Key Insights

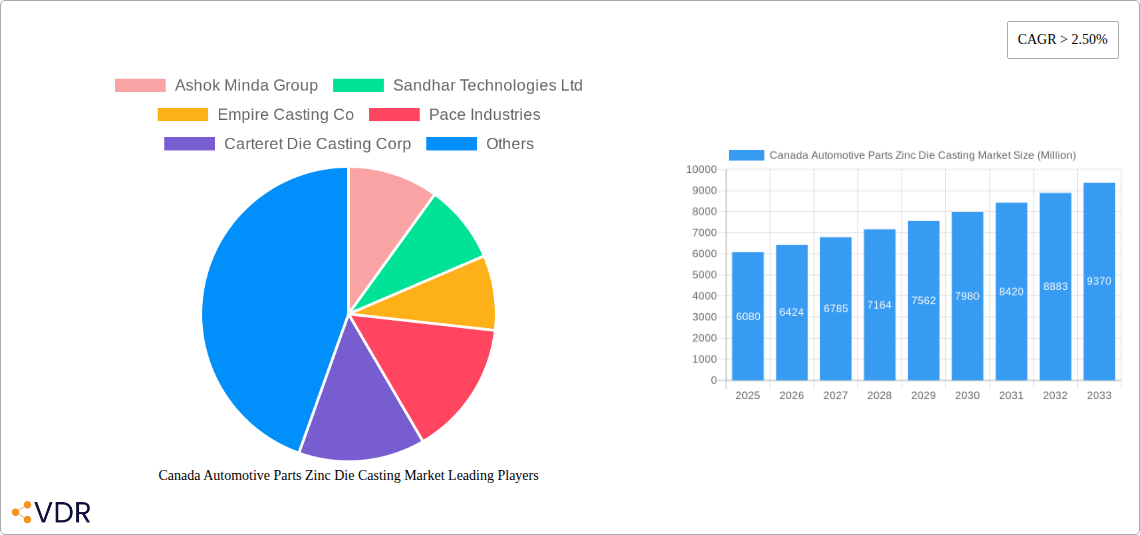

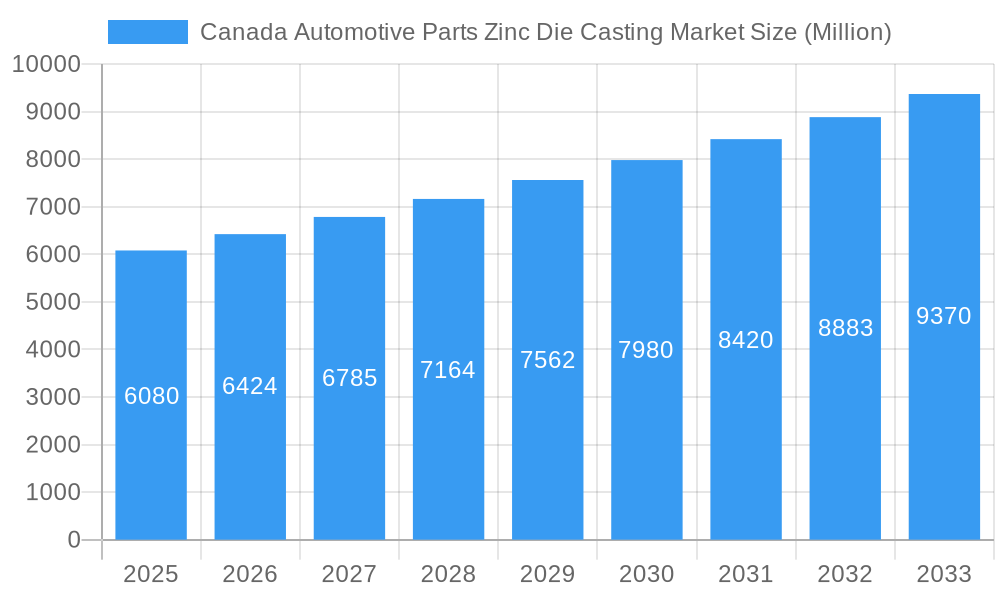

The Canada Automotive Parts Zinc Die Casting Market is poised for substantial growth, with a projected market size of $6.08 billion in 2025, driven by a robust Compound Annual Growth Rate (CAGR) of 5.6% through 2033. This upward trajectory is fueled by several key factors. The increasing demand for lightweight and durable automotive components, particularly engine parts and transmission systems, is a primary driver. Advanced manufacturing techniques like vacuum die casting are gaining traction, enabling the production of more complex and precise parts, thereby enhancing vehicle performance and fuel efficiency. Furthermore, the growing adoption of electric vehicles (EVs) necessitates specialized zinc die-cast components for battery housings, power electronics, and structural elements, contributing significantly to market expansion. Government initiatives promoting automotive manufacturing and stricter safety and emission standards also play a crucial role in stimulating the demand for high-quality, precision-engineered zinc die-cast parts.

Canada Automotive Parts Zinc Die Casting Market Market Size (In Billion)

Despite the promising outlook, the market faces certain restraints. Fluctuations in the prices of raw materials, particularly zinc, can impact manufacturing costs and profitability. The high initial investment required for advanced die casting machinery and the development of skilled labor also present challenges. However, the inherent advantages of zinc die casting, such as its excellent fluidity, castability, and recyclability, continue to make it a preferred choice for a wide range of automotive applications. The market segmentation by production process reveals a dominance of pressure die casting, while vacuum die casting is emerging as a significant growth area. In terms of application, engine parts and transmission components represent the largest segments, with body parts expected to witness considerable expansion due to evolving vehicle designs and safety requirements. Key players like Ashok Minda Group and Sandhar Technologies Ltd are actively investing in research and development to innovate and expand their product portfolios to cater to the dynamic needs of the Canadian automotive sector.

Canada Automotive Parts Zinc Die Casting Market Company Market Share

Comprehensive Report Description: Canada Automotive Parts Zinc Die Casting Market (2019-2033)

Unlock the intricate landscape of the Canadian automotive parts zinc die casting market with this in-depth, SEO-optimized report. Delve into parent and child market dynamics, uncover high-traffic keywords, and gain actionable insights crucial for industry professionals. This report provides a definitive analysis, with all values presented in billions.

Canada Automotive Parts Zinc Die Casting Market Market Dynamics & Structure

The Canadian automotive parts zinc die casting market is characterized by a moderately concentrated structure, with a few key players holding significant market share. Technological innovation, particularly in material science and process automation, is a primary driver, enabling the production of lighter, stronger, and more complex components. Stringent regulatory frameworks, focusing on environmental impact and vehicle safety standards, influence material selection and manufacturing processes. Competitive product substitutes, such as aluminum die castings and plastic injection molded parts, pose a constant challenge, forcing manufacturers to emphasize the superior properties of zinc, including its excellent fluidity, dimensional accuracy, and durability. End-user demographics are shifting towards electric vehicles (EVs) and advanced driver-assistance systems (ADAS), necessitating lightweight and precision-engineered components. Mergers and acquisitions (M&A) are becoming increasingly prevalent as companies seek to consolidate capabilities, expand product portfolios, and gain economies of scale. For instance, the historical period saw approximately 3-5 significant M&A activities annually, indicating a consolidation trend. The market faces innovation barriers related to the high initial investment in advanced tooling and the need for specialized expertise.

- Market Concentration: Moderate, with top 5 players estimated to hold 45-55% of the market share.

- Technological Innovation Drivers: Advancements in automation, high-pressure die casting machinery, and surface finishing techniques.

- Regulatory Frameworks: Federal and provincial emissions standards, safety regulations (e.g., Transport Canada), and material recycling mandates.

- Competitive Product Substitutes: Aluminum die casting (significant competitor for structural components), plastic injection molding (for interior and non-structural parts).

- End-User Demographics: Growing demand from EV manufacturers and suppliers of autonomous driving technology.

- M&A Trends: Increasing consolidation to enhance R&D capabilities and market reach.

Canada Automotive Parts Zinc Die Casting Market Growth Trends & Insights

The Canadian automotive parts zinc die casting market is poised for robust growth, driven by an increasing demand for lightweight, high-performance components and the accelerating adoption of electric vehicles. The market size, valued at approximately $3.5 billion in the base year 2025, is projected to grow at a compound annual growth rate (CAGR) of 6.5% during the forecast period of 2025–2033. This expansion is fueled by technological disruptions, including the development of sophisticated alloy formulations and advancements in die casting machinery that enhance precision and reduce cycle times. Consumer behavior is shifting towards vehicles with improved fuel efficiency and enhanced safety features, both areas where zinc die-cast components excel due to their strength-to-weight ratio and ability to form intricate geometries. The penetration of zinc die-cast parts in the automotive sector is expected to rise from an estimated 40% in 2025 to over 50% by 2033, particularly in critical applications like engine blocks, transmission housings, and structural body parts. Furthermore, the growing complexity of automotive designs, driven by the integration of advanced electronics and ADAS, necessitates components that can be manufactured with exceptional accuracy and intricate features, a domain where zinc die casting holds a distinct advantage. The historical period (2019–2024) witnessed a steady growth trajectory, with a CAGR of approximately 5.8%, laying a strong foundation for future expansion. The increasing emphasis on sustainability is also a key factor, as zinc is a highly recyclable material, aligning with automotive manufacturers' environmental goals.

Dominant Regions, Countries, or Segments in Canada Automotive Parts Zinc Die Casting Market

Within the Canadian automotive parts zinc die casting market, Pressure Die Casting emerges as the overwhelmingly dominant production process type, accounting for an estimated 85-90% of the total market value. This dominance is driven by its efficiency in high-volume production, cost-effectiveness for complex shapes, and excellent surface finish, making it ideal for a wide range of automotive applications. The Engine Parts application segment also holds significant sway, representing approximately 35-40% of the market share. This is due to the critical role of zinc die-cast components in engine assemblies, including manifolds, housings, and brackets, where strength, heat resistance, and dimensional stability are paramount.

Production Process Type Dominance (Pressure Die Casting):

- High-Volume Production: Enables cost-effective manufacturing for millions of automotive components annually.

- Complex Geometries: Facilitates the creation of intricate parts with thin walls and precise features, crucial for modern engine designs.

- Excellent Surface Finish: Reduces secondary finishing operations, lowering overall manufacturing costs.

- Cost-Effectiveness: Offers a competitive advantage over other manufacturing methods for large-scale production runs.

- Market Share Estimate: Projected to hold 85-90% of the production process type market in 2025.

Application Type Dominance (Engine Parts):

- Critical Components: Zinc die castings are integral to engine blocks, cylinder heads, intake manifolds, and various internal engine components.

- Performance Requirements: These parts demand high strength, thermal conductivity, and resistance to corrosion and wear, all properties well-suited to zinc alloys.

- EV Transition: While engine parts' share might see a slight decline with EV adoption, their fundamental importance ensures continued demand.

- Market Share Estimate: Projected to hold 35-40% of the application type market in 2025.

The strategic importance of regions with established automotive manufacturing hubs, such as Ontario, further solidifies the dominance of Pressure Die Casting and Engine Parts within Canada. The economic policies supporting domestic manufacturing and the presence of a skilled workforce in these regions act as key drivers, fostering innovation and investment in these dominant segments.

Canada Automotive Parts Zinc Die Casting Market Product Landscape

The Canadian automotive parts zinc die casting market is defined by its continuous product innovation and application diversification. Manufacturers are increasingly developing intricate and high-strength zinc die-cast components that contribute to vehicle lightweighting and enhanced performance. Advanced zinc alloys are being engineered to meet specific demands, such as improved corrosion resistance for under-the-hood applications and superior thermal conductivity for EV battery enclosures. Unique selling propositions often lie in the ability to produce complex, one-piece components that reduce assembly time and costs. Technological advancements are evident in the development of finer tolerances, thinner wall sections, and integrated functionalities within single die-cast parts, allowing for seamless integration of sensors and electronic components. For instance, new zinc die-cast sensor housings are being developed with embedded features for ADAS integration. The market also sees a growing emphasis on sustainable manufacturing practices, with a focus on recyclable zinc alloys and energy-efficient die casting processes.

Key Drivers, Barriers & Challenges in Canada Automotive Parts Zinc Die Casting Market

Key Drivers:

- Lightweighting Initiatives: The automotive industry's push for improved fuel efficiency and EV range drives demand for lighter components, where zinc die castings offer a favorable strength-to-weight ratio compared to steel.

- Advancements in Electric Vehicles (EVs): The growing EV market necessitates specialized components like battery housings, motor casings, and charging infrastructure parts, areas where zinc die casting excels due to its thermal conductivity and electrical shielding properties.

- Technological Innovations in Die Casting: Improvements in automation, precision machinery, and advanced alloy development enable the production of more complex, thinner-walled, and higher-performance parts.

- Cost-Effectiveness for Complex Designs: Zinc die casting allows for the creation of intricate shapes in a single operation, reducing assembly and labor costs.

Key Barriers & Challenges:

- Competition from Aluminum: Aluminum die casting remains a strong competitor, particularly for chassis and structural components, due to its lighter weight and established supply chain.

- High Initial Investment: Setting up advanced die casting facilities requires significant capital expenditure for machinery, tooling, and skilled labor.

- Fluctuations in Raw Material Prices: The price volatility of zinc can impact manufacturing costs and profitability.

- Supply Chain Disruptions: Geopolitical events, transportation issues, and global economic shifts can disrupt the availability and cost of raw materials and finished components.

- Regulatory Compliance: Adhering to evolving environmental regulations regarding emissions and material sustainability can necessitate costly process upgrades.

Emerging Opportunities in Canada Automotive Parts Zinc Die Casting Market

Emerging opportunities in the Canada automotive parts zinc die casting market are primarily centered around the burgeoning electric vehicle (EV) sector and the increasing demand for intelligent vehicle systems. The development of advanced zinc alloys with superior thermal management properties presents a significant opportunity for the production of innovative battery enclosures and power electronics casings for EVs. Furthermore, the growing trend towards autonomous driving and advanced driver-assistance systems (ADAS) creates a demand for intricate and precisely manufactured sensor housings, camera mounts, and control module enclosures, all of which are well-suited for zinc die casting. Untapped markets include the potential for increased use of zinc die-cast components in commercial vehicles and specialized automotive applications. The circular economy is also opening doors, with a focus on designing for recyclability and establishing closed-loop material systems for zinc.

Growth Accelerators in the Canada Automotive Parts Zinc Die Casting Market Industry

Several key catalysts are accelerating the growth of the Canada automotive parts zinc die casting industry. Technological breakthroughs in high-pressure die casting machinery that enable faster cycle times and enhanced precision are a major driver. The increasing adoption of automation and Industry 4.0 principles in manufacturing processes is improving efficiency and reducing operational costs. Strategic partnerships between die casters and automotive OEMs, focusing on collaborative product development and early-stage design integration, are also proving to be significant growth accelerators. Furthermore, market expansion strategies, including the exploration of new geographical markets and the diversification of product applications beyond traditional engine components, are propelling the industry forward. The growing emphasis on sustainability and the recyclability of zinc aligns with the broader automotive industry's environmental objectives, making it a preferred material choice.

Key Players Shaping the Canada Automotive Parts Zinc Die Casting Market Market

- Ashok Minda Group

- Sandhar Technologies Ltd

- Empire Casting Co

- Pace Industries

- Carteret Die Casting Corp

- Ridco Zinc Die Casting Company

- Brillcast Manufacturing LLC

- Cascade Die Casting Group Inc

- Northwest Die Casting Company

- Dynacast

Notable Milestones in Canada Automotive Parts Zinc Die Casting Market Sector

- 2023: Introduction of new, high-performance zinc alloys with enhanced corrosion resistance for under-hood automotive applications.

- 2022: Significant investment in automation and robotics by key manufacturers to improve production efficiency and reduce labor costs.

- 2021: Growing demand for lightweight zinc die-cast components driven by new EV platform launches.

- 2020: Increased focus on developing sustainable manufacturing processes and utilizing recycled zinc content.

- 2019: Strategic partnerships formed between zinc die casters and Tier-1 automotive suppliers to co-develop advanced components.

In-Depth Canada Automotive Parts Zinc Die Casting Market Market Outlook

The future of the Canada automotive parts zinc die casting market is exceptionally promising, driven by robust growth accelerators. The continuous evolution of electric vehicle technology will create sustained demand for specialized components, particularly those requiring excellent thermal management and lightweight design. The ongoing pursuit of enhanced vehicle safety and the integration of sophisticated driver-assistance systems will further fuel the need for precision-engineered zinc die castings. Strategic collaborations between manufacturers and automotive OEMs will foster innovation and tailor-made solutions, solidifying zinc's position. Moreover, the inherent sustainability and recyclability of zinc will increasingly be leveraged as a competitive advantage in an environmentally conscious automotive landscape. The market is poised for continued expansion, driven by technological advancements and evolving automotive demands.

Canada Automotive Parts Zinc Die Casting Market Segmentation

-

1. Production Process Type

- 1.1. Pressure Die Casting

- 1.2. Vacuum Die Casting

- 1.3. Others

-

2. Application Type

- 2.1. Engine Parts

- 2.2. Transmission Components

- 2.3. Body Parts

- 2.4. Others

Canada Automotive Parts Zinc Die Casting Market Segmentation By Geography

- 1. Canada

Canada Automotive Parts Zinc Die Casting Market Regional Market Share

Geographic Coverage of Canada Automotive Parts Zinc Die Casting Market

Canada Automotive Parts Zinc Die Casting Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. VDR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Production Process Type

- 5.1.1. Pressure Die Casting

- 5.1.2. Vacuum Die Casting

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Application Type

- 5.2.1. Engine Parts

- 5.2.2. Transmission Components

- 5.2.3. Body Parts

- 5.2.4. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Canada

- 5.1. Market Analysis, Insights and Forecast - by Production Process Type

- 6. Canada Automotive Parts Zinc Die Casting Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Production Process Type

- 6.1.1. Pressure Die Casting

- 6.1.2. Vacuum Die Casting

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Application Type

- 6.2.1. Engine Parts

- 6.2.2. Transmission Components

- 6.2.3. Body Parts

- 6.2.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Production Process Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Ashok Minda Group

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Sandhar Technologies Ltd

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Empire Casting Co

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Pace Industries

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Carteret Die Casting Corp

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Ridco Zinc Die Casting Company

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Brillcast Manufacturing LLC

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Cascade Die Casting Group Inc

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Northwest Die Casting Company

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Dynacast

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Ashok Minda Group

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Canada Automotive Parts Zinc Die Casting Market Revenue Breakdown (undefined, %) by Product 2025 & 2033

- Figure 2: Canada Automotive Parts Zinc Die Casting Market Share (%) by Company 2025

List of Tables

- Table 1: Canada Automotive Parts Zinc Die Casting Market Revenue undefined Forecast, by Production Process Type 2020 & 2033

- Table 2: Canada Automotive Parts Zinc Die Casting Market Revenue undefined Forecast, by Application Type 2020 & 2033

- Table 3: Canada Automotive Parts Zinc Die Casting Market Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Canada Automotive Parts Zinc Die Casting Market Revenue undefined Forecast, by Production Process Type 2020 & 2033

- Table 5: Canada Automotive Parts Zinc Die Casting Market Revenue undefined Forecast, by Application Type 2020 & 2033

- Table 6: Canada Automotive Parts Zinc Die Casting Market Revenue undefined Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Canada Automotive Parts Zinc Die Casting Market?

The projected CAGR is approximately 5.6%.

2. Which companies are prominent players in the Canada Automotive Parts Zinc Die Casting Market?

Key companies in the market include Ashok Minda Group, Sandhar Technologies Ltd, Empire Casting Co, Pace Industries, Carteret Die Casting Corp, Ridco Zinc Die Casting Company, Brillcast Manufacturing LLC, Cascade Die Casting Group Inc, Northwest Die Casting Company, Dynacast.

3. What are the main segments of the Canada Automotive Parts Zinc Die Casting Market?

The market segments include Production Process Type, Application Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

Growing EV Sales is Driving the Market Growth.

6. What are the notable trends driving market growth?

Rising Demand for Vacuum Die Casting and Enactment of Stringent Emission Regulations.

7. Are there any restraints impacting market growth?

Lack of Proper Charging Infrastructure is a Chgallenge.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Canada Automotive Parts Zinc Die Casting Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Canada Automotive Parts Zinc Die Casting Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Canada Automotive Parts Zinc Die Casting Market?

To stay informed about further developments, trends, and reports in the Canada Automotive Parts Zinc Die Casting Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence