Key Insights

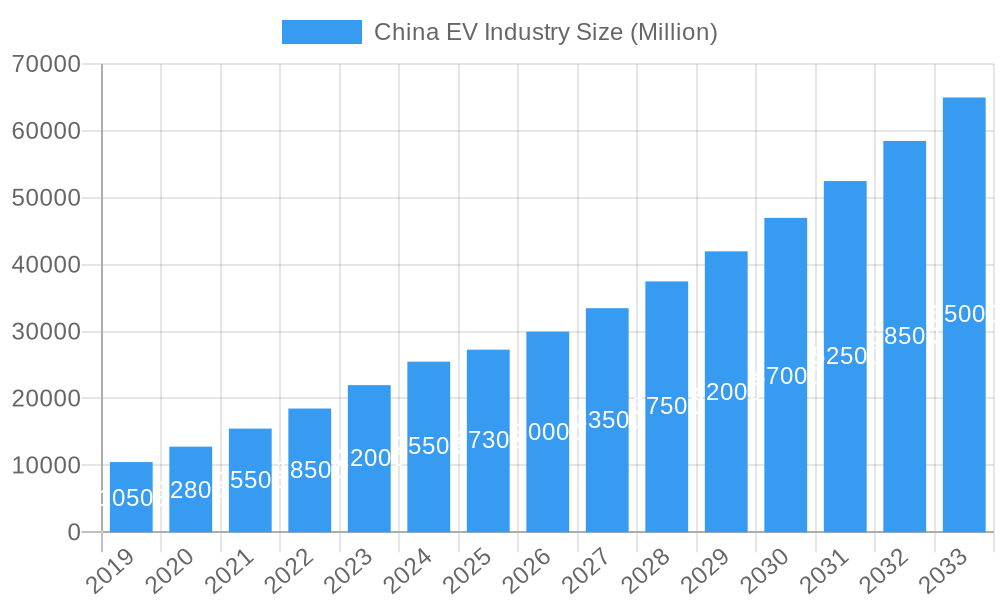

The China Electric Vehicle (EV) industry is poised for explosive growth, driven by robust government support, increasing consumer adoption, and significant technological advancements. The market is projected to reach a substantial $27,302 million by 2025, exhibiting an impressive Compound Annual Growth Rate (CAGR) of 18.3% through 2033. This surge is primarily fueled by government mandates and incentives promoting green transportation, alongside a burgeoning consumer preference for eco-friendly and technologically advanced vehicles. The widespread availability of charging infrastructure and a diversifying range of EV models, from practical hatchbacks and multi-purpose vehicles to dynamic sedans and SUVs, are further accelerating adoption. The market's dynamism is further highlighted by the increasing penetration of Battery Electric Vehicles (BEVs), along with growing interest in Fuel Cell Electric Vehicles (FCEVs), Hybrid Electric Vehicles (HEVs), and Plug-in Hybrid Electric Vehicles (PHEVs), catering to a broad spectrum of consumer needs and preferences. Leading players like BYD Auto, Tesla, and Volkswagen AG are fiercely competing, introducing innovative technologies and expanding production capacities to capture market share.

China EV Industry Market Size (In Billion)

The competitive landscape in China's EV market is intensely dynamic, characterized by the rapid innovation and strategic expansions of both domestic and international manufacturers. Chinese giants such as BYD Auto, Nio, Gac Aion, Li Auto, Wuling Motors, Hozon, and Chery Automobile are at the forefront, leveraging local market understanding and government backing to their advantage. International players like Tesla and Volkswagen AG are also making significant investments to strengthen their presence. The market is segmented across various vehicle configurations, including hatchbacks, multi-purpose vehicles, sedans, and sports utility vehicles, ensuring a wide choice for consumers. Furthermore, the fuel category segment is dominated by BEVs, with FCEVs, HEVs, and PHEVs gaining traction. Future growth is expected to be propelled by advancements in battery technology, enhanced charging infrastructure, and the continuous introduction of more affordable and feature-rich EV models, solidifying China's position as a global leader in the electric mobility revolution.

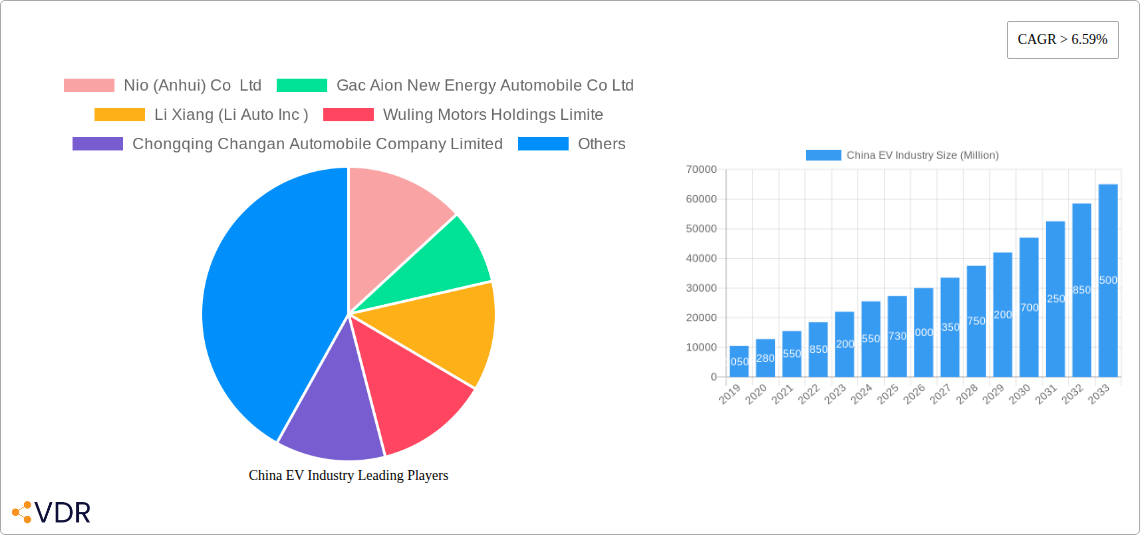

China EV Industry Company Market Share

China EV Industry Report: Unlocking Future Growth in the Electric Vehicle Revolution

Gain unparalleled insights into the dynamic China EV industry with this comprehensive report. Spanning from 2019 to 2033, with a base year of 2025 and a forecast period of 2025–2033, this report delves deep into market evolution, technological advancements, and strategic opportunities. Essential for industry professionals, investors, and policymakers, this analysis dissects the parent and child market segments, providing actionable intelligence to navigate this rapidly expanding sector.

China EV Industry Market Dynamics & Structure

The China Electric Vehicle (EV) industry is characterized by a dynamic and evolving market structure. Market concentration is influenced by a mix of established automotive giants and agile new entrants, with key players like BYD Auto Co Ltd and Tesla Inc holding significant market share. Technological innovation is primarily driven by advancements in battery technology, powertrain efficiency, and intelligent vehicle features, creating a competitive landscape where continuous R&D is paramount. Regulatory frameworks, including government subsidies and emission standards, play a crucial role in shaping market trajectory and incentivizing EV adoption. Competitive product substitutes include traditional internal combustion engine (ICE) vehicles, although their market share is steadily declining. End-user demographics are broadening, encompassing a wider range of income levels and urban-rural divides, with increasing demand for advanced features and sustainable transportation solutions. Mergers and acquisitions (M&A) trends are active as companies seek to consolidate their market position, acquire crucial technologies, or expand their product portfolios. For instance, Tesla's acquisition of SiILion battery in November 2023 signals a strategic move to bolster battery production capabilities.

- Market Concentration: Dominated by a few major players but with a growing number of specialized EV manufacturers.

- Technological Innovation: Focus on battery density, charging speed, and autonomous driving capabilities.

- Regulatory Impact: Government policies significantly influence consumer adoption and manufacturer strategies.

- M&A Activity: Driven by the pursuit of technological parity and market consolidation.

- End-User Diversification: Expanding consumer base with varied needs and preferences.

China EV Industry Growth Trends & Insights

The China EV industry is poised for remarkable growth, driven by a confluence of supportive government policies, increasing consumer awareness of environmental sustainability, and significant technological advancements. The market size evolution is projected to be substantial, with the Base Year (2025) estimated to see sales reach approximately xx million units. This upward trajectory is expected to continue throughout the Forecast Period (2025–2033), with a projected Compound Annual Growth Rate (CAGR) of xx%. Adoption rates are accelerating, fueled by the expanding charging infrastructure and the increasing availability of diverse EV models across all vehicle configurations, from compact hatchbacks to spacious SUVs. Technological disruptions are a constant feature, with breakthroughs in solid-state batteries and faster charging capabilities set to redefine user experience and address range anxiety. Consumer behavior shifts are evident, with a growing preference for intelligent features, connectivity, and the overall lower cost of ownership associated with EVs. The Historical Period (2019–2024) witnessed the foundational growth of the industry, laying the groundwork for its current expansion. Market penetration of EVs is expected to surpass xx% of the total automotive market by 2033, a testament to the industry's transformative impact.

- Market Size Projection: Significant expansion from xx million units in 2025 to an estimated xx million units by 2033.

- CAGR: Anticipated growth rate of xx% during the forecast period.

- Adoption Rates: Steadily increasing due to policy support and product proliferation.

- Technological Disruptions: Continuous innovation in battery and charging technology.

- Consumer Behavior: Shifting towards sustainable, connected, and cost-effective mobility solutions.

- Market Penetration: Expected to exceed xx% of the total vehicle market by 2033.

Dominant Regions, Countries, or Segments in China EV Industry

Within the expansive China EV industry, the Passenger Cars segment, particularly Sports Utility Vehicles (SUVs) and Sedans, is currently the dominant force driving market growth. These configurations cater to the evolving needs of Chinese consumers, offering a blend of practicality, comfort, and advanced technology. Geographically, Eastern China, with its high population density, robust economic development, and extensive charging infrastructure, stands as the leading region. The BEV (Battery Electric Vehicle) fuel category overwhelmingly dominates, accounting for the vast majority of EV sales due to government incentives and rapid technological advancements in battery electric powertrains. Key drivers for this dominance include strong economic policies from central and provincial governments that prioritize EV adoption through subsidies, tax exemptions, and preferential licensing. The rapid expansion of charging infrastructure, especially in urban centers within dominant regions, further facilitates BEV adoption. Market share within the dominant segments is highly competitive, with players like BYD Auto Co Ltd and Gac Aion New Energy Automobile Co Ltd showing strong performance. The growth potential within these segments remains exceptionally high, driven by increasing consumer demand and the continuous introduction of new, innovative models.

- Dominant Segment: Passenger Cars (SUVs and Sedans) leading market expansion.

- Leading Region: Eastern China, driven by economic prosperity and infrastructure.

- Dominant Fuel Category: BEV (Battery Electric Vehicle) due to policy support and technological maturity.

- Key Drivers:

- Economic Policies: Subsidies, tax incentives, and preferential regulations.

- Infrastructure Development: Rapid expansion of charging networks.

- Consumer Demand: Growing preference for sustainable and technologically advanced vehicles.

- Market Share: Highly competitive, with leading domestic and international manufacturers vying for dominance.

- Growth Potential: Substantial, fueled by ongoing innovation and market expansion.

China EV Industry Product Landscape

The China EV industry's product landscape is characterized by a relentless pursuit of innovation and performance. Companies are investing heavily in enhancing battery energy density, leading to longer driving ranges and faster charging times. Advanced driver-assistance systems (ADAS) and integrated smart cockpit technologies are becoming standard features, offering a more connected and intuitive driving experience. Unique selling propositions often revolve around proprietary battery management systems, sustainable material sourcing, and sleek, aerodynamic designs that optimize efficiency. Tesla Inc, for example, continues to push boundaries with its Autopilot features and software updates. Chery Automobile Co Ltd is also making strides in developing affordable yet feature-rich EV options. The performance metrics of new EVs, including acceleration, top speed, and charging efficiency, are continuously improving, making them increasingly attractive alternatives to traditional vehicles.

Key Drivers, Barriers & Challenges in China EV Industry

Key Drivers: The China EV industry is propelled by strong government support, including favorable policies and subsidies aimed at achieving carbon neutrality goals. Rapid technological advancements in battery technology, leading to increased range and faster charging, are crucial drivers. Growing environmental consciousness among consumers and the desire for lower running costs also contribute significantly. The expansion of charging infrastructure is further accelerating adoption.

Barriers & Challenges: Supply chain constraints, particularly for critical raw materials like lithium and cobalt, pose a significant challenge. Intense competition among a large number of manufacturers can lead to price wars and impact profitability. Regulatory hurdles and the evolving landscape of safety standards can also present difficulties. Developing robust and accessible charging infrastructure across the entire country remains a substantial undertaking. The initial purchase cost, though decreasing, can still be a barrier for some consumer segments.

Emerging Opportunities in China EV Industry

Emerging opportunities in the China EV industry lie in the expansion of the commercial EV segment, including electric buses and delivery vehicles, which present significant untapped market potential. The development of battery-swapping technology offers a faster alternative to charging, potentially revolutionizing urban mobility. Furthermore, the growing demand for premium EVs with advanced autonomous driving capabilities and personalized connectivity features presents a lucrative niche. The integration of EVs into smart grids and the development of vehicle-to-grid (V2G) technology are also emerging as key areas for future growth and innovation.

Growth Accelerators in the China EV Industry Industry

Several catalysts are accelerating the long-term growth of the China EV industry. Technological breakthroughs in solid-state batteries promise enhanced safety, higher energy density, and faster charging, which will significantly reduce range anxiety. Strategic partnerships between established automakers and battery manufacturers, such as Volkswagen AG's collaborations, are crucial for securing supply chains and accelerating innovation. Market expansion strategies, including the development of more affordable EV models and the penetration into rural markets, will broaden the consumer base. Investments in advanced manufacturing processes and smart factory technologies are also key to improving production efficiency and reducing costs.

Key Players Shaping the China EV Industry Market

- Nio (Anhui) Co Ltd

- Gac Aion New Energy Automobile Co Ltd

- Li Xiang (Li Auto Inc )

- Wuling Motors Holdings Limite

- Chongqing Changan Automobile Company Limited

- Volkswagen AG

- Hozon New Energy Automobile Co Ltd

- Tesla Inc

- BYD Auto Co Ltd

- Chery Automobile Co Ltd

Notable Milestones in China EV Industry Sector

- November 2023: Tesla has acquired US-based start-up SiILion battery (Battery manufacturer) to excel the battery production in US.

- November 2023: In Argentina, Volkswagen debuted the brand-new Nivus. Both the Comfortline and Highline models of the VW Nivus will be offered in Argentina. They both come equipped with a 1.0-liter TSi three-cylinder engine that generates 116 horsepower and 200 Nm of torque and is coupled to a six-speed automated transmission.

- November 2023: Tesla opened its single-point electric vehicle super-charging station between the Bay Area and Los Angeles areas in the US.

In-Depth China EV Industry Market Outlook

The in-depth China EV industry market outlook is exceptionally positive, driven by continuous technological innovation, robust government support, and evolving consumer preferences for sustainable mobility. Future market potential lies in the increasing sophistication of battery technology, enabling longer ranges and faster charging, which will further alleviate consumer concerns. Strategic opportunities abound in the development of advanced autonomous driving systems, the expansion of charging infrastructure, and the integration of EVs into broader smart city ecosystems. The burgeoning demand for electric light commercial vehicles and the potential of battery-swapping technology represent significant avenues for future growth and market diversification.

China EV Industry Segmentation

-

1. Vehicle Configuration

-

1.1. Passenger Cars

- 1.1.1. Hatchback

- 1.1.2. Multi-purpose Vehicle

- 1.1.3. Sedan

- 1.1.4. Sports Utility Vehicle

-

1.1. Passenger Cars

-

2. Fuel Category

- 2.1. BEV

- 2.2. FCEV

- 2.3. HEV

- 2.4. PHEV

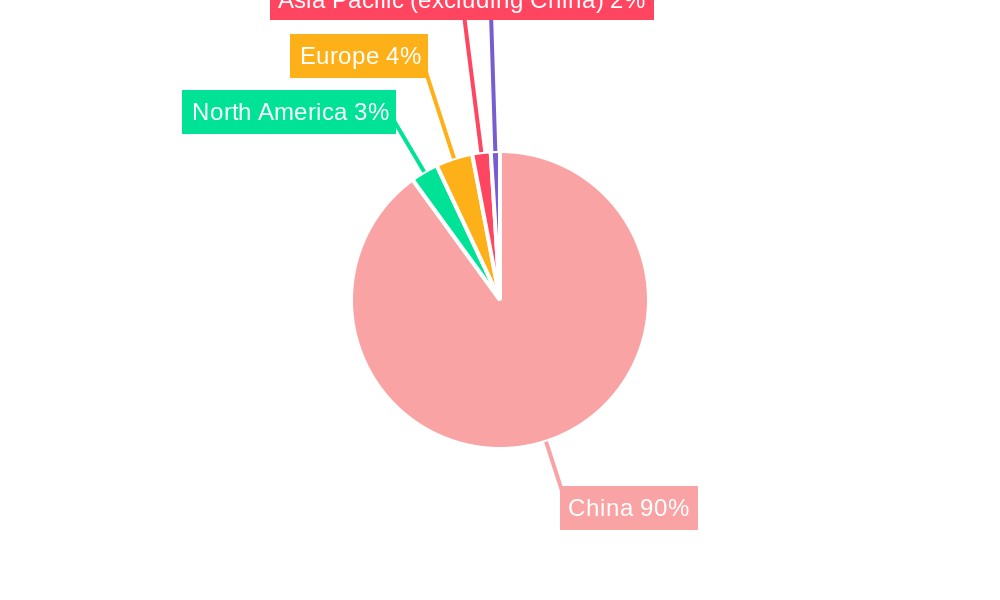

China EV Industry Segmentation By Geography

- 1. China

China EV Industry Regional Market Share

Geographic Coverage of China EV Industry

China EV Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 18.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Configuration

- 5.1.1. Passenger Cars

- 5.1.1.1. Hatchback

- 5.1.1.2. Multi-purpose Vehicle

- 5.1.1.3. Sedan

- 5.1.1.4. Sports Utility Vehicle

- 5.1.1. Passenger Cars

- 5.2. Market Analysis, Insights and Forecast - by Fuel Category

- 5.2.1. BEV

- 5.2.2. FCEV

- 5.2.3. HEV

- 5.2.4. PHEV

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. China

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Configuration

- 6. China EV Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Vehicle Configuration

- 6.1.1. Passenger Cars

- 6.1.1.1. Hatchback

- 6.1.1.2. Multi-purpose Vehicle

- 6.1.1.3. Sedan

- 6.1.1.4. Sports Utility Vehicle

- 6.1.1. Passenger Cars

- 6.2. Market Analysis, Insights and Forecast - by Fuel Category

- 6.2.1. BEV

- 6.2.2. FCEV

- 6.2.3. HEV

- 6.2.4. PHEV

- 6.1. Market Analysis, Insights and Forecast - by Vehicle Configuration

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Nio (Anhui) Co Ltd

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Gac Aion New Energy Automobile Co Ltd

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Li Xiang (Li Auto Inc )

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Wuling Motors Holdings Limite

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Chongqing Changan Automobile Company Limited

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Volkswagen AG

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Hozon New Energy Automobile Co Ltd

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Tesla Inc

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 BYD Auto Co Ltd

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Chery Automobile Co Ltd

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Nio (Anhui) Co Ltd

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: China EV Industry Revenue Breakdown (undefined, %) by Product 2025 & 2033

- Figure 2: China EV Industry Share (%) by Company 2025

List of Tables

- Table 1: China EV Industry Revenue undefined Forecast, by Vehicle Configuration 2020 & 2033

- Table 2: China EV Industry Revenue undefined Forecast, by Fuel Category 2020 & 2033

- Table 3: China EV Industry Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: China EV Industry Revenue undefined Forecast, by Vehicle Configuration 2020 & 2033

- Table 5: China EV Industry Revenue undefined Forecast, by Fuel Category 2020 & 2033

- Table 6: China EV Industry Revenue undefined Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the China EV Industry?

The projected CAGR is approximately 18.3%.

2. Which companies are prominent players in the China EV Industry?

Key companies in the market include Nio (Anhui) Co Ltd, Gac Aion New Energy Automobile Co Ltd, Li Xiang (Li Auto Inc ), Wuling Motors Holdings Limite, Chongqing Changan Automobile Company Limited, Volkswagen AG, Hozon New Energy Automobile Co Ltd, Tesla Inc, BYD Auto Co Ltd, Chery Automobile Co Ltd.

3. What are the main segments of the China EV Industry?

The market segments include Vehicle Configuration, Fuel Category.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

Increasing Air Pollution Awareness and Health Concern is Driving the Demand.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

High Cost of Installation Related to Industrial Robots.

8. Can you provide examples of recent developments in the market?

November 2023: Tesla has acquired US-based start-up SiILion battery (Battery manufacturer) to excel the battery production in US.November 2023: In Argentina, Volkswagen debuted the brand-new Nivus. Both the Comfortline and Highline models of the VW Nivus will be offered in Argentina. They both come equipped with a 1.0-liter TSi three-cylinder engine that generates 116 horsepower and 200 Nm of torque and is coupled to a six-speed automated transmission.November 2023: Tesla opened its single-point electric vehicle super-charging station between the Bay Area and Los Angeles areas in the US.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "China EV Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the China EV Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the China EV Industry?

To stay informed about further developments, trends, and reports in the China EV Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence