Key Insights

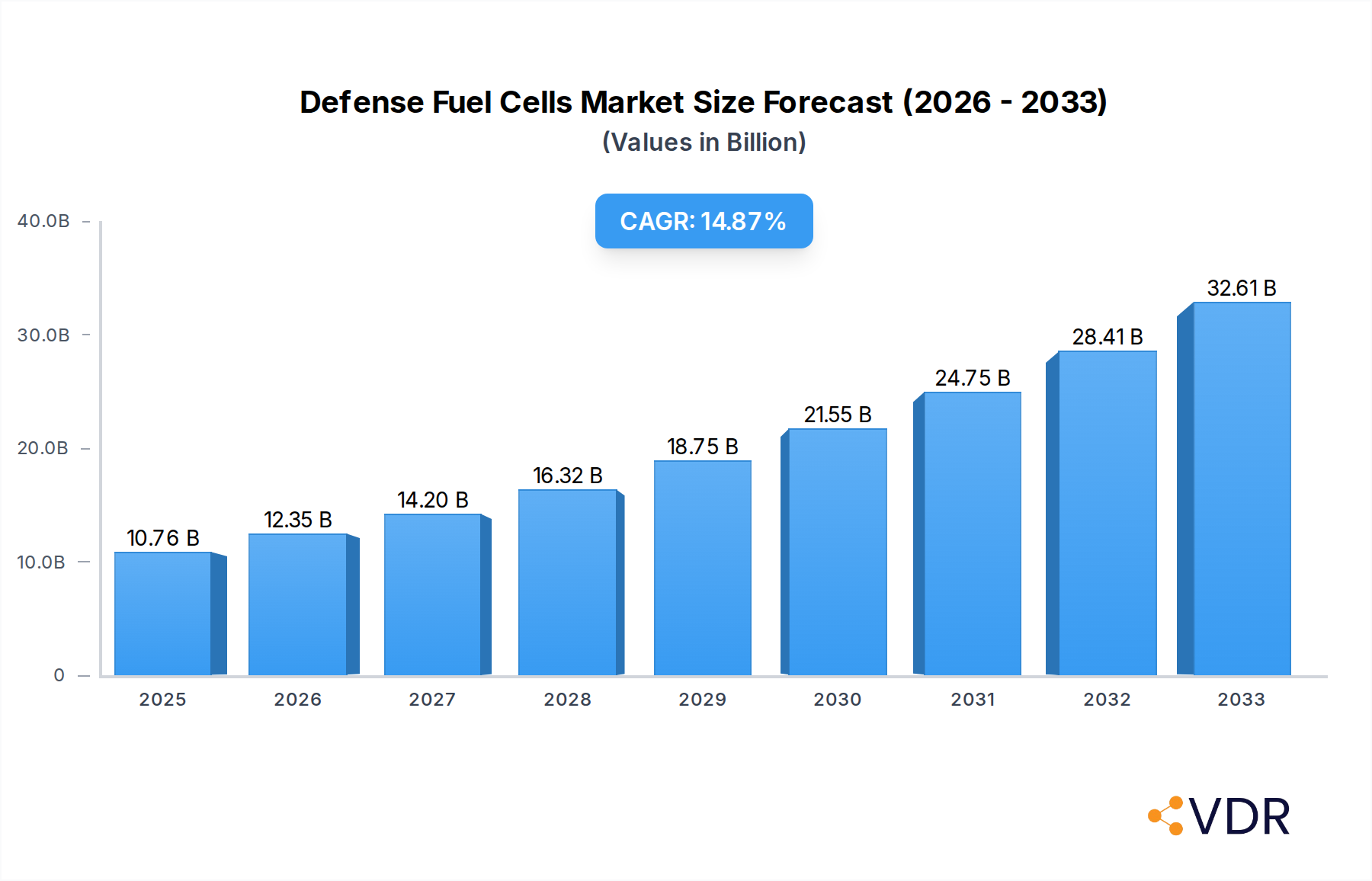

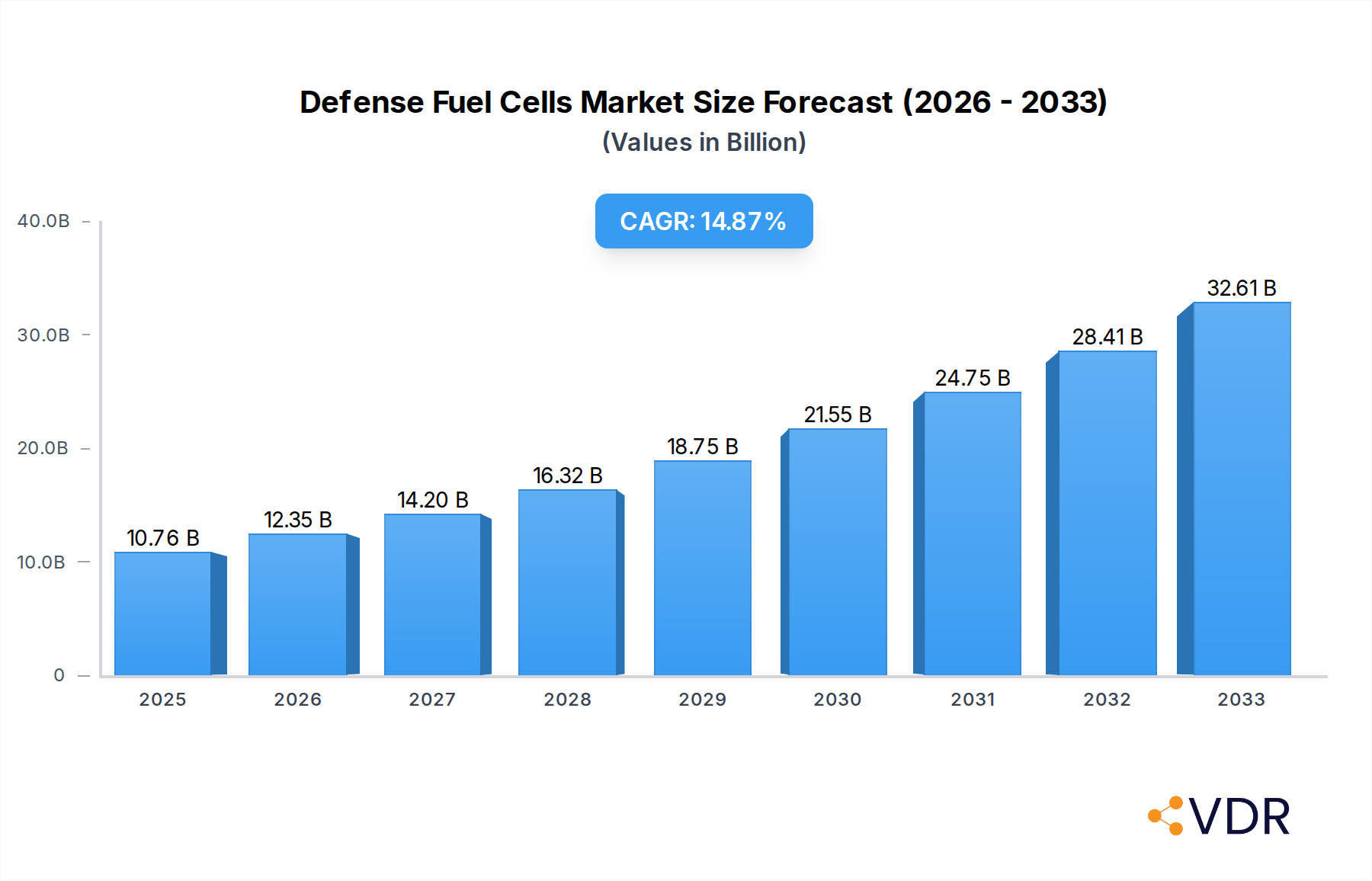

The global Defense Fuel Cells market is poised for significant expansion, projected to reach an estimated USD 10.76 billion by 2025, exhibiting a robust Compound Annual Growth Rate (CAGR) of 14.8% through 2033. This impressive growth trajectory is fueled by an increasing demand for advanced power solutions in defense applications, driven by the need for silent, reliable, and long-endurance power sources for various military operations. Key drivers include the escalating geopolitical tensions and the subsequent modernization of defense infrastructure, necessitating sophisticated portable and stationary power generation systems. The growing emphasis on reducing the logistical burden of traditional fuel supplies, coupled with the inherent advantages of fuel cells such as high energy density and reduced emissions, further propels market adoption. Furthermore, advancements in fuel cell technologies, particularly Proton Exchange Membrane Fuel Cells (PEMFC) and Solid Oxide Fuel Cells (SOFC), are enhancing their performance, efficiency, and durability, making them increasingly viable for demanding defense environments.

Defense Fuel Cells Market Size (In Billion)

The market is segmented by application into Defense and Homeland Security, with the Defense segment likely to dominate due to substantial government investments in military hardware and operational capabilities. Within types, PEMFC technology is expected to lead owing to its versatility, relatively low operating temperature, and fast response times, making it suitable for portable power units and unmanned systems. Trends such as the integration of fuel cells into unmanned aerial vehicles (UAVs), ground vehicles, and tactical power systems are reshaping the landscape. However, the market faces certain restraints, including the high initial cost of fuel cell systems and the limited availability of hydrogen infrastructure in certain regions. Despite these challenges, ongoing research and development efforts, coupled with strategic collaborations between leading companies like Ballard Power, FuelCell Energy, and Bloom Energy, are paving the way for cost reductions and wider deployment, solidifying the positive outlook for the Defense Fuel Cells market.

Defense Fuel Cells Company Market Share

Defense Fuel Cells Market Research Report: Dynamics, Growth, and Outlook 2019–2033

This comprehensive report provides an in-depth analysis of the global defense fuel cells market, offering critical insights into its dynamics, growth trends, key players, and future outlook. Leveraging extensive historical data and robust forecasting methodologies, this report is an essential resource for stakeholders seeking to understand and capitalize on opportunities within this rapidly evolving sector.

Defense Fuel Cells Market Dynamics & Structure

The defense fuel cells market is characterized by a moderate to high concentration, driven by significant investments in advanced military technology and national security. Technological innovation is a paramount driver, with ongoing research and development focused on enhancing power density, durability, and operational efficiency for diverse defense applications. Regulatory frameworks, though evolving, play a crucial role in shaping market access and standardization. Competitive product substitutes, such as advanced battery systems and traditional power generation, pose a persistent challenge, necessitating continuous product differentiation and performance improvement by fuel cell manufacturers. End-user demographics are primarily defense organizations and homeland security agencies, with a growing emphasis on portable, silent, and long-endurance power solutions for remote operations, reconnaissance, and troop support. Mergers and acquisitions (M&A) trends indicate a strategic consolidation among key players aiming to expand their technological portfolios and market reach.

- Market Concentration: Dominated by a few key players with specialized offerings for defense.

- Technological Innovation: Driven by the need for higher energy density, reduced size and weight, and extended operational lifespan.

- Regulatory Frameworks: Influenced by military specifications, safety standards, and government procurement policies.

- Competitive Substitutes: Advanced batteries, portable generators, and other energy storage solutions.

- End-User Demographics: Military branches, special forces, border patrol, and critical infrastructure protection agencies.

- M&A Trends: Strategic acquisitions to gain intellectual property, market access, and integrated solutions.

Defense Fuel Cells Growth Trends & Insights

The defense fuel cells market is poised for substantial growth, projected to expand from $1.5 billion in 2024 to an estimated $5.2 billion by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of approximately 14.8% during the forecast period (2025–2033). This growth is underpinned by increasing global defense expenditures and a strategic shift towards adopting more sustainable and efficient energy solutions. Adoption rates are accelerating as defense forces recognize the tactical advantages offered by fuel cell technology, including silent operation, reduced logistical burden, and extended mission capabilities. Technological disruptions, such as advancements in Solid Oxide Fuel Cells (SOFCs) and Proton Exchange Membrane Fuel Cells (PEMFCs) for higher power outputs and improved efficiency, are further fueling market expansion. Consumer behavior shifts among defense procurement officers are moving towards valuing long-term operational cost savings, environmental benefits, and enhanced soldier safety associated with fuel cell integration. The market penetration of fuel cells in various defense applications, from unmanned aerial vehicles (UAVs) to soldier-portable power systems, is expected to increase significantly. The base year of 2025 provides a crucial snapshot, with estimations for 2025 indicating a market size of $1.7 billion, setting the stage for the robust growth observed throughout the study period. The historical period from 2019–2024 has laid the groundwork for this projected surge, demonstrating a steady increase in research, development, and initial deployments.

Dominant Regions, Countries, or Segments in Defense Fuel Cells

The Proton Exchange Membrane Fuel Cell (PEMFC) segment is currently the dominant force driving growth within the defense fuel cells market, projected to hold a significant market share. Its widespread adoption is attributed to its suitability for a broad range of defense applications requiring compact, lightweight, and efficient power sources, particularly for portable electronics, unmanned systems, and soldier-worn equipment. The Defense application segment, encompassing land, sea, and air forces, represents the primary demand driver, followed closely by the Homeland Security segment, which focuses on border protection, critical infrastructure security, and disaster response.

Several key factors contribute to the dominance of PEMFCs and the broader defense application:

- Technological Maturity and Performance: PEMFCs offer a favorable balance of power density, operating temperature, and response time, making them ideal for the dynamic demands of military operations. Their ability to operate at lower temperatures compared to other fuel cell types enhances their versatility and ease of deployment in various environmental conditions.

- Governmental Investment and Procurement: Major defense-spending nations are heavily investing in the research, development, and procurement of advanced technologies that enhance operational capabilities. Fuel cells are increasingly prioritized for their ability to reduce reliance on fossil fuels, minimize logistical footprints, and provide silent, emissions-free power. For instance, the United States, with its significant defense budget and ongoing modernization efforts, is a leading consumer and innovator in the defense fuel cells sector.

- Growth Potential in Key Segments:

- Application: Defense: This segment is expected to grow at a CAGR of 15.5% from 2025 to 2033, driven by the need for silent, persistent power for reconnaissance drones, communication equipment, and vehicle power systems.

- Types: PEMFC: Projected to grow at a CAGR of 14.5%, benefiting from ongoing improvements in durability, cost-effectiveness, and power output.

- Application: Homeland Security: This segment, anticipated to grow at a CAGR of 13.9%, is increasingly adopting fuel cells for portable power in remote surveillance, emergency response vehicles, and personal protective equipment.

- Strategic Initiatives and Partnerships: Collaboration between defense contractors, fuel cell manufacturers, and research institutions is accelerating the development and deployment of specialized fuel cell solutions for military needs. These partnerships are crucial for tailoring technology to specific operational requirements and navigating complex procurement processes. The market share of PEMFCs is estimated to be around 60% in 2025, with a projected increase to 65% by 2033. The overall defense application segment is expected to command over 70% of the market revenue during the forecast period.

Defense Fuel Cells Product Landscape

The defense fuel cells product landscape is characterized by a growing array of highly specialized and robust power solutions. Innovations are centered on enhancing power density, reducing size and weight, and improving operational lifespan for demanding military environments. Key product types include portable fuel cell systems for individual soldiers, integrated power units for unmanned aerial vehicles (UAVs) and ground vehicles, and auxiliary power units (APUs) for naval vessels and aircraft. For example, advancements in DMFC (Direct Methanol Fuel Cell) technology are enabling smaller, more efficient power sources for soldier-worn electronics, while PEMFC systems are increasingly being deployed in medium-altitude, long-endurance (MALE) UAVs, offering extended flight times and reduced acoustic signatures. Performance metrics such as power output (ranging from a few watts to several kilowatts), efficiency, operating temperature range, and fuel consumption are critical differentiators, with manufacturers like Ballard Power and Bloom Energy leading in delivering high-performance, reliable solutions tailored to stringent defense specifications.

Key Drivers, Barriers & Challenges in Defense Fuel Cells

Key Drivers:

- Enhanced Operational Capabilities: Fuel cells provide silent, persistent, and reliable power, crucial for covert operations, extended missions, and reducing the logistical burden of traditional fuel resupply.

- Technological Advancements: Ongoing improvements in fuel cell efficiency, power density, durability, and fuel storage solutions are making them increasingly viable for diverse defense applications.

- National Security Imperatives: Governments are prioritizing energy independence, reduced carbon footprints, and enhanced technological superiority, driving investment in fuel cell research and procurement.

- Cost Reduction Efforts: As production scales and technologies mature, the cost per kilowatt of defense fuel cell systems is expected to decrease, making them more competitive.

Key Barriers & Challenges:

- High Initial Costs: The upfront investment for advanced fuel cell systems and their associated infrastructure can be significant, posing a barrier to widespread adoption, particularly for smaller defense entities.

- Infrastructure and Fueling Logistics: Establishing a reliable supply chain for hydrogen or methanol fuel, along with necessary refueling infrastructure, in remote or operational theaters presents logistical challenges.

- Durability and Reliability in Extreme Conditions: Ensuring long-term performance and reliability of fuel cells in harsh environmental conditions (e.g., extreme temperatures, dust, vibration) remains a critical area of development.

- Integration Complexity: Integrating fuel cell systems into existing military platforms and ensuring interoperability with other systems requires extensive engineering and testing.

- Regulatory Hurdles and Standardization: Developing and adhering to military-specific safety standards and procurement processes can be time-consuming and complex.

Emerging Opportunities in Defense Fuel Cells

Emerging opportunities in the defense fuel cells market lie in the increasing demand for silent and extended-endurance power for unmanned systems, particularly drones and autonomous vehicles. The development of more compact and efficient fuel cells for soldier-worn power generation systems, reducing battery weight and reliance on frequent recharging, represents another significant avenue. Furthermore, the integration of fuel cell technology into naval vessels for silent propulsion and extended patrol capabilities, as well as for powering advanced sensor arrays and communication systems, presents substantial growth potential. The push for sustainable energy solutions within military operations also opens doors for fuel cell-powered auxiliary power units (APUs) and emergency backup power for critical defense infrastructure.

Growth Accelerators in the Defense Fuel Cells Industry

Several catalysts are accelerating the growth of the defense fuel cells industry. Continuous technological breakthroughs, such as advancements in materials science for improved fuel cell membranes and catalysts, are enhancing performance and reducing costs. Strategic partnerships between leading defense contractors and specialized fuel cell manufacturers are crucial for tailoring solutions to specific military requirements and accelerating the path to deployment. Market expansion strategies, including increased government funding for R&D and procurement programs, are further stimulating growth. The growing focus on electrification of military platforms and the need for reliable, sustainable power solutions for next-generation defense systems are significant growth accelerators.

Key Players Shaping the Defense Fuel Cells Market

- Panasonic

- Toshiba

- Siemens

- Posco Energy

- Bloom Energy

- Altergy

- Ballard Power

- FuelCell Energy

- Doosan PureCell America

- Plug Power

- WATT Fuel Cell Corporation

- Ultracell

- SFC Energy

- Neah Power Systems

Notable Milestones in Defense Fuel Cells Sector

- 2019: Ballard Power Systems announces collaboration with a major defense contractor for the development of fuel cell-powered UAVs.

- 2020: U.S. Department of Defense initiates programs to explore fuel cell applications for soldier-portable power.

- 2021: Bloom Energy showcases its Solid Oxide Fuel Cell (SOFC) technology for naval applications.

- 2022: Plug Power partners with a defense firm to integrate fuel cell solutions into military vehicles.

- 2023: SFC Energy delivers advanced fuel cell power solutions for remote surveillance operations.

- 2024: FuelCell Energy receives a significant order for stationary fuel cells for critical defense infrastructure.

In-Depth Defense Fuel Cells Market Outlook

The defense fuel cells market outlook is highly optimistic, driven by an unwavering commitment from global defense organizations to modernize and enhance their operational capabilities through advanced energy solutions. The continuous pursuit of silent, persistent, and efficient power generation for a wide array of applications, from unmanned systems to soldier-worn electronics, will fuel sustained market growth. Strategic investments in research and development by leading nations and the formation of robust public-private partnerships will further accelerate technological innovation and drive down costs, making fuel cells an increasingly accessible and indispensable component of modern defense arsenals. The market is projected to witness a surge in deployments, solidifying its position as a critical enabler of future military superiority.

Defense Fuel Cells Segmentation

-

1. Application

- 1.1. Defense

- 1.2. Homeland Security

-

2. Types

- 2.1. PEMFC

- 2.2. SPFC

- 2.3. DMFC

Defense Fuel Cells Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

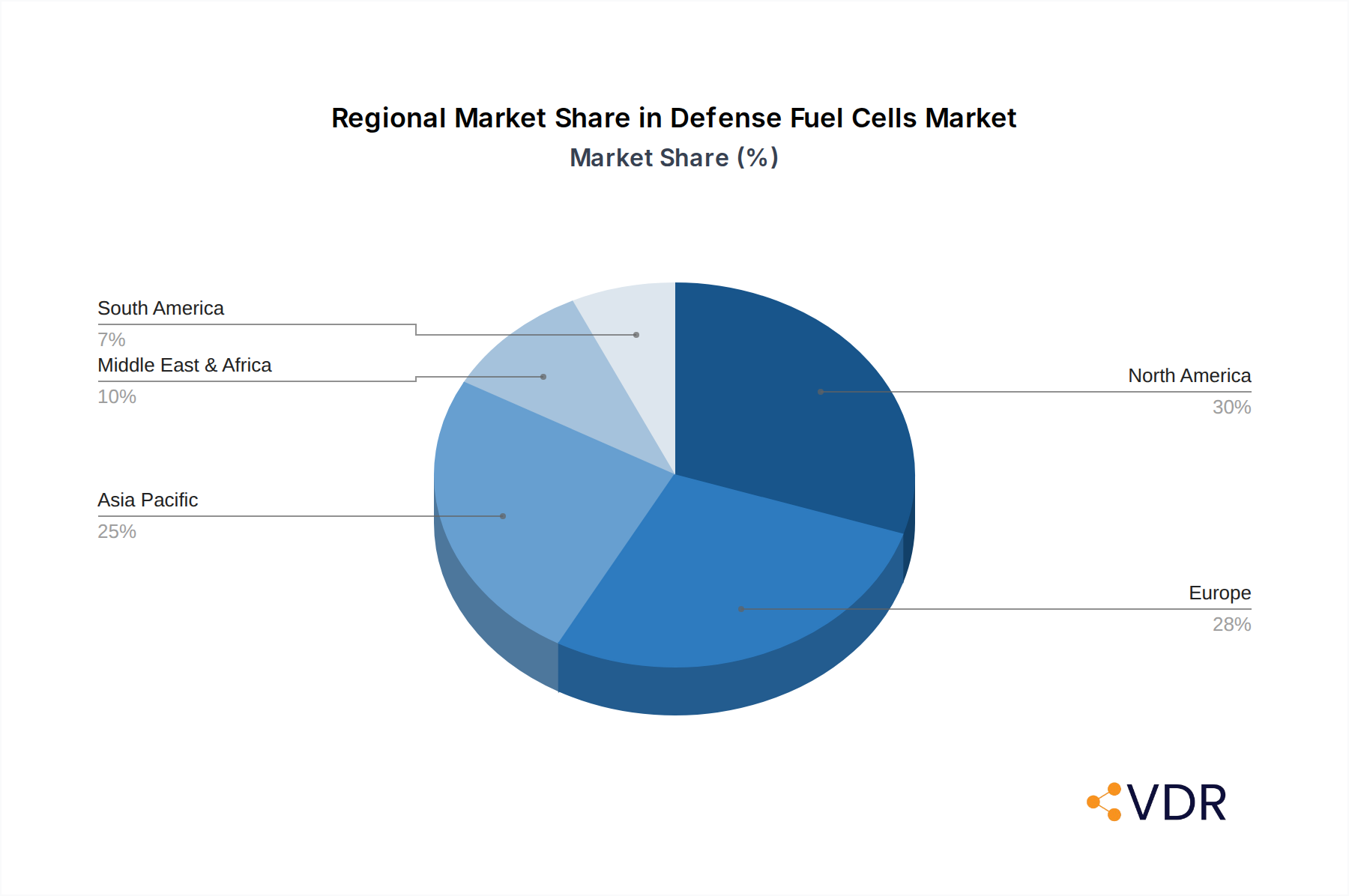

Defense Fuel Cells Regional Market Share

Geographic Coverage of Defense Fuel Cells

Defense Fuel Cells REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 14.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Defense Fuel Cells Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Defense

- 5.1.2. Homeland Security

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. PEMFC

- 5.2.2. SPFC

- 5.2.3. DMFC

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Defense Fuel Cells Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Defense

- 6.1.2. Homeland Security

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. PEMFC

- 6.2.2. SPFC

- 6.2.3. DMFC

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Defense Fuel Cells Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Defense

- 7.1.2. Homeland Security

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. PEMFC

- 7.2.2. SPFC

- 7.2.3. DMFC

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Defense Fuel Cells Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Defense

- 8.1.2. Homeland Security

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. PEMFC

- 8.2.2. SPFC

- 8.2.3. DMFC

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Defense Fuel Cells Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Defense

- 9.1.2. Homeland Security

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. PEMFC

- 9.2.2. SPFC

- 9.2.3. DMFC

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Defense Fuel Cells Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Defense

- 10.1.2. Homeland Security

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. PEMFC

- 10.2.2. SPFC

- 10.2.3. DMFC

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Panasonic

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Toshiba

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Siemens

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Posco Energy

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Bloom Energy

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Altergy

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Ballard Power

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 FuelCell Energy

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Doosan PureCell America

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Plug Power

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 WATT Fuel Cell Corporation

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Ultracell

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 SFC Energy

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Neah Power Systems

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.1 Panasonic

List of Figures

- Figure 1: Global Defense Fuel Cells Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Defense Fuel Cells Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Defense Fuel Cells Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Defense Fuel Cells Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Defense Fuel Cells Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Defense Fuel Cells Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Defense Fuel Cells Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Defense Fuel Cells Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Defense Fuel Cells Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Defense Fuel Cells Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Defense Fuel Cells Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Defense Fuel Cells Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Defense Fuel Cells Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Defense Fuel Cells Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Defense Fuel Cells Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Defense Fuel Cells Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Defense Fuel Cells Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Defense Fuel Cells Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Defense Fuel Cells Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Defense Fuel Cells Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Defense Fuel Cells Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Defense Fuel Cells Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Defense Fuel Cells Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Defense Fuel Cells Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Defense Fuel Cells Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Defense Fuel Cells Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Defense Fuel Cells Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Defense Fuel Cells Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Defense Fuel Cells Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Defense Fuel Cells Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Defense Fuel Cells Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Defense Fuel Cells Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Defense Fuel Cells Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Defense Fuel Cells Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Defense Fuel Cells Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Defense Fuel Cells Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Defense Fuel Cells Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Defense Fuel Cells Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Defense Fuel Cells Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Defense Fuel Cells Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Defense Fuel Cells Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Defense Fuel Cells Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Defense Fuel Cells Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Defense Fuel Cells Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Defense Fuel Cells Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Defense Fuel Cells Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Defense Fuel Cells Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Defense Fuel Cells Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Defense Fuel Cells Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Defense Fuel Cells Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Defense Fuel Cells Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Defense Fuel Cells Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Defense Fuel Cells Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Defense Fuel Cells Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Defense Fuel Cells Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Defense Fuel Cells Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Defense Fuel Cells Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Defense Fuel Cells Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Defense Fuel Cells Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Defense Fuel Cells Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Defense Fuel Cells Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Defense Fuel Cells Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Defense Fuel Cells Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Defense Fuel Cells Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Defense Fuel Cells Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Defense Fuel Cells Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Defense Fuel Cells Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Defense Fuel Cells Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Defense Fuel Cells Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Defense Fuel Cells Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Defense Fuel Cells Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Defense Fuel Cells Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Defense Fuel Cells Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Defense Fuel Cells Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Defense Fuel Cells Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Defense Fuel Cells Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Defense Fuel Cells Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Defense Fuel Cells?

The projected CAGR is approximately 14.8%.

2. Which companies are prominent players in the Defense Fuel Cells?

Key companies in the market include Panasonic, Toshiba, Siemens, Posco Energy, Bloom Energy, Altergy, Ballard Power, FuelCell Energy, Doosan PureCell America, Plug Power, WATT Fuel Cell Corporation, Ultracell, SFC Energy, Neah Power Systems.

3. What are the main segments of the Defense Fuel Cells?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Defense Fuel Cells," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Defense Fuel Cells report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Defense Fuel Cells?

To stay informed about further developments, trends, and reports in the Defense Fuel Cells, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence