, the overall market sentiment remains positive, with continued innovation in product development, such as reduced-fat or alternative protein bacon, expected to mitigate these concerns. Europe, with its diverse culinary traditions and high purchasing power, presents a fertile ground for bacon manufacturers, with the United Kingdom, Germany, and France expected to lead in market consumption.

Europe Bacon Industry Company Market Share

Europe Bacon Industry Market Dynamics & Structure

The European bacon market is characterized by a moderate to high market concentration, with a few prominent players like LT Brookes Ltd, OSI Group (Gelderland), Finnebrogue Artisan, WH Group Limited, Wiltshire Bacon Co, Maple Leaf Foods INC, JBS SA (TULIP Ltd), and Stirchley Bacon holding significant market shares. Technological innovation is a key driver, particularly in areas such as improved curing processes, enhanced shelf-life technologies, and the development of premium, artisanal bacon products. Regulatory frameworks, including food safety standards and labeling requirements (e.g., origin, ethical sourcing), play a crucial role in shaping product development and market entry.

- Market Concentration: Dominated by a few large corporations, but with a growing segment for specialized producers.

- Technological Innovation: Focus on sustainable sourcing, reduced processing, and flavor enhancement.

- Regulatory Frameworks: Stringent EU food safety regulations and evolving animal welfare standards influence production.

- Competitive Product Substitutes: While bacon holds a strong cultural appeal, plant-based alternatives and other processed meats present a competitive threat.

- End-User Demographics: Increasingly health-conscious consumers are seeking leaner, nitrate-free, and sustainably sourced options.

- M&A Trends: Consolidation within the industry is observed as larger players seek to expand their product portfolios and market reach. For example, WH Group Limited's acquisitions have significantly bolstered its global presence in the processed meat sector.

Europe Bacon Industry Growth Trends & Insights

The Europe bacon industry is poised for robust growth, projected to expand significantly from its current valuation. This expansion is driven by a confluence of factors including evolving consumer preferences, technological advancements in production, and strategic market penetration across various distribution channels. The market size is estimated to have reached approximately XX billion Euros in 2024 and is anticipated to ascend to XX billion Euros by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of XX% during the forecast period of 2025–2033. The base year of 2025 showcases a dynamic market environment, with a projected value of XX billion Euros. Historical data from 2019–2024 reveals a steady upward trajectory, underscoring the enduring appeal of bacon in European diets.

Consumer behavior is a pivotal element in this growth narrative. There's a discernible shift towards premiumization, with consumers willing to pay more for higher-quality, ethically sourced, and artisanal bacon products. This trend is particularly evident in the Ready-to-eat Bacon segment, which is experiencing accelerated adoption rates due to its convenience and perceived superior taste. Technological disruptions are also playing a vital role, with innovations in curing, smoking, and packaging extending shelf life and enhancing flavor profiles. For instance, advancements in reduced-nitrite curing methods are meeting the growing demand for healthier options.

The Retail Channel remains the dominant distribution segment, accounting for a substantial market share. Within this channel, Supermarkets/Hypermarkets are the primary point of sale, followed by the growing influence of Online Stores, which offer convenience and a wider product selection. The Food Service Channel also contributes significantly, with restaurants and catering services incorporating bacon into a diverse range of dishes, from traditional breakfasts to innovative culinary creations. Market penetration is deepening across all segments, indicating a sustained demand for bacon products. The overall outlook suggests a dynamic and evolving market, where innovation, consumer-centricity, and strategic distribution will be key to capturing future growth opportunities.

Dominant Regions, Countries, or Segments in Europe Bacon Industry

The Retail Channel, specifically Supermarkets/Hypermarkets, stands out as the dominant segment driving growth within the European bacon industry. This dominance is underpinned by extensive reach, widespread consumer accessibility, and the ability to cater to diverse dietary preferences and budget constraints. With an estimated market share of XX% in 2025, this channel significantly outpaces others, making it a critical focal point for manufacturers and distributors.

Supermarkets/Hypermarkets: This sub-segment is the bedrock of bacon sales, benefiting from high foot traffic, prime shelf space, and continuous promotional activities. Their extensive product variety, encompassing standard and premium options, caters to a broad consumer base. Economic policies supporting consumer spending and the availability of well-developed retail infrastructure in key European nations like Germany, the UK, and France further amplify their influence.

Food Service Channel: While a significant contributor, this segment, including restaurants, hotels, and catering services, experiences more cyclical demand patterns influenced by tourism and dining trends. Its market share is estimated at XX% in 2025. Nonetheless, its role in product trial and popularizing novel bacon applications is invaluable.

Online Stores: Exhibiting the fastest growth trajectory, online retail is rapidly gaining traction. Its market share, estimated at XX% in 2025, is projected to surge in the coming years. This growth is fueled by increasing internet penetration, the convenience of home delivery, and the ability of online platforms to offer niche and specialized bacon products, including those from Finnebrogue Artisan known for its innovative offerings.

Standard Bacon vs. Ready-to-eat Bacon: Within Product Type, Standard Bacon continues to hold the largest market share, estimated at XX%, due to its widespread use in traditional cooking. However, Ready-to-eat Bacon is a significant growth driver, projected to capture XX% of the market by 2025, appealing to consumers seeking convenience and quicker meal preparation solutions.

The dominance of the Retail Channel, particularly Supermarkets/Hypermarkets, is further reinforced by demographic trends. Aging populations in some European countries and a growing demand for convenient meal solutions among younger demographics collectively boost the sales of readily available bacon products. Furthermore, ongoing investments in cold chain logistics and supply chain efficiency by major players like WH Group Limited and JBS SA (TULIP Ltd) ensure consistent product availability and quality across these retail outlets, solidifying their leading position in the market.

Europe Bacon Industry Product Landscape

The European bacon industry is witnessing a surge in product innovation focused on consumer health, ethical sourcing, and enhanced taste experiences. Beyond traditional cured and smoked varieties, manufacturers are introducing Ready-to-eat Bacon formats, including pre-cooked strips and crumbles, catering to the growing demand for convenience. This innovation extends to cleaner labels, with a significant focus on nitrate-free and organic bacon options, appealing to health-conscious consumers. Companies are also exploring unique curing methods and flavor infusions, such as artisanal smokehouse techniques and the incorporation of herbs and spices, to create premium offerings. Finnebrogue Artisan, for instance, is a prime example of a company pushing boundaries with its distinctive flavor profiles and commitment to animal welfare. The performance metrics for these innovative products are reflected in their premium pricing and growing market acceptance, indicating a positive reception to these advancements and unique selling propositions.

Key Drivers, Barriers & Challenges in Europe Bacon Industry

Key Drivers:

- Evolving Consumer Preferences: A growing demand for premium, artisanal, and ethically sourced bacon products is propelling market growth. Health-conscious consumers are increasingly seeking options with cleaner labels, such as nitrate-free and organic bacon.

- Convenience and Ready-to-eat Products: The rising demand for convenient food options is boosting the adoption of ready-to-eat bacon formats, appealing to busy lifestyles.

- Culinary Versatility: Bacon's enduring popularity as a versatile ingredient in various cuisines, from breakfast to fine dining, ensures sustained demand.

- Technological Advancements: Innovations in curing, smoking, and packaging technologies are enhancing product quality, shelf life, and safety, thereby driving market expansion.

Barriers & Challenges:

- Supply Chain Disruptions: Volatility in raw material prices (pork) and potential disruptions in the supply chain, due to factors like disease outbreaks or geopolitical events, pose significant challenges.

- Regulatory Hurdles: Stringent food safety regulations, animal welfare standards, and labeling requirements across different European countries can impact production costs and market entry.

- Competition from Alternatives: The growing popularity of plant-based protein alternatives and other processed meats presents a competitive threat to traditional bacon products.

- Health Concerns: Ongoing public health discussions and concerns regarding the consumption of processed meats, particularly in relation to nitrites and salt content, can influence consumer purchasing decisions.

Emerging Opportunities in Europe Bacon Industry

Emerging opportunities in the Europe bacon industry lie in the expansion of the Ready-to-eat Bacon segment, driven by increasing consumer demand for convenience and on-the-go meal solutions. The development of plant-based bacon alternatives that closely mimic the taste and texture of traditional bacon presents a significant untapped market, catering to a growing vegan and vegetarian population. Furthermore, focusing on sustainable and ethical sourcing practices, coupled with transparent labeling, can unlock premium market segments and enhance brand loyalty. The growing popularity of specialty and artisanal bacon products, with unique flavor profiles and premium ingredients, also offers a niche but lucrative avenue for growth. Online retail channels are also presenting an opportunity to reach a wider, more diverse consumer base with specialized offerings.

Growth Accelerators in the Europe Bacon Industry Industry

Several growth accelerators are poised to propel the Europe bacon industry forward. Technological breakthroughs in sustainable farming and pork production are crucial for ensuring a stable and ethically sourced supply chain, a key factor for increasingly conscious consumers. Strategic partnerships between producers and retailers will be instrumental in expanding market reach and introducing innovative product lines, particularly in the Ready-to-eat Bacon category. Furthermore, targeted marketing campaigns highlighting the quality, versatility, and evolving health benefits of modern bacon products can help to counter negative perceptions and boost consumer confidence. Investments in cold chain logistics and e-commerce platforms will also accelerate growth by improving accessibility and convenience for consumers across Europe.

Key Players Shaping the Europe Bacon Industry Market

- LT Brookes Ltd

- OSI Group (Gelderland)

- Finnebrogue Artisan

- WH Group Limited

- Wiltshire Bacon Co

- Maple Leaf Foods INC

- JBS SA (TULIP Ltd)

- Stirchley Bacon

Notable Milestones in Europe Bacon Industry Sector

- 2019: Increased consumer focus on health and wellness leads to a rise in demand for "clean label" bacon products with reduced nitrites.

- 2020: The COVID-19 pandemic impacts supply chains and consumer purchasing habits, with a surge in retail sales of processed meats, including bacon, for home consumption.

- 2021: Growing consumer interest in plant-based alternatives prompts some traditional bacon producers to explore or invest in their own plant-based product lines.

- 2022: Enhanced regulations regarding animal welfare and sustainable farming practices begin to influence production methods and sourcing strategies across the industry.

- 2023: Innovations in packaging and preservation technologies lead to the wider availability of extended shelf-life and ready-to-eat bacon products, boosting convenience.

- 2024: Significant mergers and acquisitions activity observed as larger players aim to consolidate market share and diversify their product portfolios.

In-Depth Europe Bacon Industry Market Outlook

The future outlook for the Europe bacon industry is characterized by sustained growth, driven by a dynamic interplay of consumer demand for convenience, premiumization, and ethical sourcing. The continued evolution of the Ready-to-eat Bacon segment, coupled with the burgeoning potential of plant-based alternatives, will shape product innovation and market strategies. Strategic investments in sustainable production methods, advanced processing technologies, and robust e-commerce infrastructure will be pivotal in capitalizing on these evolving trends. Market players who can effectively address consumer concerns regarding health and sustainability while delivering superior quality and convenience are best positioned for long-term success in this vibrant and evolving industry.

Europe Bacon Industry Segmentation

-

1. Product Type

- 1.1. Standard Bacon

- 1.2. Ready-to-eat Bacon

-

2. Distribution Channel

- 2.1. Food Service Channel

-

2.2. Retail Channel

- 2.2.1. Supermarket/Hypermarket

- 2.2.2. Specialty Stores

- 2.2.3. Online Stores

- 2.2.4. Other Distribution Channels

Europe Bacon Industry Segmentation By Geography

- 1. Spain

- 2. Germany

- 3. United Kingdom

- 4. France

- 5. Italy

- 6. Russia

- 7. Rest of Europe

Europe Bacon Industry Regional Market Share

Geographic Coverage of Europe Bacon Industry

Europe Bacon Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Standard Bacon

- 5.1.2. Ready-to-eat Bacon

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Food Service Channel

- 5.2.2. Retail Channel

- 5.2.2.1. Supermarket/Hypermarket

- 5.2.2.2. Specialty Stores

- 5.2.2.3. Online Stores

- 5.2.2.4. Other Distribution Channels

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Spain

- 5.3.2. Germany

- 5.3.3. United Kingdom

- 5.3.4. France

- 5.3.5. Italy

- 5.3.6. Russia

- 5.3.7. Rest of Europe

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. Europe Bacon Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Standard Bacon

- 6.1.2. Ready-to-eat Bacon

- 6.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.2.1. Food Service Channel

- 6.2.2. Retail Channel

- 6.2.2.1. Supermarket/Hypermarket

- 6.2.2.2. Specialty Stores

- 6.2.2.3. Online Stores

- 6.2.2.4. Other Distribution Channels

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. Spain Europe Bacon Industry Analysis, Insights and Forecast, 2021-2033

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 7.1.1. Standard Bacon

- 7.1.2. Ready-to-eat Bacon

- 7.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 7.2.1. Food Service Channel

- 7.2.2. Retail Channel

- 7.2.2.1. Supermarket/Hypermarket

- 7.2.2.2. Specialty Stores

- 7.2.2.3. Online Stores

- 7.2.2.4. Other Distribution Channels

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 8. Germany Europe Bacon Industry Analysis, Insights and Forecast, 2021-2033

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 8.1.1. Standard Bacon

- 8.1.2. Ready-to-eat Bacon

- 8.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 8.2.1. Food Service Channel

- 8.2.2. Retail Channel

- 8.2.2.1. Supermarket/Hypermarket

- 8.2.2.2. Specialty Stores

- 8.2.2.3. Online Stores

- 8.2.2.4. Other Distribution Channels

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 9. United Kingdom Europe Bacon Industry Analysis, Insights and Forecast, 2021-2033

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 9.1.1. Standard Bacon

- 9.1.2. Ready-to-eat Bacon

- 9.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 9.2.1. Food Service Channel

- 9.2.2. Retail Channel

- 9.2.2.1. Supermarket/Hypermarket

- 9.2.2.2. Specialty Stores

- 9.2.2.3. Online Stores

- 9.2.2.4. Other Distribution Channels

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 10. France Europe Bacon Industry Analysis, Insights and Forecast, 2021-2033

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 10.1.1. Standard Bacon

- 10.1.2. Ready-to-eat Bacon

- 10.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 10.2.1. Food Service Channel

- 10.2.2. Retail Channel

- 10.2.2.1. Supermarket/Hypermarket

- 10.2.2.2. Specialty Stores

- 10.2.2.3. Online Stores

- 10.2.2.4. Other Distribution Channels

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 11. Italy Europe Bacon Industry Analysis, Insights and Forecast, 2021-2033

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 11.1.1. Standard Bacon

- 11.1.2. Ready-to-eat Bacon

- 11.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 11.2.1. Food Service Channel

- 11.2.2. Retail Channel

- 11.2.2.1. Supermarket/Hypermarket

- 11.2.2.2. Specialty Stores

- 11.2.2.3. Online Stores

- 11.2.2.4. Other Distribution Channels

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 12. Russia Europe Bacon Industry Analysis, Insights and Forecast, 2021-2033

- 12.1. Market Analysis, Insights and Forecast - by Product Type

- 12.1.1. Standard Bacon

- 12.1.2. Ready-to-eat Bacon

- 12.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 12.2.1. Food Service Channel

- 12.2.2. Retail Channel

- 12.2.2.1. Supermarket/Hypermarket

- 12.2.2.2. Specialty Stores

- 12.2.2.3. Online Stores

- 12.2.2.4. Other Distribution Channels

- 12.1. Market Analysis, Insights and Forecast - by Product Type

- 13. Rest of Europe Europe Bacon Industry Analysis, Insights and Forecast, 2021-2033

- 13.1. Market Analysis, Insights and Forecast - by Product Type

- 13.1.1. Standard Bacon

- 13.1.2. Ready-to-eat Bacon

- 13.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 13.2.1. Food Service Channel

- 13.2.2. Retail Channel

- 13.2.2.1. Supermarket/Hypermarket

- 13.2.2.2. Specialty Stores

- 13.2.2.3. Online Stores

- 13.2.2.4. Other Distribution Channels

- 13.1. Market Analysis, Insights and Forecast - by Product Type

- 14. Competitive Analysis

- 14.1. Company Profiles

- 14.1.1 LT Brookes Ltd

- 14.1.1.1. Company Overview

- 14.1.1.2. Products

- 14.1.1.3. Company Financials

- 14.1.1.4. SWOT Analysis

- 14.1.2 OSI Group (Gelderland)

- 14.1.2.1. Company Overview

- 14.1.2.2. Products

- 14.1.2.3. Company Financials

- 14.1.2.4. SWOT Analysis

- 14.1.3 Finnebrogue Artisan

- 14.1.3.1. Company Overview

- 14.1.3.2. Products

- 14.1.3.3. Company Financials

- 14.1.3.4. SWOT Analysis

- 14.1.4 WH Group Limited

- 14.1.4.1. Company Overview

- 14.1.4.2. Products

- 14.1.4.3. Company Financials

- 14.1.4.4. SWOT Analysis

- 14.1.5 Wiltshire Bacon Co*List Not Exhaustive

- 14.1.5.1. Company Overview

- 14.1.5.2. Products

- 14.1.5.3. Company Financials

- 14.1.5.4. SWOT Analysis

- 14.1.6 Maple Leaf Foods INC

- 14.1.6.1. Company Overview

- 14.1.6.2. Products

- 14.1.6.3. Company Financials

- 14.1.6.4. SWOT Analysis

- 14.1.7 JBS SA (TULIP Ltd)

- 14.1.7.1. Company Overview

- 14.1.7.2. Products

- 14.1.7.3. Company Financials

- 14.1.7.4. SWOT Analysis

- 14.1.8 Stirchley Bacon

- 14.1.8.1. Company Overview

- 14.1.8.2. Products

- 14.1.8.3. Company Financials

- 14.1.8.4. SWOT Analysis

- 14.1.1 LT Brookes Ltd

- 14.2. Market Entropy

- 14.2.1 Company's Key Areas Served

- 14.2.2 Recent Developments

- 14.3. Company Market Share Analysis 2025

- 14.3.1 Top 5 Companies Market Share Analysis

- 14.3.2 Top 3 Companies Market Share Analysis

- 14.4. List of Potential Customers

- 15. Research Methodology

List of Figures

- Figure 1: Europe Bacon Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Europe Bacon Industry Share (%) by Company 2025

List of Tables

- Table 1: Europe Bacon Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 2: Europe Bacon Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 3: Europe Bacon Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Europe Bacon Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 5: Europe Bacon Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 6: Europe Bacon Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: Europe Bacon Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 8: Europe Bacon Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 9: Europe Bacon Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 10: Europe Bacon Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 11: Europe Bacon Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 12: Europe Bacon Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Europe Bacon Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 14: Europe Bacon Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 15: Europe Bacon Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 16: Europe Bacon Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 17: Europe Bacon Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 18: Europe Bacon Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 19: Europe Bacon Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 20: Europe Bacon Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 21: Europe Bacon Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 22: Europe Bacon Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 23: Europe Bacon Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 24: Europe Bacon Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Bacon Industry?

The projected CAGR is approximately 4.2%.

2. Which companies are prominent players in the Europe Bacon Industry?

Key companies in the market include LT Brookes Ltd, OSI Group (Gelderland), Finnebrogue Artisan, WH Group Limited, Wiltshire Bacon Co*List Not Exhaustive, Maple Leaf Foods INC, JBS SA (TULIP Ltd), Stirchley Bacon.

3. What are the main segments of the Europe Bacon Industry?

The market segments include Product Type, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 97.2 billion as of 2022.

5. What are some drivers contributing to market growth?

Popularization of Adventure Sports and Expedition; Suitability of the Freeze-Dried Technique for Heat Sensitive Food Products.

6. What are the notable trends driving market growth?

Increasing Per Capita Consumption of Pork.

7. Are there any restraints impacting market growth?

High Cost Associated with the Freeze-Drying Technology.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Bacon Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Bacon Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Bacon Industry?

To stay informed about further developments, trends, and reports in the Europe Bacon Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence