Key Insights

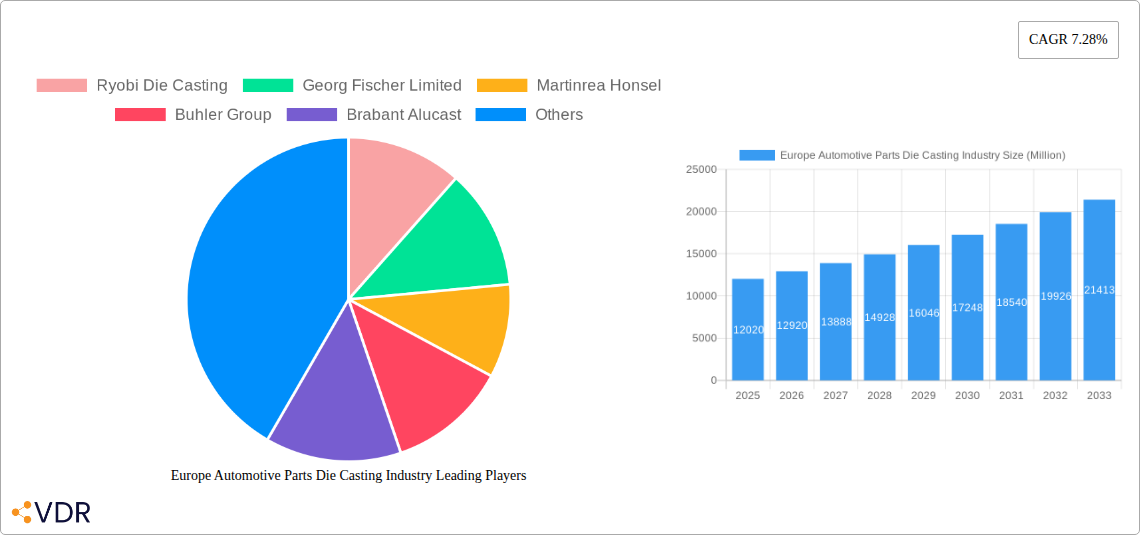

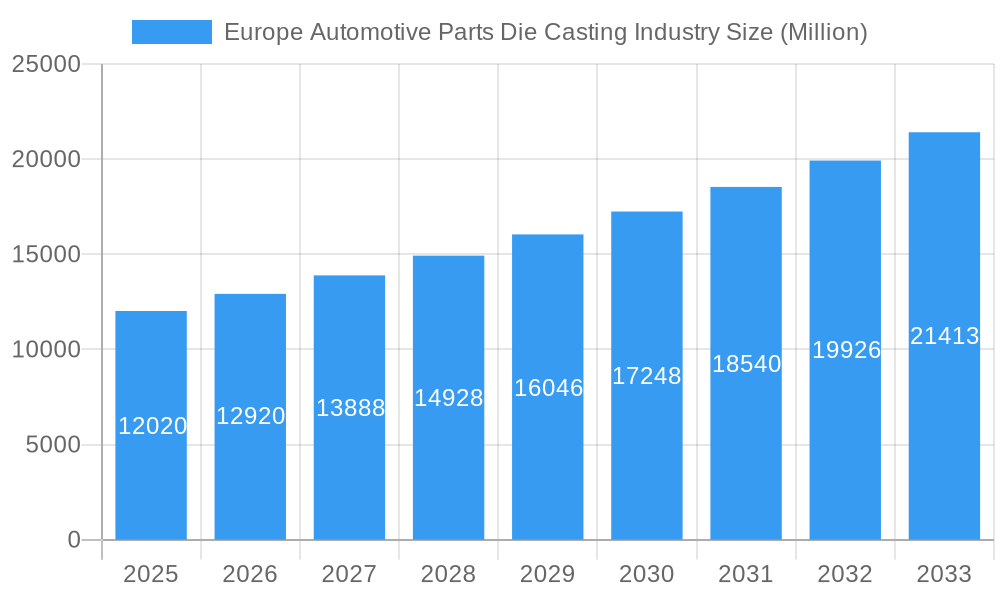

The European automotive parts die casting market, valued at €12.02 billion in 2025, is projected to experience robust growth, driven by the increasing demand for lightweight vehicles and the rising adoption of electric vehicles (EVs). The market's Compound Annual Growth Rate (CAGR) of 7.28% from 2025 to 2033 indicates a significant expansion over the forecast period. Key drivers include stringent fuel efficiency regulations pushing automakers towards lighter vehicle designs, where die casting plays a crucial role. Furthermore, the increasing complexity of automotive components and the need for high-precision parts further fuel market expansion. Aluminum die casting dominates the metal type segment, owing to its lightweight and high-strength properties, making it ideal for engine parts, transmission components, and structural parts. The vacuum die casting process is gaining traction due to its ability to produce high-quality castings with intricate designs. Major players like Ryobi Die Casting, Georg Fischer Limited, and Nemak are investing heavily in advanced technologies and expanding their production capacities to meet the growing demand. The market is segmented by production process (vacuum, pressure, and other), metal type (aluminum, zinc, and other), and application (engine parts, transmission, structural, and others). Germany, France, and the UK are the leading markets within Europe, reflecting the concentration of automotive manufacturing in these regions. However, growth is expected across other European countries as the automotive industry continues to evolve.

Europe Automotive Parts Die Casting Industry Market Size (In Billion)

The competitive landscape is characterized by both established multinational corporations and specialized regional players. Consolidation and strategic partnerships are likely to occur as companies strive for greater market share and technological advancements. While the market faces challenges like fluctuating raw material prices and the need for skilled labor, the long-term outlook remains positive, driven by the ongoing trends in automotive technology and the increasing demand for high-performance, lightweight automotive components. The continued adoption of innovative die casting techniques, alongside sustainable manufacturing practices, will play a crucial role in shaping the market's future trajectory. This growth is further supported by governmental initiatives promoting sustainable transportation and the overall strengthening of the European automotive sector in the years to come.

Europe Automotive Parts Die Casting Industry Company Market Share

Europe Automotive Parts Die Casting Industry Market Report: 2019-2033

This comprehensive report provides a detailed analysis of the European automotive parts die casting market, encompassing market dynamics, growth trends, regional performance, key players, and future outlook. With a focus on the parent market (Automotive Parts) and child market (Die Casting), this report is invaluable for industry professionals, investors, and strategic decision-makers. The study period covers 2019-2033, with 2025 as the base and estimated year.

Study Period: 2019–2033 Base Year: 2025 Estimated Year: 2025 Forecast Period: 2025–2033 Historical Period: 2019–2024

Europe Automotive Parts Die Casting Industry Market Dynamics & Structure

The European automotive parts die casting market is a dynamic and evolving landscape, characterized by a moderate level of concentration with established key players holding substantial market shares. The industry is propelled by relentless technological innovation, with a significant emphasis on the development and application of lightweight materials like advanced aluminum and magnesium alloys, alongside the widespread integration of automation and intelligent manufacturing processes. Simultaneously, increasingly stringent regulatory frameworks, particularly those focused on reducing emissions and enhancing vehicle safety, are fundamentally shaping material choices and production methodologies. While competitive pressure from alternative manufacturing processes, such as forging and advanced machining, certainly exists, die casting maintains a robust and advantageous position due to its inherent cost-effectiveness and exceptional versatility, particularly for high-volume production runs of complex components. The primary end-user demographic remains predominantly the automotive Original Equipment Manufacturers (OEMs) and Tier 1 suppliers. Mergers and acquisitions (M&A) activity has been observed as moderate in recent years, often driven by strategic consolidation to achieve economies of scale, enhance technological capabilities, and expand market reach. Estimated deal values in the past five years reflect this ongoing strategic realignment.

- Market Concentration: Moderately concentrated, with the top 5 players commanding a significant market share, estimated at approximately xx%.

- Technological Innovation: The industry is actively pursuing innovations in lightweighting through advanced Aluminum and Magnesium alloys, driving automation adoption, and optimizing die casting processes for enhanced efficiency and precision.

- Regulatory Framework: Stringent emission standards and evolving safety regulations are a key influence, driving demand for specific materials and production methods that align with environmental and safety goals.

- Competitive Substitutes: While forging, precision machining, and advanced plastic injection molding present ongoing competitive pressures, die casting's advantages in volume and cost remain formidable.

- End-User Demographics: The market is predominantly served by automotive OEMs and Tier 1 suppliers, catering to both passenger vehicle and commercial vehicle segments.

- M&A Trends: Moderate M&A activity has been observed, driven by strategic expansion, technological integration, and consolidation efforts, with an estimated deal value in the range of xx million units between 2019 and 2024.

Europe Automotive Parts Die Casting Industry Growth Trends & Insights

The European automotive parts die casting market experienced a xx% CAGR from 2019 to 2024, reaching an estimated market size of xx million units in 2024. This growth is attributed to the increasing demand for vehicles, particularly in key markets within Europe. However, the market faced challenges due to supply chain disruptions and fluctuating raw material prices in the period 2020-2022. Looking forward, the market is projected to experience a xx% CAGR from 2025 to 2033, driven by the increasing adoption of electric vehicles (EVs) and the consequent demand for lightweight and efficient components. Technological advancements, such as the use of AI in optimizing casting processes and the development of new alloys, further contribute to growth. Consumer preferences towards fuel-efficient and technologically advanced vehicles also play a significant role.

Dominant Regions, Countries, or Segments in Europe Automotive Parts Die Casting Industry

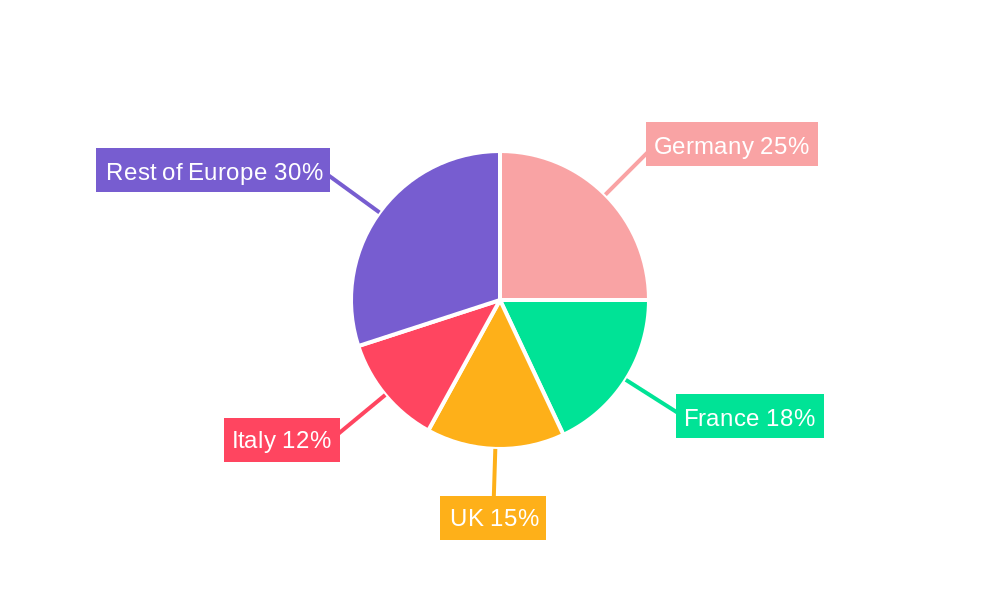

Geographically, Germany, France, and Italy stand out as the leading hubs for the European automotive parts die casting market. This dominance is largely attributed to their substantial automotive manufacturing bases, well-developed supplier networks, and robust supporting industrial infrastructure. Within the different production process types, pressure die casting commands the largest market share, a position secured by its exceptional production efficiency and suitability for high-volume, mass-produced components. Aluminum alloys consistently emerge as the dominant metal type due to their advantageous lightweight properties and excellent casting characteristics, crucial for meeting modern automotive demands. Key application segments driving demand include engine parts and transmission components, which collectively represent a significant portion of the market. The continued evolution of electric vehicles is also spurring growth in demand for structural components and other specialized parts.

- By Production Process Type: Pressure Die Casting is the leading segment, estimated to account for xx million units in 2024, followed by Vacuum Die Casting (xx million units in 2024) and other specialized production processes (xx million units in 2024).

- By Metal Type: Aluminum alloys remain the dominant metal, projected at xx million units in 2024, followed by Zinc alloys (xx million units in 2024) and a range of other specialized metal types (xx million units in 2024).

- By Application Type: Engine Parts are a major application, with an estimated demand of xx million units in 2024, alongside Transmission Components at xx million units. Structural Parts are also a significant and growing segment (xx million units in 2024), with other application types showing considerable growth potential (xx million units in 2024).

- Key Drivers: The strong presence of the automotive industry in Germany, France, and Italy, coupled with government incentives for electric vehicle adoption and ongoing technological advancements in die casting processes, are significant market drivers.

Europe Automotive Parts Die Casting Industry Product Landscape

The product landscape within the Europe Automotive Parts Die Casting Industry is characterized by a relentless pursuit of innovation across materials, manufacturing processes, and component design. A primary focus is on the increased utilization of lightweight alloys, predominantly aluminum and its advanced variants, alongside magnesium alloys. This strategic shift is driven by the imperative to enhance vehicle fuel efficiency and reduce overall weight. Advanced die casting processes, such as high-pressure die casting (HPDC) and increasingly, low-pressure die casting (LPDC) for specific applications, are employed to achieve superior dimensional accuracy, exceptional surface finish, and intricate geometries in components. The overarching trend is towards the production of high-strength, lightweight parts that not only meet but exceed the stringent performance requirements of modern vehicles, especially those in the burgeoning electric vehicle (EV) segment. Unique selling propositions (USPs) for manufacturers often revolve around demonstrably improved process efficiency, higher component precision and repeatability, and ultimately, reduced material costs and waste, contributing to a more sustainable manufacturing ecosystem.

Key Drivers, Barriers & Challenges in Europe Automotive Parts Die Casting Industry

Key Drivers:

- Sustained and growing demand for new vehicles across the European continent.

- The accelerating adoption of lightweight materials in automotive design to meet fuel economy and performance targets.

- Continuous technological advancements in die casting processes, including increased automation, the integration of Artificial Intelligence (AI) for process optimization, and the development of novel tooling solutions.

- Supportive government policies and initiatives aimed at bolstering the automotive industry and promoting technological innovation.

Challenges and Restraints:

- Volatility in raw material prices, particularly for key metals like Aluminum and Zinc, which can impact production costs and profitability.

- Disruptions in global supply chains and ongoing logistical challenges, affecting the timely procurement of raw materials and delivery of finished components.

- Increasingly stringent environmental regulations related to emissions from foundries and waste disposal practices, requiring significant investment in cleaner technologies.

- Intense and persistent competition from alternative manufacturing technologies that may offer perceived advantages in specific applications or cost structures.

Emerging Opportunities in Europe Automotive Parts Die Casting Industry

- Growth of the electric vehicle (EV) market and the demand for lightweight components.

- Increased adoption of advanced driver-assistance systems (ADAS) and the need for precise, high-performance parts.

- Development of innovative die casting alloys with improved properties (e.g., strength, corrosion resistance).

- Expansion into niche markets, such as the aerospace and renewable energy sectors.

Growth Accelerators in the Europe Automotive Parts Die Casting Industry

Long-term growth for the Europe Automotive Parts Die Casting Industry will be significantly fueled by a confluence of factors. Continued and accelerated technological advancements, encompassing areas such as smart manufacturing, Industry 4.0 integration, and advanced simulation tools, will enhance efficiency and capability. Strategic partnerships and closer collaborations between die casters and automotive OEMs are crucial for co-developing innovative solutions and ensuring alignment with future vehicle architectures. Expansion into new or emerging markets, both geographically and in terms of novel applications, will also be a key growth driver. The unwavering focus on lightweighting, driven by both regulatory pressures and consumer demand for more efficient vehicles, will continue to propel the market. Furthermore, the global imperative for sustainability in manufacturing will encourage the adoption of more environmentally friendly die casting processes and materials. Crucially, government regulations and incentives that actively promote the widespread adoption of electric vehicles will create substantial and sustained demand for high-quality, lightweight, and precisely engineered die-cast components.

Key Players Shaping the Europe Automotive Parts Die Casting Industry Market

- Ryobi Die Casting

- Georg Fischer Limited

- Martinrea Honsel

- Buhler Group

- Brabant Alucast

- DGS Druckguss Systeme

- Nemak

- Dynacast

- Rheinmetall Automotive

Notable Milestones in Europe Automotive Parts Die Casting Industry Sector

- September 2022: Rheinmetall AG secured a EUR 20 million (USD 23.6 million) order for its Turbo Bypass Valve (TBV) Gen 6, highlighting the demand for advanced engine components.

- May 2022: GF Casting Solutions committed to enhancing EV product development, emphasizing the industry's shift towards electric mobility.

In-Depth Europe Automotive Parts Die Casting Industry Market Outlook

The European automotive parts die casting market is poised for significant growth over the next decade, driven by the increasing demand for lightweight and high-performance components in the automotive industry, particularly for electric vehicles. Strategic partnerships, technological innovation, and expansion into new markets will shape the future landscape. The market's growth will depend on navigating challenges like raw material price volatility and maintaining a competitive edge. Opportunities exist in developing sustainable and innovative casting solutions to meet evolving environmental regulations and consumer preferences.

Europe Automotive Parts Die Casting Industry Segmentation

-

1. Production Process Type

- 1.1. Vacuum Die Casting

- 1.2. Pressure Die Casting

- 1.3. Other Production Process Types

-

2. Metal Type

- 2.1. Aluminum

- 2.2. Zinc

- 2.3. Other Metal Types

-

3. Application Type

- 3.1. Engine Parts

- 3.2. Transmission Components

- 3.3. Structural Parts

- 3.4. Other Application Types

Europe Automotive Parts Die Casting Industry Segmentation By Geography

-

1. Europe

- 1.1. Germany

- 1.2. United Kingdom

- 1.3. France

- 1.4. Italy

- 1.5. Russia

- 1.6. Rest of Europe

Europe Automotive Parts Die Casting Industry Regional Market Share

Geographic Coverage of Europe Automotive Parts Die Casting Industry

Europe Automotive Parts Die Casting Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.28% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Production Process Type

- 5.1.1. Vacuum Die Casting

- 5.1.2. Pressure Die Casting

- 5.1.3. Other Production Process Types

- 5.2. Market Analysis, Insights and Forecast - by Metal Type

- 5.2.1. Aluminum

- 5.2.2. Zinc

- 5.2.3. Other Metal Types

- 5.3. Market Analysis, Insights and Forecast - by Application Type

- 5.3.1. Engine Parts

- 5.3.2. Transmission Components

- 5.3.3. Structural Parts

- 5.3.4. Other Application Types

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Production Process Type

- 6. Europe Automotive Parts Die Casting Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Production Process Type

- 6.1.1. Vacuum Die Casting

- 6.1.2. Pressure Die Casting

- 6.1.3. Other Production Process Types

- 6.2. Market Analysis, Insights and Forecast - by Metal Type

- 6.2.1. Aluminum

- 6.2.2. Zinc

- 6.2.3. Other Metal Types

- 6.3. Market Analysis, Insights and Forecast - by Application Type

- 6.3.1. Engine Parts

- 6.3.2. Transmission Components

- 6.3.3. Structural Parts

- 6.3.4. Other Application Types

- 6.1. Market Analysis, Insights and Forecast - by Production Process Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Ryobi Die Casting

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Georg Fischer Limited

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Martinrea Honsel

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Buhler Group

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Brabant Alucast

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 DGS Druckguss Systeme*List Not Exhaustive

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Nemak

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Dynacast

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Rheinmetall Automotive

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.1 Ryobi Die Casting

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Europe Automotive Parts Die Casting Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Europe Automotive Parts Die Casting Industry Share (%) by Company 2025

List of Tables

- Table 1: Europe Automotive Parts Die Casting Industry Revenue Million Forecast, by Production Process Type 2020 & 2033

- Table 2: Europe Automotive Parts Die Casting Industry Revenue Million Forecast, by Metal Type 2020 & 2033

- Table 3: Europe Automotive Parts Die Casting Industry Revenue Million Forecast, by Application Type 2020 & 2033

- Table 4: Europe Automotive Parts Die Casting Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 5: Europe Automotive Parts Die Casting Industry Revenue Million Forecast, by Production Process Type 2020 & 2033

- Table 6: Europe Automotive Parts Die Casting Industry Revenue Million Forecast, by Metal Type 2020 & 2033

- Table 7: Europe Automotive Parts Die Casting Industry Revenue Million Forecast, by Application Type 2020 & 2033

- Table 8: Europe Automotive Parts Die Casting Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 9: Germany Europe Automotive Parts Die Casting Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: United Kingdom Europe Automotive Parts Die Casting Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: France Europe Automotive Parts Die Casting Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: Italy Europe Automotive Parts Die Casting Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 13: Russia Europe Automotive Parts Die Casting Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: Rest of Europe Europe Automotive Parts Die Casting Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Automotive Parts Die Casting Industry?

The projected CAGR is approximately 7.28%.

2. Which companies are prominent players in the Europe Automotive Parts Die Casting Industry?

Key companies in the market include Ryobi Die Casting, Georg Fischer Limited, Martinrea Honsel, Buhler Group, Brabant Alucast, DGS Druckguss Systeme*List Not Exhaustive, Nemak, Dynacast, Rheinmetall Automotive.

3. What are the main segments of the Europe Automotive Parts Die Casting Industry?

The market segments include Production Process Type, Metal Type, Application Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 12.02 Million as of 2022.

5. What are some drivers contributing to market growth?

Growing Use of Aluminum in Die Casting Equipment to Increase Market Demand.

6. What are the notable trends driving market growth?

Increasing Demand from the Commercial Vehicle Segment.

7. Are there any restraints impacting market growth?

Fluctuations in Raw Material Prices.

8. Can you provide examples of recent developments in the market?

September 2022: Rheinmetall AG (Rheinmetall) secured a new EUR 20 million (USD 23.6 million) order for its cutting-edge air-divert valve, the Turbo Bypass Valve (TBV) Gen 6, further solidifying its position as a key player in the industry. This order adds to the series of recent successful orders received by the Group subsidiary. Production of the TBV Gen 6 will be carried out at Pierburg's Neuss, Germany, plant.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Automotive Parts Die Casting Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Automotive Parts Die Casting Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Automotive Parts Die Casting Industry?

To stay informed about further developments, trends, and reports in the Europe Automotive Parts Die Casting Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence