Key Insights

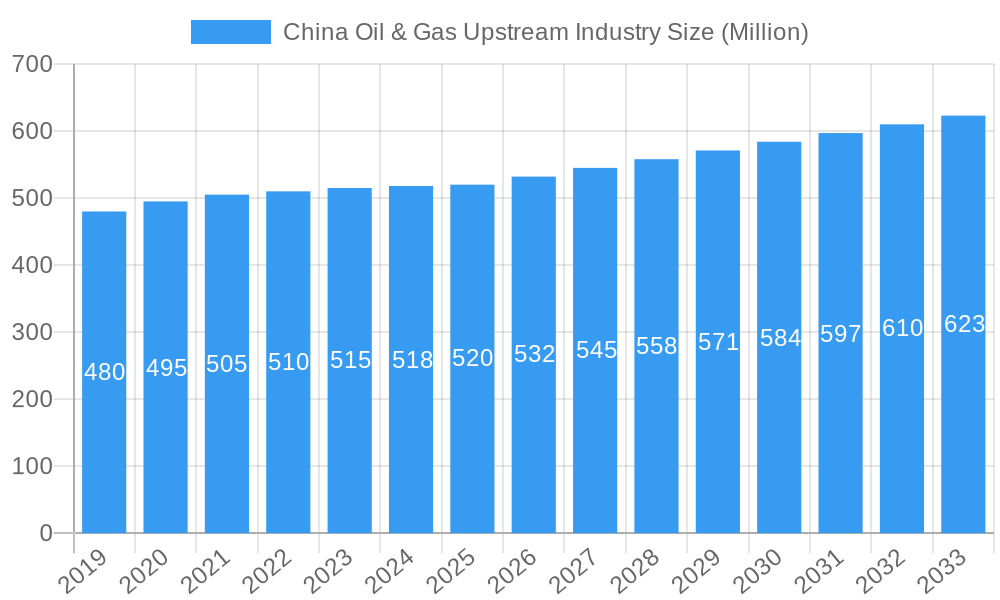

The China Oil & Gas Upstream Industry is projected to experience robust expansion. With a base year of 2025, the market size is estimated at $77.69 billion and is expected to grow at a Compound Annual Growth Rate (CAGR) of 5.15% through 2033. This growth is driven by sustained energy demand from China's industrial and economic sectors, alongside strategic initiatives to boost domestic production and reduce import dependency. The upstream segment, focusing on exploration and production (E&P), is pivotal. Government support for exploration in new regions and the implementation of advanced technologies are key growth catalysts. Investments in onshore and offshore fields are vital for future energy security. China's commitment to energy independence, coupled with technological advancements for efficient extraction from complex reserves, underpins this positive market outlook.

China Oil & Gas Upstream Industry Market Size (In Billion)

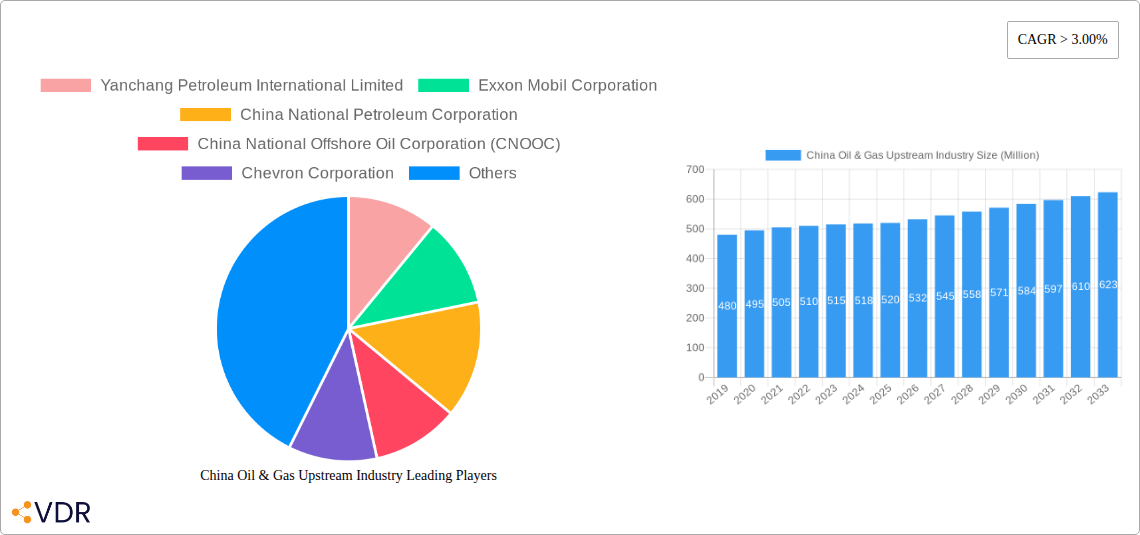

The industry features a dynamic mix of major state-owned enterprises and prominent international corporations. Leading domestic players, including China National Petroleum Corporation (CNPC), China National Offshore Oil Corporation (CNOOC), and Sinopec, spearhead exploration and production, utilizing extensive resources and local geological expertise. Global energy giants such as ExxonMobil, Chevron, and BP contribute significant technological innovation and capital investment. The sector is increasingly focusing on both conventional and unconventional resources, including shale oil and gas. While navigating challenges like volatile global oil prices, environmental regulations, and the energy transition, China's substantial energy consumption and its strategic priority for domestic supply ensure ongoing investment and development in the oil and gas upstream sector.

China Oil & Gas Upstream Industry Company Market Share

China Oil & Gas Upstream Industry Market Analysis: Reserving the Future of Energy (2019–2033)

Uncover the critical trends, market dynamics, and future trajectory of China's booming Oil & Gas Upstream Industry. This comprehensive report, covering the Study Period 2019–2033 with Base Year 2025, delivers unparalleled insights into the parent and child market segments, investment opportunities, and key players shaping the nation's energy security. With meticulous data analysis, including quantitative projections and qualitative assessments, this report is an indispensable resource for industry professionals, investors, and policymakers seeking to navigate and capitalize on the rapidly evolving Chinese energy landscape. All monetary values are presented in Million units.

China Oil & Gas Upstream Industry Market Dynamics & Structure

The China Oil & Gas Upstream Industry is characterized by a dynamic interplay of state-owned giants and emerging private players, navigating a complex regulatory environment driven by national energy security imperatives. Market concentration remains high, with major entities like China National Petroleum Corporation (CNPC), China National Offshore Oil Corporation (CNOOC), and China Petroleum & Chemical Corporation (Sinopec) holding substantial influence. Technological innovation is a key driver, with significant investments flowing into advanced exploration and production (E&P) techniques, particularly for challenging onshore and offshore reserves. Regulatory frameworks, while evolving, prioritize domestic production and sustainable development, influencing foreign investment and operational strategies. Competitive product substitutes, though growing in renewable energy, are not yet a direct threat to the foundational demand for oil and gas in the medium term. End-user demographics are shifting, with increasing demand from industrial sectors and a growing, albeit still nascent, focus on cleaner energy integration. Mergers and acquisitions (M&A) trends are closely tied to national strategic goals, often involving consolidation for efficiency and resource optimization.

- Market Concentration: Dominated by CNPC, CNOOC, and Sinopec, with a combined market share exceeding 85%.

- Technological Innovation Drivers: Focus on deepwater exploration, shale gas technology, and enhanced oil recovery (EOR) methods.

- Regulatory Frameworks: Driven by national energy security policies, environmental regulations, and production targets.

- Competitive Product Substitutes: Growing but not yet significantly impacting upstream demand in the forecast period.

- M&A Trends: Strategic acquisitions and partnerships aimed at consolidating resources and technological capabilities.

China Oil & Gas Upstream Industry Growth Trends & Insights

The China Oil & Gas Upstream Industry is poised for substantial growth, fueled by escalating domestic energy demand and strategic government initiatives to bolster national energy security. The market size is projected to witness a Compound Annual Growth Rate (CAGR) of approximately 4.5% over the forecast period of 2025–2033, reaching an estimated market value of over $250,000 Million by 2033. Adoption rates for advanced E&P technologies, such as seismic imaging and horizontal drilling, are rapidly increasing, enabling the exploitation of previously inaccessible reserves. Technological disruptions, including the application of artificial intelligence (AI) and machine learning (ML) in reservoir analysis and production optimization, are becoming integral to operational efficiency. Consumer behavior shifts, while primarily driven by the industrial sector, are beginning to incorporate a growing awareness of environmental impact, indirectly influencing the demand for cleaner extraction methods and gas over liquid fuels where feasible. China's commitment to energy self-sufficiency will continue to be a paramount factor driving upstream investments, particularly in both onshore and offshore exploration projects. The discovery of significant new reserves, as detailed in the industry developments, underscores the immense potential for sustained production growth. The increasing complexity and depth of discovered fields necessitate higher capital expenditure, which in turn drives innovation and market expansion. The integration of digital technologies is also enhancing operational efficiency, reducing costs, and improving safety standards across the sector.

Dominant Regions, Countries, or Segments in China Oil & Gas Upstream Industry

The Onshore segment currently dominates the China Oil & Gas Upstream Industry, driven by established production bases and significant recent discoveries, particularly in the Tarim Basin. This dominance is further cemented by favorable economic policies and extensive infrastructure development that supports onshore exploration and extraction. The Tarim Basin, located in the Xinjiang Uygur Autonomous Region, has emerged as a critical hub for both oil and gas production, with recent discoveries by Sinopec and CNPC highlighting its vast, untapped potential. These discoveries, such as Sinopec's Shunbei oil and gas field with approximately 100 million tons of reserves and CNPC's super-deep oil and gas area with 1 billion tons of reserves, underscore the strategic importance and high growth potential of onshore regions.

- Tarim Basin Dominance: The Tarim Basin is a key driver of onshore growth, boasting substantial oil and gas reserves and ongoing exploration success.

- Sinopec's Shunbei Discovery: An estimated 88 million tons of condensate oil and 290 billion cubic meters of natural gas.

- CNPC's Super-Deep Discovery: A 1-billion-ton oil and gas area with significant drilling depths.

- Economic Policies: Government incentives and policies aimed at boosting domestic production provide a strong impetus for onshore development.

- Infrastructure: Existing and expanding pipeline networks and transportation facilities facilitate efficient resource exploitation and distribution.

- Technological Advancement in Onshore: Innovations in shale oil extraction, as evidenced by PetroChina's Gulong prospect discovery (1.268 billion tons of oil in place), are unlocking previously uneconomical reserves.

- Growth Potential: The ongoing exploration and development in basins like Tarim and Songliao indicate sustained high growth potential for the onshore segment.

While the Offshore segment, particularly in the South China Sea, also holds significant potential and is a focus for CNOOC, onshore developments currently command a larger share of market activity and investment due to established infrastructure and more accessible reserves. However, offshore exploration is set to grow in importance as technological advancements make deepwater extraction more viable.

China Oil & Gas Upstream Industry Product Landscape

The product landscape in China's oil and gas upstream sector is primarily focused on the extraction of crude oil and natural gas. Innovations are centered on enhancing recovery rates from existing fields and unlocking new reserves through advanced exploration and drilling techniques. This includes the development of specialized equipment for deep drilling, sophisticated seismic imaging technologies for better reservoir characterization, and advanced hydraulic fracturing methods for shale resources. The performance metrics revolve around reserve discovery rates, production volumes, extraction efficiency, and cost per barrel. Unique selling propositions for companies lie in their ability to access challenging reserves, their technological prowess in maximizing recovery, and their adherence to increasingly stringent environmental standards.

Key Drivers, Barriers & Challenges in China Oil & Gas Upstream Industry

Key Drivers:

- National Energy Security: China's strong imperative to reduce reliance on imported energy sources is a primary growth accelerator.

- Growing Domestic Demand: Sustained economic growth and industrialization drive continuous demand for oil and gas.

- Technological Advancements: Innovations in exploration, drilling, and extraction technologies enable access to new and complex reserves.

- Government Support & Investment: Favorable policies and significant state-backed investment in the sector.

- Resource Potential: Vast and diverse geological formations with identified significant hydrocarbon reserves.

Barriers & Challenges:

- Environmental Regulations: Stricter environmental protection laws increase operational costs and compliance burdens.

- Geological Complexity: Exploiting deep, ultra-deep, and offshore reserves presents significant technical and financial challenges.

- Geopolitical Risks: Global energy market volatility and international relations can impact supply chains and investment.

- Aging Infrastructure: Modernization and maintenance of existing infrastructure require substantial capital expenditure.

- Talent Shortage: A need for specialized expertise in advanced E&P technologies.

- Supply Chain Disruptions: Global events can impact the availability and cost of critical equipment and materials.

Emerging Opportunities in China Oil & Gas Upstream Industry

Emerging opportunities lie in the increased exploitation of shale oil and gas, particularly in mature basins like Daqing, as demonstrated by PetroChina's significant discovery. The development of ultra-deep oil and gas fields in basins like Tarim presents a significant frontier for future production. Furthermore, advancements in carbon capture, utilization, and storage (CCUS) technologies within upstream operations offer opportunities for more sustainable hydrocarbon extraction and the potential to develop new revenue streams. Investments in digital transformation, including AI and IoT for predictive maintenance and optimized production, are also creating new avenues for efficiency and cost reduction.

Growth Accelerators in the China Oil & Gas Upstream Industry Industry

Long-term growth in the China Oil & Gas Upstream Industry will be significantly accelerated by continued state investment in strategic exploration projects, particularly in frontier regions like the Tarim Basin and offshore continental shelves. Technological breakthroughs in enhanced oil recovery (EOR) techniques will be crucial for maximizing output from mature fields. Strategic partnerships with international oil companies for technology transfer and joint ventures in complex projects will also play a vital role. Furthermore, the increasing integration of digital technologies across the value chain, from seismic data analysis to automated drilling, will drive efficiency and cost-effectiveness, acting as significant growth catalysts.

Key Players Shaping the China Oil & Gas Upstream Industry Market

- Yanchang Petroleum International Limited

- Exxon Mobil Corporation

- China National Petroleum Corporation

- China National Offshore Oil Corporation (CNOOC)

- Chevron Corporation

- BP PLC

- Shell PLC

- China Petroleum & Chemical Corporation (Sinopec)

Notable Milestones in China Oil & Gas Upstream Industry Sector

- January 2022: Sinopec discovered a new oil and gas area with approximately 100 million tons of reserves in the Tarim Basin. These reserves in Sinopec's Shunbei oil and gas field are estimated to provide 88 million tons of condensate oil and 290 billion cubic meters of natural gas, significantly boosting domestic reserves.

- June 2021: China National Petroleum Corporation (CNPC) announced the discovery of a new 1-billion-ton super-deep oil and gas area in the Tarim Basin. The well's depth of 8,470 meters and an oil column height of 550 meters highlighted advancements in deep E&P capabilities.

- August 2021: PetroChina announced a massive shale oil discovery at the Gulong prospect in the Songliao Basin, detecting 1.268 billion tons of oil in place (9.3 billion barrels), indicating the potential of unconventional resources.

In-Depth China Oil & Gas Upstream Industry Market Outlook

The outlook for China's Oil & Gas Upstream Industry remains robust, driven by a strategic imperative for energy self-sufficiency and continued economic expansion. Growth accelerators will center on leveraging advanced technologies to unlock complex reserves, such as ultra-deep onshore fields and deepwater offshore opportunities. The sustained investment in exploration and production, coupled with government support for domestic resource development, will ensure a strong trajectory. Furthermore, the increasing focus on digitalization and operational efficiency will enhance competitiveness and sustainability. The market is expected to see continued strategic collaborations and technological innovation, positioning China to meet its growing energy demands effectively.

China Oil & Gas Upstream Industry Segmentation

- 1. Onshore

- 2. Offshore

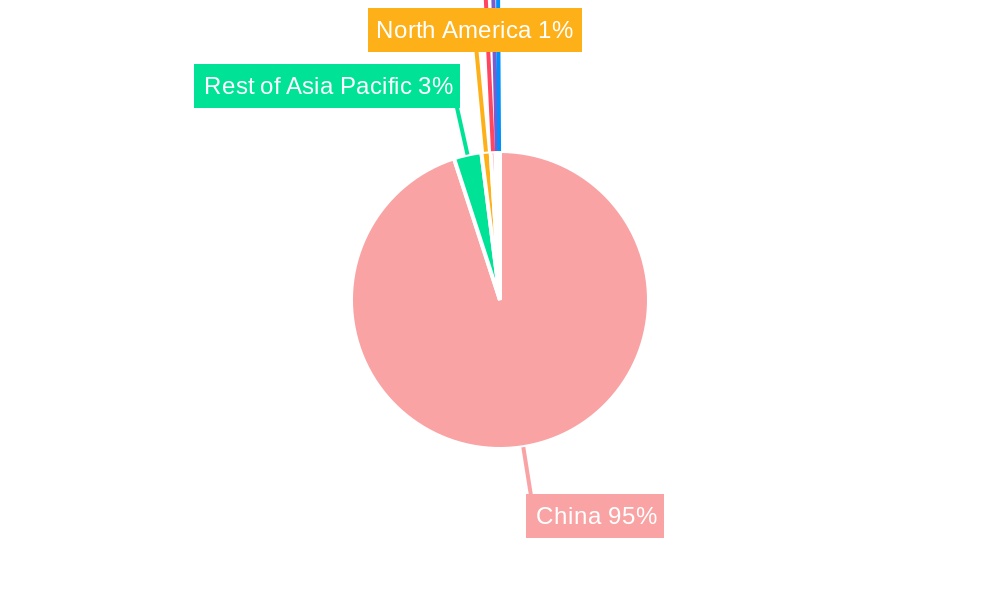

China Oil & Gas Upstream Industry Segmentation By Geography

- 1. China

China Oil & Gas Upstream Industry Regional Market Share

Geographic Coverage of China Oil & Gas Upstream Industry

China Oil & Gas Upstream Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.15% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Onshore

- 5.2. Market Analysis, Insights and Forecast - by Offshore

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. China

- 6. China Oil & Gas Upstream Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Onshore

- 6.2. Market Analysis, Insights and Forecast - by Offshore

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Yanchang Petroleum International Limited

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Exxon Mobil Corporation

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 China National Petroleum Corporation

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 China National Offshore Oil Corporation (CNOOC)

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Chevron Corporation

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 BP PLC

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Shell PLC*List Not Exhaustive

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 China Petroleum & Chemical Corporation (Sinopec)

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.1 Yanchang Petroleum International Limited

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: China Oil & Gas Upstream Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: China Oil & Gas Upstream Industry Share (%) by Company 2025

List of Tables

- Table 1: China Oil & Gas Upstream Industry Revenue billion Forecast, by Onshore 2020 & 2033

- Table 2: China Oil & Gas Upstream Industry Revenue billion Forecast, by Offshore 2020 & 2033

- Table 3: China Oil & Gas Upstream Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: China Oil & Gas Upstream Industry Revenue billion Forecast, by Onshore 2020 & 2033

- Table 5: China Oil & Gas Upstream Industry Revenue billion Forecast, by Offshore 2020 & 2033

- Table 6: China Oil & Gas Upstream Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the China Oil & Gas Upstream Industry?

The projected CAGR is approximately 5.15%.

2. Which companies are prominent players in the China Oil & Gas Upstream Industry?

Key companies in the market include Yanchang Petroleum International Limited, Exxon Mobil Corporation, China National Petroleum Corporation, China National Offshore Oil Corporation (CNOOC), Chevron Corporation, BP PLC, Shell PLC*List Not Exhaustive, China Petroleum & Chemical Corporation (Sinopec).

3. What are the main segments of the China Oil & Gas Upstream Industry?

The market segments include Onshore, Offshore.

4. Can you provide details about the market size?

The market size is estimated to be USD 77.69 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Increasing Electricity Demand4.; Rsing Investments in the Coal Industry.

6. What are the notable trends driving market growth?

Offshore Segment to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; Increasing Installation of Renewable Energy Sources.

8. Can you provide examples of recent developments in the market?

In January 2022, Sinopec discovered a new oil and gas area with approximately 100 million tons of reserves in the Tarim Basin of northwest China's Xinjiang Uygur Autonomous Region. These latest reserves in Sinopec's Shunbei oil and gas field are estimated to provide 88 million tons of condensate oil and 290 billion cubic meters of natural gas.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "China Oil & Gas Upstream Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the China Oil & Gas Upstream Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the China Oil & Gas Upstream Industry?

To stay informed about further developments, trends, and reports in the China Oil & Gas Upstream Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence